“Too many people spend money they haven’t earned, to buy things they don’t want, to impress people they don’t like.” — Will Rogers

In a consumer culture that equates success with spending, African America remains uniquely vulnerable. The historical denial of access to capital and economic agency has not merely constrained African Americans’ ability to accumulate wealth it has warped the cultural psychology of money itself, bending consumption from a utilitarian act into something closer to an identity claim. Now, a small but growing movement within the community is embracing a deliberate counteroffensive: minimalism. The philosophy is straightforward of less spending, less clutter, fewer financial obligations, and more intentional deployment of resources. But the more consequential question is whether this aesthetic and lifestyle ethos can be converted into a durable institutional strategy for wealth building, and whether the infrastructure exists to capture and redirect the capital it might free.

The structural context for this argument is more specific — and more damning — than the familiar headline figures suggest. African American household assets reached $7.1 trillion in 2024, a half-trillion-dollar increase that might appear encouraging at first glance. But the composition of that wealth exposes the mechanism of the problem: corporate equities and mutual fund shares, the asset class that generated the year’s fastest growth at 22.2%, represent less than 5% of African American holdings and a mere 0.7% of total U.S. household equity assets. The community is, in other words, almost entirely absent from the compounding wealth engine that most reliably converts income into intergenerational capital. On the liability side, consumer credit has surged to $740 billion, now representing nearly half of all African American household debt and approaching parity with home mortgage obligations of $780 billion, a near 1:1 ratio that represents a fundamental inversion of healthy household finance. For white households, the ratio stands at approximately 3:1 in favor of mortgage debt over consumer credit. The African American community stands alone in this precarious position. The debt itself flows almost entirely outward: with African American-owned banks holding just $6.4 billion in combined assets, the vast majority of $1.55 trillion in African American household liabilities flows to institutions outside the community, meaning that interest payments, fees, and the wealth-building potential of lending relationships are systematically siphoned away from Black-owned financial institutions. The historical dimension compounds the structural one. Black farmers owned more than 16 million acres of land in 1910; by 1997 they had lost more than 90% of it through state-sanctioned violence and discriminatory structures, a compounded loss estimated at $326 billion. From 1992 to 2002 alone, 94% of Black farmers lost part or all of their farmland, three times the rate at which white farmers lost land. What minimalism confronts, then, is not merely a spending habit. It is a balance sheet in structural retreat where African American households are asset-poor, debt-heavy, and systematically drained by the institutions that hold the debt.

Minimalism is not simply about having fewer possessions or a tidier apartment. It is a structural challenge to compulsive consumption. But for African Americans, consumption frequently functions as both a status signal and a psychological buffer. The legacy of economic exclusion has produced what some economists describe as compensatory consumption purchasing to claim affirmation in a society that has historically devalued Black presence. Designer goods become cultural armor. The latest consumer technology becomes a credential of arrival. Automobiles are more than vehicles; they are visible declarations of survival and dignity. This dynamic has its own historical coherence. In the early twentieth century, Harlem’s “Sunday Best” was less an act of religious observance than a form of public defiance, a counter-narrative to pervasive images of African American poverty and invisibility. The twenty-first-century iteration of that impulse has been systematically captured by brands whose ownership and supply chains are entirely removed from the community’s economic interests. To embrace minimalism, then, is to confront not only consumer capitalism but also the psychological architecture that colonialism and exclusion built. It demands a community-wide renegotiation of what economic success actually looks like and for whom it is being performed.

The utility of minimalism as a wealth-building mechanism is not merely philosophical it is arithmetically demonstrable. A household reducing monthly discretionary spending by five hundred dollars, through fewer restaurant meals, less fast fashion, and deferred consumer electronics, could redirect six thousand dollars annually into productive instruments: a college savings plan, a real estate investment trust with Black ownership, Treasury bonds for capital preservation, equity crowdfunding platforms supporting Black-led ventures, or a direct contribution to an HBCU endowment fund. Over a decade, with even modest returns, that redirected capital compounds into a six-figure investment position. Scaled across one million African American households practicing this discipline, the aggregate represents a wealth transfer of historic proportions initiated not by policy intervention or philanthropic rescue, but by the community’s own redirected consumption decisions. The distinction between compulsive and intentional spending is not a luxury concern. It is the difference between subsidizing someone else’s institutional power and building your own.

The most direct application of minimalism is also the most legible: the household balance sheet. A family that eliminates one financed vehicle and opts for a used purchase outright removes both a monthly payment and an interest obligation, freeing several hundred dollars a month that compound differently when redirected. Choosing a duplex over a single-family home and renting the second unit transforms the primary residence from a consumption asset into an income-producing one — the kind of structural move that converts homeownership from a wealth symbol into a wealth mechanism. Retirement contributions left at the employer match rather than maximized represent another form of consumption by inertia; households that treat the gap between the match ceiling and the IRS contribution limit as a monthly target are effectively building a tax-advantaged investment position that most never access. The same logic applies to life insurance: the difference between a term policy and a whole-life policy, redirected into an index fund over twenty years, is not a marginal decision. These are not sacrifices. They are reallocations — the substitution of visible, depreciating expenditure for invisible, compounding position-building. At scale, if HBCU alumni associations or community organizations created coordinated vehicles to receive and deploy this redirected capital — endowment contributions, community development financial institutions, Black-owned bank deposits — the household discipline becomes institutional fuel. But the household is where the discipline begins and where it is most immediately actionable.

Historically, African America has deployed its dollars as a political instrument. The Montgomery Bus Boycott extracted direct economic cost from a segregated transit system. The 2020 Blackout Day redirected consumer attention toward Black-owned businesses and away from corporations that profited from Black spending without reciprocal investment in Black communities. Minimalism extends this tradition into daily economic practice. It is a sustained withdrawal from the consumption patterns that extractive industries have engineered to capture Black income. Consumer surveillance capitalism studies African American spending behavior in granular detail, refining the advertising systems designed to push more debt, more aspirational luxury, and more financial dependency. Opting out methodically is not merely frugality — it is a form of information asymmetry disruption, denying data that feeds systems designed to work against Black institutional interests.

The objection that minimalism is a privilege of the already comfortable misreads the proposition. For lower-income households, intentional resource management is not a new concept — it is frequently a survival discipline already in practice. What is missing is not the behavior but the infrastructure to leverage it: institutions capable of receiving redirected capital, community platforms that make collective commitment visible and accountable, and frameworks that connect household choices to institutional outcomes. Minimalism as a communal strategy must also extend its frame of reference. Digital minimalism can reduce the tech dependency being engineered into younger generations at enormous cost to family finances. Food minimalism can recalibrate spending patterns distorted by food desert geography. Spatial minimalism can encourage shared community investment over the overcapitalized private home as the primary wealth vehicle. None of these requires material sacrifice — all of them require institutional infrastructure to translate reduced consumption into coordinated capital formation.

Minimalism will not, by itself, undo redlining, reverse discriminatory lending, or equalize inherited wealth. It is a tool, not a solution — one component of a coordinated institutional strategy that also requires political leverage, legal infrastructure, and sustained endowment growth. But it is a tool African America has yet to fully institutionalize. The community already possesses the spending mass. What it requires is the institutional architecture to redirect that mass with precision. The question is not whether African America can afford to consume less. The question is whether it can afford not to.

Land is the only thing in the world that amounts to anything, for it’s the only thing in this world that lasts. It’s the only thing worth workingfor, worth fighting for… – Ted Turner

Raw land is among the oldest and most durable asset classes available to private investors. For the HBCU community — individuals, families, alumni associations, and institutional partners — it is also among the most underutilized.

