We are forced to trust the very institutions who stole the land in the first place because we have not developed and maintained our own. – William A. Foster, IV

A grandfather in Wilcox County plants loblolly pine on forty acres in 1961, the year the trees will outlive him being the whole point. He tells his children the timber is not for cutting; it is for holding. When he dies without a will, the forty acres become the property of nine heirs, then, a generation later, of thirty-one. No bank will lend against a title held by thirty-one people who cannot agree to sign the same document. The family calls the county forester listed on the state’s directory, the only one covering their district, because there is no other option in the phone book and no other name anyone in the family has ever heard mentioned with trust. The advice that comes back is vague, the timeline uncertain, and there is no second opinion to check it against, no other firm to call, no one who looks like the family sitting across the table. The pines keep growing, undermanaged not for lack of care but for lack of anywhere safe to take that care. Forty years after planting, a timber company buys out the confused heirs for a fraction of the standing timber’s value, and the grandfather’s patient capital becomes someone else’s harvest.

That scene is not a story about one bad forester or one unlucky family. It is a story about what happens when an entire asset class has exactly zero Black-owned institutions capable of serving it; no brokerage, no financing arm, no forestry consultancy, no appraisal firm built by and accountable to the community whose land is on the table. For nearly every other category of wealth-building infrastructure, HBCU Standard has documented at least a partial institutional base: Black-owned banks and credit unions, Black-owned commercial real estate firms, Black-owned construction companies. In rural land and timberland specifically, a category increasingly discussed as an inflation hedge, a carbon-credit asset, and a durable multigenerational holding — that base does not exist. Not a small one. Not a regional one. None. And the absence does not simply mean missed opportunity. It means that every African American family holding rural land, and every one considering buying it, is doing so without the single thing that would let them tell the difference between good advice and bad: a trusted counterparty inside the industry with something to lose if it gets that advice wrong.

This is the predicament worth naming plainly. A family that already holds land has, in most of the rural South, exactly one state district forester assigned to their county, no competing Black-owned firm to call for a second opinion, and no institutional recourse if that forester’s guidance turns out to serve someone else’s interests rather than theirs. A family looking to buy timberland as an asset has no Black-owned equivalent of a firm like Hall and Hall, which does not simply broker land but finances it directly, offering loan programs ranging from low variable rates to full thirty-year fixed terms so a client can originate, appraise, and fund an acquisition inside a single relationship. That vertical integration is precisely what makes an institution durable across a timber rotation: the same firm that helps a client find and value a parcel can also lend against it, rather than sending the client back out to a separate lender with no connection to the land or the deal.

To understand why that absence matters, it helps to see what a firm like Hall and Hall actually does, because it bears almost no resemblance to the real estate transaction most readers know from buying a house. A residential agent lists a property, compares it against recent sales of similar homes nearby, and hands the buyer off to a conventional mortgage lender who underwrites based on the buyer’s income and an appraiser’s estimate of the house’s value alone. None of those tools transfer to timberland. Valuing a working forest requires an actual cruise of the standing timber; a forester physically walking the property to inventory species, age, volume per acre, and growth rate because the trees themselves are a separate, living asset with their own market price, layered on top of the bare land value, changing every year whether anyone touches it or not. Financing the purchase means underwriting against decades of projected harvest income, and often against secondary income like grazing or hunting leases, rather than a buyer’s fixed monthly paycheck, which is why Hall and Hall runs its own loan programs instead of referring clients to a bank teller. And the transaction itself carries considerations a residential closing never touches: mineral rights that may or may not convey with the surface, water rights in Western states, conservation easements that permanently restrict future use in exchange for tax benefits, access easements across neighboring land, and a formal management plan for what happens to the timber over the next thirty years, not just what happens at the closing table. A firm built to handle all of that under one roof, continuously, is a fundamentally different kind of institution than a residential brokerage that occasionally lists rural acreage on the side and it is exactly why calling a local real estate agent, however well-intentioned, is not a substitute for the thing that’s missing.

No Black-owned firm offers any piece of that stack, let alone all of it. A family that finds its way past appraisal and negotiation on its own still has to secure financing from an institution outside the community entirely often the very kind of lender whose historical record with Black landowners is the reason for caution in the first place.

That wariness is not paranoia. It has a documented record behind it. Pigford v. Glickman, settled in 1999 as one of the largest civil rights settlements in American history, established in federal court that the USDA had systematically discriminated against Black farmers in the allocation of farm loans and disaster assistance between 1981 and 1996 delaying and denying credit that white farmers received routinely, and for over a decade failing to functionally operate the very civil rights office meant to investigate complaints about it. Congress appropriated another $1.2 billion in 2010 for a second settlement, Pigford II, because so many farmers with legitimate claims had been unable to file the first time. This is not ancient history from the era of outright land theft after emancipation. It is a pattern of institutional behavior toward Black landowners that persisted into living memory, inside the very federal agency structure that state and district foresters, county extension offices, and agricultural lenders all sit within. A family that has watched that pattern play out in the district office, in the bank, sometimes in their own family’s dealings with a local forester has every reason to want a trusted, accountable alternative before signing anything. The absence of that alternative is the actual risk, not an inconvenience layered on top of one.

Layer the heirs’ property problem on top of that trust deficit and the predicament compounds rather than adds. Research out of the University of Georgia’s Warnell School of Forestry has documented how clouded title land passed down without a will, held as an undivided interest among a growing number of descendants locks families out of financing, cost-share programs, and professional forest management, because no lender or agency wants to deal with an ownership structure that any single heir could blow up with a partition sale. Resolving that title requires legal expertise most families cannot afford and most local firms are not built to provide with any particular care. Mavis Gragg’s organization HeirShares exists specifically to clear these legal pathways, and the Federation of Southern Cooperatives has run a Land Assistance Fund toward the same end for decades. But neither is a brokerage, a lender, or a forestry management firm. They can help a family reach clean title. They cannot then walk that family through financing a thinning operation, negotiating a fair timber sale, or acquiring a second parcel to expand the holding, the actual services a firm like Hall and Hall provides continuously to the families who already trust it. Clearing title without a trusted destination to route the resulting clean parcel toward simply relocates the risk rather than resolving it.

The scale of what’s been lost while this institutional vacuum sat unfilled is worth stating plainly, in the register this publication uses for these numbers rather than the multi-trillion projections other outlets reach for. In 1910, according to the National Forest Foundation, Black Americans owned 195 timber companies and comprised roughly a quarter of all employees in the forest products industry. By 1920, per the Land Trust Alliance, African American farmers controlled approximately 14 percent of the nation’s farmland; today that figure is under 1 percent, and total African American land ownership across every category; timberland, farmland, residential, everything has fallen from an estimated 15 to 16 million acres to under 2 million. Set that number against a single entry on the Land Report’s 2025 ranking of America’s largest private landowners: the Emmerson family, through Sierra Pacific Industries, holds 2.44 million acres of timberland in California, Oregon, and Washington alone more than the entirety of Black land ownership nationwide, across every category, combined. John Malone holds roughly 2.2 million acres across four states. The Reed family’s Green Diamond Resource Company, built from a Pacific Northwest logging operation started in 1897, holds about 2.1 million acres. Each of those holdings is the product of a century or more of uninterrupted institutional continuity: clean title passed down without interruption, financing relationships maintained across generations, professional forestry management retained continuously rather than improvised family by family. That continuity is precisely what heirs’ property and the absence of a trusted institutional counterparty have made structurally difficult for Black landowners to replicate, no matter how much care any individual family brings to the effort.

