We are forced to trust the very institutions who stole the land in the first place because we have not developed and maintained our own. – William A. Foster, IV

A grandfather in Wilcox County plants loblolly pine on forty acres in 1961, the year the trees will outlive him being the whole point. He tells his children the timber is not for cutting; it is for holding. When he dies without a will, the forty acres become the property of nine heirs, then, a generation later, of thirty-one. No bank will lend against a title held by thirty-one people who cannot agree to sign the same document. The family calls the county forester listed on the state’s directory, the only one covering their district, because there is no other option in the phone book and no other name anyone in the family has ever heard mentioned with trust. The advice that comes back is vague, the timeline uncertain, and there is no second opinion to check it against, no other firm to call, no one who looks like the family sitting across the table. The pines keep growing, undermanaged not for lack of care but for lack of anywhere safe to take that care. Forty years after planting, a timber company buys out the confused heirs for a fraction of the standing timber’s value, and the grandfather’s patient capital becomes someone else’s harvest.

That scene is not a story about one bad forester or one unlucky family. It is a story about what happens when an entire asset class has exactly zero Black-owned institutions capable of serving it; no brokerage, no financing arm, no forestry consultancy, no appraisal firm built by and accountable to the community whose land is on the table. For nearly every other category of wealth-building infrastructure, HBCU Standard has documented at least a partial institutional base: Black-owned banks and credit unions, Black-owned commercial real estate firms, Black-owned construction companies. In rural land and timberland specifically, a category increasingly discussed as an inflation hedge, a carbon-credit asset, and a durable multigenerational holding — that base does not exist. Not a small one. Not a regional one. None. And the absence does not simply mean missed opportunity. It means that every African American family holding rural land, and every one considering buying it, is doing so without the single thing that would let them tell the difference between good advice and bad: a trusted counterparty inside the industry with something to lose if it gets that advice wrong.

This is the predicament worth naming plainly. A family that already holds land has, in most of the rural South, exactly one state district forester assigned to their county, no competing Black-owned firm to call for a second opinion, and no institutional recourse if that forester’s guidance turns out to serve someone else’s interests rather than theirs. A family looking to buy timberland as an asset has no Black-owned equivalent of a firm like Hall and Hall, which does not simply broker land but finances it directly, offering loan programs ranging from low variable rates to full thirty-year fixed terms so a client can originate, appraise, and fund an acquisition inside a single relationship. That vertical integration is precisely what makes an institution durable across a timber rotation: the same firm that helps a client find and value a parcel can also lend against it, rather than sending the client back out to a separate lender with no connection to the land or the deal.

To understand why that absence matters, it helps to see what a firm like Hall and Hall actually does, because it bears almost no resemblance to the real estate transaction most readers know from buying a house. A residential agent lists a property, compares it against recent sales of similar homes nearby, and hands the buyer off to a conventional mortgage lender who underwrites based on the buyer’s income and an appraiser’s estimate of the house’s value alone. None of those tools transfer to timberland. Valuing a working forest requires an actual cruise of the standing timber; a forester physically walking the property to inventory species, age, volume per acre, and growth rate because the trees themselves are a separate, living asset with their own market price, layered on top of the bare land value, changing every year whether anyone touches it or not. Financing the purchase means underwriting against decades of projected harvest income, and often against secondary income like grazing or hunting leases, rather than a buyer’s fixed monthly paycheck, which is why Hall and Hall runs its own loan programs instead of referring clients to a bank teller. And the transaction itself carries considerations a residential closing never touches: mineral rights that may or may not convey with the surface, water rights in Western states, conservation easements that permanently restrict future use in exchange for tax benefits, access easements across neighboring land, and a formal management plan for what happens to the timber over the next thirty years, not just what happens at the closing table. A firm built to handle all of that under one roof, continuously, is a fundamentally different kind of institution than a residential brokerage that occasionally lists rural acreage on the side and it is exactly why calling a local real estate agent, however well-intentioned, is not a substitute for the thing that’s missing.

No Black-owned firm offers any piece of that stack, let alone all of it. A family that finds its way past appraisal and negotiation on its own still has to secure financing from an institution outside the community entirely often the very kind of lender whose historical record with Black landowners is the reason for caution in the first place.

That wariness is not paranoia. It has a documented record behind it. Pigford v. Glickman, settled in 1999 as one of the largest civil rights settlements in American history, established in federal court that the USDA had systematically discriminated against Black farmers in the allocation of farm loans and disaster assistance between 1981 and 1996 delaying and denying credit that white farmers received routinely, and for over a decade failing to functionally operate the very civil rights office meant to investigate complaints about it. Congress appropriated another $1.2 billion in 2010 for a second settlement, Pigford II, because so many farmers with legitimate claims had been unable to file the first time. This is not ancient history from the era of outright land theft after emancipation. It is a pattern of institutional behavior toward Black landowners that persisted into living memory, inside the very federal agency structure that state and district foresters, county extension offices, and agricultural lenders all sit within. A family that has watched that pattern play out in the district office, in the bank, sometimes in their own family’s dealings with a local forester has every reason to want a trusted, accountable alternative before signing anything. The absence of that alternative is the actual risk, not an inconvenience layered on top of one.

Layer the heirs’ property problem on top of that trust deficit and the predicament compounds rather than adds. Research out of the University of Georgia’s Warnell School of Forestry has documented how clouded title land passed down without a will, held as an undivided interest among a growing number of descendants locks families out of financing, cost-share programs, and professional forest management, because no lender or agency wants to deal with an ownership structure that any single heir could blow up with a partition sale. Resolving that title requires legal expertise most families cannot afford and most local firms are not built to provide with any particular care. Mavis Gragg’s organization HeirShares exists specifically to clear these legal pathways, and the Federation of Southern Cooperatives has run a Land Assistance Fund toward the same end for decades. But neither is a brokerage, a lender, or a forestry management firm. They can help a family reach clean title. They cannot then walk that family through financing a thinning operation, negotiating a fair timber sale, or acquiring a second parcel to expand the holding, the actual services a firm like Hall and Hall provides continuously to the families who already trust it. Clearing title without a trusted destination to route the resulting clean parcel toward simply relocates the risk rather than resolving it.

The scale of what’s been lost while this institutional vacuum sat unfilled is worth stating plainly, in the register this publication uses for these numbers rather than the multi-trillion projections other outlets reach for. In 1910, according to the National Forest Foundation, Black Americans owned 195 timber companies and comprised roughly a quarter of all employees in the forest products industry. By 1920, per the Land Trust Alliance, African American farmers controlled approximately 14 percent of the nation’s farmland; today that figure is under 1 percent, and total African American land ownership across every category; timberland, farmland, residential, everything has fallen from an estimated 15 to 16 million acres to under 2 million. Set that number against a single entry on the Land Report’s 2025 ranking of America’s largest private landowners: the Emmerson family, through Sierra Pacific Industries, holds 2.44 million acres of timberland in California, Oregon, and Washington alone more than the entirety of Black land ownership nationwide, across every category, combined. John Malone holds roughly 2.2 million acres across four states. The Reed family’s Green Diamond Resource Company, built from a Pacific Northwest logging operation started in 1897, holds about 2.1 million acres. Each of those holdings is the product of a century or more of uninterrupted institutional continuity: clean title passed down without interruption, financing relationships maintained across generations, professional forestry management retained continuously rather than improvised family by family. That continuity is precisely what heirs’ property and the absence of a trusted institutional counterparty have made structurally difficult for Black landowners to replicate, no matter how much care any individual family brings to the effort.

