It is our duty to fight for our freedom. It is our duty to win. We must love each other and support each other. We have nothing to lose but our chains. – Assata Shakur

In February 1999, TLC released what would become one of the defining singles of their career. “No Scrubs” shot to number one on the Billboard Hot 100, where it remained for four consecutive weeks. The song’s message was clear and unapologetic: women were setting standards, and men who could not meet them need not apply. Within weeks, a relatively unknown rap group from Yonkers called Sporty Thievz fired back with “No Pigeons,” an answer record that used the same beat to deliver an equally scathing critique of women they deemed unworthy.

This exchange sparked what became known as a gender war on and off the airwaves, with radio stations playing both songs back-to-back and nightclubs dividing along battle lines — women shrieking in solidarity with TLC while men whooped for Sporty Thievz. Was this the inflection point where romantic and communal relationships between Black men and women began to fracture? Probably not. The roots run far deeper. But these songs crystallized something that had been building for years, a shift from celebration to criticism, from love songs to diss tracks, from the assumption of solidarity to the performance of mutual contempt.

Rewind a decade, and Black music told a fundamentally different story. The late 1980s and early 1990s gave us ballads that treated Black love not as a battlefield but as a sanctuary. Luther Vandross, Anita Baker, and Whitney Houston soundtracked weddings and anniversaries with a tenderness that affirmed the depth and dignity of Black romantic life. Mary J. Blige’s “Real Love” carried the longing of a generation. K-Ci & JoJo’s “All My Life” became a generational confession. Even within hip-hop, before the genre’s full commercial industrialization, there were moments of striking vulnerability. LL Cool J’s “I Need Love” in 1987 — a soft, earnest admission of emotional need — stood in productive tension with the bravado that would later become the genre’s commercial signature. These were not merely popular songs. They were cultural touchstones that told young Black people what love could look like, should look like. They were aspirational documents for a community’s interior life. And critically, the women in those songs, in those videos, on those album covers, looked like the community. They were Black women, centered and celebrated.

Something changed in the 1990s, and the change was not accidental. Dr. Dre and Snoop Dogg’s early albums codified a posture of romantic detachment, the deliberate rejection of love and respect for women, into hip-hop’s dominant vocabulary. This was compelling music that sold in enormous quantities, and in selling, it set a template. What had been one strand within a diverse genre became its commercial center of gravity. But the ideological shift ran deeper than misogyny alone. As hip-hop’s commercial footprint expanded through the mid-to-late 1990s and into the 2000s, something subtler and in some ways more psychologically damaging began appearing in the culture’s most visible spaces: the music video. The women cast as aspirational, as desirable, as worth pursuing began, with increasing frequency, to not be Black.

This was not happenstance. It was a pattern deliberate enough to be legible. As rap artists accumulated wealth and crossover appeal, the women featured alongside them in videos on yachts, in mansions, in the visual grammar of success skewed lighter, then non-Black altogether. The message embedded in those images was not subtle to anyone paying attention: arrival meant distance from Blackness. The highest expression of a Black man’s success, as the visual culture of the era constructed it, was access to women who were not Black. Video vixens of lighter complexions were elevated as the standard while dark-skinned Black women were marginalized or absent entirely. The beauty hierarchy being constructed in plain sight on BET and MTV was one in which Black women occupied an increasingly precarious position in the desirability calculus of their own community’s most prominent cultural exports.

By the time “No Scrubs” arrived in 1999, it landed in a culture already primed for conflict. Co-written by Kandi Burruss and Tameka “Tiny” Cottle during their downtime from Xscape, the song was a declaration of standards — women demanding ambition, respect, and genuine partnership rather than the attention of men riding in the passenger seat of someone else’s car. The demands were not unreasonable. Demands that ironically, many Black men would declare normal and reasonable from non-Black women. And within a media landscape designed to amplify division, what began as standard-setting quickly escalated into something more corrosive.

The response was immediate and polarizing. Radio stations hosted debates. BET reportedly edited both videos into a single seven-minute clip of gender war theater. MTV put both in heavy rotation. The media did not merely cover the conflict, it manufactured it into a cultural event, validating in the process the notion that Black men and women were not simply in disagreement but were fundamentally adversarial. Sporty Thievz’s rebuttal climbed to number 12 on the Billboard Hot 100, confirming that the antagonism resonated on both sides of the divide.

What made this moment significant was not the back-and-forth between two songs. It was what that back-and-forth revealed about the direction popular culture was pulling Black romantic life. These songs did not create the tensions between Black men and women. Economic dislocation, the carnage of the War on Drugs, and the structural dismantling of urban manufacturing bases had already placed enormous strain on Black households and Black partnership. Sociologist Elijah Anderson observed that young men in economically marginalized Black communities often pursued social status through the exploitation and diminishment of women, a pattern that commercial hip-hop both reflected and, once amplified at industrial scale, reinforced. The music industry, predominantly white-owned and indifferent to the social consequences of what it distributed, found conflict profitable and invested accordingly. What the community was living, the industry packaged and sold back to it as entertainment.

But HBCU Money still believes in love so enjoy….

The visual erasure of Black women from the aspirational imagination of hip-hop did not stay confined to the screen. It seeped into everyday life with a thoroughness that was difficult to track precisely because it moved through private conversation, social expectation, and the slow accumulation of cultural messaging rather than through any single declarable event. By the early 2000s, a certain strain of public Black male discourse had begun treating dating or marrying non-Black women not merely as a personal preference but as a marker of status, sophistication, or liberation — a signal that one had transcended the presumed limitations of the community one came from. The logic was sometimes stated explicitly, more often implied: that Black women were too difficult, too loud, too independent, too damaged by their own circumstances to be worthy partners for men who had achieved something. The very qualities that had allowed Black women to survive conditions designed to break them were reframed as character defects.