None of this argues that timberland is a bad asset for African American families to hold or acquire. It argues the opposite: that the fundamentals of the asset class; steady periodic cash flow from harvests, low correlation with equity markets, a growing carbon-credit revenue stream for standing forest, and a purchase price still within reach of pooled institutional capital make it exactly the kind of holding worth building durable infrastructure around. And the talent to staff that infrastructure is not the missing piece. Alabama A&M University, one of the nineteen 1890 land-grant HBCUs rather than one of the handful of flagship HBCUs (Howard, Morehouse, Spelman) usually invoked in this conversation, runs the only professionally accredited forestry degree at an HBCU and operates as a USDA Forest Service Center of Excellence. Southern University and A&M College in Baton Rouge, part of the only historically Black land-grant university system in the country, offers a bachelor’s, master’s, and Ph.D. in Urban Forestry through a program it describes as the most comprehensive of its kind in the nation. Tuskegee University runs combined forestry programs with Auburn, Iowa State, the University of Michigan, and Idaho State, sending its students on to finish accredited degrees at partner institutions. And a partnership dating to 1993 between the U.S. Forest Service and four HBCUs; Alabama A&M, Southern, Tuskegee, and Florida A&M has, according to the Forest Service’s own national diversity student programs manager, trained two-thirds of the Black foresters currently working inside the agency. That is not a thin pipeline. It is a substantial, decades-old talent base, producing credentialed foresters at meaningful scale, virtually none of whom currently have the option of being hired into a private Black-owned brokerage, appraisal, or land-management firm because no such firm exists to hire them. The gap in this asset class was never expertise. It is the institution that expertise would staff.

What the Wilcox County family needed in 1961, and what a family looking to buy its first parcel of timberland needs today, is the same thing: an institution built specifically to hold this asset class the way Sierra Pacific and Green Diamond hold theirs, financed the way Hall and Hall finances its own clients’ acquisitions, staffed by graduates of Alabama A&M, Southern, and Tuskegee who are accountable to the community whose trust the industry has not yet earned, and structured to move a family from clouded title through financing through active management without ever requiring them to extend blind faith to a district office or an outside lender with no history of earning it. Every piece of that institution’s eventual capability already exists somewhere, disconnected from the others; title-clearing organizations, a credentialed forestry pipeline, cooperative land trusts, community capital sitting in Black-owned banks and HBCU endowments. Coordinating those pieces into one accountable, professionally staffed, vertically financed institution is not a distant aspiration. It is the specific, buildable answer to a specific, well-documented predicament.

The grandfather who planted loblolly pine in 1961 was making an institutional bet without an institution to back it, trusting that the trees, the family, and eventually someone trustworthy to manage them, would all still be standing when the rotation came due. The trees held up their end. What failed was everything around them: the title no bank would recognize, the forester no one had reason to trust, the financing that had to be sought from strangers, the firm that never got built to stand between the family and the forced sale. Until African America has its own version of the institution that holds land the way Sierra Pacific and Green Diamond hold theirs and finances it the way Hall and Hall finances its own, every acre already owned and every acre still to be bought carries a risk no amount of individual caution can fully offset.

Disclaimer: This article was assisted by ClaudeAI.

Land is the only thing in the world that amounts to anything, for it’s the only thing in this world that lasts. It’s the only thing worth workingfor, worth fighting for… – Ted Turner

Raw land is among the oldest and most durable asset classes available to private investors. For the HBCU community — individuals, families, alumni associations, and institutional partners — it is also among the most underutilized.

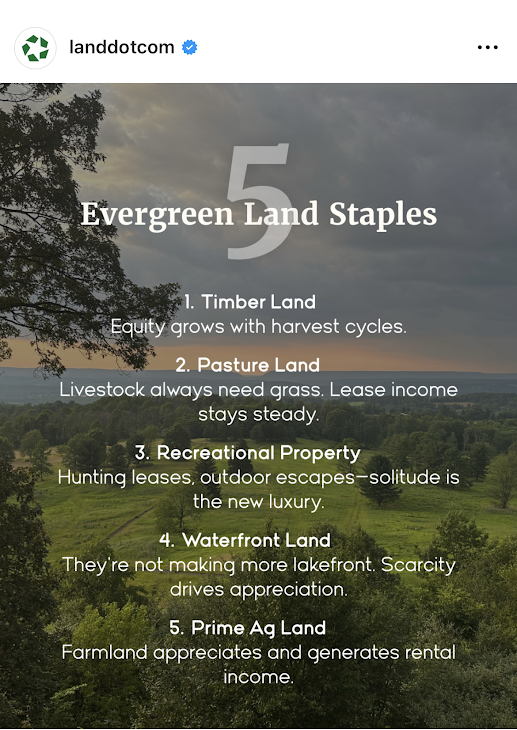

There is a social media post circulating in land investment circles that reads simply: “Forget the luck of the Irish. We prefer the certainty of a deed.” Beneath that caption sits a framework titled “5 Evergreen Land Staples” — timberland, pastureland, recreational property, waterfront land, and prime agricultural ground — each chosen for the same fundamental quality: enduring income or appreciation that does not require the daily volatility management of equities or the tenant fragility of residential real estate. The post is from Land.com, a mainstream marketplace catering primarily to rural landowners. The audience it implicitly addresses is white, rural, and generationally landed. Yet the analytical framework it articulates is precisely what the African American institutional ecosystem needs to operationalize and the HBCU community, with its networks of graduates, alumni chapters, and anchor institutions spread across the American South and beyond, is uniquely positioned to execute it at scale.

The stakes are not trivial. As the Federation of Southern Cooperatives Land Assistance Fund has documented, African Americans own less than 1% of all privately owned rural land in the United States. That figure represents one of the most consequential economic collapses in modern American history, a loss that accelerated across the 20th century through discriminatory lending, heirs’ property dispossession, and the systematic exclusion of Black farmers from federal agricultural credit systems. Between 1910 and 2020, African American land ownership fell by roughly 90%, from an estimated 15–16 million acres to less than 2 million today. Reversing even a fraction of that trajectory requires not only individual decision-making but coordinated institutional action. This article maps a practical framework anchored in the five evergreen land categories for how African Americans at every life stage, and HBCU-affiliated institutions at every organizational level, can begin to build durable land portfolios through structures that keep capital inside the ecosystem.

Before addressing who should invest and how, it is worth establishing why the five categories on that social media post represent genuinely strategic holdings rather than speculative fashions. Timberland is distinctive because its primary asset — standing timber — continues growing in value as long as it stands. As one institutional investor noted at the 2009 Timberland Investment World Summit, timber was the only major asset class not to decline during the Great Recession: “As long as the sun is shining trees will grow and your timber’s value will increase.” For long-horizon investors, which includes endowments, alumni foundations, and family trusts, timberland offers inflation protection, biological growth as a return mechanism, and periodic harvest income that can be timed to liquidity needs. Pastureland generates recurring lease income from ranchers and livestock operators with relatively low management overhead, while the underlying land appreciates over time and the lessee carries operational risk. For a first-generation land investor or a young family with limited bandwidth for active management, a leased pasture parcel generates cash flow from day one. Recreational property, including hunting and fishing grounds, has benefited from the structural shift toward experiential consumption, outdoor recreation spending in the United States now exceeds $780 billion annually and the demand for private access through leased hunting rights or short-term rentals has made rural recreational parcels a viable income source even at modest scale. Waterfront land commands a persistent scarcity premium, as lakefront, riverfront, and coastal parcels face an absolute supply constraint that no amount of construction can remedy, with appreciation rates for quality holdings historically outpacing inland equivalents by substantial margins. Prime agricultural land, the fifth category, combines appreciation and income in proportions that no other asset class consistently replicates, with farmland producing positive real returns in nearly every decade since World War II while the growing global demand for food production adds a structural tailwind that shows no sign of abating.