None of this argues that timberland is a bad asset for African American families to hold or acquire. It argues the opposite: that the fundamentals of the asset class; steady periodic cash flow from harvests, low correlation with equity markets, a growing carbon-credit revenue stream for standing forest, and a purchase price still within reach of pooled institutional capital make it exactly the kind of holding worth building durable infrastructure around. And the talent to staff that infrastructure is not the missing piece. Alabama A&M University, one of the nineteen 1890 land-grant HBCUs rather than one of the handful of flagship HBCUs (Howard, Morehouse, Spelman) usually invoked in this conversation, runs the only professionally accredited forestry degree at an HBCU and operates as a USDA Forest Service Center of Excellence. Southern University and A&M College in Baton Rouge, part of the only historically Black land-grant university system in the country, offers a bachelor’s, master’s, and Ph.D. in Urban Forestry through a program it describes as the most comprehensive of its kind in the nation. Tuskegee University runs combined forestry programs with Auburn, Iowa State, the University of Michigan, and Idaho State, sending its students on to finish accredited degrees at partner institutions. And a partnership dating to 1993 between the U.S. Forest Service and four HBCUs; Alabama A&M, Southern, Tuskegee, and Florida A&M has, according to the Forest Service’s own national diversity student programs manager, trained two-thirds of the Black foresters currently working inside the agency. That is not a thin pipeline. It is a substantial, decades-old talent base, producing credentialed foresters at meaningful scale, virtually none of whom currently have the option of being hired into a private Black-owned brokerage, appraisal, or land-management firm because no such firm exists to hire them. The gap in this asset class was never expertise. It is the institution that expertise would staff.

What the Wilcox County family needed in 1961, and what a family looking to buy its first parcel of timberland needs today, is the same thing: an institution built specifically to hold this asset class the way Sierra Pacific and Green Diamond hold theirs, financed the way Hall and Hall finances its own clients’ acquisitions, staffed by graduates of Alabama A&M, Southern, and Tuskegee who are accountable to the community whose trust the industry has not yet earned, and structured to move a family from clouded title through financing through active management without ever requiring them to extend blind faith to a district office or an outside lender with no history of earning it. Every piece of that institution’s eventual capability already exists somewhere, disconnected from the others; title-clearing organizations, a credentialed forestry pipeline, cooperative land trusts, community capital sitting in Black-owned banks and HBCU endowments. Coordinating those pieces into one accountable, professionally staffed, vertically financed institution is not a distant aspiration. It is the specific, buildable answer to a specific, well-documented predicament.

The grandfather who planted loblolly pine in 1961 was making an institutional bet without an institution to back it, trusting that the trees, the family, and eventually someone trustworthy to manage them, would all still be standing when the rotation came due. The trees held up their end. What failed was everything around them: the title no bank would recognize, the forester no one had reason to trust, the financing that had to be sought from strangers, the firm that never got built to stand between the family and the forced sale. Until African America has its own version of the institution that holds land the way Sierra Pacific and Green Diamond hold theirs and finances it the way Hall and Hall finances its own, every acre already owned and every acre still to be bought carries a risk no amount of individual caution can fully offset.

Disclaimer: This article was assisted by ClaudeAI.

Let us put our money together; let us use our money; let us put our money out at usury among ourselves, and reap the benefit ourselves. – Maggie Lena Walker

The HBCU Card routes HBCU community spending through a family-owned Minnesota bank. African American-owned financial institutions are watching from the sideline. HBCUs are institutions with balance sheets, alumni networks, and banking relationships. When those relationships run through a family-owned bank in St. Paul, Minnesota, the question is not whether the partnership is well-intentioned. The question is who is building institutional capacity for whom.

There is an old arrangement, familiar to the sharecropping South, called the company store. The employer owned the land, controlled the wages, and operated the only store within reach. The worker labored, earned, and spent and every dollar completed a circle that ended back in the employer’s pocket. The arrangement was not presented as exploitation. It was presented as convenience. As service. As the reasonable way things worked given the options available. The options, of course, were controlled by the same party that ran the store. HBCUs in 2026 are not sharecroppers. They are institutions with endowments, alumni networks, and balance sheets. Which makes it harder, not easier, to explain why they are running the company store model on their own communities.

A prepaid Mastercard called the HBCU Card is circulating in HBCU communities, issued through Sunrise Banks, N.A., a family-owned bank headquartered in St. Paul, Minnesota. It carries the logos of individual HBCUs. It returns a fraction of transaction fees to participating schools. The pitch is that HBCU students and alumni can express institutional pride through their spending and send a little money back to their alma mater in the process. That is the whole proposal. Read it twice if you need to.

It is not alignment. It is a licensing agreement dressed up as solidarity.

Sunrise Banks is a privately held, family-owned institution headquartered in St. Paul, Minnesota, wholly owned by University Financial Corp, GBC, led by CEO David Reiling and his father, Bill Reiling. The bank is a certified B Corporation and holds CDFI designation from the U.S. Treasury. Its social impact commitments are real. None of that is the point. Sunrise Banks is not an African American-owned institution. It has no ownership ties to the HBCU community. It is not part of the African American financial ecosystem in any structural sense. It is a vendor that found a distribution channel, and the distribution channel said yes. Banking is not a transaction. It is infrastructure. Deposits flow into balance sheets that fund mortgages, small business loans, and community reinvestment. When that capital is held by institutions with ownership accountability to the depositing community, it compounds within that ecosystem. When it flows to an outside institution, however well-certified, however socially conscious its marketing, it leaves. A branded card does not change the direction of the outflow. Pride does not reroute capital. Ownership does.

HBCUs are, by their founding logic, in the business of building something that lasts. Endowments. Land. Research infrastructure. Alumni networks that compound across generations. That is the institutional premise. Against that premise, the HBCU Card is an embarrassment. It asks HBCU communities to generate transaction fee revenue, a rounding error in any serious capital strategy — and hand the actual value of the arrangement to a Minnesota family bank. The HBCU gets logo placement. Sunrise Banks gets a branded distribution network across dozens of historically Black institutions, customer acquisition at scale, and the reputational association with one of African America’s most symbolically resonant set of institutions. That is not a partnership. That is a concession. This would be forgivable if there were no alternative. There is. There are 221 of them.

As of 2025, there are 205 active African American-owned credit unions holding more than $8.15 billion in assets and serving nearly 727,000 members across 29 states and the District of Columbia. There are 16 African American-owned banks holding $6.7 billion in combined assets. Louisiana alone has 25 African American-owned credit unions. Illinois has 23. Virginia has 13. These institutions are not obscure. They are documented, chartered, federally insured, and in many cases operating within miles of HBCU campuses. Six HBCU-affiliated credit unions, institutions built specifically to serve the campus financial community, are still active after five such institutions closed or were absorbed since 2020. Their combined assets total $76.8 million. They are contracting. The HBCU Card is expanding. This is the choice being made.

The six that remain deserve to be named because the institutions they were built to serve have apparently forgotten them. Southern Teachers & Parents Federal Credit Union, founded to serve the Southern University system across its Baton Rouge, New Orleans, and Shreveport campuses, is the largest of the survivors at $30.3 million in assets. Florida A&M University Federal Credit Union serves the flagship public HBCU in Florida. Virginia State University Federal Credit Union serves one of Virginia’s historically Black institutions. Councill Federal Credit Union serves the Alabama A&M University community. Arkansas A&M College Federal Credit Union serves the University of Arkansas at Pine Bluff. Xavier University of Louisiana Federal Credit Union serves the only historically Black Catholic university in the Western Hemisphere. These six institutions held a combined $76.8 million in assets as of the most recent reporting, a number that should be ten times larger given the campus communities they sit inside. Prairie View A&M University Federal Credit Union, founded in 1937 by sixteen people who built a financial institution to serve the employees of Texas’s first state-supported college for African Americans, did not survive. It was absorbed by Cy-Fair Federal Credit Union, the credit union of a Houston-area school district with a documented record of racial inequity in its own student discipline. An 85-year-old Black institution, built by and for a Black university community, became a subsidiary of a school district credit union. Prairie View A&M University has nothing publicly to say about it. These institutions are not disappearing because they failed their communities. They are disappearing because their communities’ own flagship institutions will not anchor them.