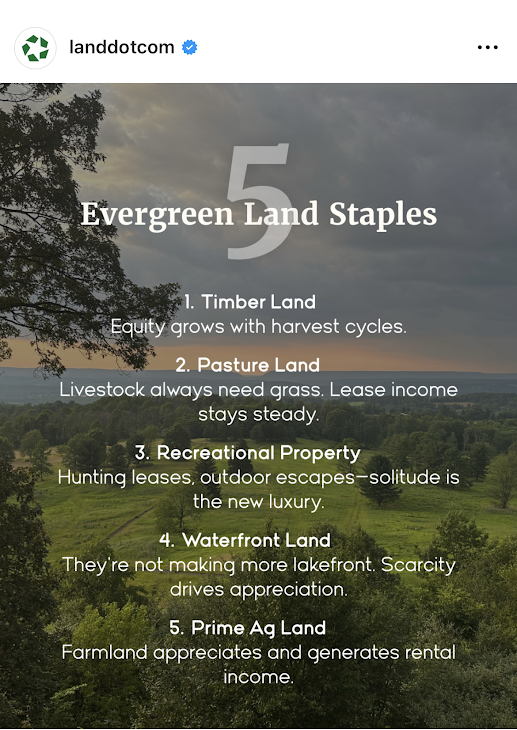

There is a social media post circulating in land investment circles that reads simply: “Forget the luck of the Irish. We prefer the certainty of a deed.” Beneath that caption sits a framework titled “5 Evergreen Land Staples” — timberland, pastureland, recreational property, waterfront land, and prime agricultural ground — each chosen for the same fundamental quality: enduring income or appreciation that does not require the daily volatility management of equities or the tenant fragility of residential real estate. The post is from Land.com, a mainstream marketplace catering primarily to rural landowners. The audience it implicitly addresses is white, rural, and generationally landed. Yet the analytical framework it articulates is precisely what the African American institutional ecosystem needs to operationalize and the HBCU community, with its networks of graduates, alumni chapters, and anchor institutions spread across the American South and beyond, is uniquely positioned to execute it at scale.

The stakes are not trivial. As the Federation of Southern Cooperatives Land Assistance Fund has documented, African Americans own less than 1% of all privately owned rural land in the United States. That figure represents one of the most consequential economic collapses in modern American history, a loss that accelerated across the 20th century through discriminatory lending, heirs’ property dispossession, and the systematic exclusion of Black farmers from federal agricultural credit systems. Between 1910 and 2020, African American land ownership fell by roughly 90%, from an estimated 15–16 million acres to less than 2 million today. Reversing even a fraction of that trajectory requires not only individual decision-making but coordinated institutional action. This article maps a practical framework anchored in the five evergreen land categories for how African Americans at every life stage, and HBCU-affiliated institutions at every organizational level, can begin to build durable land portfolios through structures that keep capital inside the ecosystem.

Before addressing who should invest and how, it is worth establishing why the five categories on that social media post represent genuinely strategic holdings rather than speculative fashions. Timberland is distinctive because its primary asset — standing timber — continues growing in value as long as it stands. As one institutional investor noted at the 2009 Timberland Investment World Summit, timber was the only major asset class not to decline during the Great Recession: “As long as the sun is shining trees will grow and your timber’s value will increase.” For long-horizon investors, which includes endowments, alumni foundations, and family trusts, timberland offers inflation protection, biological growth as a return mechanism, and periodic harvest income that can be timed to liquidity needs. Pastureland generates recurring lease income from ranchers and livestock operators with relatively low management overhead, while the underlying land appreciates over time and the lessee carries operational risk. For a first-generation land investor or a young family with limited bandwidth for active management, a leased pasture parcel generates cash flow from day one. Recreational property, including hunting and fishing grounds, has benefited from the structural shift toward experiential consumption, outdoor recreation spending in the United States now exceeds $780 billion annually and the demand for private access through leased hunting rights or short-term rentals has made rural recreational parcels a viable income source even at modest scale. Waterfront land commands a persistent scarcity premium, as lakefront, riverfront, and coastal parcels face an absolute supply constraint that no amount of construction can remedy, with appreciation rates for quality holdings historically outpacing inland equivalents by substantial margins. Prime agricultural land, the fifth category, combines appreciation and income in proportions that no other asset class consistently replicates, with farmland producing positive real returns in nearly every decade since World War II while the growing global demand for food production adds a structural tailwind that shows no sign of abating.

For the African American individual investor, particularly recent HBCU graduates entering the workforce, raw land is rarely the first investment that financial advisors recommend. Equities, retirement accounts, and residential real estate occupy the conventional hierarchy. This is understandable but strategically incomplete. Raw land, particularly rural parcels in the 10–100 acre range, is far more accessible in price terms than most urban professionals realize. In many parts of the rural South and Midwest, quality pastureland or timberland can be acquired for $1,500–$4,000 per acre, meaning a 20-acre parcel may require a down payment comparable to what urban renters spend in twelve months on housing. The critical discipline for individual investors is to treat the first land acquisition not as a lifestyle purchase but as a strategic asset. A 20-acre timberland parcel generates modest income while the timber matures but builds balance sheet equity that can later be pledged as collateral for subsequent acquisitions, a mechanism that generationally landed families have used for centuries. The key to making this work is choosing land that produces some income immediately, whether through a hunting lease, a hay-cutting arrangement, or a grazing license, so that carrying costs do not exceed cash flow while long-term appreciation accrues. Structurally, individuals should acquire rural land through a single-member LLC rather than in personal name, for both liability protection and eventual transfer efficiency. The LLC structure also allows for the clean addition of family members as equity holders over time, laying the legal groundwork for the next stage of ownership.

A young family with children faces a different calculus than a single investor. The time horizon extends to 30 or 40 years, the need for tax-efficient transfer becomes relevant, and the question of heirs’ property known as the informal, undivided ownership arrangement that has caused the dispossession of millions of acres of Black-owned land must be proactively addressed from the first deed. Heirs’ property arrangements leave undivided interests in land vulnerable to partition sales, through which any one heir can force a sale often to outside buyers at below-market prices. A young family acquiring land today should structure the purchase inside a family LLC or land trust from inception, with a clear operating agreement specifying decision-making rights, buyout provisions, and management authority. This structural discipline costs several hundred dollars in legal fees at formation but eliminates the single greatest mechanism by which Black-owned land has historically been lost. For young families, pastureland and prime agricultural ground are the most suitable of the five categories. Leased to a working farmer on an annual or multi-year cash rent arrangement, these parcels generate predictable income typically $100–$300 per acre annually in productive regions while the family’s equity compounds. Agricultural land near HBCUs, particularly the 1890 land-grant institutions with active extension programs, offers an additional advantage: the university’s agronomic and soil science resources can improve the land’s productivity and rental value over time, particularly where a formal university-farmer partnership exists.

For African American households in the wealth-accumulation or pre-retirement phase, typically those between 45 and 65 with existing equity in residential real estate or retirement accounts, raw land fills a specific portfolio gap. It provides non-correlated returns, inflation protection, and estate planning flexibility that equity-heavy portfolios lack. At this stage, the five-category framework can be pursued more deliberately. Waterfront land and timberland, which require longer holding periods to realize full appreciation, are most appropriate for mature investors who do not need near-term liquidity. A modest timber holding, held for 20 years through a managed investment timberland organization, can produce both periodic harvest income and terminal land value appreciation that substantially outpaces a bond portfolio over the same horizon. Conservation easements on qualifying land parcels offer an additional mechanism: by granting a qualified land trust a permanent easement that restricts development, the landowner receives a federal income tax deduction equal to the value of the development rights surrendered, a tool that high-income African American professionals have underutilized relative to white rural landowners who have deployed it extensively. This is also the stage at which entry into private Real Estate Investment Trust structures becomes viable. A private REIT organized around agricultural or timberland holdings allows a group of accredited investors like friends, family members, or professional associates to pool capital into a formal investment vehicle with a shared land portfolio, professional management, and pass-through tax treatment. Unlike publicly traded REITs, a private land REIT can be sized for a community of 10–50 investors, managed by a professional trustee, and built specifically around the five evergreen categories. The formation cost is meaningful but amortizes quickly across the investor pool, and the structure creates a formal institutional container for what would otherwise remain fragmented individual decisions.