For the African American individual investor, particularly recent HBCU graduates entering the workforce, raw land is rarely the first investment that financial advisors recommend. Equities, retirement accounts, and residential real estate occupy the conventional hierarchy. This is understandable but strategically incomplete. Raw land, particularly rural parcels in the 10–100 acre range, is far more accessible in price terms than most urban professionals realize. In many parts of the rural South and Midwest, quality pastureland or timberland can be acquired for $1,500–$4,000 per acre, meaning a 20-acre parcel may require a down payment comparable to what urban renters spend in twelve months on housing. The critical discipline for individual investors is to treat the first land acquisition not as a lifestyle purchase but as a strategic asset. A 20-acre timberland parcel generates modest income while the timber matures but builds balance sheet equity that can later be pledged as collateral for subsequent acquisitions, a mechanism that generationally landed families have used for centuries. The key to making this work is choosing land that produces some income immediately, whether through a hunting lease, a hay-cutting arrangement, or a grazing license, so that carrying costs do not exceed cash flow while long-term appreciation accrues. Structurally, individuals should acquire rural land through a single-member LLC rather than in personal name, for both liability protection and eventual transfer efficiency. The LLC structure also allows for the clean addition of family members as equity holders over time, laying the legal groundwork for the next stage of ownership.

A young family with children faces a different calculus than a single investor. The time horizon extends to 30 or 40 years, the need for tax-efficient transfer becomes relevant, and the question of heirs’ property known as the informal, undivided ownership arrangement that has caused the dispossession of millions of acres of Black-owned land must be proactively addressed from the first deed. Heirs’ property arrangements leave undivided interests in land vulnerable to partition sales, through which any one heir can force a sale often to outside buyers at below-market prices. A young family acquiring land today should structure the purchase inside a family LLC or land trust from inception, with a clear operating agreement specifying decision-making rights, buyout provisions, and management authority. This structural discipline costs several hundred dollars in legal fees at formation but eliminates the single greatest mechanism by which Black-owned land has historically been lost. For young families, pastureland and prime agricultural ground are the most suitable of the five categories. Leased to a working farmer on an annual or multi-year cash rent arrangement, these parcels generate predictable income typically $100–$300 per acre annually in productive regions while the family’s equity compounds. Agricultural land near HBCUs, particularly the 1890 land-grant institutions with active extension programs, offers an additional advantage: the university’s agronomic and soil science resources can improve the land’s productivity and rental value over time, particularly where a formal university-farmer partnership exists.

For African American households in the wealth-accumulation or pre-retirement phase, typically those between 45 and 65 with existing equity in residential real estate or retirement accounts, raw land fills a specific portfolio gap. It provides non-correlated returns, inflation protection, and estate planning flexibility that equity-heavy portfolios lack. At this stage, the five-category framework can be pursued more deliberately. Waterfront land and timberland, which require longer holding periods to realize full appreciation, are most appropriate for mature investors who do not need near-term liquidity. A modest timber holding, held for 20 years through a managed investment timberland organization, can produce both periodic harvest income and terminal land value appreciation that substantially outpaces a bond portfolio over the same horizon. Conservation easements on qualifying land parcels offer an additional mechanism: by granting a qualified land trust a permanent easement that restricts development, the landowner receives a federal income tax deduction equal to the value of the development rights surrendered, a tool that high-income African American professionals have underutilized relative to white rural landowners who have deployed it extensively. This is also the stage at which entry into private Real Estate Investment Trust structures becomes viable. A private REIT organized around agricultural or timberland holdings allows a group of accredited investors like friends, family members, or professional associates to pool capital into a formal investment vehicle with a shared land portfolio, professional management, and pass-through tax treatment. Unlike publicly traded REITs, a private land REIT can be sized for a community of 10–50 investors, managed by a professional trustee, and built specifically around the five evergreen categories. The formation cost is meaningful but amortizes quickly across the investor pool, and the structure creates a formal institutional container for what would otherwise remain fragmented individual decisions.

Not every land investment begins with a formal institutional structure. Some of the most durable private wealth in America was built by small groups of trusted individuals such as former college roommates, fraternity and sorority members, professional cohort peers who pooled capital informally before any institution took notice. For the HBCU community, this peer-to-peer investment model is both historically familiar and structurally underdeployed. A group of five former classmates, each contributing $10,000, creates a $50,000 acquisition fund. In rural land markets across the South, that capital is sufficient to purchase 15–30 acres of quality pastureland or recreational property with room for closing costs and an operating reserve. The land is titled inside a jointly owned LLC, the operating agreement governs decision-making and buyout rights, and the group begins building a shared balance sheet that none of them could have assembled individually on the same timeline. The social infrastructure already exists. HBCU alumni networks are among the most tight-knit in American higher education, and the bonds forged between classmates across Greek organizations, residence halls, student government, and athletic programs carry the relational trust that small investment partnerships require above all else. What is missing is not the social capital but the financial framework to convert it into land equity. The practical steps are straightforward: the group agrees on an investment policy covering land category, geographic focus, minimum hold period, and income distribution schedule; forms an LLC with an operating agreement drafted by a real estate attorney; designates a managing member responsible for vendor relationships, lease management, and annual reporting; and commits to a first acquisition within a defined timeframe, preventing the initiative from dissolving into indefinite planning. Over time, these peer land partnerships can grow through reinvested income, additional capital calls, and the addition of new members at formally appraised entry valuations. A group that begins with five classmates and 25 acres can, within a decade of disciplined reinvestment, hold a diversified portfolio spanning multiple land categories across several states anchored not by institutional mandate but by the simple decision of like-minded people to build something together.

HBCU alumni associations sit at the intersection of institutional loyalty and latent investment capital. Most chapters hold reserve funds that have been accumulated through dues, fundraising, and event revenue that are parked in bank accounts earning negligible interest. Very few chapters have formalized investment policies, and this represents one of the most tractable missed opportunities in the HBCU ecosystem. An alumni chapter with $200,000 in reserves can, with proper legal structuring, become a founding limited partner in a private land REIT or a land investment LLC alongside other chapters. Five chapters pooling $200,000 each creates a $1 million acquisition fund capable of purchasing 250–500 acres of quality pastureland, timberland, or agricultural ground in rural markets adjacent to HBCUs. That land, leased and managed professionally, generates annual income that returns to the chapters while the underlying asset appreciates. Over a 15-year horizon, the portfolio can be refinanced to fund new acquisitions replicating the leverage cycle that institutional endowments have used with alternative assets for decades. The governance structure matters enormously. An alumni land partnership should be organized as a limited partnership or private REIT with an independent general partner or trustee, clear investment policy statements, annual audited financial statements, and a defined liquidity event horizon. The informality that characterizes most alumni chapter finances is incompatible with institutional land ownership at scale. But with proper structuring, the alumni network becomes what it has always had the potential to be: a distributed institutional investor class with shared objectives and collective bargaining power. Nationally coordinated alumni associations, the general alumni bodies of the major HBCU systems, are positioned to act at an even larger scale. A national alumni association with 50,000 dues-paying members and a modest per-member investment program could capitalize a seven-figure land acquisition fund within a single fiscal year. Structured as a private REIT with a land-grant mission overlay, specifically acquiring land adjacent to 1890 HBCU campuses or in counties with high concentrations of African American agricultural heritage, such a fund would generate financial returns while simultaneously reinforcing the geographic and economic footprint of the institutions themselves.

The structure of land acquisition matters as much as the acquisition itself, and for the African American investor at every level — individual, family, peer partnership, or alumni association — the financing institution is a strategic choice, not merely a transactional convenience. African American-owned banks hold just $6.4 billion in assets, while African American credit unions hold $8.2 billion, meaning these institutions together control less than $15 billion in combined lending capacity despite serving a market of more than 40 million people — insufficient to exert meaningful influence in national credit markets without deliberate capital infusion from within the community itself. When an African American investor finances a land purchase through a Black-owned bank or credit union rather than a mainstream white-owned lender, the mortgage deposit strengthens that institution’s liquidity ratio, expands its lending capacity through fractional reserve multiplication, and keeps the interest income circulating within the ecosystem rather than exiting to a Wall Street balance sheet. Every dollar deposited into an African American financial institution can translate into multiples of additional lending capacity once multiplied through the banking system — meaning that the collective financing decisions of HBCU alumni and community investors are not merely personal financial choices but acts of institutional capitalization. A community that builds land equity through Black-owned financial institutions simultaneously strengthens two pillars of its economic architecture: the land base that generates long-term wealth and the banking infrastructure that finances the next generation of acquisition.