This was not a fringe conversation. It became, with the amplification of the internet and eventually social media, a mainstream one relitigated endlessly in think pieces, radio debates, YouTube channels, and the comment sections of platforms that rewarded provocation over nuance. Black women responded with a mixture of hurt, anger, and their own declarations of independence from a community they felt had devalued them. Some began openly discussing dating outside their race with the same performative energy that had been directed at them. What had begun as a visual preference embedded in music videos had, over the course of a decade and a half, become a full-scale public negotiation over the terms of Black romantic belonging conducted almost entirely in the register of grievance.

The accumulated effect on a generation was not trivial. The words used to describe each other shape how people see each other, expect from each other, and ultimately what they believe is possible between each other. When the dominant narrative in the music young people consumed shifted from devotion to suspicion, from partnership to transaction, from vulnerability to armor, those shifts did not stay contained within the space of entertainment. They became internalized frameworks for courtship, for conflict, for what intimacy was permitted to look like. Young Black women who grew up hearing themselves described as pigeons, hoes, or gold diggers, and who watched the women in their favorite artists’ videos grow progressively less likely to resemble them, absorbed messages about their worth that the external world was already working hard to diminish. Young Black men who absorbed the message that emotional openness was weakness, that Black women were adversaries to be outmaneuvered or obstacles to be bypassed on the road to something better, were being trained away from the very capacities that stable, sustaining relationships require.

Flash forward to 2026, and the cultural inheritance of that era is visible everywhere. Online spaces where Black men and women engage have become, in many corners, theaters of mutual grievance and elaborate performances of self-protective independence that leave little room for the kind of trust that partnership demands. Love songs have become harder to find in mainstream Black pop, as though tenderness has been deemed commercially unviable. Artists like PJ Morton, who make soulful music about Black love in its full complexity, play smaller rooms while music that treats romantic relationships as contests dominates the charts. This is not to suggest that beautiful expressions of Black love have disappeared. They have not. But they have been pushed to the margins of a culture that once placed them at its center.

The stakes of this cultural displacement extend well beyond the personal. As HBCU Money has documented, the marriage rate among African Americans has dropped precipitously over the past several decades, from roughly 60 percent in the 1960s to just 29 percent in 2021 and that decline carries direct economic consequences for the community’s long-term wealth position. Black married couples held a median net worth of $131,000 in 2019, compared to only $29,000 for Black single individuals — a fourfold gap that represents not merely a lifestyle difference but a structural disadvantage in capital accumulation, homeownership, and the ability to transfer wealth across generations. A culture that spent two decades using its most powerful media to communicate that Black women were not the preferred partners of successful Black men, and that Black men were not worthy of Black women’s investment, did not simply produce unhappy relationships. It produced an economic headwind that compounds over time and registers now in the net worth data of an entire community.

None of this means that “No Scrubs” and “No Pigeons” caused the decline of Black marriage or the erosion of Black wealth. They did not. But they were early, loud signals of a cultural drift that institutions like HBCUs, Black media, Black churches, Black family networks were too slow to name and too under-resourced to counter. The music reflected life. But music also shapes life, and the failure to contest the direction that shaping was taking was itself a strategic failure.

The question now is not how to assign blame for the past quarter century. It is whether the community has the institutional will to consciously reconstruct the cultural narrative that was lost. That means creating material and institutional conditions in which stable Black partnership can flourish such as relationship education, financial literacy, community infrastructure that treats Black family formation as a strategic priority rather than a private matter. It means supporting artists who treat Black love as a subject worthy of complexity and craft rather than caricature. It means being deliberate, in public spaces, about the language used to describe one another and understanding that those descriptions accumulate into the expectations young people carry into their most formative relationships.

Before the gender wars, before the videos, before mutual contempt became entertainment and the erasure of Black women from Black men’s aspirational imagination became a cultural norm, Black music told a different story, one in which men and women were engaged in a common project, in which love was not weakness but the foundation of collective strength, and in which the most natural expression of a Black man’s success was a Black woman beside him. That story was not naïve. It was aspirational in the deepest sense: it named what the community was capable of and invited people to live up to it.

That story is still available to be told. The beat can carry a different message. Whether it does depends on what the community decides to demand, to create, and to believe is still possible.

Disclaimer: This article was assisted by ClaudeAI.

African American-owned credit unions hold more than $8.15 billion in assets and serve 726,929 members in 2025, more than doubling their asset base from $3.81 billion in 2016. That growth confirms that Black-owned cooperative finance remains a living, expanding sector — not a historical artifact. Yet placed against the broader credit union landscape, the numbers tell a more sobering story. The federally insured credit union system holds $2.37 trillion in total assets across 4,411 institutions. African American-owned credit unions, with 205 active institutions down from 318 in 2016, control just 0.34 percent of that total asset base. The sector’s 453 Minority Depository Institution-designated peers collectively hold $95.1 billion in assets; African American institutions account for less than 9 percent of that figure. The gap is not closing fast enough.

The structural challenges are as significant as the asset gap. The median African American-owned credit union holds approximately $2.47 million in assets and serves roughly 618 members placing it squarely in the asset tier where the national system is contracting most aggressively, with institutions under $10 million posting declines in assets, membership, and net worth year over year. Only 40 percent of these institutions maintain an active public website, rendering the majority functionally invisible to younger and mobile-first members. An estimated 30 percent are affiliated with religious congregations, compared to approximately 5 percent of all U.S. credit unions, introducing succession and governance risks that extend well beyond normal institutional turnover. Meanwhile, the HBCU-based credit union subsector has seen five of its eleven institutions close or be absorbed since 2020, leaving six survivors holding a combined $76.8 million in assets — institutions that represent the most direct expression of university-anchored Black financial infrastructure and are quietly disappearing without coordinated intervention.