Not every land investment begins with a formal institutional structure. Some of the most durable private wealth in America was built by small groups of trusted individuals such as former college roommates, fraternity and sorority members, professional cohort peers who pooled capital informally before any institution took notice. For the HBCU community, this peer-to-peer investment model is both historically familiar and structurally underdeployed. A group of five former classmates, each contributing $10,000, creates a $50,000 acquisition fund. In rural land markets across the South, that capital is sufficient to purchase 15–30 acres of quality pastureland or recreational property with room for closing costs and an operating reserve. The land is titled inside a jointly owned LLC, the operating agreement governs decision-making and buyout rights, and the group begins building a shared balance sheet that none of them could have assembled individually on the same timeline. The social infrastructure already exists. HBCU alumni networks are among the most tight-knit in American higher education, and the bonds forged between classmates across Greek organizations, residence halls, student government, and athletic programs carry the relational trust that small investment partnerships require above all else. What is missing is not the social capital but the financial framework to convert it into land equity. The practical steps are straightforward: the group agrees on an investment policy covering land category, geographic focus, minimum hold period, and income distribution schedule; forms an LLC with an operating agreement drafted by a real estate attorney; designates a managing member responsible for vendor relationships, lease management, and annual reporting; and commits to a first acquisition within a defined timeframe, preventing the initiative from dissolving into indefinite planning. Over time, these peer land partnerships can grow through reinvested income, additional capital calls, and the addition of new members at formally appraised entry valuations. A group that begins with five classmates and 25 acres can, within a decade of disciplined reinvestment, hold a diversified portfolio spanning multiple land categories across several states anchored not by institutional mandate but by the simple decision of like-minded people to build something together.

HBCU alumni associations sit at the intersection of institutional loyalty and latent investment capital. Most chapters hold reserve funds that have been accumulated through dues, fundraising, and event revenue that are parked in bank accounts earning negligible interest. Very few chapters have formalized investment policies, and this represents one of the most tractable missed opportunities in the HBCU ecosystem. An alumni chapter with $200,000 in reserves can, with proper legal structuring, become a founding limited partner in a private land REIT or a land investment LLC alongside other chapters. Five chapters pooling $200,000 each creates a $1 million acquisition fund capable of purchasing 250–500 acres of quality pastureland, timberland, or agricultural ground in rural markets adjacent to HBCUs. That land, leased and managed professionally, generates annual income that returns to the chapters while the underlying asset appreciates. Over a 15-year horizon, the portfolio can be refinanced to fund new acquisitions replicating the leverage cycle that institutional endowments have used with alternative assets for decades. The governance structure matters enormously. An alumni land partnership should be organized as a limited partnership or private REIT with an independent general partner or trustee, clear investment policy statements, annual audited financial statements, and a defined liquidity event horizon. The informality that characterizes most alumni chapter finances is incompatible with institutional land ownership at scale. But with proper structuring, the alumni network becomes what it has always had the potential to be: a distributed institutional investor class with shared objectives and collective bargaining power. Nationally coordinated alumni associations, the general alumni bodies of the major HBCU systems, are positioned to act at an even larger scale. A national alumni association with 50,000 dues-paying members and a modest per-member investment program could capitalize a seven-figure land acquisition fund within a single fiscal year. Structured as a private REIT with a land-grant mission overlay, specifically acquiring land adjacent to 1890 HBCU campuses or in counties with high concentrations of African American agricultural heritage, such a fund would generate financial returns while simultaneously reinforcing the geographic and economic footprint of the institutions themselves.

The structure of land acquisition matters as much as the acquisition itself, and for the African American investor at every level — individual, family, peer partnership, or alumni association — the financing institution is a strategic choice, not merely a transactional convenience. African American-owned banks hold just $6.4 billion in assets, while African American credit unions hold $8.2 billion, meaning these institutions together control less than $15 billion in combined lending capacity despite serving a market of more than 40 million people — insufficient to exert meaningful influence in national credit markets without deliberate capital infusion from within the community itself. When an African American investor finances a land purchase through a Black-owned bank or credit union rather than a mainstream white-owned lender, the mortgage deposit strengthens that institution’s liquidity ratio, expands its lending capacity through fractional reserve multiplication, and keeps the interest income circulating within the ecosystem rather than exiting to a Wall Street balance sheet. Every dollar deposited into an African American financial institution can translate into multiples of additional lending capacity once multiplied through the banking system — meaning that the collective financing decisions of HBCU alumni and community investors are not merely personal financial choices but acts of institutional capitalization. A community that builds land equity through Black-owned financial institutions simultaneously strengthens two pillars of its economic architecture: the land base that generates long-term wealth and the banking infrastructure that finances the next generation of acquisition.

At the institutional tier, the strategic imperative is even more pronounced. As of 2014, Tuskegee University controlled approximately 5,000 acres, ranking 12th among all American colleges in total land holdings, while Alabama A&M (2,300 acres), Alcorn State (1,756 acres), Prairie View A&M (1,502 acres), Kentucky State (915 acres), and Southern University (884 acres) collectively controlled more than 12,000 acres, placing all six among the top 100 college landowners in the United States. Those figures have not been comprehensively updated in the intervening decade, and the actual current land position of these institutions accounting for acquisitions, dispositions, and reclassifications likely differs. What has not changed is the strategic imperative to treat that land base as a productive investment asset rather than passive institutional real estate. A coordinated commitment of $1 million from each of the nineteen 1890 land-grant HBCUs would create a $19 million revolving fund capable, through its placement in African American banks and credit unions, of generating $7–$10 in agricultural lending capacity for every dollar committed financing not just land acquisition but the full productive cycle of African American farming. That mechanism addresses credit access. The complementary challenge is equity accumulation: deploying HBCU endowment capital, alongside alumni and friends’ capital, into the five evergreen land categories through a structured private REIT. An HBCU-anchored land REIT, capitalized with institutional endowment commitments as the senior tranche and alumni association and individual investor capital as subordinate tranches, would create a properly tiered investment structure with aligned incentives. The endowment’s priority return on its senior capital is protected; alumni investors participate in the upside above that hurdle; and the land itself remains in community-aligned ownership regardless of which investor class holds primacy at any given moment. Over time, the REIT’s land holdings can be diversified across all five evergreen categories — timberland for long-horizon appreciation, pastureland and agricultural ground for current income, waterfront parcels for high-appreciation positioning, and recreational property for near-term income generation — creating a portfolio whose income streams are non-correlated and whose asset values compound independently of equity market cycles.

The five evergreen land categories are individually sound investment ideas. Their strategic power for the HBCU community, however, lies not in isolated individual transactions but in the construction of a layered, coordinated ecosystem from the 22-year-old HBCU graduate purchasing her first 20-acre pasture parcel in Alabama, to the alumni chapter launching a multi-state agricultural REIT, to the 1890 HBCUs deploying endowment capital as the institutional anchor of a Black-managed timberland fund. At the most fundamental level, virtually every economic system man has ever created relies on one undeniable truth: whoever controls the land controls the system. The African American institutional ecosystem has the networks, the talent, and increasingly the structured financial vehicles to re-enter land ownership at meaningful scale. What it requires now is the strategic coordination to treat land not as a nostalgic aspiration but as a compounding institutional asset — one deed, one acre, one fund at a time.

Disclaimer: This article was assisted by ClaudeAI.

“The most important investment you can make is in yourself.” – Warren Buffett

There is a financial contradiction embedded in the romantic lives of African Americans that most personal finance commentators decline to address directly, because addressing it directly is uncomfortable. The contradiction is this: African Americans, as a group, occupy the most economically precarious position of any major demographic in the United States, which makes the cost of courtship a genuine strategic burden — and yet marriage, and the household formation it produces, remains one of the most powerful wealth-building mechanisms available to individuals operating without inherited capital. African Americans cannot afford to date the way the broader culture has normalized dating. And they cannot afford not to.

This is not a romantic observation. It is an institutional and economic one, and it deserves to be examined as such.

The arithmetic is brutal when you sit with it. According to a February 2025 survey by BMO Financial Group, the average American adult spends $2,279 on dates per year, with the all-in cost of a single date from pre-date grooming to gas money estimated at nearly $168. At one date per week, that annualized figure climbs well past $8,700. Set that against an African American median household income that, per the most recent Census data, sits at roughly $52,000 — still last among all major ethnic groups — and courtship is consuming somewhere in the range of 16 to 17 percent of African American median income. No other major demographic group faces that proportional burden. The cumulative cost is not simply personal; it is communal, because money extracted from the African American household through consumption-oriented dating is money that does not compound, does not build equity, and does not circulate within Black institutional ecosystems.