At the institutional tier, the strategic imperative is even more pronounced. As of 2014, Tuskegee University controlled approximately 5,000 acres, ranking 12th among all American colleges in total land holdings, while Alabama A&M (2,300 acres), Alcorn State (1,756 acres), Prairie View A&M (1,502 acres), Kentucky State (915 acres), and Southern University (884 acres) collectively controlled more than 12,000 acres, placing all six among the top 100 college landowners in the United States. Those figures have not been comprehensively updated in the intervening decade, and the actual current land position of these institutions accounting for acquisitions, dispositions, and reclassifications likely differs. What has not changed is the strategic imperative to treat that land base as a productive investment asset rather than passive institutional real estate. A coordinated commitment of $1 million from each of the nineteen 1890 land-grant HBCUs would create a $19 million revolving fund capable, through its placement in African American banks and credit unions, of generating $7–$10 in agricultural lending capacity for every dollar committed financing not just land acquisition but the full productive cycle of African American farming. That mechanism addresses credit access. The complementary challenge is equity accumulation: deploying HBCU endowment capital, alongside alumni and friends’ capital, into the five evergreen land categories through a structured private REIT. An HBCU-anchored land REIT, capitalized with institutional endowment commitments as the senior tranche and alumni association and individual investor capital as subordinate tranches, would create a properly tiered investment structure with aligned incentives. The endowment’s priority return on its senior capital is protected; alumni investors participate in the upside above that hurdle; and the land itself remains in community-aligned ownership regardless of which investor class holds primacy at any given moment. Over time, the REIT’s land holdings can be diversified across all five evergreen categories — timberland for long-horizon appreciation, pastureland and agricultural ground for current income, waterfront parcels for high-appreciation positioning, and recreational property for near-term income generation — creating a portfolio whose income streams are non-correlated and whose asset values compound independently of equity market cycles.

The five evergreen land categories are individually sound investment ideas. Their strategic power for the HBCU community, however, lies not in isolated individual transactions but in the construction of a layered, coordinated ecosystem from the 22-year-old HBCU graduate purchasing her first 20-acre pasture parcel in Alabama, to the alumni chapter launching a multi-state agricultural REIT, to the 1890 HBCUs deploying endowment capital as the institutional anchor of a Black-managed timberland fund. At the most fundamental level, virtually every economic system man has ever created relies on one undeniable truth: whoever controls the land controls the system. The African American institutional ecosystem has the networks, the talent, and increasingly the structured financial vehicles to re-enter land ownership at meaningful scale. What it requires now is the strategic coordination to treat land not as a nostalgic aspiration but as a compounding institutional asset — one deed, one acre, one fund at a time.

Disclaimer: This article was assisted by ClaudeAI.

The race for profit in the 1970s transformed decaying urban space into what one U.S. senator described as a ‘golden ghetto,’ where profits for banks and real estate brokers were never ending, while shattered credit and ruined neighborhoods were all that remained for African Americans who lived there. — Keeanga-Yamahtta Taylor

In the vast and dynamic economy of American real estate, now collectively valued at over $100 trillion, African America holds just $2.24 trillion in real estate assets. Though this figure represents a 4.2 percent increase from 2022, it remains only 5 percent of total U.S. household real estate wealth. For a community that comprises over 13 percent of the U.S. population, this disparity reflects not mere misfortune but a structural condition produced over generations by deliberate policy, institutional exclusion, and a sustained absence of coordinated wealth strategy. The Federal Reserve defines real estate as “land and any permanent structures, like a home, or improvements attached to the land, whether natural or man-made.” In the African American asset portfolio, real estate accounts for 34.3 percent of total holdings, the single largest asset class. That real estate functions simultaneously as the community’s greatest asset and its most glaring vulnerability is not a paradox but a diagnosis. The foundation exists. What is missing is the institutional architecture to build upon it.

The raw numbers make the opportunity cost unmistakable. Redfin estimates U.S. residential real estate alone at approximately $50 trillion. Were African Americans to own property proportional to their share of the national population, their residential holdings alone would exceed $6.5 trillion nearly triple current estimates. The commercial real estate sector, valued between $22.5 and $26.8 trillion, and the $23 trillion in unimproved land represent additional frontiers where African American institutional presence is negligible. These are not simply numbers. They are the coordinates of a strategic gap that no amount of individual homeownership ambition, however admirable, can close without deliberate institutional action.

The African American homeownership rate sits at approximately 44 percent, compared to nearly 75 percent for white households, a gap that has persisted, in varying form, for over a century. But homeownership rates alone obscure the more consequential structural problem: the overwhelming concentration of African American real estate holdings in primary residential properties. The community remains dramatically underrepresented in commercial real estate, rental income properties, and unimproved land holdings. Residential ownership offers stability and modest equity accumulation. It does not generate the income streams, leverage opportunities, or intergenerational transfer mechanisms that characterize wealth at institutional scale. The distinction between a community that owns homes and a community that owns productive real estate assets is the distinction between personal security and institutional power.

The historical forces that produced this condition are not obscure. Redlining systematically denied mortgage credit to African American households throughout the mid-twentieth century, confining Black investment to neighborhoods artificially depressed in value and infrastructure. Predatory lending in subsequent decades extracted billions in wealth from these same communities through subprime instruments designed to fail. Urban renewal programs, euphemistically named but functionally destructive, cleared vast swaths of Black commercial and residential property under the authority of eminent domain. Gentrification, the contemporary variant of this pattern, continues to displace African American communities from land whose value, built in part through decades of residency, now accrues to others. These mechanisms were not incidental. They were structural. And structural problems require structural responses.

The cultural narrative around African American real estate has not always served strategic ends. For generations, homeownership has been understood as an arrival, a threshold crossed, a symbol of stability and middle-class membership. This framing is emotionally powerful and historically resonant. It is also, from a wealth-building perspective, incomplete. Institutional investors and generational wealth holders do not experience real estate primarily as shelter. They experience it as a portfolio of productive assets—income-generating, tax-advantaged, equity-building, and scalable. The divergence in these frameworks has produced divergent outcomes. While white households and institutional capital have moved aggressively into multifamily development, commercial acquisition, and land banking, African Americans have remained disproportionately concentrated in single-family residential ownership, often in markets subject to rapid tax appreciation that outpaces income growth. The next strategic imperative is a cultural and institutional shift: from celebrating real estate as a destination to deploying it as an instrument.

The mechanism best suited to that deployment for scale, for liquidity, and for institutional alignment is the Real Estate Investment Trust. A REIT is a company that owns, operates, or finances income-producing real estate and, by law, must distribute at least 90 percent of its taxable income to shareholders annually. REITs offer individual and institutional investors access to commercial real estate returns without requiring direct property management, and they can be structured as either publicly traded vehicles or private instruments accessible to accredited investors and philanthropic foundations. Among hundreds of REITs listed on U.S. exchanges, RLJ Lodging Trust, founded by Robert L. Johnson, stands as a rare and instructive exception: an African American-led REIT operating at institutional scale in the premium hotel sector. That RLJ remains an outlier rather than a model replicated across asset classes and geographies is itself a measure of the institutional gap this analysis addresses. The architecture for such vehicles exists. What has been missing is the coordinated institutional will to build them.