The scale of what coordinated HBCU engagement could mean to this sector is not theoretical. The median African American-owned credit union holds approximately $2.47 million in assets and serves roughly 618 members, operating at the margin of viability in an asset tier where the national system is contracting fastest. Only 40 percent have a functional public website. Thirty percent are congregation-affiliated, with succession risks that threaten their continuity across a single pastoral transition. These institutions are not failing for lack of purpose. They are failing for lack of the institutional anchor relationships that would capitalize and stabilize them. HBCUs are precisely that anchor. A single mid-sized HBCU redirecting its payroll processing and student financial services to an African American-owned financial institution is a capitalization event for that institution. Six HBCUs doing it in a coordinated way reshape a sector. Instead, the sector contracts and HBCUs sign prepaid card deals.

The HBCU Card requires nothing from the institution except a logo. There is no governance, no balance sheet commitment, no strategic partnership to build or manage. An administrator with a full calendar can execute it in an afternoon. That is the real explanation, and it is worth saying plainly: this is what institutional avoidance looks like when it has been dressed up with branding. Banking with an African American-owned institution requires relationships to be built, terms to be negotiated, and sometimes real advocacy inside a bureaucracy that defaults to the path of least resistance. It is harder. It is supposed to be harder. Institutions that will not do the harder work in service of their own community’s financial ecosystem are not being strategic. They are being comfortable.

The Jewish American institutional ecosystem did not build generational financial infrastructure by licensing its brand to well-intentioned outside vendors. It built banks. It built credit unions. It built investment vehicles and directed capital toward them, institution by institution, decade by decade. Cuban American financial infrastructure in South Florida did not emerge from branded prepaid cards issued by Anglo-owned banks. It emerged from institutional discipline from the deliberate decision to route deposits, payroll, and investment relationships toward institutions owned by the community they were meant to serve. African American institutions are capable of the same discipline. The question that must be asked plainly, at this point, is whether they intend to practice it.

Sunrise Banks will receive a branded distribution network across the HBCU ecosystem, customer acquisition at scale, and the reputational weight of an association with institutions that African America has defended, funded, and attended for over 150 years. HBCUs will receive a transaction fee drip. That is the deal, and anyone who has read a term sheet in their life can see which side of it they want to be on. The deeper insult is that the card’s central premise that cultural identity can be expressed through a branded payment instrument is not wrong. OneUnited Bank, one of the largest African American-owned bank in the country with $756 million in assets, already offers a full range of culturally branded debit card designs as part of its standard deposit product. The infrastructure to do this through a Black-owned bank already exists. HBCUs have simply chosen not to direct their communities toward it.

The alternative does not require building anything new. It requires redirecting what already moves. Payroll. Student fee processing. Operating accounts. Auxiliary enterprise banking. These are cash flows that exist at every HBCU right now, today, flowing through institutions with no ownership accountability to the African American community. Fort Valley State University in Georgia operates with Citizens Trust Bank and Carver State Bank in the same state. Edward Waters University in Jacksonville, Florida sits in a market with documented African American-owned financial institution presence. Bethune-Cookman University and Florida Memorial University operate in a Florida context where redirecting institutional banking relationships would register immediately and materially in the balance sheets of the African American-owned credit unions that are currently fighting to survive. None of this requires a capital campaign. It requires a decision.

Delaware State University sits in proximity to one of the most financially sophisticated African American communities on the East Coast and banks with institutions that have no structural accountability to that community. Cheyney University, the oldest HBCU in the country, founded in 1837, older than the Civil War, operates in Pennsylvania, a state with documented African American-owned financial institutions, without a formal banking relationship with a single one of them. These are not resource constraints. These are not governance complications. These are choices. Call them what they are.

This is not an indictment of Sunrise Banks. The Reiling family built a legitimate community development institution and its credentials are real. But good intentions held by people outside a community are not a substitute for ownership infrastructure inside it and this distinction should not have to be explained to the leadership of institutions that exist precisely because the African American community refused to accept the benevolence of outside institutions as a substitute for their own. The HBCU was the answer to that substitution. The HBCU Card reverses the logic entirely.

The pattern is not new and it is not subtle. African American institutions accept the role of distribution channel, brand partner, and program host for arrangements that deliver the primary economic value to someone else. The community benefit is always in the framing. It is often partially real. What it never builds is the ownership infrastructure that makes a community institutionally durable across generations. HBCU Money has documented this in research pipelines that route HBCU-generated intellectual capital into PWI commercialization structures. In philanthropic arrangements that deliver program dollars without governance rights. In workforce development partnerships that build human capital for employers with no reciprocal obligation to the communities supplying the talent. The HBCU Card is the same transaction in a different category. The African American community keeps accepting these terms. Its institutions keep modeling the acceptance. And then everyone wonders why the ecosystem does not compound.

HBCUs are not passive observers of the African American financial ecosystem. They are, or should be, its institutional anchors. A single HBCU redirecting its payroll, student financial services, and auxiliary enterprise banking to African American-owned institutions is a capitalization event for those institutions. Six doing it in coordination reshape the sector’s asset base. Twenty doing it is a structural transformation of African American financial infrastructure that no amount of philanthropic giving or federal grant-making has ever achieved. That is what is being traded away for transaction fee revenue from a prepaid card. Let that land.

The 205 African American-owned credit unions and 16 African American-owned banks — Liberty Bank and Trust, Citizens Trust Bank, Mechanics and Farmers Bank, Optus Bank, Industrial Bank, First Independence Bank, and the rest — are not waiting to be discovered. They are chartered, capitalized, and operational. They have been there. What they have not had is the institutional anchor relationships that HBCUs are positioned to provide and have repeatedly declined to provide. That is the record. It is not ambiguous.

The HBCU Card will keep finding takers. The path of least institutional resistance always does. What it will not build, what it cannot build, is the African American financial ecosystem that 150 years of HBCU existence should by now have helped to anchor. That ecosystem is being built, slowly and against the current, by institutions that have received none of the loyalty that their community’s flagship universities should be directing toward them. HBCUs were founded as an act of defiance against a system that refused to invest in Black institutional capacity. The HBCU Card is an act of surrender to the same logic, branded in school colors.

African America knows the statistic. It has been recited at every convocation, posted on every community Facebook page, cited in every financial literacy workshop for the last thirty years: a dollar circulates in the Jewish American community for an estimated 20 days, in Asian American communities for roughly 28 days, and exits the African American community in less than 6 hours. The room nods. The speaker moves on. And then the HBCU signs a deal with Sunrise Banks. This is the part that should produce institutional shame and does not. The circulation of the Black dollar has become African America’s most repeated and least practiced idea. It functions as a ritual, spoken to affirm shared values, set aside before the next institutional decision is made. And the institutional decisions are where the actual economy is built or surrendered. HBCUs are supposed to be different. They are the institutions African America built when it was not allowed to build them. They carry that founding act in their names. They commemorate it at every homecoming. And then Alabama State University hands a $125 million investment management contract to a European American-owned firm without a public accounting of whether a single African American-owned asset manager was seriously considered. And Howard University puts PNC’s name on a center for entrepreneurship. And HBCU after HBCU runs its student financial services through Wells Fargo or Bank of America while Liberty Bank, Citizens Trust, and Mechanics and Farmers Bank operate in the same states, serve the same communities, and wait for a relationship that does not come. “Buy Black” is the slogan. The institutional behavior is: accept the proposal from whoever shows up with the most polished deck. This cannot be fixed at the household level. Individual people buying Black cannot compensate for institutions that do not. When HBCUs alongside fraternities, sororities, churches, and every other pillar of African American institutional life model the extraction rather than the retention, the community internalizes the lesson being taught, not the slogan being chanted. The HBCU Card is not an isolated mistake. It is a current example of a durable institutional posture: perform solidarity, outsource the economics.

