Imagine a family that built a house. Not inherited it, not stumbled into it but built it, board by board, through discipline, ingenuity, and collective sacrifice. The house was real. It had rooms filled with furniture, a business on the corner, a bank down the street, a school nearby. The neighborhood thrived because the institutions within it were strong and self-reinforcing. Then the neighbors burned it down. Not metaphorically — burned it down, seized the land, rewrote the deed, and walked away with the tools. This happened not once but repeatedly, across generations and geographies, through legal architecture and extralegal violence alike. The family’s anger is entirely justified. The theft was real. The arson was documented. The loss was total and the perpetrators largely unaccountable.

But the house still needs to be rebuilt.

And here is the hard truth that justified anger cannot dissolve: the rebuilding requires the same discipline, ingenuity, and collective sacrifice as the original construction perhaps more, because this time it must be built with proper defenses. Stronger foundations. Diversified income streams. Institutions designed to survive hostility rather than assume good faith. The family cannot afford to rest in the rubble and call it protest. It cannot furnish an unbuilt house with aspirational spending and call it progress. The grief is legitimate. The rage is warranted. But neither grief nor rage lays a single board. The house demands builders, and builders before they can rest, must first build.

There is a structural mismatch at the center of African American economic life that rarely receives the frank, quantitative examination it deserves. The cultural aspiration toward comfort, leisure, and luxury, a posture increasingly celebrated under the banner of the “soft life” has emerged with real force and not without moral legitimacy. The desire to rest, to be unburdened, to live well is a reasonable human aspiration, and for Black women in particular it carries the weight of generations of overextension. But aspiration untethered from income architecture is not a lifestyle strategy it is a financial liability. And the numbers, examined without sentiment, make the case plainly: African American household income does not currently support the consumption patterns and life expectations that have come to dominate the cultural conversation.

This is not a moral indictment. It is a structural diagnosis. The soft life is not wrong. The economics are simply not there yet.

The median weekly earnings for Black full-time workers in the first quarter of 2024 stood at $908 compared to $1,157 for White workers and $1,505 for Asian workers. Annualized, this places median Black worker earnings at approximately $47,200. The median household income for African Americans reached $56,020 in 2024, compared to a national average household income of $83,810 and a White household average of $124,500. Some 61.8% of African American households earn less than $75,000 annually, and only 27% of Black households exceed $100,000 in income, a threshold that 46.8% of White households surpass. These are not marginal differences. They are structural chasms that determine what households can afford to save, invest, and build.

The income gap is not merely a matter of aggregate shortfall. It is a function of occupational concentration. African Americans remain dramatically underrepresented in the highest-earning career categories: STEM-based science and engineering, investment finance, business ownership at scale, and the upper tiers of corporate management. In 2021, Black or African American workers in science and engineering occupations had median earnings of $59,800, the lowest among racial and ethnic groups tracked, compared to $107,900 for Asian workers in the same fields. The salary premium that STEM careers offer over non-STEM work exists for Black workers, but the participation rate limits how broadly that premium reaches across the community. Nearly 58% of Black or African American workers are employed outside of science, engineering, or STEM-related areas entirely.

The gender dimension of this problem is frequently misread. African American women have achieved meaningful gains in labor force participation and educational attainment, outpacing Black men in college enrollment by a substantial margin. But participation rates and credential accumulation have not translated into equivalent entry into high-compensation fields. Black women are heavily represented in management roles, the service industry, sales, and office occupations — sectors characterized by modest wage ceilings and limited equity upside. Black women’s median weekly earnings of $887 represent 85.3% of White women’s earnings of $1,040 — a gap that, while narrower than the male-to-male disparity, still accumulates into meaningful lifetime income deficits. More critically, neither the occupational profile of Black men nor that of Black women places either group in proximity to the financial services, technology entrepreneurship, or ownership-class economics that generate the kind of income and wealth capable of sustaining the consumption expectations that aspirational culture projects.

There is, however, a dimension of the income problem that earned wages alone cannot fully illuminate, and it may be the most telling of all: passive income. Wealth that works while one sleeps through dividends, rental income, business distributions, and interest is not a luxury feature of the financial system. It is the mechanism by which all other wealth gaps compound and perpetuate. Only 7% of Black households report receiving passive income from sources such as rental properties, interest, dividends, or business ownership compared to 24% of White households. And when such income does exist, the median amount for Black families is approximately $2,000 annually, compared to nearly $5,000 for White households. This is not a secondary observation. It is the statistical signature of a community almost entirely excluded from the capital class — the tier of economic life where money generates more money without additional labor.