The possibilities are concrete. An HBCU-anchored REIT acquiring and managing student housing near Black college campuses could deliver 7 to 10 percent annual returns to alumni investors while stabilizing the residential environments upon which those campuses depend. A community-oriented REIT acquiring retail corridors in majority-Black metropolitan markets could generate dividend income while reversing commercial disinvestment in those neighborhoods. Private REITs, structured to blend fiduciary return with community development mission, could attract philanthropic capital alongside institutional investors, broadening both the investor base and the strategic reach. None of these structures require regulatory innovation or special dispensation. They require capital aggregation, professional management capacity, and the kind of coordinated institutional collaboration that other communities have built over decades.

HBCUs are among the most strategically positioned institutions within the African American ecosystem to anchor this kind of real estate development and the most underutilized in precisely that role. Many HBCUs are already substantial landowners. Howard University controls significant real estate in one of the most valuable urban markets in the country; other institutions hold campuses, adjacent parcels, and legacy properties whose full strategic value has rarely been extracted. What HBCUs have not done, with few exceptions, is build the institutional infrastructure such as real estate arms, development subsidiaries, and endowment-backed investment funds that would allow them to act as coordinated economic developers rather than passive landholders. The academic mission and the economic mission are not in tension here. An HBCU that trains real estate developers, appraisers, construction professionals, and fund managers while deploying its own endowment capital into community-anchored development projects is executing both missions simultaneously.

Yet the HBCU campus itself is only the most visible node in a much larger network. HBCU alumni associations and their affiliated local chapters represent one of the most geographically dispersed and institutionally underutilized pools of organized Black professional capital in the country. Alumni networks of HBCUs extend into every major metropolitan area and across significant segments of the African American professional class. These networks have historically mobilized around homecoming, scholarship, and campus giving. Their strategic potential as vehicles for real estate capital formation—pooling accredited investor capital into private REIT structures, co-investing in development projects near home campuses, or anchoring land cooperative initiatives in cities where chapters are active—has barely been explored. The alumni chapter, reimagined as a local investment vehicle tied to a broader institutional strategy, could function as a distributed engine of Black real estate accumulation in a way that no single centralized fund can replicate.

African American-led banks and credit unions occupy the complementary position on the financing side of this equation. Black-owned financial institutions have historically served communities excluded from conventional lending markets, and their expansion into commercial real estate lending is both a logical extension of that mission and a strategic necessity. The barriers are real: underwriting standards calibrated to conventional risk models, limited capital reserves relative to the scale of commercial transactions, and regulatory environments that require careful navigation. But regulatory relief mechanisms, Community Reinvestment Act credits, philanthropic loan guarantees, and structured partnerships with larger financial institutions can each play a role in expanding the commercial lending capacity of Black-owned banks. Patient capital deployed with longer time horizons and a tolerance for mission-aligned risk is often the difference between a viable community development project and one that never reaches the financing stage. Black financial institutions, working in concert with HBCU endowments and alumni-backed investment vehicles, could provide precisely that capital layer.

Yet the households that must ultimately anchor this investment model carry a debt burden that makes participation structurally difficult. African American households currently hold approximately $780 billion in mortgage debt against $740 billion in consumer credit—a ratio that is almost precisely the inverse of the 3:1 mortgage-to-consumer-credit structure that characterizes financially healthy households across every other ethnic demographic group in America. As HBCU Money has documented in its analysis of African American household debt, reaching that 3:1 ratio would require either eliminating $480 billion in consumer credit or adding $1.5 trillion in new mortgage debt neither of which is achievable through household-level decisions alone, and both of which are complicated by the same discriminatory credit markets and institutional voids that have shaped the real estate gap itself. With African American-owned banks and credit unions controlling less than $15 billion in combined assets, the community lacks the internal financial infrastructure to intermediate this debt restructuring on its own terms. The implication for real estate investment vehicles aimed at alumni households is direct: minimum investment thresholds, liquidity provisions, and distribution schedules must be designed with an honest accounting of where Black household finances actually are, not where conventional investment frameworks assume them to be. A fund architecture calibrated to households that hold meaningful liquid capital beyond retirement accounts will exclude the majority of its intended participants. One designed with awareness of the consumer-credit trap and structured to allow smaller initial commitments, phased capital calls, and reliable quarterly income distributions can meet alumni households where they stand and build participation from there.

The real estate investment gap cannot be understood in isolation from the broader passive income crisis that structurally defines African American household economics. Census Bureau and Federal Reserve data document that only approximately seven percent of Black households report receiving passive income of any kind from rental properties, interest-bearing instruments, dividends, or business ownership compared to roughly twenty-four percent of white households. The median passive income figure for Black families barely reaches two thousand dollars annually, against nearly five thousand for Asian, Latino, and white households. These are not incidental disparities. They reflect the same structural exclusion from mortgage markets, from equity accumulation, from income-generating asset ownership that has confined African American real estate holdings to the residential and the personal. A household that relies entirely on wages and salaries, holds no appreciating assets, and must meet every financial obligation from current earnings has no margin for accumulation, no buffer against disruption, and nothing to transmit to the next generation. Real estate, properly structured as an income-generating asset rather than a residence, is the most historically available and institutionally scalable mechanism for breaking that cycle which is precisely why the shift from shelter to strategy is not a matter of aspiration but of arithmetic.

The unimproved land question deserves separate analysis, because it represents both an acute historical injury and a forward-looking strategic opportunity that the community has not yet fully reckoned with. The United States holds an estimated $23 trillion in unimproved land. African American ownership of such land, particularly outside urban centers, has been dramatically eroded over the twentieth century. The Great Migration, which carried millions of Black Southerners to Northern and Western cities between 1910 and 1970, also severed family ties to rural land that was subsequently lost through heir property fragmentation, tax delinquency, and outright dispossession. Heir property, land held by multiple descendants without clear legal title, remains a particular vulnerability, as it disqualifies owners from federal disaster relief, federally backed mortgage programs, and legal protections available to titled owners. The legal infrastructure to address this exists: clear title initiatives, land trust structures, and targeted litigation have each proven effective in specific contexts. What has been absent is the coordinated institutional commitment to deploy them at scale.

Land banking, the strategic acquisition and holding of unimproved land for future development, conservation, or appreciation, is among the most powerful and least discussed tools available to African American institutional investors. It requires neither immediate development capital nor complex management infrastructure. It requires patience, coordination, and a long time horizon. With climate change accelerating the valuation of water rights and agricultural land, and with urban expansion continuously pushing development pressure outward, unimproved land acquired today at current market prices will almost certainly appreciate substantially over the coming decades. African American land cooperatives, land trusts anchored by HBCU endowments, and investment syndicates organized through alumni networks and Black financial institutions are all viable vehicles for this kind of acquisition. The question is whether the institutional coordination to pursue it can be assembled before further displacement forecloses the opportunity.

The policy environment for African American real estate development is, at the federal level, unfavorable and unlikely to improve in the near term. This makes the strategic reorientation toward city, county, and municipal policy levers not merely a preference but a practical necessity. African American political power is most concentrated and most effective at the local level in city councils, county commissions, planning boards, and municipal development authorities. Zoning reform, public land disposition policy, tax increment financing districts, and municipal bond programs can each be structured to support African American commercial real estate development when the political will to do so is present. Black-majority cities and counties that form deliberate real estate development coalitions—sharing resources, coordinating acquisition strategies, and protecting public land from speculative divestment—can build the kind of policy infrastructure that generates compounding institutional advantage over time.

Philanthropy, historically oriented toward direct service and individual scholarship, must reorient a meaningful portion of its capital toward real estate infrastructure if the structural gap is to close. This means endowment investments in REIT vehicles and land trusts, not merely program grants. It means loan guarantees for Black commercial developers working in markets where conventional underwriting systematically undervalues the opportunity. It means funding the legal capacity to protect heir property and challenge exclusionary zoning. And it means building the professional training pipelines at HBCUs and through professional associations that will produce the underwriters, fund managers, appraisers, and developers without whom the most elegant institutional architecture remains unexecuted. Capital formation and talent formation are not sequential problems. They are simultaneous ones, and the institutions best positioned to address both in concert are already embedded in the African American community.