Disclaimer: This article was assisted by ClaudeAI.

African American-owned credit unions hold more than $8.15 billion in assets and serve 726,929 members in 2025, more than doubling their asset base from $3.81 billion in 2016. That growth confirms that Black-owned cooperative finance remains a living, expanding sector — not a historical artifact. Yet placed against the broader credit union landscape, the numbers tell a more sobering story. The federally insured credit union system holds $2.37 trillion in total assets across 4,411 institutions. African American-owned credit unions, with 205 active institutions down from 318 in 2016, control just 0.34 percent of that total asset base. The sector’s 453 Minority Depository Institution-designated peers collectively hold $95.1 billion in assets; African American institutions account for less than 9 percent of that figure. The gap is not closing fast enough.

The structural challenges are as significant as the asset gap. The median African American-owned credit union holds approximately $2.47 million in assets and serves roughly 618 members placing it squarely in the asset tier where the national system is contracting most aggressively, with institutions under $10 million posting declines in assets, membership, and net worth year over year. Only 40 percent of these institutions maintain an active public website, rendering the majority functionally invisible to younger and mobile-first members. An estimated 30 percent are affiliated with religious congregations, compared to approximately 5 percent of all U.S. credit unions, introducing succession and governance risks that extend well beyond normal institutional turnover. Meanwhile, the HBCU-based credit union subsector has seen five of its eleven institutions close or be absorbed since 2020, leaving six survivors holding a combined $76.8 million in assets — institutions that represent the most direct expression of university-anchored Black financial infrastructure and are quietly disappearing without coordinated intervention.

The sector’s geographic concentration compounds these institutional vulnerabilities. Maryland, Mississippi, Missouri, and Virginia together account for roughly 80 percent of all African American-owned credit union assets nationally, while states like California, Minnesota, and Wisconsin maintain only token institutional presences despite substantial African American populations. The South remains the geographic and institutional core, with Louisiana’s 25 institutions representing the largest state count and Mississippi’s Hope Credit Union standing as the sector’s clearest model of what scale and institutional commitment can produce. The path forward runs through consolidation where fragmentation cannot be reversed, digital investment where infrastructure is absent, geographic expansion where populations go unserved, and the fuller utilization of federal support mechanisms such as MDI designation, CDFI certification, and NCUA technical assistance that the sector has historically left on the table.

ADDITIONAL NOTES

African American-owned credit unions now hold $8.15 billion in total assets across 205 active institutions, representing 0.34 percent of the $2.37 trillion held by all federally insured credit unions nationally.

Total assets in the sector have more than doubled since 2016, rising from $3.81 billion — a 114 percent increase — while membership grew 39.5 percent from 521,078 to 726,929 members over the same period.

AACUs average assets per institution: approximately $39.8 million. AACUs median assets per institution: approximately $2.47 million. The gap between the mean and median reflects a sector dominated at the top by a small number of large institutions while the majority operate at a scale that limits their competitive viability.

AACUs average members per institution: approximately 3,546. AACUs median members per institution: approximately 618.

Only 40 percent of African American-owned credit unions maintain an active public website, representing a critical digital infrastructure deficit in an era of mobile-first financial services.

An estimated 30 percent of African American-owned credit unions are affiliated with religious congregations compared to approximately 5 percent of all U.S. credit unions introducing institutional succession risk as American religious participation continues its long-term demographic decline.

Louisiana has the largest number of active African American-owned credit union institutions (25), followed by Illinois (23), New York (15), Texas (14), Virginia (13), and Alabama and the District of Columbia with 12 and 10 respectively. Maryland leads all states in total sector assets at $4.47 billion, followed by Mississippi at $1.05 billion and Missouri at $480 million.

California — the most populous U.S. state and home to one of the largest African American populations in the country — has a single active African American-owned credit union with $318,105 in assets and 262 members, a presence that has contracted since 2016.

The sector’s credit union count has declined from 318 institutions in 2016 to 205 active institutions in 2025, a reduction of 35 percent, driven primarily by closures, mergers into non-Black institutions, and voluntary dissolutions.

For comparison, the national credit union system added 2.9 million members over the past year alone, reaching 143.2 million total members — nearly 200 times the total membership of all African American-owned credit unions combined.

Land is the only thing in the world that amounts to anything, for it’s the only thing in this world that lasts. It’s the only thing worth workingfor, worth fighting for… – Ted Turner

Raw land is among the oldest and most durable asset classes available to private investors. For the HBCU community — individuals, families, alumni associations, and institutional partners — it is also among the most underutilized.

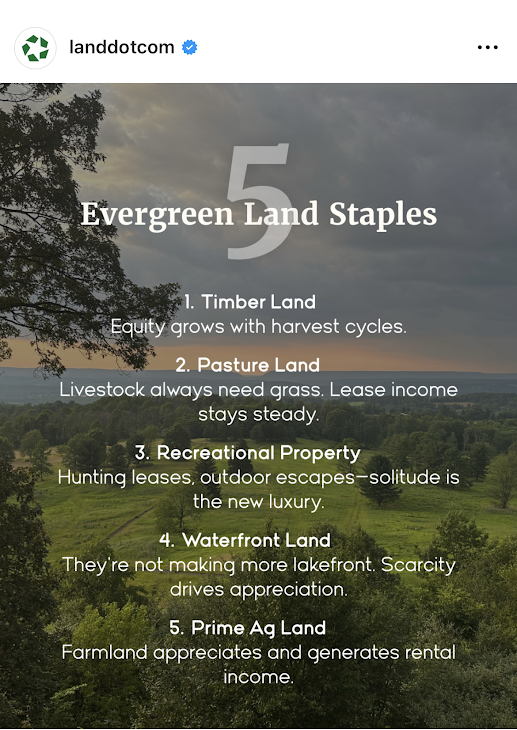

There is a social media post circulating in land investment circles that reads simply: “Forget the luck of the Irish. We prefer the certainty of a deed.” Beneath that caption sits a framework titled “5 Evergreen Land Staples” — timberland, pastureland, recreational property, waterfront land, and prime agricultural ground — each chosen for the same fundamental quality: enduring income or appreciation that does not require the daily volatility management of equities or the tenant fragility of residential real estate. The post is from Land.com, a mainstream marketplace catering primarily to rural landowners. The audience it implicitly addresses is white, rural, and generationally landed. Yet the analytical framework it articulates is precisely what the African American institutional ecosystem needs to operationalize and the HBCU community, with its networks of graduates, alumni chapters, and anchor institutions spread across the American South and beyond, is uniquely positioned to execute it at scale.

The stakes are not trivial. As the Federation of Southern Cooperatives Land Assistance Fund has documented, African Americans own less than 1% of all privately owned rural land in the United States. That figure represents one of the most consequential economic collapses in modern American history, a loss that accelerated across the 20th century through discriminatory lending, heirs’ property dispossession, and the systematic exclusion of Black farmers from federal agricultural credit systems. Between 1910 and 2020, African American land ownership fell by roughly 90%, from an estimated 15–16 million acres to less than 2 million today. Reversing even a fraction of that trajectory requires not only individual decision-making but coordinated institutional action. This article maps a practical framework anchored in the five evergreen land categories for how African Americans at every life stage, and HBCU-affiliated institutions at every organizational level, can begin to build durable land portfolios through structures that keep capital inside the ecosystem.