The crisis is compounded by employment fragility. African American men between the ages of 20 and 24 have historically carried unemployment rates roughly double those of their white male peers and these are the years during which romantic partnerships form with the most frequency and social intensity, and also the years of maximum economic vulnerability for the demographic most burdened by the cultural expectation of financing courtship. The collision of maximum relational pressure and minimum economic stability is not accidental. It is structural, and the consequences of navigating it poorly leading to the accumulating debt in pursuit of performed affluence, or deferring the relational investments that ultimately build household wealth reverberate for decades.

What is rarely said plainly enough is that courtship itself, when conducted without financial discipline, functions as a form of capital extraction. Every dollar spent performing prosperity in a relationship like the unnecessary dinner, the performative gift, the vacation financed on credit is a dollar transferred out of a community already operating with the thinnest capital base in the country. The African American community has constructed, over generations, a rich institutional infrastructure: HBCUs, Black-owned financial institutions, fraternities and sororities, professional associations, religious organizations, and community development organizations. The health of that infrastructure depends, at its foundation, on the accumulation of wealth within African American households. Romance, conducted poorly, undermines that foundation directly.

And yet the opposite error of treating financial precarity as a reason to defer relational commitment indefinitely is equally destructive, and arguably more so at the institutional level. Marriage, sociologists have long established, is not merely a romantic arrangement. It is the primary non-institutional mechanism through which ordinary Americans build wealth. The two-income household produces compounding effects on savings capacity that single-income households simply cannot replicate. The married couple that directs dual incomes toward an investment portfolio, a property, a business capitalization, or a child’s education produces generational effects that individual accumulation, however disciplined, rarely matches. Economists studying the racial wealth gap have identified the marriage rate differential between African Americans and other groups as one of the structural contributors to the persistence of that gap not because marriage is morally superior to other arrangements, but because household formation is a capital formation mechanism, and lower rates of stable household formation mean lower rates of capital accumulation across the community.

The data on African American marriage rates is now well established. Black Americans marry at lower rates than any other major demographic group in the country, and those who do marry do so later. The causes are multiple and structural with high male incarceration rates, chronic unemployment disparities, elevated student debt burdens concentrated among Black women who have simultaneously outpaced Black men in educational attainment but the consequences operate as a compounding disadvantage. Every generation that forms fewer stable households is a generation that produces less transferable wealth. Every household that dissolves under financial stress and financial incompatibility remains among the most commonly cited causes of relationship dissolution is a household that fails to produce the institutional legacy it might have otherwise built.

The tension, then, is genuinely bilateral. Dating as currently practiced by too many African Americans is financially unsustainable and institutionally corrosive. But the instinct to disengage from romantic partnership altogether, whether from economic discouragement or cultural frustration, forfeits the most accessible wealth-building mechanism available to people without inherited capital. The resolution of this tension is not a lifestyle choice. It is a strategic discipline.

What that discipline requires, practically, begins with a fundamental reorientation of what courtship is for. In the broader American consumer culture, dating has been commodified into a performance, a sequential escalation of expenditure designed to signal value, demonstrate seriousness, and compete for desirability. That model was designed for, and is subsidized by, demographics with higher income floors and different capital structures. African Americans who adopt it wholesale are importing a financial logic that was never calibrated for their economic reality. The more productive frame is to understand courtship as what it has always been, beneath the cultural noise: an evaluation of partnership potential. The question that dating should answer is not who can perform affluence most convincingly but who can build alongside you most effectively.

The previous guidance this publication offered to HBCU men to be honest about your finances, maintain an emergency fund scaled to the specific vulnerability of African American employment, set expectations within a budget rather than beyond it, and resist the conflation of income with wealth remains sound, but it is incomplete if read only as personal financial advice. Its deeper implication is institutional. The man or woman who enters a serious relationship without financial honesty, without emergency reserves, and without a clear orientation toward asset accumulation is not simply making a personal error. They are entering a partnership that is structurally likely to fail under economic stress, and the failure of that partnership will remove another household from the African American wealth-building ecosystem. The stakes are communal, not merely personal.

The same logic applies to partner selection. This is a dimension of the conversation that cultural politeness often forecloses, but institutional analysis cannot afford to ignore. The choice of a romantic partner is, among other things, a capital allocation decision. A partnership between two individuals who are aligned on financial values, who are both oriented toward asset accumulation rather than consumption performance, and who are capable of the financial transparency that stable households require, produces outcomes that misaligned partnerships simply do not. The HBCU graduate who selects a partner based on emotional chemistry while ignoring or minimizing financial incompatibility is not being romantic they are being strategically imprecise about one of the most consequential decisions they will make. Given the compounding nature of household economics, imprecision here has long time horizons.

This is not an argument for mercenary partnership or the subordination of genuine affection to spreadsheet optimization. It is an argument that the dichotomy between romance and financial strategy is false, and that maintaining it as if it were real is a luxury African Americans, as a community, cannot afford. Other communities have understood for generations that courtship and institutional continuity are related phenomena. The institution of marriage among Jewish American families, which social scientists have identified as one of the structural contributors to that community’s remarkable intergenerational wealth transfer, is not simply an artifact of religious tradition. It is reinforced by a dense network of institutional expectations, community norms, and financial literacy frameworks that treat household formation as a community-level priority rather than a purely private one. The same patterns, in different cultural registers, appear in other communities that have achieved disproportionate wealth accumulation relative to their initial American circumstances.

African American institutions such as HBCUs, fraternities, sororities, religious organizations, professional associations have the capacity to play this coordinating role. The HBCU campus, which has historically served not merely as an educational institution but as a marriage market and professional network, is an underutilized asset in this regard. When two HBCU graduates form a household, they are not just creating a family. They are activating a set of institutional networks, alumni relationships, professional associations, and community commitments that have real capital value. When that household builds wealth, and directs that wealth through Black-owned financial institutions, invests in Black-owned enterprises, and contributes to HBCU endowments, it completes a capital circulation loop that strengthens the entire ecosystem. The household is not the end of the story. It is the seed of a much larger institutional project.

But the institutional infrastructure currently available to support that project is insufficient to the scale of the problem. Providing personal finance guidance to individual graduates, or hosting mixers within existing alumni networks, addresses symptoms rather than causes. What is actually required are new institutions purpose-built to treat relationship formation and household financial stability as interconnected civic priorities and the African American community is now beginning to conceptualize what those institutions might look like.

One framework that has emerged from this conceptual work is the proposed Ossie Davis and Ruby Dee Trust, a nonprofit structure designed to treat Black relationship formation as essential civic infrastructure. Rather than addressing individual behavior, it embeds an Institutional Matchmaking Network inside existing Black institutions such as HBCUs, Black Greek-letter organizations, and Black professional societies organizing participants into cohorts around values alignment and life stage rather than the transactional logic of dating apps. Institutional partners would be evaluated not by attendance but by households formed over time. Alongside this, the Trust’s proposed Black Marriage Economic Stabilization Fund directly attacks the structural barriers to marriage formation: student loan interest relief for married participants, down payment matching grants, emergency household stabilization funds, and cooperative legal planning tools. If society subsidizes corporate capitalization through tax structures and preferential credit, there is no principled argument against subsidizing household formation among the demographic most systematically denied access to those same structures.

A second emerging framework addresses what enters the household economically at the moment of formation. The proposed HBCU Alumni Trust would provide every HBCU graduate, at graduation, with a beneficial interest in a professionally managed irrevocable trust generating monthly income distributions for life, with 75 percent accessible and 25 percent mandatorily reinvested, and underlying assets protected by spendthrift provisions for a ten-year vesting period. Its purpose is not primarily about returns. It is about changing the conditions under which graduates enter the courtship market. A graduate carrying a monthly income stream is a categorically different actor than one entering post-graduation life with $40,000 in student debt and no liquidity buffer less likely to perform prosperity they do not possess, less likely to make partnership decisions driven by economic desperation, and more likely to be the kind of financially stable partner around whom a wealth-building household can actually be built.