The $2.24 trillion that African Americans hold in real estate today is not a ceiling. It is a baseline and a revealing one. It documents both the resilience of a community that has accumulated meaningful assets despite systematic exclusion and the magnitude of the institutional work that remains. Closing the gap between that baseline and a holdings figure commensurate with population share and historical contribution will not be accomplished through individual homeownership campaigns or federal grant programs. It will be accomplished through the deliberate construction of institutional vehicles like REITs, land trusts, endowment-backed development funds, alumni investment networks, cooperative land banks, and community development financial institutions operating in coordinated alignment around a shared strategic logic. That logic is not complicated. Land is productive. Institutions that own it accumulate power. Communities that build institutions to own it at scale build the kind of durable wealth that survives political cycles, economic shocks, and generational transitions. The architecture exists. The question is whether the will to build it does too.

Sidebar: Action Framework for African American Real Estate Advancement

Priority Area

Recommended Action

Commercial Real Estate

Launch African American-owned REITs and real estate investment funds

HBCU, Alumni Associations, Chapters’ Role

Develop endowment-backed real estate divisions in conjunction with alumni chapters and educational pipelines

Land Banking

Form community land trusts and cooperatives to acquire unimproved land

Policy

Advocate for federal and state legislation to simplify land title and incentivize investment

Philanthropy

Provide catalytic funding for institutional real estate ventures

Public-Private

Secure partnerships for municipal land disposition and infrastructure integration

Disclaimer: This article was assisted by ClaudeAI.

The United States, a land famed for its abundance and ambition, sits atop one of the most valuable portfolios of real estate in the world. From the towering commercial properties of Manhattan to the suburban sprawl of Phoenix and the vast, untouched stretches of prairie and desert in between, the collective valuation of U.S. real estate has breached an astonishing threshold: $100 trillion.

According to recent estimates, the total value of U.S. residential real estate hovers around $50 trillion, while commercial real estate accounts for an additional $22.5 to $26.8 trillion. Less visible but equally consequential is the nation’s unimproved land—agricultural acreage, forests, deserts, and raw parcels—with a market value estimated at $23 trillion. Together, these segments reveal a profound truth about the American economy: it is built quite literally on a foundation of land wealth that continues to define its structure, resilience, and long-term power.

The Residential Bedrock

Homeownership, long considered the American Dream, is more than a cultural aspiration—it is the foundation of household wealth and the gravitational center of the U.S. economy. Redfin estimates that American homes are now worth a cumulative $50 trillion, a figure that has surged nearly 50% since 2020, when the pandemic-era monetary policy and fiscal stimulus unleashed a flurry of homebuying and refinancing activity.

This valuation includes not only primary residences but also investment properties and vacation homes. Approximately 65% of Americans own homes, and for most, their house remains their single largest asset. According to the Federal Reserve’s Survey of Consumer Finances, real estate comprises more than 50% of household net worth among the middle class, making housing prices not just a matter of market speculation but a critical economic indicator.

But the recent surge in interest rates has cast a shadow. The Federal Reserve’s aggressive tightening campaign to combat inflation has pushed mortgage rates above 7%, slowing home sales and triggering price corrections in overheated markets. Nevertheless, inventory shortages and strong labor markets have kept residential property values elevated. Analysts believe this plateau—rather than a crash—will be the new normal, as housing markets recalibrate in a high-rate environment.

Commercial Real Estate’s Reckoning

The U.S. commercial real estate (CRE) market, estimated to be worth between $22.5 trillion and $26.8 trillion according to the Federal Reserve Bank of St. Louis, finds itself at a crossroads. Office towers, retail strips, multifamily developments, and industrial warehouses are being repriced in real time as remote work, e-commerce, and rising interest rates challenge legacy models.

Office vacancies in major cities like San Francisco, Chicago, and Washington, D.C. have climbed to record highs—some surpassing 30%—as companies consolidate physical footprints. This has sparked what some are calling a “silent crisis” for CRE. Valuations have dropped precipitously in certain metro areas, and regional banks with significant exposure to commercial mortgages have found themselves vulnerable.

But it is not all doom and gloom. Industrial and logistics properties—particularly those near ports, rail hubs, and urban fulfillment centers—continue to outperform, benefiting from the growth of e-commerce and reshoring of manufacturing. Meanwhile, multifamily housing has emerged as a relative safe haven, with demand bolstered by rising mortgage costs that have priced many out of homeownership.

Institutional investors, from pension funds to private equity giants, are rebalancing portfolios, shedding underperforming assets while doubling down on high-performing sub-sectors. The great repricing of commercial property could ultimately yield a leaner, more sustainable industry.

America’s Undervalued Treasure: Unimproved Land

Beyond the skyscrapers and suburbs lies the nation’s quietest giant—its unimproved land, whose estimated value of $23 trillion remains largely outside the public imagination. This figure, derived from the Bureau of Economic Analysis and academic research, encompasses the total value of raw, undeveloped land, including forests, deserts, wetlands, farmland, and government-owned acreage.

Unimproved land is often overlooked in discussions of wealth, yet it plays a central role in climate resilience, national food security, conservation, and future development. It is the terra firma upon which cities expand, solar farms rise, and conservation easements are negotiated. It also serves as collateral in trillions of dollars of financing across industries.

Yet unlike residential and commercial properties, unimproved land lacks a robust national marketplace or transparent pricing. It is often subject to local zoning laws, speculative investment, and environmental regulation—making it both a store of untapped value and a highly complex asset class. With climate change accelerating, land with access to water, resilience to extreme weather, and proximity to urban centers is already commanding premium valuations.

Land is also becoming a focus for sovereign wealth funds, family offices, and climate-conscious investors. “Farmland and timberland are now being seen as long-duration, inflation-resistant assets,” says Daniel Krueger, managing director of a Colorado-based land investment firm. “We’re at the early stages of a global land rush driven by food, carbon, and water scarcity.”

A National Portfolio of Strategic Assets

Taken together, the U.S. real estate sector functions as a $100 trillion national portfolio, integral not just to individuals and corporations but to the state itself. Local governments rely on property taxes for more than 70% of their operating budgets, while real estate assets underpin infrastructure financing through municipal bonds. The U.S. government also owns about 640 million acres of land—roughly 28% of the country—much of which is leased for energy, timber, and recreation, generating billions in annual revenue.

Real estate also serves as the backbone of U.S. capital markets. Mortgage-backed securities, REITs, and land-based derivatives are woven into the financial system, linking Wall Street to Main Street. In a typical year, real estate transactions account for more than 17% of GDP when including construction, financing, insurance, and brokerage services.

Yet this vast portfolio is not without its vulnerabilities. Natural disasters, rising sea levels, zoning bottlenecks, affordability crises, and infrastructure underinvestment all threaten the productivity of American land. Moreover, decades of racially discriminatory policies in housing and land access continue to cast a long shadow, leaving millions of Americans excluded from the benefits of land ownership.

The Geopolitics of Land

In a global economy defined increasingly by resources, logistics, and sovereignty, America’s real estate advantage is also geopolitical. With a vast and varied landscape, stable legal system, deep capital markets, and strong property rights, U.S. land remains an attractive destination for foreign capital. Investors from Canada, Germany, Singapore, and the Middle East have spent billions acquiring trophy assets in cities like New York, Los Angeles, and Miami, as well as farmland in the Midwest and ranches in Texas.

But the rise of China, strategic concerns around food and data security, and the politicization of foreign ownership have made real estate an arena of national interest. Several states have passed or are considering legislation restricting land purchases by foreign governments or their proxies. Meanwhile, the Committee on Foreign Investment in the United States (CFIUS) has widened its scope to include real estate transactions near sensitive military or infrastructure sites.

These developments suggest a growing recognition that land—long viewed as inert and apolitical—is in fact a strategic resource requiring oversight and planning.