The implications of that exclusion are severe. Black households rely more heavily on wages and salaries rather than passive income streams, and without accumulated wealth or financial investments, it becomes harder to transition from relying solely on wages to generating income passively. The debt burden compounds this further: Black households tend to carry higher levels of student loan debt relative to income, which reduces the disposable income that could otherwise be directed toward wealth-generating assets. This is the trap in precise structural terms: earned income is consumed servicing debt, leaving no surplus to convert into the asset base that generates passive returns. Each month begins at zero. Each generation inherits the same constraint. The soft life as aspiration sits atop this architecture and finds no foundation.

The consequence of this occupational and income reality extends further into household formation. The marriage rate among African Americans has fallen from approximately 60% in the 1960s to just 29% in 2021. This matters economically in ways that exceed the social commentary often surrounding it. Black married couples had a median net worth of $131,000 in 2019, compared to only $29,000 for Black single individuals — a gap of roughly three to four times. The dual-income household is not merely a social arrangement; it is a capital formation mechanism. Two modest incomes, pooled and directed strategically, can accomplish what a single income, however aspirationally deployed, cannot. When household formation rates decline, the financial unit of account shrinks. The result is not simply less comfort it is structurally constrained savings capacity, reduced homeownership rates, diminished retirement security, and negligible investable surplus.

This brings the soft-life discourse into direct collision with economic arithmetic. The soft life, as a cultural concept, carries entirely legitimate roots. The desire to step back from overextension is not irrational; it is self-preserving. But the aspiration as it has been culturally operationalized — emphasizing travel, luxury goods, minimal work, and premium consumption — requires an income infrastructure that the median African American household does not possess. The soft life as an aesthetic has spread across a community where, the median Black household holds just $44,100 in net worth compared to $284,310 for White households or roughly 15 cents for every dollar White households possess. The median Black household has only $2,200 in checking and savings accounts, approximately a fifth of what White households hold. Aspirational consumption layered over that wealth foundation does not produce liberation. It produces debt.