The version of dating that is making African Americans broke, therefore, is not simply an individual failure of financial discipline. It is a community failure to have built and sustained the normative frameworks, the matchmaking infrastructure, and the financial tools within which courtship is understood as institutional preparation rather than consumption performance. Young African Americans inherit a culture of dating that was not designed with their economic realities or institutional interests in mind. The Ossie Davis and Ruby Dee Trust, the HBCU Alumni Trust, and the broader institutional imagination they represent are attempts to change that inheritance not through cultural policing or moral instruction, but through the construction of institutions that make the financially disciplined, partnership-oriented approach to courtship the path of least resistance rather than the path of greatest sacrifice.

The calculation, ultimately, is not whether African Americans can afford to date. They can, if they do it with discipline, honesty, and a clear-eyed understanding of what partnership is for. The calculation is whether African Americans can afford to continue treating courtship as a consumption category rather than a capital formation strategy and whether the institutions that serve African American life are willing to accept responsibility for building the infrastructure that makes the difference. The evidence of seven decades of compounding wealth gaps suggests, emphatically, that they cannot afford the former. The emergence of institutional frameworks designed to address the structural conditions of Black household formation suggests, cautiously, that some are beginning to accept the latter.

Disclaimer: This article was assisted by Claude AI.

This here, right now, at this very moment, is all that matters to me. I love you. That’s urgent like a motherf**ker. – Darius Lovehall

There is a particular kind of magic that happens when Black people are given the space to simply be to lead, to create, to fail and succeed without the exhausting weight of being a perpetual outsider. Historically Black Colleges and Universities have always understood this. For more than 150 years, HBCUs have offered something that no diversity initiative, no DEI task force, and no affinity group within a predominantly white institution can fully replicate: an entire ecosystem built in, by, and for Black people. The effects of that ecosystem ripple outward in ways we are still measuring including into who HBCU alumni choose to build their lives with.

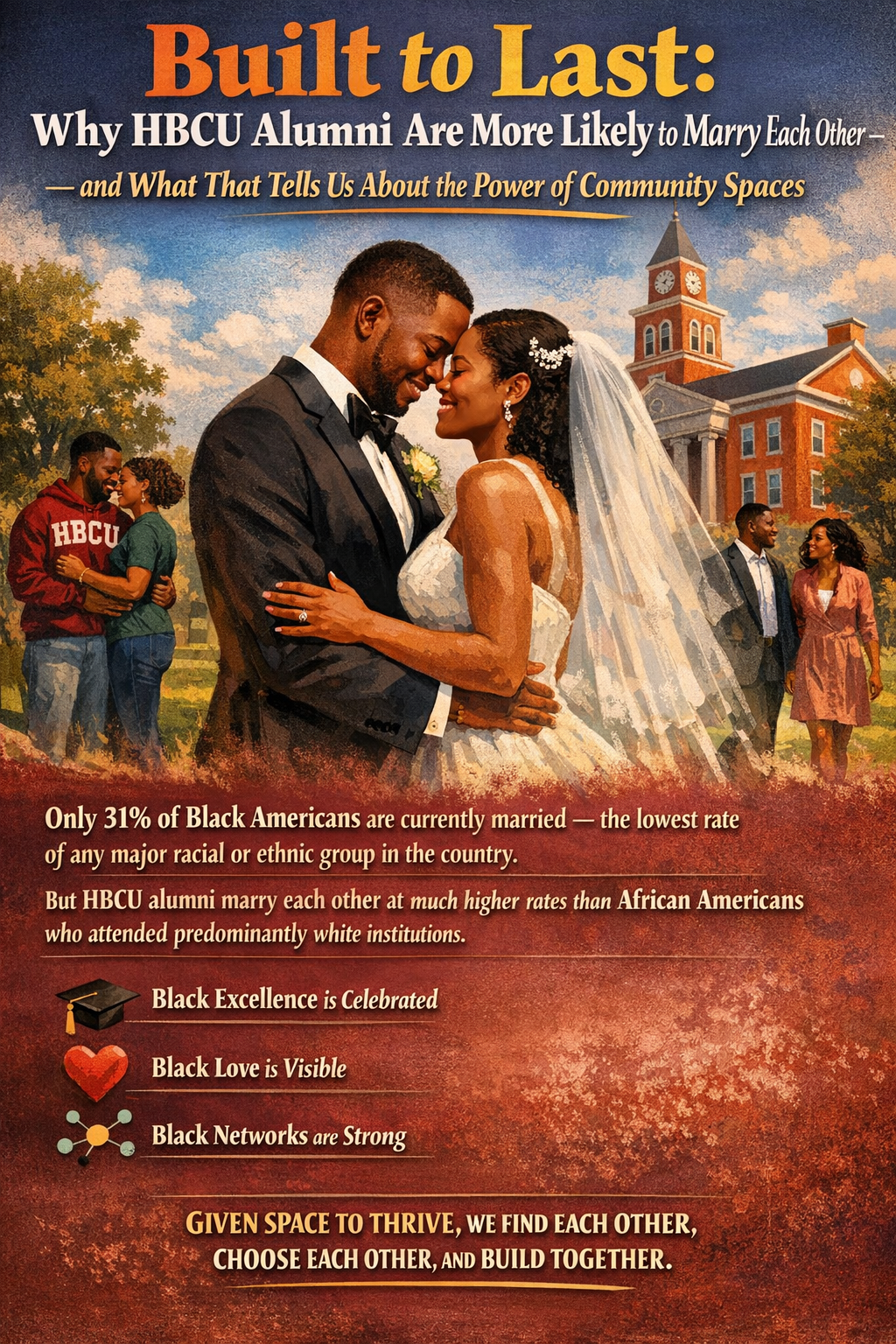

Research into the marital patterns of African Americans reveals a striking divergence between HBCU graduates and their counterparts who attended predominantly white institutions. HBCU alumni marry each other — Black men marrying Black women, Black women marrying Black men at significantly higher rates than African Americans who attended PWIs, where interracial marriages are considerably more common. This is not a coincidence. It is the natural fruit of what intentional community spaces produce.

The baseline numbers are sobering. Only 31% of Black Americans are currently married, compared to 48% of all Americans. Half of African Americans have never been married, compared to 34% of the general population, making African Americans the least married of any major racial or ethnic group in the country. There are approximately 5.18 million Black married-couple families in the United States today. That number has room — significant room — to grow. Currently, about 9–10% of Black college students attend HBCUs. Among college-educated Black newlyweds at PWIs, roughly 21% marry someone from another racial or ethnic group, with that figure rising to 30% among college-educated Black men. The picture at HBCUs is markedly different, and the reasons are structural, not accidental.

The social architecture of an HBCU where Black students are the majority, the leadership, the faculty, the homecoming court, the engineering honor society, and the debate team means that the romantic world reflects the academic world. HBCU alumni who marry are overwhelmingly likely to have met their spouse within a Black social and professional network, often one that traces its roots directly back to campus. African Americans who attend PWIs, by contrast, are exposed to a social universe numerically and institutionally dominated by white peers. Friendships, romantic relationships, and professional networks form disproportionately across racial lines not through any individual fault, but as a straightforward consequence of who is in the room. When your environment is 85% white, the statistical likelihood of cross-racial coupling rises organically. The HBCU alumni network functions, among other things, as a long-running and remarkably effective matchmaking institution one whose impact on community formation has never been fully quantified.

Sociologists have long understood that residential and institutional proximity is one of the strongest predictors of who people marry. We meet our partners in the spaces we inhabit — at work, at school, in our neighborhoods, at our houses of worship. The institution you attend for four formative years, the one that shapes your professional ambitions, your intellectual identity, your social circle, and your sense of self, will inevitably shape who you consider a natural life partner. For HBCU students, those four years are spent in an environment where Black excellence is not exceptional it is expected. Where Black love is not a political statement but a daily reality, visible in the couples holding hands on the quad, in the married faculty members co-teaching courses, in the alumni couples who return to homecoming year after year. Love, like ambition and leadership, is modeled. Young people see what is possible and, consciously or not, begin to orient their own futures accordingly.