Before addressing who should invest and how, it is worth establishing why the five categories on that social media post represent genuinely strategic holdings rather than speculative fashions. Timberland is distinctive because its primary asset — standing timber — continues growing in value as long as it stands. As one institutional investor noted at the 2009 Timberland Investment World Summit, timber was the only major asset class not to decline during the Great Recession: “As long as the sun is shining trees will grow and your timber’s value will increase.” For long-horizon investors, which includes endowments, alumni foundations, and family trusts, timberland offers inflation protection, biological growth as a return mechanism, and periodic harvest income that can be timed to liquidity needs. Pastureland generates recurring lease income from ranchers and livestock operators with relatively low management overhead, while the underlying land appreciates over time and the lessee carries operational risk. For a first-generation land investor or a young family with limited bandwidth for active management, a leased pasture parcel generates cash flow from day one. Recreational property, including hunting and fishing grounds, has benefited from the structural shift toward experiential consumption, outdoor recreation spending in the United States now exceeds $780 billion annually and the demand for private access through leased hunting rights or short-term rentals has made rural recreational parcels a viable income source even at modest scale. Waterfront land commands a persistent scarcity premium, as lakefront, riverfront, and coastal parcels face an absolute supply constraint that no amount of construction can remedy, with appreciation rates for quality holdings historically outpacing inland equivalents by substantial margins. Prime agricultural land, the fifth category, combines appreciation and income in proportions that no other asset class consistently replicates, with farmland producing positive real returns in nearly every decade since World War II while the growing global demand for food production adds a structural tailwind that shows no sign of abating.

For the African American individual investor, particularly recent HBCU graduates entering the workforce, raw land is rarely the first investment that financial advisors recommend. Equities, retirement accounts, and residential real estate occupy the conventional hierarchy. This is understandable but strategically incomplete. Raw land, particularly rural parcels in the 10–100 acre range, is far more accessible in price terms than most urban professionals realize. In many parts of the rural South and Midwest, quality pastureland or timberland can be acquired for $1,500–$4,000 per acre, meaning a 20-acre parcel may require a down payment comparable to what urban renters spend in twelve months on housing. The critical discipline for individual investors is to treat the first land acquisition not as a lifestyle purchase but as a strategic asset. A 20-acre timberland parcel generates modest income while the timber matures but builds balance sheet equity that can later be pledged as collateral for subsequent acquisitions, a mechanism that generationally landed families have used for centuries. The key to making this work is choosing land that produces some income immediately, whether through a hunting lease, a hay-cutting arrangement, or a grazing license, so that carrying costs do not exceed cash flow while long-term appreciation accrues. Structurally, individuals should acquire rural land through a single-member LLC rather than in personal name, for both liability protection and eventual transfer efficiency. The LLC structure also allows for the clean addition of family members as equity holders over time, laying the legal groundwork for the next stage of ownership.

A young family with children faces a different calculus than a single investor. The time horizon extends to 30 or 40 years, the need for tax-efficient transfer becomes relevant, and the question of heirs’ property known as the informal, undivided ownership arrangement that has caused the dispossession of millions of acres of Black-owned land must be proactively addressed from the first deed. Heirs’ property arrangements leave undivided interests in land vulnerable to partition sales, through which any one heir can force a sale often to outside buyers at below-market prices. A young family acquiring land today should structure the purchase inside a family LLC or land trust from inception, with a clear operating agreement specifying decision-making rights, buyout provisions, and management authority. This structural discipline costs several hundred dollars in legal fees at formation but eliminates the single greatest mechanism by which Black-owned land has historically been lost. For young families, pastureland and prime agricultural ground are the most suitable of the five categories. Leased to a working farmer on an annual or multi-year cash rent arrangement, these parcels generate predictable income typically $100–$300 per acre annually in productive regions while the family’s equity compounds. Agricultural land near HBCUs, particularly the 1890 land-grant institutions with active extension programs, offers an additional advantage: the university’s agronomic and soil science resources can improve the land’s productivity and rental value over time, particularly where a formal university-farmer partnership exists.

For African American households in the wealth-accumulation or pre-retirement phase, typically those between 45 and 65 with existing equity in residential real estate or retirement accounts, raw land fills a specific portfolio gap. It provides non-correlated returns, inflation protection, and estate planning flexibility that equity-heavy portfolios lack. At this stage, the five-category framework can be pursued more deliberately. Waterfront land and timberland, which require longer holding periods to realize full appreciation, are most appropriate for mature investors who do not need near-term liquidity. A modest timber holding, held for 20 years through a managed investment timberland organization, can produce both periodic harvest income and terminal land value appreciation that substantially outpaces a bond portfolio over the same horizon. Conservation easements on qualifying land parcels offer an additional mechanism: by granting a qualified land trust a permanent easement that restricts development, the landowner receives a federal income tax deduction equal to the value of the development rights surrendered, a tool that high-income African American professionals have underutilized relative to white rural landowners who have deployed it extensively. This is also the stage at which entry into private Real Estate Investment Trust structures becomes viable. A private REIT organized around agricultural or timberland holdings allows a group of accredited investors like friends, family members, or professional associates to pool capital into a formal investment vehicle with a shared land portfolio, professional management, and pass-through tax treatment. Unlike publicly traded REITs, a private land REIT can be sized for a community of 10–50 investors, managed by a professional trustee, and built specifically around the five evergreen categories. The formation cost is meaningful but amortizes quickly across the investor pool, and the structure creates a formal institutional container for what would otherwise remain fragmented individual decisions.

Not every land investment begins with a formal institutional structure. Some of the most durable private wealth in America was built by small groups of trusted individuals such as former college roommates, fraternity and sorority members, professional cohort peers who pooled capital informally before any institution took notice. For the HBCU community, this peer-to-peer investment model is both historically familiar and structurally underdeployed. A group of five former classmates, each contributing $10,000, creates a $50,000 acquisition fund. In rural land markets across the South, that capital is sufficient to purchase 15–30 acres of quality pastureland or recreational property with room for closing costs and an operating reserve. The land is titled inside a jointly owned LLC, the operating agreement governs decision-making and buyout rights, and the group begins building a shared balance sheet that none of them could have assembled individually on the same timeline. The social infrastructure already exists. HBCU alumni networks are among the most tight-knit in American higher education, and the bonds forged between classmates across Greek organizations, residence halls, student government, and athletic programs carry the relational trust that small investment partnerships require above all else. What is missing is not the social capital but the financial framework to convert it into land equity. The practical steps are straightforward: the group agrees on an investment policy covering land category, geographic focus, minimum hold period, and income distribution schedule; forms an LLC with an operating agreement drafted by a real estate attorney; designates a managing member responsible for vendor relationships, lease management, and annual reporting; and commits to a first acquisition within a defined timeframe, preventing the initiative from dissolving into indefinite planning. Over time, these peer land partnerships can grow through reinvested income, additional capital calls, and the addition of new members at formally appraised entry valuations. A group that begins with five classmates and 25 acres can, within a decade of disciplined reinvestment, hold a diversified portfolio spanning multiple land categories across several states anchored not by institutional mandate but by the simple decision of like-minded people to build something together.

HBCU alumni associations sit at the intersection of institutional loyalty and latent investment capital. Most chapters hold reserve funds that have been accumulated through dues, fundraising, and event revenue that are parked in bank accounts earning negligible interest. Very few chapters have formalized investment policies, and this represents one of the most tractable missed opportunities in the HBCU ecosystem. An alumni chapter with $200,000 in reserves can, with proper legal structuring, become a founding limited partner in a private land REIT or a land investment LLC alongside other chapters. Five chapters pooling $200,000 each creates a $1 million acquisition fund capable of purchasing 250–500 acres of quality pastureland, timberland, or agricultural ground in rural markets adjacent to HBCUs. That land, leased and managed professionally, generates annual income that returns to the chapters while the underlying asset appreciates. Over a 15-year horizon, the portfolio can be refinanced to fund new acquisitions replicating the leverage cycle that institutional endowments have used with alternative assets for decades. The governance structure matters enormously. An alumni land partnership should be organized as a limited partnership or private REIT with an independent general partner or trustee, clear investment policy statements, annual audited financial statements, and a defined liquidity event horizon. The informality that characterizes most alumni chapter finances is incompatible with institutional land ownership at scale. But with proper structuring, the alumni network becomes what it has always had the potential to be: a distributed institutional investor class with shared objectives and collective bargaining power. Nationally coordinated alumni associations, the general alumni bodies of the major HBCU systems, are positioned to act at an even larger scale. A national alumni association with 50,000 dues-paying members and a modest per-member investment program could capitalize a seven-figure land acquisition fund within a single fiscal year. Structured as a private REIT with a land-grant mission overlay, specifically acquiring land adjacent to 1890 HBCU campuses or in counties with high concentrations of African American agricultural heritage, such a fund would generate financial returns while simultaneously reinforcing the geographic and economic footprint of the institutions themselves.