The sector’s geographic concentration compounds these institutional vulnerabilities. Maryland, Mississippi, Missouri, and Virginia together account for roughly 80 percent of all African American-owned credit union assets nationally, while states like California, Minnesota, and Wisconsin maintain only token institutional presences despite substantial African American populations. The South remains the geographic and institutional core, with Louisiana’s 25 institutions representing the largest state count and Mississippi’s Hope Credit Union standing as the sector’s clearest model of what scale and institutional commitment can produce. The path forward runs through consolidation where fragmentation cannot be reversed, digital investment where infrastructure is absent, geographic expansion where populations go unserved, and the fuller utilization of federal support mechanisms such as MDI designation, CDFI certification, and NCUA technical assistance that the sector has historically left on the table.

ADDITIONAL NOTES

African American-owned credit unions now hold $8.15 billion in total assets across 205 active institutions, representing 0.34 percent of the $2.37 trillion held by all federally insured credit unions nationally.

Total assets in the sector have more than doubled since 2016, rising from $3.81 billion — a 114 percent increase — while membership grew 39.5 percent from 521,078 to 726,929 members over the same period.

AACUs average assets per institution: approximately $39.8 million. AACUs median assets per institution: approximately $2.47 million. The gap between the mean and median reflects a sector dominated at the top by a small number of large institutions while the majority operate at a scale that limits their competitive viability.

AACUs average members per institution: approximately 3,546. AACUs median members per institution: approximately 618.

Only 40 percent of African American-owned credit unions maintain an active public website, representing a critical digital infrastructure deficit in an era of mobile-first financial services.

An estimated 30 percent of African American-owned credit unions are affiliated with religious congregations compared to approximately 5 percent of all U.S. credit unions introducing institutional succession risk as American religious participation continues its long-term demographic decline.

Louisiana has the largest number of active African American-owned credit union institutions (25), followed by Illinois (23), New York (15), Texas (14), Virginia (13), and Alabama and the District of Columbia with 12 and 10 respectively. Maryland leads all states in total sector assets at $4.47 billion, followed by Mississippi at $1.05 billion and Missouri at $480 million.

California — the most populous U.S. state and home to one of the largest African American populations in the country — has a single active African American-owned credit union with $318,105 in assets and 262 members, a presence that has contracted since 2016.

The sector’s credit union count has declined from 318 institutions in 2016 to 205 active institutions in 2025, a reduction of 35 percent, driven primarily by closures, mergers into non-Black institutions, and voluntary dissolutions.

For comparison, the national credit union system added 2.9 million members over the past year alone, reaching 143.2 million total members — nearly 200 times the total membership of all African American-owned credit unions combined.

If you torture the data long enough, it will confess to anything. — Ronald Coase

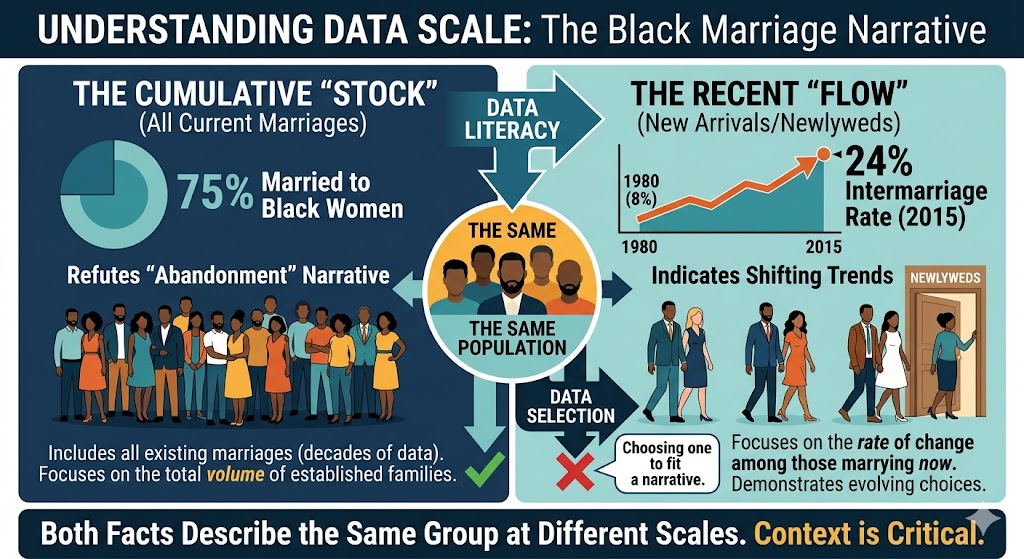

A particular kind of rhetorical move has become standard in Black online discourse around marriage, and it goes roughly like this: Black women claim that Black men are abandoning them for women of other races. Black men respond that the data proves this is false, that the overwhelming majority of Black men who marry do in fact marry Black women. They cite the statistics. They declare the narrative debunked. They move on, satisfied that they have won the argument with evidence.

They have not won the argument. They have answered a question that was not quite being asked, using data that does not quite say what they think it says while simultaneously being correct. This is the uncomfortable, clarifying reality that neither side of this debate has been willing to sit with: both claims are true, they are not in contradiction, and the failure to understand why is fundamentally a failure of data literacy.