The Sustainability Imperative

In the 21st century, the full value of real estate can no longer be measured in dollars alone. Sustainability, resilience, and carbon sequestration are emerging as parallel dimensions of value. Developers are increasingly required to meet environmental standards, and landowners are being incentivized to conserve forests, wetlands, and grasslands as carbon sinks.

The Inflation Reduction Act of 2022 poured billions into climate-smart land use initiatives, including tax credits for renewable energy on farmland and funding for urban tree canopies. These programs aim to make the American landscape more resilient while tying land use directly to climate goals.

Urban planning is also being reimagined. Cities like Portland, Denver, and Austin are investing in zoning reform to allow for greater density, affordability, and transit-oriented development. Meanwhile, rural communities are embracing land trusts and cooperative ownership models to prevent land loss and promote inclusive growth.

The Repricing of the American Dream

As the United States approaches a new demographic, environmental, and economic era, the notion of land as a static store of wealth is evolving. The repricing of American real estate—spurred by demographic shifts, financial innovation, and climate change—will redefine value for the next generation.

For homeowners, it means contending with climate risk disclosures and insurance volatility. For developers and institutional investors, it entails navigating rising construction costs, policy uncertainty, and ESG mandates. For policymakers, it means rethinking land taxation, infrastructure planning, and public land stewardship.

Yet the fundamental truth remains: the United States possesses one of the most valuable and versatile land portfolios in the world. With judicious management, equitable access, and forward-looking investment, that $100 trillion empire can continue to generate prosperity for decades to come.

In an age of intangibles—from cloud computing to cryptocurrencies—the solidity of land and property remains unmatched. America’s $100 trillion real estate empire is not just a measure of wealth; it is a reflection of national identity, economic philosophy, and strategic foresight. How the country chooses to steward this land—who gets to own it, how it is used, and whether it serves the public good—will shape the next chapter of the American experiment.

Sidebar: By the Numbers – U.S. Real Estate Valuations

Residential Real Estate: $50 trillion (Redfin, 2024)

Commercial Real Estate: $22.5–$26.8 trillion (Federal Reserve Bank of St. Louis, 2024)

Real Estate Contribution to U.S. GDP: ~17% (including indirect industries)

In an age of intangibles—from cloud computing to cryptocurrencies—the solidity of land and property remains unmatched. America’s $100 trillion real estate empire is not just a measure of wealth; it is a reflection of national identity, economic philosophy, and strategic foresight. How the country chooses to steward this land—who gets to own it, how it is used, and whether it serves the public good—will shape the next chapter of the American experiment.

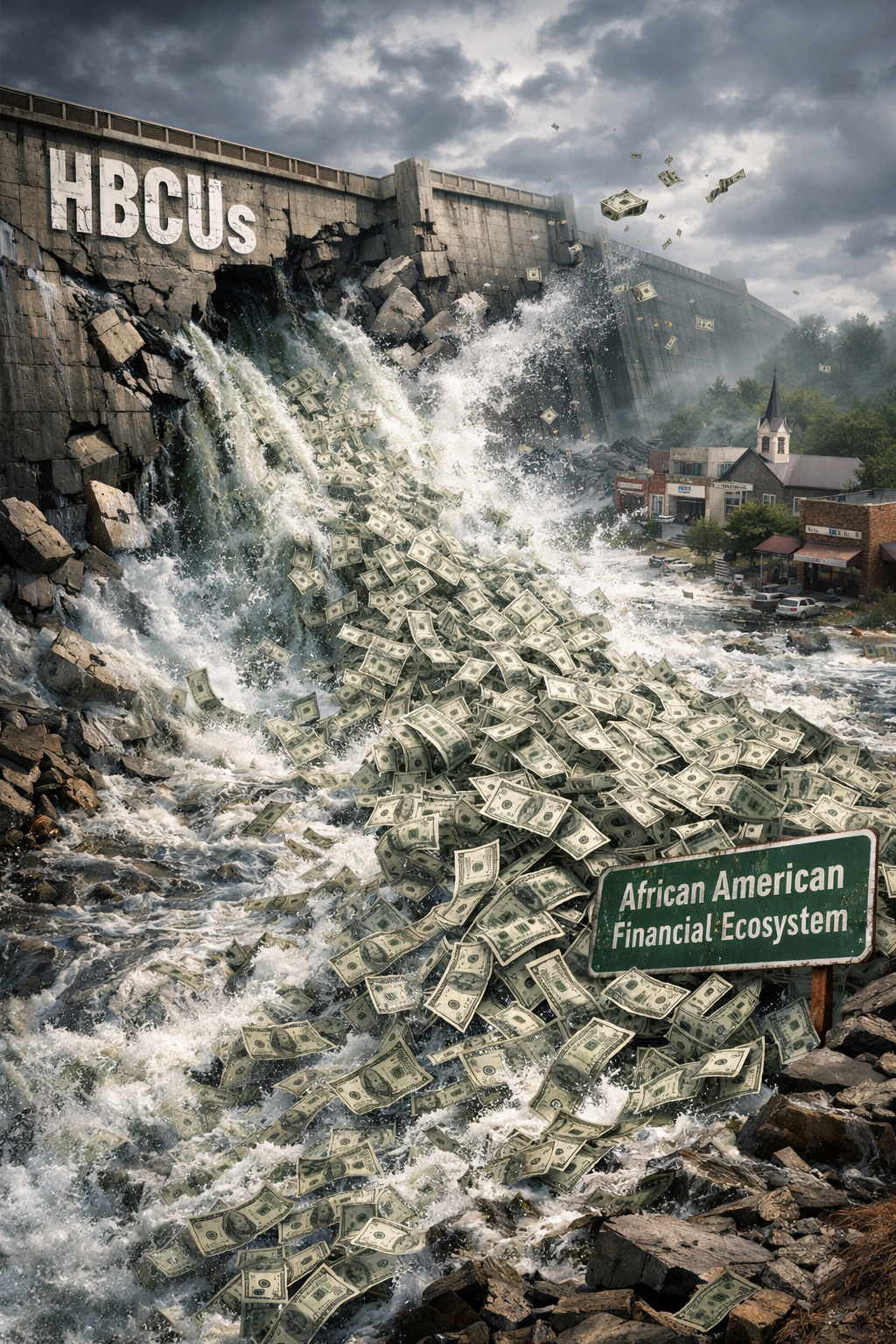

“It is disappointing that HBCUs and any African American institution for that matter have not figured out yet that the circulation of our social, economic, and political capital with each other at the institutional level is where the acute crisis of closing the wealth gap truly lies. Yet, we still chase colder ice.” – William A. Foster, IV

The percentage of PWI dollars that flow into African American owned businesses is likely limited to catering a social event. Beyond that, their dollar never even likely floats pass an African American business. However, HBCUs certainly cannot say the same. HBCU capital leaving the African American financial ecosystem looks like every dam on Earth broke at the same time.

Virginia Union University’s recent announcement of a partnership with Keller Williams Richmond West represents a familiar pattern in HBCU decision-making, one that undermines the very mission these institutions claim to champion. While VUU proudly touts this collaboration as “groundbreaking” and positions it as a pathway to “closing the racial wealth gap,” the partnership reveals a fundamental misunderstanding of how wealth gaps are actually closed. The reality is stark: you cannot close a racial wealth gap by systematically excluding institutions from your own community from the economic opportunities your institution creates.

When HBCUs partner exclusively with non-Black institutions, they create what economists call a “leaky bucket” effect. The money, talent, and social capital generated by these historically Black institutions flow outward to other communities rather than circulating within the African American ecosystem. Every dollar spent with a non-Black vendor, every partnership signed with a non-Black firm, every opportunity directed away from Black-owned businesses represents wealth that could have been building generational prosperity in Black communities—but instead enriches other groups. This is where the fundamental disconnect lies: HBCUs understand the importance of encouraging individual African Americans to support Black-owned businesses, yet these same institutions fail to apply this principle at the institutional level where the real economic power resides.