The structure of land acquisition matters as much as the acquisition itself, and for the African American investor at every level — individual, family, peer partnership, or alumni association — the financing institution is a strategic choice, not merely a transactional convenience. African American-owned banks hold just $6.4 billion in assets, while African American credit unions hold $8.2 billion, meaning these institutions together control less than $15 billion in combined lending capacity despite serving a market of more than 40 million people — insufficient to exert meaningful influence in national credit markets without deliberate capital infusion from within the community itself. When an African American investor finances a land purchase through a Black-owned bank or credit union rather than a mainstream white-owned lender, the mortgage deposit strengthens that institution’s liquidity ratio, expands its lending capacity through fractional reserve multiplication, and keeps the interest income circulating within the ecosystem rather than exiting to a Wall Street balance sheet. Every dollar deposited into an African American financial institution can translate into multiples of additional lending capacity once multiplied through the banking system — meaning that the collective financing decisions of HBCU alumni and community investors are not merely personal financial choices but acts of institutional capitalization. A community that builds land equity through Black-owned financial institutions simultaneously strengthens two pillars of its economic architecture: the land base that generates long-term wealth and the banking infrastructure that finances the next generation of acquisition.

At the institutional tier, the strategic imperative is even more pronounced. As of 2014, Tuskegee University controlled approximately 5,000 acres, ranking 12th among all American colleges in total land holdings, while Alabama A&M (2,300 acres), Alcorn State (1,756 acres), Prairie View A&M (1,502 acres), Kentucky State (915 acres), and Southern University (884 acres) collectively controlled more than 12,000 acres, placing all six among the top 100 college landowners in the United States. Those figures have not been comprehensively updated in the intervening decade, and the actual current land position of these institutions accounting for acquisitions, dispositions, and reclassifications likely differs. What has not changed is the strategic imperative to treat that land base as a productive investment asset rather than passive institutional real estate. A coordinated commitment of $1 million from each of the nineteen 1890 land-grant HBCUs would create a $19 million revolving fund capable, through its placement in African American banks and credit unions, of generating $7–$10 in agricultural lending capacity for every dollar committed financing not just land acquisition but the full productive cycle of African American farming. That mechanism addresses credit access. The complementary challenge is equity accumulation: deploying HBCU endowment capital, alongside alumni and friends’ capital, into the five evergreen land categories through a structured private REIT. An HBCU-anchored land REIT, capitalized with institutional endowment commitments as the senior tranche and alumni association and individual investor capital as subordinate tranches, would create a properly tiered investment structure with aligned incentives. The endowment’s priority return on its senior capital is protected; alumni investors participate in the upside above that hurdle; and the land itself remains in community-aligned ownership regardless of which investor class holds primacy at any given moment. Over time, the REIT’s land holdings can be diversified across all five evergreen categories — timberland for long-horizon appreciation, pastureland and agricultural ground for current income, waterfront parcels for high-appreciation positioning, and recreational property for near-term income generation — creating a portfolio whose income streams are non-correlated and whose asset values compound independently of equity market cycles.

The five evergreen land categories are individually sound investment ideas. Their strategic power for the HBCU community, however, lies not in isolated individual transactions but in the construction of a layered, coordinated ecosystem from the 22-year-old HBCU graduate purchasing her first 20-acre pasture parcel in Alabama, to the alumni chapter launching a multi-state agricultural REIT, to the 1890 HBCUs deploying endowment capital as the institutional anchor of a Black-managed timberland fund. At the most fundamental level, virtually every economic system man has ever created relies on one undeniable truth: whoever controls the land controls the system. The African American institutional ecosystem has the networks, the talent, and increasingly the structured financial vehicles to re-enter land ownership at meaningful scale. What it requires now is the strategic coordination to treat land not as a nostalgic aspiration but as a compounding institutional asset — one deed, one acre, one fund at a time.

Disclaimer: This article was assisted by ClaudeAI.

The South never stopped fighting the Civil War. It was the Cold War before the Cold War with USSR and it has been the Cold War after the USSR collapsed. America’s greatest war has always been within. The North, then and for too long thereafter thought it could give an inch and welcome its southern brethren back, but a mile and then some were taken. At this moment, all that remains for the South to conquer is the taking of the North’s financial capital from New York and it will have – checkmate. The South has risen and won. – William A. Foster, IV