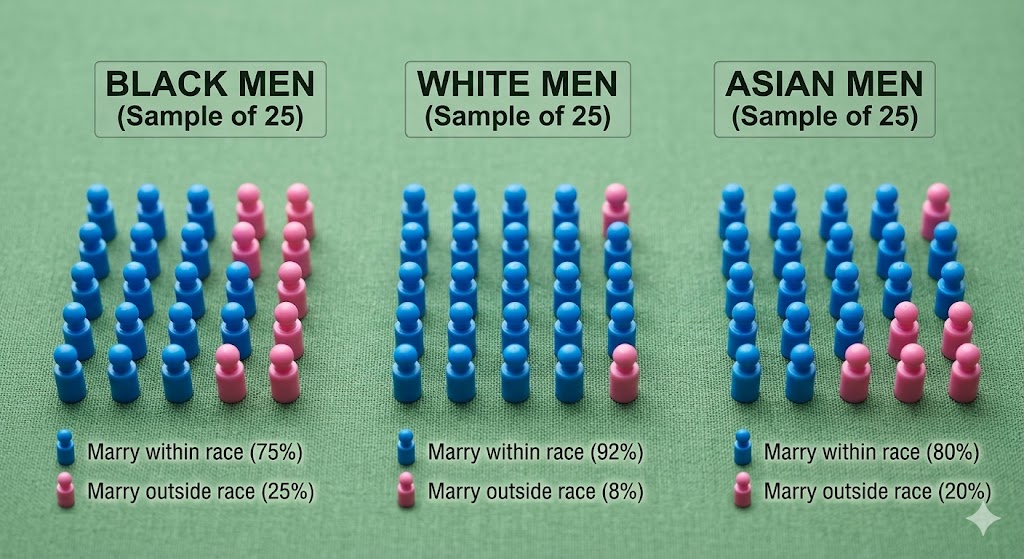

The statistics are not in dispute. According to Pew Research Center analysis of U.S. Census data, roughly 75 percent of married Black men are married to Black women. Among newly married Black men, a more precise cohort that captures current behavior rather than accumulated stock, approximately 64 percent marry Black women. These are majority figures. They are decisive. Any claim that Black men have broadly turned away from Black women as partners cannot survive contact with those numbers, and Black men who cite them in their defense are citing real data correctly.

But here is what that same data also shows, in the same reports, on the same pages: among all groups of men in America, Black men have experienced the fastest-growing intermarriage rate over the past four decades, a rise that is without parallel in the data. In 1980, 8 percent of newly married Black men wed outside the race. By 2015, that figure had reached 24 percent, a tripling of the rate over 35 years, while the Black share of the marriage market remained essentially constant. No other male group comes close to that rate of change.

Intermarriage Rates Among Newly Married Adults, by Race and Gender (Pew Research Center, 2015)

Group

Men

Women

Gender Gap

Black

24%

12%

12 pts (M higher)

Hispanic

26%

28%

2 pts (F higher)

Asian

21%

36%

15 pts (F higher)

White

12%

10%

2 pts (M higher)

Source: Pew Research Center, “Intermarriage in the U.S. 50 Years After Loving v. Virginia” (2017). Newly married = wed within the prior 12 months.

The comparison table requires some careful reading. Hispanic men, at 26 percent, have a nominally higher intermarriage rate than Black men in absolute terms. But Hispanic intermarriage rates have been essentially flat since 1980, shaped by the consistent arrival of immigrant cohorts who marry within their community before subsequent generations integrate more broadly. The Hispanic figure is demographically stable. The Black male figure is demographically dynamic — it moved, substantially and consistently, across a generation.

Intermarriage Rate Trajectory Among Newly Married Men, 1980 vs. 2015 (Pew Research Center)

Group (Men)

1980 Rate

2015 Rate

Black men

8%

24% (+16 pts)

Hispanic men

~26%

26% (flat)

Asian men

26%

21% (slight decline)

White men

4%

12% (+8 pts)

Source: Pew Research Center. Hispanic 1980 figure reflects early ACS-era estimates; trajectory reflects relative stability across the period.

The trajectory table is where the Black male pattern becomes impossible to explain away. A rate that triples over 35 years, in a population whose share of the marriage market did not meaningfully change, is not demographic noise. It is a structural signal. Something changed in the conditions under which Black men form partnerships and the data points consistently toward the same structural variable: education and income mobility. Black men who attain a bachelor’s degree intermarry at 30 percent. Black men without a college degree intermarry at 17 percent. The intermarriage rate is not evenly distributed across the Black male population. It concentrates among those with the credentials and income that predict integration into majority-white professional and social environments.

These two facts are majority intra-racial marriage, fastest-growing intermarriage rate among men describe the same population, measured at different scales. The first is an absolute majority statement. The second is a relative and directional statement about change over time. Neither cancels the other. A community can be predominantly endogamous and simultaneously the demographic group whose male intermarriage rate has grown faster than any other in the country. Both coordinates are necessary to accurately describe the terrain. Choosing to cite only one of them is not data literacy. It is data selection which is a different thing entirely, and always in service of a conclusion reached before the data was consulted.

The impulse behind the selective reading is understandable, even if the execution is flawed. Black men have spent years being characterized in cultural commentary as disloyal, as chasing proximity to whiteness, as leveraging any financial or social ascent to exit the community that produced them. That characterization is often unfair, often reductive, and frequently deployed without statistical grounding of its own. The defensive response, reaching for data that proves the accusation false, is a natural one. But a defensive reading of data is still a compromised reading. When you approach a dataset looking for vindication rather than understanding, you will find the numbers that vindicate you and stop there. The 75 percent figure becomes a shield. The trajectory becomes inconvenient and gets left on the table.

This is precisely what data illiteracy looks like in practice. It is not ignorance of numbers. It is the selective deployment of real numbers to foreclose rather than advance understanding. The person citing the 75 percent is not making a statistical error. They are making an interpretive error by treating a partial truth as a complete one, and treating the absence of explicit contradiction as confirmation. The result is a community that believes it has examined the evidence and settled the question, when in reality it has examined the portion of the evidence that was comfortable and set down the rest.