PWI environments, for all their academic prestige, rarely offer this. Black students at PWIs often describe a bifurcated social experience belonging to affinity groups and cultural organizations that provide community, while simultaneously navigating a broader campus culture in which they are the minority. Black love is possible at PWIs, of course, and it flourishes there too. But the structural conditions do not make it the default. They make it something you find in spite of your environment, not because of it.

This conversation extends well beyond marriage rates, though those rates are a particularly measurable indicator of something larger. What HBCUs demonstrate is the transformative power of institutions that a community owns, shapes, and sustains for itself. This principle has animated Black institution-building in America since Reconstruction from Black Wall Street in Tulsa to the network of Black-owned banks, newspapers, hospitals, and churches that constituted what historians call the “Black counterpublic.” When a community has its own institutions, it controls its own narratives. It defines its own standards of beauty, intelligence, leadership, and desirability. It produces its own role models, generates its own wealth pathways, and creates an internal ecosystem dense enough that community members can meet each other’s needs — economic, social, spiritual, romantic — without having to seek fulfillment exclusively in outside spaces. The higher intra-community marriage rate among HBCU alumni is one data point in a much larger argument: that Black institutions do not merely provide education or services. They produce belonging. And belonging, once cultivated, has a way of reproducing itself in careers built together, in communities sustained together, and in families formed together.

For a publication dedicated to the intersection of Black financial life and Black excellence, the marriage data carries specific economic weight. Marriage, when it functions well, is one of the most powerful wealth-building vehicles available to any household. Two incomes, shared expenses, combined assets, coordinated estate planning, and intergenerational wealth transfer — these are the mechanisms by which families accumulate and maintain economic stability across generations. The racial wealth gap in the United States is staggering and persistent. For Black families to close that gap through their own accumulated power, marriage stability within the community matters. When HBCU alumni marry each other, they are pooling Black wealth with Black wealth building households that invest in Black communities, buy homes in Black neighborhoods, fund Black businesses, and leave assets to Black children. This is not about exclusion. It is about the compounding power of economic solidarity.

HBCU alumni already tend to earn strong incomes, leverage their alumni networks for professional advancement, and demonstrate higher rates of giving back to their alma maters and communities. According to the Gallup-USA Funds Minority College Graduates Report, 40% of Black HBCU graduates report thriving in financial well-being, compared to just 29% of Black graduates from non-HBCUs — the largest well-being gap Gallup measured between the two groups. Economic stability is one of the strongest individual predictors of marriage. Add to that the wealth-building power of sustained intra-community partnership, and the picture that emerges is of a uniquely powerful pipeline, one that begins with a campus in a college town and ends, generations later, in families that have genuinely built something lasting.

The most compelling question the data raises is not descriptive it is projective. If the HBCU environment produces meaningfully higher rates of Black marriage and intra-community partnership, what would happen to African American marriage rates if the share of Black college students attending HBCUs grew from today’s 10% to 25%, 50%, or even 75%? The answer, modeled carefully against current demographic data, is striking. These projections are calibrated estimates rather than census findings — they are directionally honest and mathematically grounded, built from known marriage rate differentials, HBCU graduation advantages, and the share of college-educated adults within the total Black population. One additional factor amplifies every projection: research shows that Black students at HBCUs are 33% more likely to graduate than their counterparts at comparable institutions, meaning scaling HBCU enrollment also scales Black degree attainment itself.

At 25% HBCU enrollment, roughly where HBCU attendance stood in the mid-1970s, the overall Black marriage rate would likely move from 31% toward 33–34%. That may sound modest, but in a population of nearly 47 million Black Americans, a two-to-three point increase represents roughly 500,000 to 700,000 additional married Black households, with intra-community marriage among college-educated Black Americans rising from roughly 79–80% toward 82–83%. At 50%, a transformational shift where the majority of college-educated Black Americans are formed in Black-centered environments, the overall Black marriage rate would likely climb toward 36–38%, closing nearly a third of the gap with the national average. The HBCU alumni network, at this density, becomes a dominant force in Black professional and social life: a self-reinforcing ecosystem where Black partner exposure is high across the entire college-educated class, translating to roughly 1.2 to 1.5 million additional Black married households.

At 75% HBCU enrollment, history offers its own precedent. Before integration dispersed the Black college-going population into majority-white institutions, HBCUs educated virtually all Black college graduates and during that era, African Americans age 35 and older were actually more likely to be married than white Americans, a trend that held from 1890 until sometime in the 1960s. A return toward 75% HBCU enrollment would not be an experiment in an unknown direction. It would be a partial return to conditions that demonstrably worked with a projected Black marriage rate of 40–42%, approaching parity with the national average for the first time in over six decades, and as many as 2 to 2.5 million additional Black married households.

HBCU Enrollment

Est. Black Marriage Rate

Intra-Community Marriage

New Married Households

10% (Today)

31%

~79–80%

Baseline

25%

33–34%

~82–83%

+500K–700K

50%

36–38%

~86–88%

+1.2M–1.5M

75%

40–42%

~90%+

+2M–2.5M

These projections carry honest caveats. Students who self-select HBCUs today may already have stronger pro-community cultural orientations, meaning the marginal effect per new HBCU enrollee may be somewhat smaller than current graduate data suggest. Marriage rates are also multi-causal — mass incarceration, income inequality, student debt, and campus gender ratio imbalances all independently shape outcomes. No single variable, however powerful, tells the whole story. But the directional conclusion is unmistakable: HBCU enrollment is a lever of community formation, not merely academic achievement. Pulling it harder produces more Black marriages, more Black wealth, and more Black families compounding across generations.

Every few years, critics question the continued relevance of HBCUs in an era of expanding integration and formal diversity efforts at major universities. The marriage data, alongside every other metric by which HBCU graduates outperform expectations relative to their socioeconomic backgrounds, is a decisive answer to that question. HBCUs are not relics of segregation. They are proof of concept — evidence that when Black people are given a fully resourced, culturally affirming environment to grow in, they flourish in ways that reverberate across every dimension of life. The lesson is not that PWIs should be abandoned or that integration was wrong. The lesson is that the goal was never assimilation — it was equity. And equity means Black people having their own institutions, not merely access to someone else’s. It means Tuskegee and Xavier and North Carolina A&T and Prairie View and Dillard and Morgan State existing not as alternatives of last resort but as premier, first-choice destinations that produce exactly the kind of human outcomes — professional, civic, familial — that their graduates embody.

The couples who meet at HBCU homecoming and marry a few years later are not a sentimental footnote to the HBCU story. They are a central chapter. They are what it looks like when a community invests in itself deeply enough that its members find each other, choose each other, and build together. The data suggests that with more investment — more students, more resources, more deliberate choice — the results scale. Two million additional Black married households is not a fantasy. It is arithmetic. And it starts with the decision of where to spend four years.

Disclaimer: This article was assisted by ClaudeAI.

HBCUs are more than just schools, they are a home. – Chadwick Boseman

The paradox is impossible to ignore: African American communities consistently champion the importance of buying Black and supporting Black-owned businesses, yet when it comes to what may be the largest purchase of a lifetime, a college education, the overwhelming majority of Black families choose to invest those dollars elsewhere. This decision has profound consequences for the survival and strength of Historically Black Colleges and Universities, institutions that remain pillars of Black achievement, economic mobility, and community power.

As of Spring 2025, approximately 19.4 million students are enrolled in U.S. colleges and universities, with about 15 million undergraduates and over 3 million graduate students, according to data from the National Student Clearinghouse Research Center reported by NPR and BestColleges. This enrollment represents a recovery from pandemic-era declines, though numbers remain below 2010 peaks. African American students comprise roughly 13-15% of this total enrollment, representing approximately 2.5 to 2.9 million students across all institution types. When we calculate the economic value of these students based on current tuition rates, the numbers are staggering.