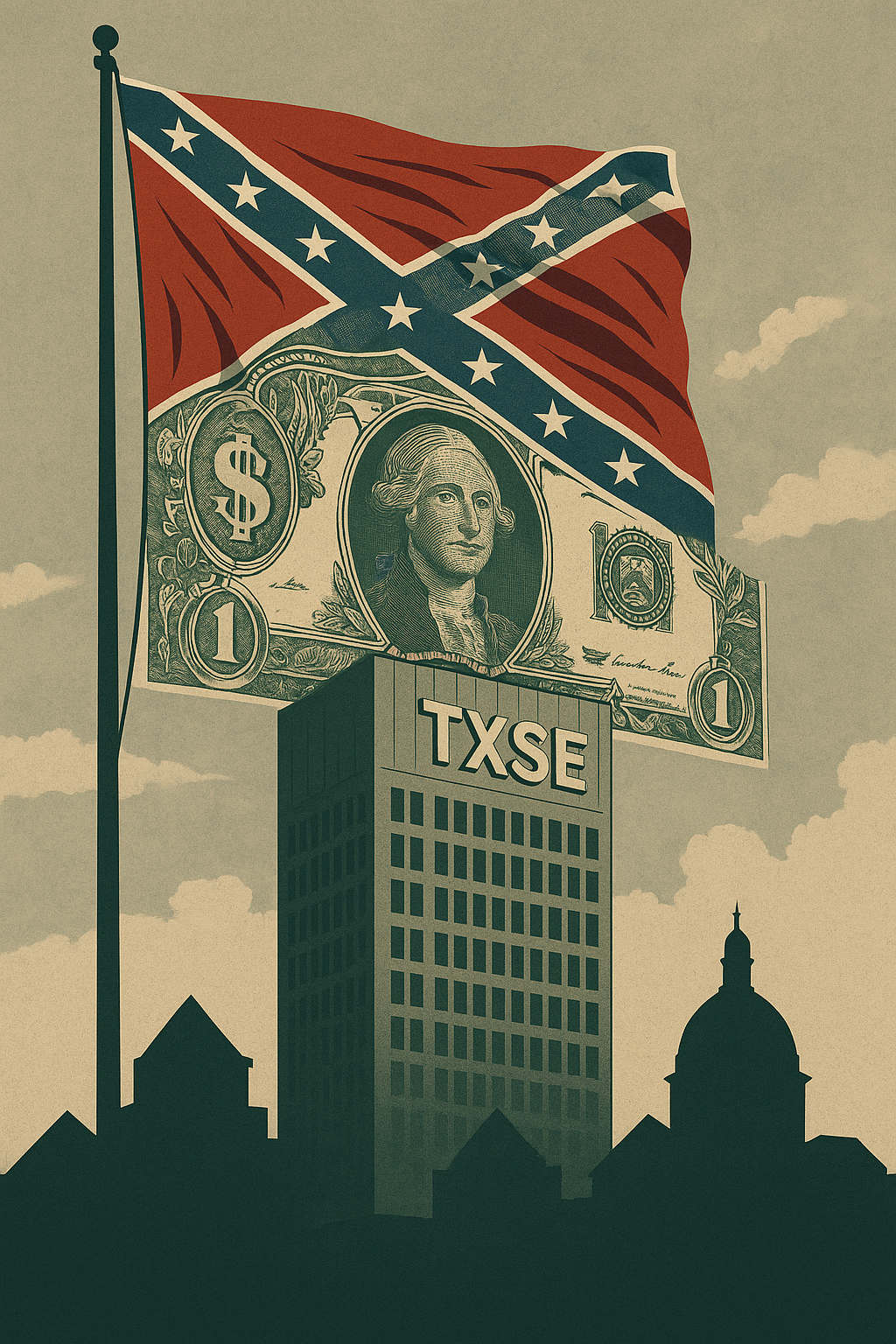

The United States has never had a single center of financial power, but it has never had one this far south either. The Texas Stock Exchange — TXSE — formally launching in 2025, is not a regional curiosity. It is the institutional centerpiece of a coordinated effort to reshape who controls the rules of American capital markets, and the African American institutional ecosystem has not yet reckoned with what that means for its long-term economic position.

Founded in 2023 and capitalized with $120 million in initial funding from investors including BlackRock, Citadel Securities, Charles Schwab, and Virtu Financial, TXSE is aiming directly at the New York Stock Exchange and Nasdaq. Its headquarters are in Dallas. Its leadership includes former Texas Governor Rick Perry and former Dallas Federal Reserve President Richard Fisher. Its pitch to potential issuers is a governance environment that its founders describe as more CEO-friendly: reduced compliance requirements, streamlined listing rules, and a posture explicitly hostile to the accountability frameworks that have, however imperfectly, created some structural space for African American institutional participation in mainstream capital markets. For the African American institutional ecosystem — HBCUs, Black-owned banks and credit unions, Black-owned companies, professional associations, and the community development financial institutions that serve communities mainstream finance has historically ignored — this is not a distant policy question. It is a direct threat to the ownership architecture that the community is still trying to build.

To understand TXSE requires understanding the political economy of the modern South, and that requires a historical anchor. During Reconstruction, African Americans built consequential institutional infrastructure against enormous opposition: Black-owned banks, insurance companies, newspapers, and colleges that competed credibly in American economic and civic life. That infrastructure was not dismantled by market forces. It was dismantled by the same mechanism that has constrained African American institutional ownership in every era — control the rules of the game, and you control who benefits from playing it. The Freedman’s Savings Bank collapsed after federal mismanagement stripped depositors of $3 million in assets. The Greenwood District of Tulsa, the most concentrated expression of African American commercial ownership in the country’s history, was burned in 1921 with official sanction. Across the South and beyond, Black-owned enterprises were regulated out of existence, denied credit access, or destroyed. The consistent instrument was institutional architecture — the deliberate construction of financial rules that embedded the interests of one group at the expense of another. The Texas Stock Exchange is that instrument, updated for the twenty-first century.

Texas has rapidly positioned itself as the national headquarters of the movement to strip social and governance accountability from investment and corporate decision-making. In 2023, Governor Greg Abbott signed legislation banning state contracts with any firm that considers environmental, social, or governance factors in its investment decisions. The state legislature has moved to constrain public pension fund managers from incorporating anything beyond narrow financial return metrics, explicitly prohibiting the mission-aligned investing frameworks that community development financial institutions and HBCU-linked endowment vehicles depend on to justify participation in community-anchored development projects. Florida has enacted parallel restrictions. Oklahoma’s state treasurer blacklisted more than a dozen financial institutions for their stated climate commitments. Tennessee, Georgia, and a growing list of other states are constructing the same legal and financial infrastructure, all oriented toward the same goal: a parallel financial order governed by Southern political priorities, insulated from federal regulatory oversight and from the investment norms of the institutions that have grudgingly made room for African American institutional participation. What HBCU Money has documented over years of covering African American institutional finance by highlighting the slow erosion of Black-owned banks, the chronic undercapitalization of HBCU endowments, the failure of institutional capital to circulate within the African American ecosystem is now confronting a coordinated counterforce operating with the full backing of state governments, sovereign-scale endowments, and the largest names in global finance.

TXSE’s proposed listing standards deserve careful scrutiny because their effect on African American institutional economic participation is structural, not incidental. The exchange plans to impose earnings tests and revenue thresholds that would disqualify an estimated thirty percent or more of companies currently listed on Nasdaq, a category that includes a disproportionate share of minority-led, cooperatively structured, mission-driven, and early-stage enterprises. The cooperative structures, community development financial institutions, and early-stage technology firms that represent the growth edge of African American institutional economic activity are precisely the kinds of entities these standards are calibrated to exclude. Simultaneously, Texas has enacted legislation limiting shareholder lawsuits unless investors own at least three percent of a company’s shares. That threshold effectively neutralizes most activist shareholders, including African American pension funds, HBCU endowment investment vehicles, and minority-focused fund managers that rarely accumulate the concentrated positions necessary to meet that bar. The combination is a governance architecture designed to concentrate power among already-powerful institutional insiders and to diminish the accountability levers that African American institutional investors have worked to develop. This is not an accident of design. It is the design.

The University of Texas Investment Management Company — UTIMCO — manages the combined endowments of both the University of Texas System and the Texas A&M System. Together, these pools constitute one of the largest publicly managed academic endowment complexes in the United States, surpassing Harvard in combined assets under management. UTIMCO has, under sustained pressure from the Texas conservative political establishment, moved aggressively to align its investment posture with the ideological priorities of state leadership. It has reduced exposure to investment vehicles that incorporate social or governance accountability factors and directed assets toward domestic energy production, real estate, and financial instruments consistent with what its political overseers consider appropriate. UTIMCO’s scale gives it significant market-moving influence. Its alignment whether formal or informal with the TXSE project represents a formidable concentration of institutionally managed capital operating explicitly outside the accountability frameworks that African American institutional investors have built their participation strategies around. HBCU endowments hold a combined base that, while growing, remains dwarfed by what UTIMCO alone commands. The strategic implication is direct: when the largest endowment systems in the South are operating with an investment philosophy that excludes the governance accountability frameworks African American institutions depend on, the negotiating position of those institutions in the broader capital market is weakened.

The direct risks to African American institutional ownership are compounding across three distinct dimensions. The first concerns the exclusion of Black-led enterprises from the visibility, liquidity, and valuation premiums that accompany public market access. HBCU Money has documented that African American-owned employer businesses generated $212 billion in combined revenue in 2022 — a figure that, while representing meaningful growth, amounts to 0.43 percent of total U.S. business revenue for a community that constitutes over fourteen percent of the population. The exchange listing premium with the ability to attract institutional capital, establish a public valuation, and access the equity markets for growth financing has historically been one of the structural mechanisms that translates enterprise scale into compounding institutional wealth. TXSE’s listing standards are calibrated against the cooperative enterprises, CDFIs, and early-stage technology firms at the growth edge of African American institutional economic activity. Without access to a major exchange platform, these firms face persistent disadvantages in attracting the institutional capital that would allow them to scale. Over time, this structural exclusion deepens the ownership gap not through any single discriminatory act, but through the cumulative operation of market design.