The gender gap column in the first table is where the conversation should actually be happening. Among every other racial group, the gender intermarriage gap is narrow or runs in the direction of women with Hispanic women and men are essentially equal; Asian women dramatically exceed Asian men; white men and women are within two percentage points of each other. Among Black Americans, the gap is 12 percentage points, and it runs entirely in the direction of men. That gap has been present since at least 1980, and it widens sharply with education: among newly married Black college graduates, 30 percent of men intermarry compared to 13 percent of women. The more education, the wider the gap.

This asymmetry matters because it is not offset. When a Black man marries outside the race, there is no symmetric compensating behavior among Black women. The pool of available same-race partners for Black women, particularly credentialed, economically stable Black women contracts in direct proportion to the Black male intermarriage rate, without equivalent contraction on the other side. Combined with the well-documented effects of incarceration rates on the available Black male population and an educational attainment gap that has shifted decisively toward Black women over three decades, the structural picture that emerges is one of a marriage market with a meaningful and measurable supply-demand imbalance. That imbalance has quantifiable downstream consequences for household wealth formation, given that married households across all racial groups accumulate significantly more wealth than single ones.

None of this is an accusation. It is an accounting. And the distinction matters enormously for how Black communities engage with the question. An accusation calls for defense. An accounting calls for analysis. The man who hears the trajectory data as an indictment of his personal character is reading sociology as if it were a court proceeding. The figures say nothing about any individual’s choices or motivations. They describe population-level patterns with structural determinants, determinants that are, importantly, amenable to institutional response if the community is willing to read the data honestly enough to identify what the actual levers are.

Learning to read data better means, first, understanding the difference between absolute levels and rates of change, and refusing to treat a snapshot as a substitute for a trend. It means placing a number in comparative context not just asking what percentage, but compared to whom, over what period, and moving in which direction. It means sitting with findings that complicate the narrative you prefer, rather than mining the dataset for the figure that ends the conversation on your terms. And it means understanding that two statistics can both be true, can appear to pull in different directions, and can together describe something more accurate and more useful than either describes alone.

Black men are not abandoning Black women en masse. That is true, and the data supports it. Black men have also recorded the fastest-growing intermarriage rate of any male demographic group in America, a rate that has tripled since 1980 and that concentrates among the most educated and economically mobile. That is also true, and the same data supports it. The community that can hold both facts simultaneously without defensiveness and without accusation and ask what structural conditions produce that pattern and what the downstream consequences are for Black household formation and wealth accumulation, is engaging in the kind of rigorous self-examination that serious institutional development requires. The community that cites one number and declares the conversation over is having a different discussion entirely. It is the one that feels better, about a problem it has decided not to fully understand.

Disclaimer: This article was assisted by ClaudeAI.

When the missionaries came to Africa they had the Bible and we had the land. They said ‘Let us pray.’ We closed our eyes. When we opened them we had the Bible and they had the land. – Desmond Tutu

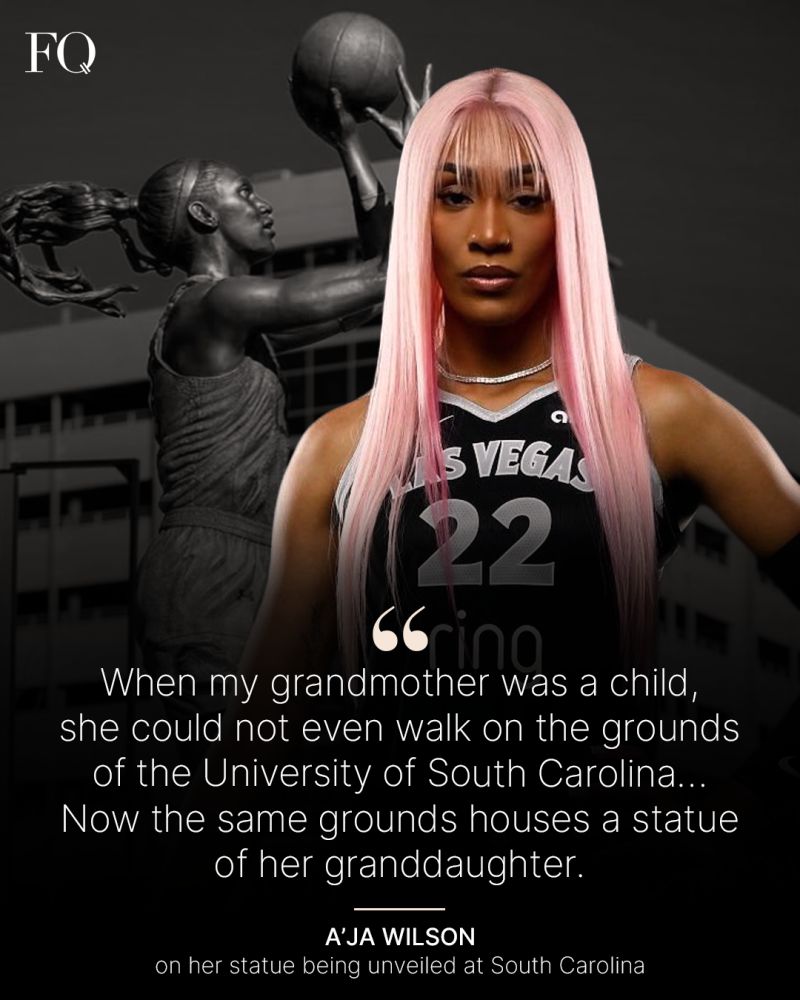

The image is powerful: A’ja Wilson, WNBA superstar and Olympic gold medalist, immortalized in bronze on the grounds of the University of South Carolina. Wilson herself captured the poignancy of the moment in a quote that went viral: “When my grandmother was a child, she could not even walk on the grounds of the University of South Carolina… Now the same grounds houses a statue of her granddaughter.”