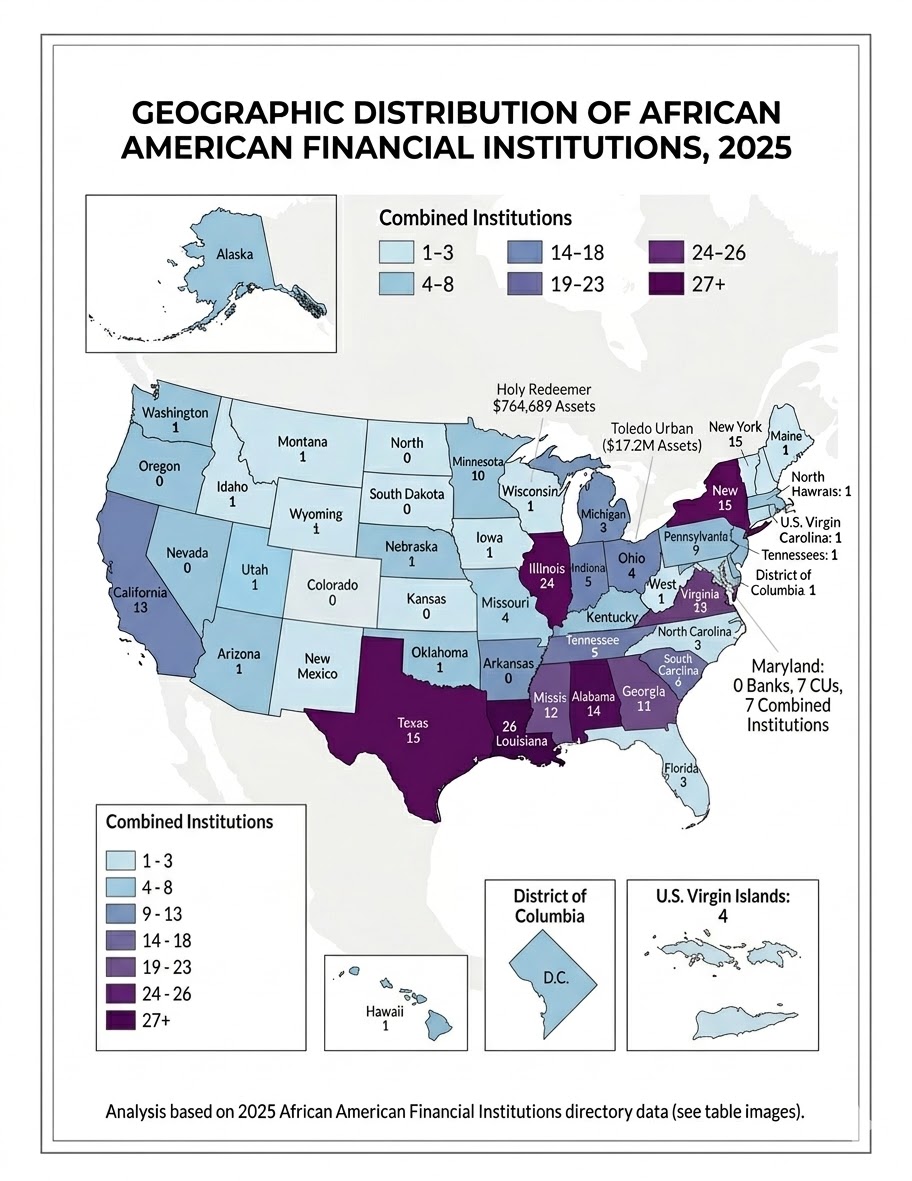

Consumer credit among African American households climbed to $740 billion in 2024, representing nearly 48% of all African American household liabilities and growing at more than double the rate of asset appreciation. The shift toward unsecured, high-interest borrowing to fund present consumption represents the structural outcome of a community whose income and wealth positions do not support the lifestyles being pursued. With African American-owned banks holding just $6.4 billion in combined assets, the vast majority of that $1.55 trillion in household liabilities flows to institutions outside the community meaning that interest payments, fees, and the wealth-building potential of lending relationships are being systematically extracted from the Black institutional ecosystem. The community is not simply spending beyond its means; it is doing so in a way that enriches external financial institutions rather than its own.

The comparison with other groups is instructive precisely because it is structural, not cultural. Households that have accumulated generational wealth, that inherit homes rather than rent them, that receive family capital for business formation or down payments, that can distribute housing costs across extended family networks, or that have parents who absorb the student debt burden — those households operate from a fundamentally different economic baseline. The aspiration toward leisure and comfort that is financially reasonable for households with $284,000 in net worth, with 24% receiving passive income, is not the same proposition for households with $44,000 in net worth, with $26,000 in student loan debt, and fewer than one in ten receiving any passive income whatsoever. This is not a commentary on character. It is a commentary on compound arithmetic.

The three missing pillars; high-income career concentration, passive income streams, and wealth-building household formation, reinforce one another in ways that make each individually insufficient to close the gap. High earned income without passive income accumulation remains treadmill economics: impressive in the short run, exhausting across a lifetime, and non-transferable across generations. Passive income without the earned income base to seed initial investments is equally out of reach for most households. And both are more difficult to build and sustain outside of the two-income, asset-pooling household structure that marriage has historically provided. The causality runs in a specific direction: institutional infrastructure creates the conditions for sustainable individual and collective wealth building, not the other way around. But at the household level, the sequencing is equally specific where earned income must first be directed toward asset acquisition rather than consumption, and those assets must be allowed to compound before comfort becomes the organizing principle of financial life.

What the data demand is a recalibration of collective strategy, beginning with income generation at the individual level and extending upward through institutional infrastructure. The income problem is real and addressable, but it requires African Americans — men and women alike — to direct educational and career investments toward the highest-compensation fields in the economy: engineering, software development, quantitative finance, medicine, law at the partnership track, and scalable business ownership. The wage premium of STEM occupations over non-STEM work stands at roughly $19,100 per year even at the median. But earned income must be understood as the raw material for wealth, not the destination. The destination is an asset base generating passive returns — the condition that makes rest not just emotionally justified but financially sustainable.

The institutional dimension cannot be separated from either the income or the passive income dimension. If approximately 95% of African American debt is held by non-Black institutions, and that debt carries an average interest rate of 8%, African American households collectively transfer roughly $120 billion annually in interest payments to institutions with no vested interest in Black wealth creation. That capital hemorrhage occurs upstream of any lifestyle decision. It is the structural tax imposed by institutional absence, the cost of lacking the banking, investment, and insurance infrastructure to retain and recirculate capital within the community. The passive income gap is not only a personal finance failure; it is the individual-level expression of institutional underdevelopment. Communities that have strong banks, investment firms, and cooperative capital structures create the conditions in which their members can access investment vehicles, receive competitive lending terms, and build the asset portfolios that generate passive returns. Those institutions do not yet exist at adequate scale for African America.

The soft life is a worthy destination. But destinations require roads, and roads require investment. The African American community is not yet at a place; economically, institutionally, or in terms of income concentration in high-value careers and asset-generating passive income streams, where widespread leisure is the financially rational near-term posture. The pragmatic path forward involves strategic sacrifice now: of time, of consumption, of immediate comfort, in exchange for the capital, credentials, and institutional infrastructure that make genuine ease sustainable across a generation and transferable to the next. Every dollar directed toward an index fund rather than a luxury purchase, every professional credential pursued in a high-compensation field, every household formed that pools two incomes toward asset acquisition rather than consumer spending — these are not acts of deprivation. They are acts of institution-building at the individual scale. And they are the precondition for the rest that so many in this community have, entirely reasonably, been waiting a very long time to claim.

That is the harder conversation. It is also the more honest one.

Disclaimer: This article was assisted by Claude AI.