The conversation about the circulation of the African American dollar has historically focused on individual consumer behavior. We’ve heard for decades about the need for Black consumers to shop at Black-owned stores, bank with Black-owned financial institutions, and hire Black-owned service providers. Studies have shown that a dollar circulates in Asian communities for approximately thirty days, in Jewish communities for around twenty days, in white communities for seventeen days, but in Black communities for only six hours before leaving. This abysmal circulation rate is correctly identified as a critical factor in the persistent wealth gap. But what these discussions almost always miss is that individual consumer behavior, while important, pales in comparison to institutional spending power.

When Virginia Union University signs a multiyear partnership with Keller Williams, it’s not spending a few hundred or even a few thousand dollars. Institutional partnerships involve hundreds of thousands or millions of dollars in direct and indirect economic benefits—facility usage, marketing exposure, student referrals, commission opportunities, and brand association. A single institutional partnership can equal the spending power of hundreds or thousands of individual consumers. Yet HBCUs consistently fail to recognize that their institutional spending decisions have exponentially more impact on wealth circulation than any individual consumer choice their students or alumni might make.

VUU’s partnership with Keller Williams is particularly emblematic of this pattern. According to the announcement, this collaboration will create “the first Keller Williams Real Estate Hub on an HBCU campus in Virginia” and will be “designed to bridge education, entrepreneurship, and real estate into one powerful ecosystem.” The goals are admirable: career readiness, economic mobility, wealth-building opportunities through real estate education and professional pathways. The partnership is positioned as being co-led by members of Delta Sigma Theta Sorority, Incorporated, with explicit language about sisterhood, brotherhood, and service in action. But here’s the question VUU administrators apparently didn’t ask: Why not create this “powerful ecosystem” with a Black-owned real estate company?

The assumption underlying most HBCU partnerships with non-Black firms seems to be that suitable Black-owned alternatives don’t exist. This assumption is demonstrably false. Black-owned real estate companies operate throughout the United States, including in Virginia and the Richmond area. These firms possess the expertise, resources, and commitment to serve HBCU students and alumni. United Real Estate Richmond, which describes itself as the largest Black-owned real estate firm in the Mid-Atlantic region, operates right in VUU’s backyard. CTI Real Estate is a Black-owned, woman-owned firm serving Virginia and Maryland. Nationally, companies like Braden Real Estate Group—a Black-owned Houston-based brokerage co-founded by Prairie View A&M University graduate Nicole Braden Handy—demonstrate the success of HBCU alumni in building substantial real estate businesses. H.J. Russell & Company, founded in 1952, stands as one of the largest minority-owned real estate firms in the United States. These Black-owned firms have proven track records of success, deep community connections, and explicit missions to build wealth in African American communities. These firms could provide the same—or better—opportunities that Keller Williams offers, with the added benefit of keeping wealth circulating in the Black community.

The difference would be transformative. A partnership with a Black-owned real estate firm would actually contribute to closing the wealth gap. It would demonstrate to students what Black excellence in business looks like. It would create mentorship opportunities with professionals who understand the unique challenges and opportunities facing Black Americans in real estate. It would ensure that the commissions, fees, and other economic benefits generated by the partnership stay within the African American economic ecosystem. Most importantly, it would model the institutional behavior necessary for true wealth accumulation—showing students that circulation of Black dollars must happen at every level, not just in their personal spending habits.

But to truly understand what institutional circulation looks like, consider this scenario: An African American real estate investment firm—owned by an HBCU alumnus and employing HBCU graduates as project managers, analysts, and development specialists—decides to develop a mixed-use building in Richmond. The firm uses Braden Real Estate Group to acquire the land. They secure financing from an African American bank like OneUnited Bank or Liberty Bank, supplemented by an investment syndicate of African American investors. The construction is handled by an African American-owned construction company like H.J. Russell & Company. When the transaction closes, it’s processed through Answer Title & Escrow LLC, the Black-owned title company founded by University of the District of Columbia alumna Donna Shuler. The property management contract goes to another Black-owned firm. The legal work is handled by Black attorneys. The accounting is done by a Black-owned firm.

This is what institutional circulation actually looks like. In this single development project, wealth circulates through multiple Black-owned institutions at every stage of the transaction. The bank earns interest income that it can then lend to other Black businesses and homeowners. The title company generates revenue that allows it to hire more staff and take on larger projects. The construction company builds its portfolio and capacity to compete for even bigger developments. The real estate investment firm creates returns for its Black investors and proves the viability of Black-owned development companies. The project managers and analysts gain experience that prepares them to start their own firms. Every single point in the transaction keeps wealth circulating within the African American economic ecosystem, building institutional capacity, creating jobs, generating returns, and proving that Black-owned institutions can handle sophisticated, large-scale projects.

Now contrast that with what happens when VUU partners with Keller Williams. Students may get training and even jobs as real estate agents, but the institutional wealth flows to Keller Williams—a non-Black company. The commissions generated by VUU-affiliated agents enrich Keller Williams’ franchise system. The brand association benefits Keller Williams’ reputation. The networking opportunities primarily connect students to Keller Williams’ existing (predominantly non-Black) networks. And when these students eventually facilitate property transactions, the ancillary services—financing, title work, legal services—typically flow to whatever institutions Keller Williams recommends, which are unlikely to be Black-owned.

The VUU-Keller Williams partnership might help individual Black students enter the real estate industry, but it does absolutely nothing to build the Black-owned institutional infrastructure necessary for true wealth building. In fact, it actively undermines that infrastructure by directing institutional resources and opportunities away from Black-owned firms. VUU essentially takes Black talent, students who could be building careers with Black-owned firms, and channels them into a non-Black institution, teaching them that Black institutions aren’t capable of providing the same opportunities.

This is the critical insight that HBCUs continue to miss: institutional circulation of capital is what builds lasting economic power. When individual Black consumers support Black businesses, they create important but limited impact. One person shopping at a Black-owned grocery store or banking with a Black-owned bank makes a difference, but a small one. When Black institutions support Black businesses, they create transformative, generational impact. An HBCU that partners with Black-owned banks, construction companies, real estate firms, technology providers, and service companies doesn’t just create individual transactions it builds an entire ecosystem of mutually reinforcing institutions that grow stronger together. This institutional ecosystem then has the power to compete with non-Black institutions, create opportunities at scale, and genuinely close wealth gaps.

Think about what would happen if every HBCU made a commitment to work exclusively with Black-owned institutions whenever viable alternatives exist. Imagine if all 101 HBCUs banked with Black-owned banks, used Black-owned construction companies for campus buildings, partnered with Black-owned real estate firms for student housing and community development, contracted with Black-owned technology companies for IT services, and hired Black-owned firms for legal, accounting, and consulting work. The combined institutional spending power of HBCUs would transform the Black business landscape. Black-owned banks would have hundreds of millions in deposits, allowing them to make larger loans and compete for more business. Black-owned construction companies would have steady revenue streams that would allow them to invest in equipment, hire skilled workers, and bid on larger projects. Black-owned real estate firms would have the institutional backing to compete for major developments. Black-owned technology companies would have the resources to innovate and scale.

But beyond the immediate economic impact, this institutional circulation would create something even more valuable: proof of concept. When Alabama State University chooses a Black-owned bank to handle a $125 million transaction, it proves that Black-owned financial institutions can handle sophisticated, large-scale deals. When VUU partners with a Black-owned real estate firm to create a campus-based real estate hub, it proves that Black-owned companies can deliver the same quality and scale as non-Black competitors. When HBCUs consistently work with Black-owned construction companies, law firms, accounting firms, and consulting companies, they build a track record of success that these firms can point to when competing for other major contracts. This institutional validation is precisely what Black-owned businesses need to break through the barriers that have historically excluded them from large-scale opportunities.