It’s the kind of story that gets shared across social media, celebrated in sports columns, and held up as evidence of how far we’ve come as a nation. But is it? Is this progress, or is this something else entirely? Is this the culmination of the civil rights movement, or is it the very thing that movement warned us about—the integration of individuals while the institutions built to serve the community crumble?

There’s another story here, one that rarely gets told in the celebratory press releases and ESPN features. It’s a story about institutional theft, strategic underfunding, and the systematic gutting of Black educational institutions that continues to this day. Because while A’ja Wilson’s grandmother couldn’t walk on USC’s campus due to segregation, the institution that would have educated her, South Carolina State University has been financially starved for generations to help build the very programs that now celebrate diversity milestones.

Before we dive deeper into the numbers, we must ask a fundamental question: Who determines what progress looks like for the African American community? This question cuts to the heart of the paradox surrounding A’ja Wilson’s statue and the underfunding of HBCUs. African America has long suffered from a destructive pincer movement between two ideological forces, both claiming to know what’s best for Black communities, neither actually serving those communities’ interests. On one side sits conservative ideology, committed to choking resources from Black institutions through “fiscal responsibility” rhetoric and states’ rights arguments that echo the same justifications used to maintain segregation. This path leads to institutions like South Carolina State University being denied half a billion dollars while legislatures claim budgets are tight and everyone must sacrifice equally ignoring that the sacrifices are never equal.

On the other side sits liberal ideology that views the disappearance of distinctly African American institutions not as a tragedy but as the ultimate goal. In this worldview, true progress means Black students dispersed throughout predominantly white institutions, Black neighborhoods giving way to “diverse” communities, and HBCUs eventually becoming obsolete historical footnotes and relics of a segregated past we’ve happily moved beyond. Both roads lead to the same destination: the destruction of Black institutional power, Black economic infrastructure, and Black self-determination. One just has sugar on top.

The conservative approach is at least honest in its hostility. Budget cuts, funding formulas that disadvantage HBCUs, and legislative indifference make their intentions clear. But the liberal approach is perhaps more insidious because it wraps institutional decimation in the language of progress, integration, and opportunity. It celebrates the statue while ignoring the $500 million debt. It applauds diversity in predominantly white spaces while shrugging at the decline of Black spaces. This false choice between resource starvation and institutional disappearance has been forced upon African American communities for six decades. Meanwhile, no one asked whether the Jewish community should close Yeshiva University to prove they’ve integrated. No one suggests that Catholic universities are relics of discrimination that should fade away. No one celebrates the closing of women’s colleges as a victory for gender equality. Yet HBCUs are expected to gracefully accept their decline as the price of progress. And when they struggle due to systematic underfunding, that struggle is presented as evidence that they’re no longer necessary rather than proof that they’ve been deliberately undermined.

Real progress would mean African American communities having the power to determine their own institutional futures. It would mean robust, well-funded HBCUs and access to all institutions. It would mean integration as addition, not subtraction and expanding opportunities without destroying the institutions that served the community when no one else would.

According to Forbes reporting, South Carolina State University has been underfunded by nearly $500 million over the years. This isn’t an accident or an oversight it’s a pattern repeated across the nation. Much of that funding that should have gone to SC State was instead redirected to predominantly white institutions like USC, enabling them to build state-of-the-art facilities, offer competitive scholarships, and recruit top talent like A’ja Wilson. The results speak for themselves: USC now boasts a $1.1 billion endowment as of 2025, while South Carolina State struggles with just $17.2 million. That’s not a typo—USC’s endowment is more than 60 times larger than the institution that was created specifically to serve Black students when USC wouldn’t admit them. Let that sink in for a moment. The money that could have made SC State a powerhouse institution offering world-class facilities, attracting premier faculty, and providing transformational opportunities for thousands of Black students was instead funneled to USC. And now we’re supposed to celebrate that USC has become diverse enough to recruit and celebrate Black athletes while the institution that was built specifically to serve Black students struggles with inadequate funding, aging infrastructure, and an endowment that wouldn’t cover the cost of a single building on USC’s campus. This is not progress. This is resource extraction disguised as inclusion.

The cruel irony of school integration is rarely discussed in polite company. Yes, it was necessary. Yes, it broke down legal barriers that should never have existed. But it also created an economic hemorrhaging from Black institutions that has never been addressed or remedied. Today, less than 10% of African American tuition revenue flows into Historically Black Colleges and Universities. Read that statistic again. Despite making up over 13% of the U.S. population and a significant portion of college students, the institutions built specifically to serve the Black community receive less than a tenth of the tuition dollars spent by Black families on higher education. Where does the other 90% go? Largely to predominantly white institutions that, for decades or even centuries, excluded Black students entirely. Institutions that built their endowments, their reputations, and their infrastructure without ever having to serve Black communities—until it became politically and economically advantageous to do so.

The financial disparity tells only part of the story. HBCUs have experienced a devastating brain drain over the past six decades, a loss of intellectual capital, leadership talent, and institutional knowledge that would be considered catastrophic in any other context. The nation’s brightest Black students, who once had little choice but to attend HBCUs, now have the option to attend any institution. On its face, this seems like unqualified good news. But when those predominantly white institutions actively recruit Black talent while simultaneously supporting state funding mechanisms that starve HBCUs, the result is predictable: HBCUs lose both the students and the resources, creating a vicious cycle of decline.

This brain drain extends beyond students. Faculty members, seeing better funding and facilities elsewhere, often make the rational choice to leave. Donors, wanting to support institutions perceived as prestigious or on the rise, redirect their giving. Athletes, artists, and future leaders choose schools with newer facilities and bigger budgets. And with each departure, the HBCU left behind grows weaker, making it harder to compete for the next generation of talent. The students who remain at HBCUs often from lower-income backgrounds, first-generation college students, or those specifically committed to the HBCU mission deserve the same quality of education and resources as their peers at heavily-funded state flagships. Instead, they attend institutions forced to do more with less, year after year, generation after generation.