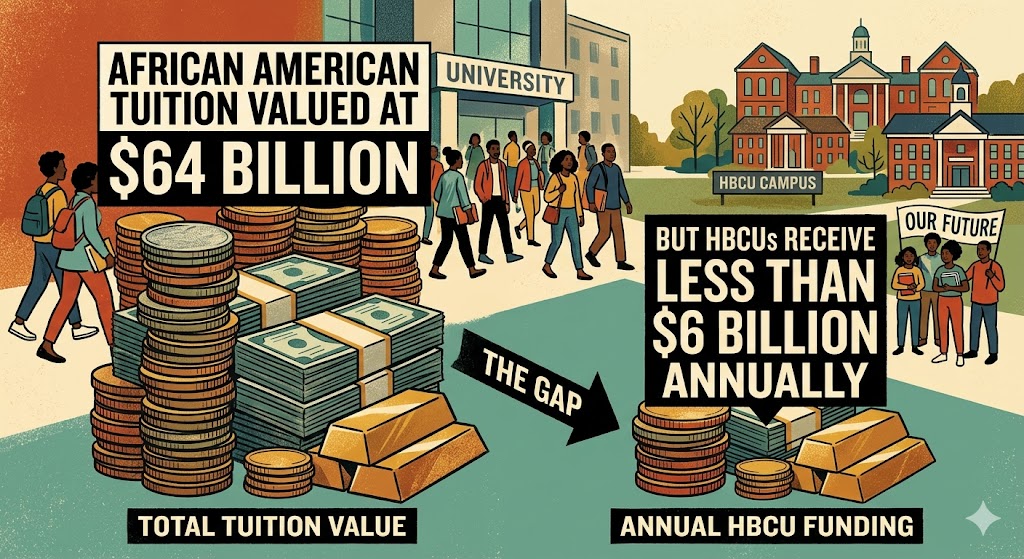

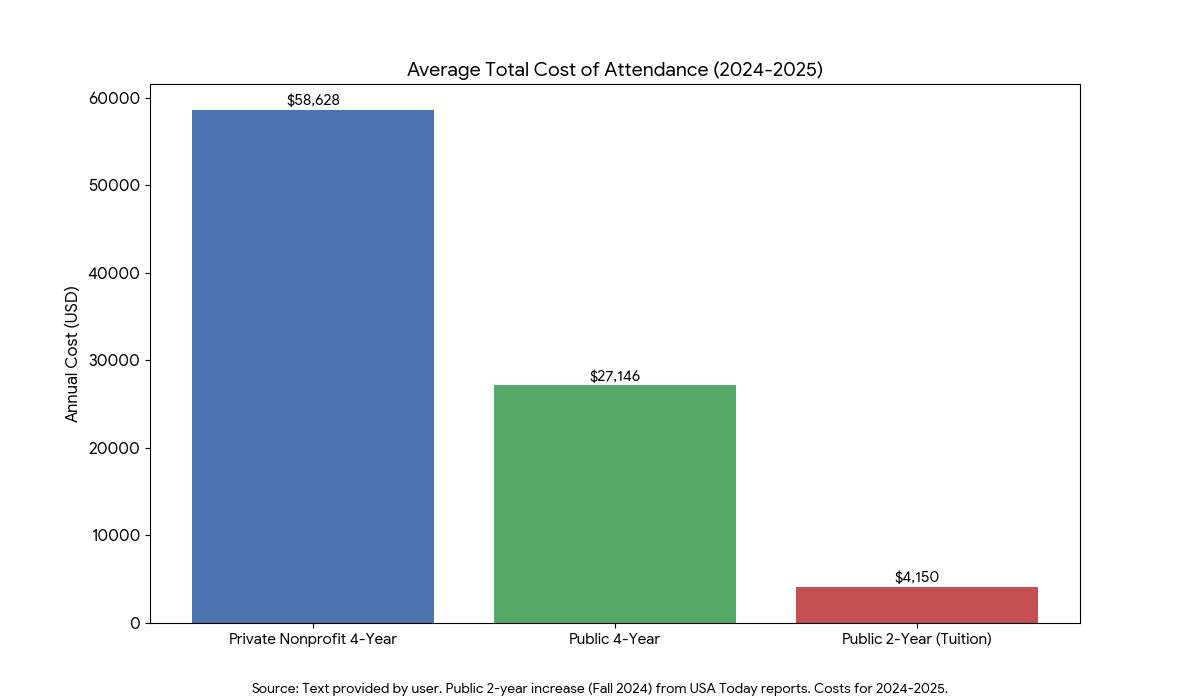

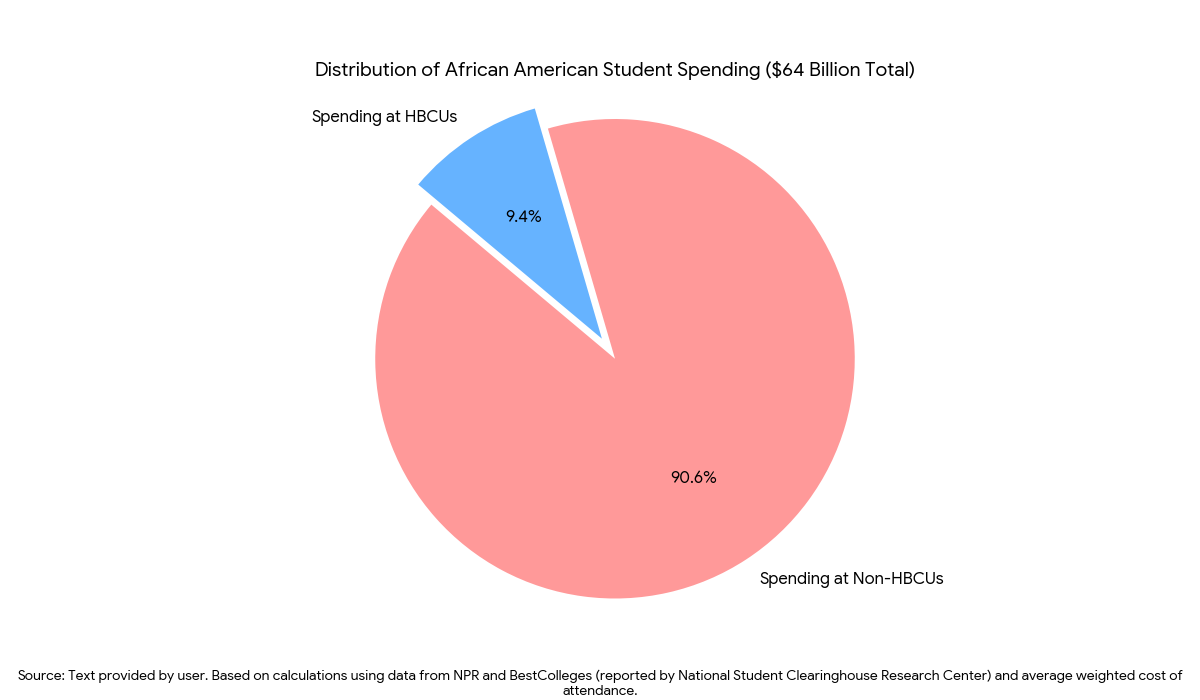

For the 2024-2025 academic year, public four-year institutions charge approximately $11,950 for in-state students and $31,880 for out-of-state students. Private nonprofit four-year schools average around $45,000 in tuition and fees. Public two-year colleges, which experienced a 3% enrollment increase in Fall 2024 according to USA Today reports, charge an average of $4,150 for in-district students. When you factor in room and board expenses, which averaged $13,310 for 2024-2025, the total cost of attendance reaches approximately $27,146 at public four-year institutions and $58,628 at private nonprofit four-year schools. Using a weighted average cost of attendance of approximately $26,000-$28,000 per year across all institution types, African American students and their families collectively spend approximately $64 billion annually on higher education. This represents enormous purchasing power—power that could transform Black institutions and communities if redirected strategically.

Here’s the uncomfortable truth: of that $64 billion, African American students at HBCUs represent only about $6 billion in tuition revenue and that $6 billion is essentially all HBCUs have to work with. Unlike predominantly white institutions with massive endowments, substantial state funding, and robust donor bases, HBCUs are almost entirely tuition-dependent. This means that more than 90% of African American education dollars approximately $58 billion annually flow to institutions that were not built for us, by us, or with our advancement as their primary mission.