The second dimension of risk concerns HBCU endowments and the broader African American institutional investment ecosystem. As HBCU Money has reported, African American-owned banks currently hold approximately $6.4 billion in combined assets — down from forty-eight institutions in 2001 to just seventeen today, and down from a peak share of 0.2 percent of total U.S. banking assets in 1926 to 0.027 percent today. HBCU endowments are managed, in most cases, through large fund managers some of whom are direct investors in the TXSE. As the exchange scales and as its listed companies grow in market capitalization, passive investment vehicles and actively managed funds will increasingly hold TXSE-listed assets as a matter of index composition and portfolio construction. HBCU endowment pools, pension funds serving African American public employees, and investment vehicles managed on behalf of Black institutional clients could find themselves indirectly capitalizing an exchange whose structural design, governance philosophy, and political alignment work against African American institutional interests. Annual interest payments transferred from Black households to non-Black financial institutions are estimated at approximately $120 billion — more than half of what all Black-owned businesses generate in revenue in an entire year. TXSE’s governance model is structured to compound that dynamic, not to reverse it.

The third and most consequential dimension concerns the governance architecture within which African American institutional ownership operates in publicly listed companies more broadly. The decades-long effort to increase African American representation in corporate governance, to build institutional investor coalitions capable of pressing for equitable accountability, and to develop shareholder advocacy tools that translate institutional capital into institutional voice has depended on an exchange and regulatory environment that, however reluctantly, created minimum conditions for accountability. TXSE’s governance philosophy centered on limiting shareholder litigation, reducing disclosure requirements, and eliminating the governance frameworks that allowed accountability advocacy to function would, if it achieves the national scale it is pursuing, erode the leverage that African American institutional investors have slowly accumulated. This is not a threat to abstract norms. It is a threat to the concrete mechanisms through which African American institutional capital translates into institutional power.

There is a cultural branding dimension to TXSE that should not be dismissed as mere marketing, because culture and capital are not separate categories they are the same category expressed differently. TXSE supporters have embraced the ‘Y’all Street’ branding, positioning Dallas as the spiritual and institutional opposite of what they call ‘woke capital.’ The slogans — ‘Texas roots. Global reach,’ ‘Built for CEOs, not bureaucrats’ — are explicit declarations of institutional identity. They communicate to potential issuers what governance norms the exchange will enforce, and they communicate to African American institutional stakeholders what norms will be conspicuously absent. An exchange that markets itself as the home of American finance divorced from social accountability is not making a neutral statement about regulatory philosophy. It is announcing its constituency. For the African American institutional ecosystem, that announcement should carry the same interpretive weight as any other structural signal about where capital will and will not flow.

The strategic response available to African American institutions is not the construction of a competing exchange. That framing misreads both the competitive dynamics of exchange infrastructure and the actual leverage points available. Exchanges are winner-take-most infrastructure. TXSE enters the market with $120 million in capitalization, the institutional backing of the largest names in global finance, and the network effects of a state government willing to direct sovereign-scale endowment capital in its direction. A Black-led exchange starting from zero cannot compete with that on equivalent terms in the near term, and proposing otherwise is not strategy — it is aspiration dressed as a plan. The more consequential response is coordinated institutional non-participation: the deliberate, organized withdrawal of African American institutional capital from TXSE’s orbit, combined with the systematic redirection of that capital toward institutions and instruments that serve African American ownership interests. This is not the high road. It is the only road with actual traction.

Executing that response, however, requires an honest accounting of which African American institutions are actually free to act and that accounting begins with the distinction between public and private HBCUs. The majority of HBCUs are public institutions, and the majority of public HBCUs are located in precisely the Southern states that are constructing the Southern Capital Doctrine. Southern University operates under the authority of the Louisiana Board of Regents. Florida A&M is a Florida state institution. North Carolina A&T, Prairie View A&M, Alabama State, Jackson State each operates within a state governance structure that gives hostile state legislatures direct leverage over budget, investment policy, and institutional positioning. These institutions cannot unilaterally reallocate endowment assets, cannot take public institutional positions against the financial policies of their host states, and in many cases cannot even direct their banking relationships without navigating state procurement rules that route dollars away from Black-owned institutions. Asking public HBCUs to lead the charge against TXSE is asking institutions to act against the direct interests of the governments that control their operating budgets. That is not a realistic foundation for strategy.

The private HBCUs occupy a structurally different position. Howard, Morehouse, Spelman, Hampton, Tuskegee, Xavier, Dillard, and their peer institutions have independent governance, control their own endowment investment decisions, and face no state legislative veto over their financial positioning. They are the tier of the HBCU ecosystem with the freedom to act directly to reallocate endowment capital away from fund managers backing TXSE, to direct institutional deposits toward Black-owned banks, to take explicit public positions on exchange governance policy, and to convene the broader institutional conversation that a coordinated response requires. The scale of their endowments, while modest relative to their peer institutions in the broader higher education landscape, is sufficient to establish meaningful momentum if directed in concert. Howard University’s endowment alone, if managed with the strategic intentionality that this moment demands, could anchor a coalition capable of making market-visible moves. Private HBCUs have the freedom that public HBCUs do not. The question is whether they will exercise it.

But the public HBCU ecosystem is not, for this reason, strategically irrelevant. It simply operates through a different institutional layer one that is frequently overlooked precisely because it does not appear on the official organizational chart. Every public HBCU has an alumni association that is legally and operationally independent of the institution itself. Every public HBCU has a foundation, a separately incorporated philanthropic entity with its own board, its own investment decisions, and its own capacity to act without state legislative approval. The Prairie View A&M National Alumni Association is not a Texas state agency. The Southern University Foundation is not subject to the Louisiana Board of Regents. The alumni associations and foundations of public HBCUs can bank with Black-owned financial institutions, direct philanthropic capital toward CDFIs, take public positions on financial policy questions, and coordinate with private HBCUs in ways that the institutions themselves cannot. If that coordination is sufficiently explicit and sustained, the functional effect is equivalent to the institution acting even though technically it is not. This is not a workaround. It is how every other community with sophisticated institutional strategy operates. The university cannot endorse a candidate. The alumni PAC can. The university cannot divest from a financial institution. The foundation can choose where to bank. The structure already exists. It simply has not been deployed with this level of strategic intention.

This layered architecture suggests a three-tier framework for the African American institutional response to TXSE. The first tier consists of private HBCUs acting as direct institutional agents reallocating endowment capital, directing deposits, and convening the policy conversation. The second tier consists of public HBCU alumni associations and foundations acting as coordinated proxy agents making the investment and banking decisions the institutions themselves cannot make, in deliberate alignment with the strategic direction being set by private HBCUs in the first tier. The third tier consists of the broader African American institutional network — Black-owned banks and credit unions, Black-owned firms, the Thurgood Marshall Fund and UNCF, the HBCU Faculty Development Network, African American professional associations, and African American-controlled pension and foundation assets — functioning as the connective tissue that allows the first two tiers to operate in concert without requiring any single institution to take a politically exposed position alone. Jewish American institutional strategy has operated through exactly this kind of layered coordination for generations. Korean rotating credit associations, Indian American technology sector networks, and Irish American political machines have each built equivalent structures calibrated to their specific institutional contexts. The African American community has all of the institutional components. It has not yet assembled them into a coordinated response mechanism.

On the question of regulatory engagement, intellectual honesty requires acknowledging the political environment directly. Petitioning the current Securities and Exchange Commission for intervention in TXSE’s governance standards is not a realistic near-term lever. The present administration’s posture toward exchange regulation, and toward the financial accountability frameworks that any such petition would invoke, makes meaningful regulatory relief under current leadership implausible. The more strategically sound approach is to build the legal and analytical record now to commission the research, document the structural exclusions, develop the regulatory theory, and position African American institutional stakeholders to arrive at a future administration’s SEC with a fully developed dossier rather than a reactive complaint. This is not passivity. It is the institutional discipline of building for the long game. Every dollar spent on legal analysis and regulatory documentation today is leverage that compounds when the political environment changes. TXSE is not going away. Its governance standards will be litigated and legislated over decades, not months. The community that has done the analytical work in advance will have the most influence over how that process resolves.