State governments have become expert at justifying HBCU underfunding through seemingly neutral “funding formulas” based on enrollment numbers, research output, and facility utilization. This is where conservative fiscal ideology and liberal integrationist ideology converge into a unified assault on Black institutional sustainability. These formulas ignore the historical context that created the disparities in the first place. How can an HBCU compete on research output when it’s been denied the laboratory facilities, equipment, and graduate programs that enable such research? How can it boost enrollment when prospective students see crumbling buildings next to a predominantly white institution’s gleaming new science complex—built partially with funds diverted from the HBCU’s budget? How can it improve facility utilization when it doesn’t have the capital to build new facilities in the first place?

Conservative legislators champion these “neutral” formulas as fiscally responsible governance, conveniently ignoring that the formulas are designed to perpetuate historical inequity while providing political cover for continued discrimination. Meanwhile, liberal voices remain largely silent about these formulas because they don’t fundamentally object to HBCU decline, they’ve happily accepted the premise that integration means these institutions should eventually fade away. Arguably, many liberals quietly support conservatives as a means to an end of their agenda. The result is the same regardless of which party controls the statehouse: HBCUs lose funding, infrastructure deteriorates, and the institutional capacity of the Black community diminishes. The conservative approach does it through direct budget cuts and “objective” formulas. The liberal approach does it through purposeful neglect and celebrating individual success stories at PWIs as proof that separate institutions are no longer needed. Both roads, sugar-coated or not, lead to the same hell.

South Carolina State University’s $500 million funding gap didn’t happen overnight. It’s the accumulated result of decades of choices—choices to prioritize USC over SC State, to invest in predominantly white institutions while allowing the HBCU to make do with aging infrastructure and limited resources. The numbers tell a devastating story. As of June 2024, the University of South Carolina’s endowment reached $1.044 billion, a figure that crossed the billion-dollar threshold for the first time in the institution’s history. By October 2025, it had grown to $1.1 billion with a 12.8% return that exceeded median returns for similar institutions. This massive war chest funds scholarships, faculty recruitment, research initiatives, and state-of-the-art facilities. Meanwhile, South Carolina State University’s endowment stood at approximately $17.2 million as of 2023. Let that disparity sink in: $1.1 billion versus $17.2 million. USC’s endowment is more than 60 times larger than SC State’s. USC can establish endowed faculty chairs for $1.5 million, name entire departments for $3 million, and fund comprehensive scholarship programs all from investment returns alone. SC State struggles to fund basic operations.

This isn’t coincidence. This is the direct result of systematic resource allocation that has funneled state support, donor dollars, and institutional advantages to USC while SC State has been left to survive on scraps. When the state underfunds SC State by $500 million over the years and redirects those resources to USC, this is the inevitable outcome: one institution accumulates generational wealth while the other fights for survival. USC used this enormous financial advantage to build a basketball program capable of recruiting a generational talent like A’ja Wilson. It constructed state-of-the-art training facilities, hired top-tier coaches with competitive salaries, and created an environment where champions could be developed. The USC Foundations managed portfolio supports permanent, invested funds that ensure long-term financial stability, the kind of stability that allows an institution to compete for the best students, faculty, and athletes. All admirable goals except when achieved partially through funds that should have gone to the state’s HBCU, and when celebrated as “progress” while the disparity grows ever wider.

To SC State’s credit, it is fighting back. The university raised over $6 million in the 2024-25 fiscal year and achieved a 15.2% alumni giving rate as of July 2025, a remarkable achievement given the economic challenges many HBCU alumni face. But even record-breaking fundraising cannot overcome a 60-to-1 endowment disadvantage created by generations of state-sanctioned discrimination. This isn’t ancient history. Forbes reported on this ongoing underfunding in recent years, documenting a pattern of systematic disinvestment that continues today. While we celebrate milestones like statues on integrated campuses and billion-dollar endowments at predominantly white institutions, the institutions that educated Black students when no one else would continue to be starved of resources, their endowments a fraction of what they should be, their futures perpetually uncertain.

True progress would be A’ja Wilson’s statue at USC and South Carolina State University receiving its full $500 million in owed funding (plus interest). Progress would be that less-than-10% of Black tuition dollars flowing to HBCUs becoming 70%, 80%, or 90%. Progress would be state legislatures across the nation acknowledging decades of discriminatory funding and implementing genuine remedies, not just apologies. Progress would look like HBCUs having facilities that rival their state flagship counterparts. It would mean competitive faculty salaries that stop the brain drain. It would mean endowments built through equitable state funding and private investment that reflect the institutions’ importance to American education. Instead, we get symbolic victories while the infrastructure crumbles. We celebrate individual Black excellence at predominantly white institutions while the institutions built to serve Black communities struggle to keep the lights on.

Acknowledging this reality doesn’t require diminishing A’ja Wilson’s achievements. She is an extraordinary athlete and role model who has earned every accolade. The issue isn’t her success or where she chose to attend college, the issue is a system that presents her individual achievement as collective progress while systematically defunding Black institutions and using integration as justification for that defunding. Fixing this requires several concrete steps. State legislatures must conduct honest audits of HBCU funding over the past 60 years and develop remediation plans to address documented underfunding. South Carolina owes SC State $500 million and that debt should be acknowledged and paid. This isn’t charity; it’s restitution for documented, systematic discrimination. Endowment equity must be addressed directly. When USC holds $1.1 billion while SC State holds $17.2 million—a 60-to-1 disparity—that gap didn’t emerge from market forces or donor preferences alone. It resulted from decades of state policy that enriched one institution while impoverishing the other. South Carolina should establish a dedicated endowment equalization fund, potentially matching private donations to SC State dollar-for-dollar until the disparity is meaningfully reduced.