We talk extensively about supporting Black businesses, banking Black, and keeping dollars circulating in our communities. Yet when families sit down to make college decisions, often the single largest financial investment they will make outside of purchasing a home, the conversation shifts. Suddenly, the narrative becomes about rankings, prestige, resources, and opportunities at predominantly white institutions, while HBCUs are considered as backup options or dismissed entirely.

This pattern has devastating consequences. The approximately 222,300 African American students currently enrolled at HBCUs generate roughly $6 billion in tuition revenue and for most HBCUs, that tuition revenue represents the vast majority of their operating budgets. Unlike well-endowed predominantly white institutions that rely heavily on endowment returns, substantial state appropriations, federal research grants, and robust alumni giving, HBCUs are critically dependent on tuition dollars just to keep their doors open. When Black students choose to take their tuition dollars elsewhere, it directly threatens these institutions’ survival, limiting their ability to maintain programs, hire faculty, upgrade facilities, and provide student services.

The impact extends far beyond immediate operating budgets. Every student who chooses a predominantly white institution over an HBCU represents not just lost tuition revenue today, but lost philanthropic potential tomorrow. Alumni giving is the lifeblood of institutional endowments, and alumni tend to give most generously to the institutions they attended. When successful Black professionals graduate from predominantly white institutions, their alumni donations when they give at all flow back to those schools. Harvard, Yale, Stanford, and other elite institutions benefit from the success of Black graduates who might have attended HBCUs if those institutions had received even a fraction of the resources concentrated at the top of higher education’s hierarchy. Meanwhile, HBCU endowments remain comparatively microscopic, not because their graduates are less successful, but because there are fewer of them writing checks back to their alma maters.

This creates a vicious cycle. Smaller enrollment means less tuition revenue and for institutions operating almost entirely on tuition, this is an existential threat. Fewer graduates means smaller donor pools. Smaller donor pools mean smaller endowments. Smaller endowments mean even greater dependence on tuition revenue and less money for scholarships, facilities, and programs. Less competitive resources make it harder to attract students. And the cycle continues, generation after generation.

The wealth gap between HBCU endowments and those of predominantly white institutions is staggering and growing. Howard University recently became the first HBCU to cross the $1 billion endowment mark, a milestone that should be celebrated but instead highlights the crisis. The top 10 HBCU endowments combined total approximately $2.6 billion. Meanwhile, Harvard University’s endowment alone exceeds $50 billion, and the top 10 predominantly white institutions hold a combined $336 billion in endowments. The PWI-to-HBCU endowment gap stands at 129 to 1. Only one HBCU has an endowment over $1 billion, while 148 predominantly white institutions have endowments exceeding that mark. This disparity means that while HBCUs scrape by on tuition revenue with minimal endowment support, elite PWIs can offer generous financial aid packages funded by massive investment returns, making them appear more affordable even as they siphon Black student dollars away from Black institutions.

In barbershops and beauty salons, at family gatherings and community events, the conversation about economic empowerment is constant. We discuss the importance of circulation of Black dollars, the need to build generational wealth, and the imperative of supporting institutions that support us. Social media amplifies calls to buy Black, support Black-owned restaurants, use Black banks, and patronize Black professionals. Yet somehow, this collective consciousness evaporates when it’s time to choose a college. Parents who wouldn’t think twice about driving across town to support a Black-owned business will encourage their children to attend predominantly white institutions without seriously considering HBCU alternatives. Students who wear “support Black business” t-shirts apply exclusively to schools where they will be a small minority, where their history may be marginalized, and where their dollars will fund institutions with no historical commitment to Black advancement.

This isn’t about judgment these are rational decisions made by families trying to secure the best possible future for their children in a competitive world. The problem is that these individual rational choices, when aggregated, produce a collective outcome that weakens the very institutions most committed to Black success.

Consider what HBCUs accomplish with their fraction of African American education dollars. These institutions enroll approximately 10% of all African American college students but produce nearly 20% of Black graduates. They generate an even higher percentage of Black professionals in critical fields like engineering, medicine, and education. The majority of Black doctors, a disproportionate share of Black lawyers, and a significant portion of Black educators earned their degrees from HBCUs. HBCUs create environments where Black students see themselves in positions of leadership, where their history and culture are centered rather than marginalized, and where they build networks that last lifetimes. Research consistently shows that Black students at HBCUs report higher levels of engagement, stronger sense of belonging, and greater confidence in their abilities compared to Black students at predominantly white institutions.

They accomplish all of this while operating on budgets that would be considered inadequate at any predominantly white institution. They make miracles happen with limited resources, outdated facilities, and faculty salaries that make it difficult to compete for top talent. Imagine what they could do with just a fraction of that $64 billion currently flowing elsewhere.

The numbers tell a stark story. Approximately 292,500 students currently attend HBCUs, with African American students comprising about 76% of that enrollment roughly 222,300 Black students. At an average cost of attendance of $26,000-$28,000 annually, these students represent approximately $6 billion in tuition revenue flowing to HBCUs each year. Meanwhile, the remaining 2.3 to 2.7 million African American college students roughly 90% of all Black college students generate approximately $58 billion in tuition revenue for predominantly white institutions.

Think about that ratio: $6 billion staying in Black institutions versus $58 billion leaving them. This isn’t about equity or fairness this is about economic power and where we choose to deploy it. Every semester, Black families collectively make purchasing decisions that send nearly ten times more money to institutions with no historical commitment to Black advancement than to institutions that were literally built to educate us when no one else would.

The enrollment landscape is shifting. Spring 2025’s 19.4 million total enrollment shows growth in both undergraduate and graduate programs. Particularly significant is the 3% surge in community college enrollment in Fall 2024, suggesting that cost considerations are increasingly driving educational decisions. This cost consciousness presents an opportunity. As families become more aware of student debt burdens and question the return on investment of expensive predominantly white institutions, HBCUs offer compelling value propositions. But they can only compete if they have the resources to tell their stories effectively, maintain quality programs, and provide the support services today’s students expect.

The net price reality adds another dimension. While published tuition rates provide a baseline, actual costs after financial aid vary significantly, typically ranging from $17,000 to $25,000 depending on institution type. However, African American students often face higher net prices than their peers at the same institutions due to lower family wealth and less access to non-loan aid. This means Black families are stretching further financially, taking on more debt, and working more hours often to attend institutions with no particular commitment to Black student success.

The solution requires a fundamental shift in how we think about educational choices. White families don’t agonize over whether to “give HBCUs a chance” they automatically prioritize their own institutions. They attend state flagships, legacy schools where their parents and grandparents went, institutions that have accumulated centuries of wealth from their community’s investment. They don’t need to be convinced to support their own. Yet somehow, Black families have internalized a narrative that HBCUs are noble but limited, worth considering but not prioritizing, respectable but not prestigious. This is the mental colonization that costs us $58 billion annually.

We need to be as intentional about our education spending as we claim to be about supporting Black businesses. This means making HBCUs the default choice, not the backup plan. It means understanding that when white families send their children to their flagship state universities and legacy institutions, they’re not making a sacrifice they’re making an investment in institutional power that compounds over generations. Black families deserve the same mindset. The choice of where to spend education dollars is an economic decision with ramifications far beyond individual degree attainment. It’s about building institutional power that can withstand political and social headwinds.

Institutional strength matters. Strong HBCUs create jobs in Black communities, anchor local economies, generate Black wealth through employment and contracts, and serve as catalysts for community development. They provide platforms for Black intellectual leadership, preserve and advance Black culture, and create networks of mutual support that span generations and geographies. In an increasingly uncertain social and political environment, the importance of strong Black institutions becomes even more apparent. When external support proves unreliable, when political winds shift, when social progress reverses, communities need institutions they control and can depend on. HBCUs represent exactly that kind of institutional foundation.

The question isn’t whether HBCUs deserve support their track record speaks for itself. The question is whether African American families will align their spending decisions with their stated values around Black economic empowerment. That $64 billion represents power—power to build, strengthen, and sustain institutions that have proven their commitment to Black success. How we choose to deploy that power will determine whether HBCUs merely survive or truly thrive in the generations ahead.

The choice is ours. The power has always been ours. The question is whether we’ll use it.

Disclaimer: This article was assisted by ClaudeAI.