I freed a thousand slaves, I could have freed a thousand more if only they knew they were slaves. – Harriet Tubman

Recently, Harriet Tubman was chosen by New York-based advocacy group Women on 20s as the winner of its campaign to put a woman’s face on the $20 bill. Excuse us while we have flashbacks of 2008 when America voted and elected the first (half) African American president. The country rejoiced and patted itself on the back. Apparently, electing a (half) African American was enough to cleanse the institutional problems that African America faced and continues to face even almost eight years later. But we must be making progress, right? It is 2015 and we elected a (half) African American as president after all. The sad irony about Harriet Tubman being elected to be on the twenty dollar bill is that that her death in 1913 represents arguably the period of economic apex for African America.

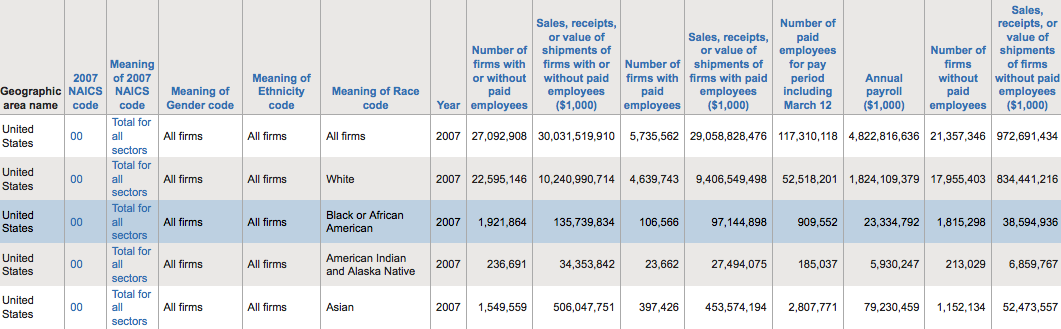

Harriet Tubman may or may not find her way onto the twenty dollar bill, but what of the substantive reality of African America’s economic situation. Between 1888 and 1934, African America started 134 banks. Today, there are less than 25 banks left that do not control even half of one percent of African America’s buying power. African American owned credit unions comprise 340 institutions, but even with that number still do not combine with the banks to even control one percent of the $1.1 trillion in African American buying power. As a result, African Americans are often subject to predatory financial services (even by our own people like Magic Johnson and Russell Simmons), redlining, gentrification, and lack of small business growth which directly impacts wealth creation and community employment. To the last point, the lack of business ownership by African America is frightening since the days of Black Wall St. After owning 500 hospitals in the early twentieth century, African America is down to one leaving serious questions about the economics of the community’s long-term health prospects. The wealth divide between African American and every other group is staggering. Latino America, the second poorest group, is still eleven percent wealthier than African America. One could argue their willingness to engage in labor that African America qualitatively feels is beneath them while increasing their business ownership in their own communities is part of that narrative. Asians and European America have 14 times and 20 times the amount of wealth that African America has, respectively (chart above). In large part, the other three groups have a strong investment in business ownership. Something that is often a byproduct of either a strong banking system or in the Latino American case a strong shadow banking system within the community that is largely reliant on cash and admonishes the use of debt. African American firms (chart below) currently only account for 0.4 percent of America’s total $30 trillion in annual firm sales. This is one of the reasons that the unemployment rate in our community remains stubbornly twice that of the overall rate. While other groups can hire within their own community, African America is largely dependent on public sector employment and external private sector employment, where more times than not they are a quota hire.

Any time you hear community activist talk about ways to solve the ails of African America’s economic there is always this belief that if we can just get African Americans to circulate the dollar, then all would be solved. Unfortunately, the institution most in charge of circulating the dollar – the bank – we prefer to use ones that are not owned by our community. It is one of the key reasons the dollar circulates less than one time in our community. Circulation also entails more than consumer behavior which is often the thing that is promoted most. However, putting deposits in an African American bank that in turn make loans so an African American family can buy a home in an African American neighborhood and strengthen its social fabric or an African American small business owner can borrow to start a business and employ the community so that unemployment rates are not reaching 20 percent plus like was the case in Detroit often seems loss on us. We can not be too upset though because we are often listening to these same community activists who have little or no economic or financial backgrounds. Collectively known as, the preachers, teachers, and reachers crew. For some reason, we have attributed to knowing the higher power as also knowing supply and demand. The second group, teachers, are anyone who thinks because they have a college degree in anything that they are economically qualified to advise. Lastly, the reachers who think that the federal government somehow can wave some magic economic wand and correct our economic woes.

Seemingly gone are the days of A.G. Gaston and Madam C.J. Walker, two African American titans of business ownership in the early twentieth century. These “activist” both started banks in their communities. Ensuring not only strong capital circulation, but employment as well. Today, where everyone deems themselves an “activist” because it has become the popular thing to do, while adding absolutely no substance or meat and potatoes to their community’s institutional infrastructure beyond marching up and down the street, posting articles on Facebook, or in this case voting for Harriet Tubman to be on the twenty dollar bill. We are not discussing actual economic equality or freedom. We are discussing the faux appearance of it and you know what they say you get what you pay for. It speaks largely to our own economic and financial illiteracy. Unfortunately, even many of the “educated” among us are just as guilty if not more so. African America’s educated behave as if they are somehow wealthy because they have a degree and in turn buy too much house, the latest fashion, or foreign car, but are as asset poor as those on Section 8 living. The accumulation of stocks, emergency savings, investment properties, intellectual property, or other assets that produce wealth and passive income are an absent concern.

Just as Harriet could not free those who did not realize they were slaves, it seems we still have a long way to go to convince many of our own that just having an income, a degree, or using other communities economic ecosystem does not mean you have entered the world of economic freedom. The trip along Harriet’s underground railroad required a sacrifice by individuals and families. It was not a comfortable journey, but it was a real journey toward the start of freedom. We are poorer today than when Harriet died over 100 years ago, an institutional economic ecosystem of our own that is going extinct, but her face on the twenty dollar bill has to be a sign of our freedom, equality, and progress, right? One wonders if Harriet’s revolver still works.