Federal policy (one day) must address the structural disadvantages HBCUs face in funding formulas, perhaps through direct appropriations that account for historical discrimination. The current system perpetuates inequality under the guise of neutrality. Alumni of all institutions, but particularly successful HBCU graduates at predominantly white institutions, must direct resources back to HBCUs to help stop the financial bleeding. Every major gift to a PWI with a billion-dollar endowment is a choice not to support an HBCU fighting to survive. And perhaps most importantly, we must change the narrative. We must stop treating the closure or decline of HBCUs as inevitable or even acceptable. These institutions represent irreplaceable cultural and educational resources that deserve investment, not managed decline. A $17.2 million endowment for an institution serving thousands of students is a scandal that should generate the same outrage as crumbling infrastructure or contaminated water supplies.

A’ja Wilson’s grandmother couldn’t walk on USC’s campus as a child. That was wrong, and it’s right that those barriers no longer exist. But her grandmother could have attended South Carolina State University, an institution that has been systematically underfunded for generations, partially to build up institutions like USC. That underfunding continues today, as true now as it was decades ago. So when we celebrate the statue, what exactly are we celebrating? The opening of doors, or the closing of others? Individual achievement, or institutional destruction?

The question of whose version of progress we accept matters deeply. The conservative approach would deny South Carolina State its $500 million and call it fiscal responsibility. The liberal approach celebrates the statue as proof we’ve moved beyond needing institutions like SC State. Both ideologies, whether through resource starvation or purposeful neglect disguised as integration, arrive at the same endpoint: weakened Black institutions and diminished Black institutional power. But there’s a third path, one that rejects this false choice entirely. It’s a vision of progress defined by and for the African American community—one that says we can have A’ja Wilson’s statue at USC and a fully-funded South Carolina State University with facilities that rival any institution in the nation. One that recognizes robust HBCUs as evidence of progress, not obstacles to it.

We can hold all these truths simultaneously. We can celebrate individual achievements while demanding that the institutions built to serve Black students receive the funding and support they deserve. We can acknowledge barriers broken while refusing to accept that the gutting of Black institutions is an acceptable price for that change whether that gutting comes from conservative budget cuts or liberal narratives that view HBCU decline as inevitable evolution. Until we do, stories like A’ja Wilson’s statue will remain bittersweet moments of individual triumph shadowed by institutional injustice, symbols that raise more questions than they answer about what progress actually means and who gets to define it. And the power to define what progress means will remain in the hands of those who have never had to worry about the survival of their own institutions.

The question isn’t whether A’ja Wilson deserves her statue. She absolutely does. The question is whether South Carolina State University deserves its $500 million. It absolutely does, too. And until that debt is paid, we haven’t truly addressed what integration cost or what real progress requires. More importantly, until African American communities have the power to define progress for themselves to build and sustain their own institutions without being forced to choose between resource starvation and institutional disappearance we’re still living with the consequences of other people’s definitions, other people’s choices, and other people’s versions of what our future should look like. Both roads of conservative resource choking and liberal institutional disappearance lead to the same hell. One just comes with celebration, statues, and sugar on top. Real progress would mean building a new road entirely.

Disclaimer: This article was assisted by ClaudeAI.

“We must understand Africa, not just as a motherland, but as a partner in destiny. Anything less risks repeating the same colonial footprints we so passionately denounce.” – Dr. Ayodele Moore, Diaspora Strategist

There is a story told about a river that, after centuries of being dammed, rerouted, and renamed by those who neither lived along its banks nor drank from its waters, finally broke through and began flowing again toward the sea. The people downstream celebrated. They built rafts and canoes and set out with great feeling, paddling hard toward the sound of the ocean they had always known was there. But feeling is not navigation, and a raft is not a fleet. Many paddled in circles. Some washed ashore on banks they did not recognize, without maps, without provisions, without a plan for what came next. And some — and this is the part of the story most often left out — arrived upstream, where people already lived, already fished, already governed the water according to their own knowledge and custom. The arrivals called out in the language of kinship. We share this river, they said. We come from the same source. And that was true. But kinship is not a governance structure. It is not a trade agreement or a land compact or a system of shared decision-making. The people who already lived there had heard the language of kinship before, spoken by others who also believed their shared geography entitled them to a kind of authority they had never been asked to hold. Kin can be pariah. Blood can arrive as burden. The question the upstream people were asking was not whether the arrivals were family. It was whether they had come to fish together or to tell them how to fish. A few of the arrivals understood the difference. They put down their nets, picked up their ears, and asked what the river needed, not what they needed from it. Those were the ones who stayed. Those were the ones who built something that lasted. The difference between those two groups was not the sincerity of their return. Both had crossed the same distance with equal longing. The difference was institutional humility, the willingness to arrive not as rescuers but as partners, not with a deed but with a blueprint drawn in consultation with the people who had never left.

There is a moment, familiar to anyone who has traveled to Accra or Kigali or Lagos with serious intent, when the romance of return meets the weight of reality. The streets are alive, the culture is rich, the people are brilliant, and the infrastructure like roads, power grids, financial systems, legal frameworks is visibly strained under the pressure of decades of underdevelopment, debt dependency, and strategic neglect by the global order. It is in that moment that a genuine question must be asked: What did you come here to do?

For a growing number of African Americans, the answer to that question has been shaped more by exhaustion than by strategy. The relentless psychological toll of American racial violence, the compounding weight of systemic disenfranchisement, and the spiritual hunger for belonging have conspired to produce a powerful movement of emotional return. Ghana’s “Year of Return” in 2019 drew tens of thousands. Real estate investment seminars fill hotel ballrooms in Nairobi. Digital nomad communities in Kigali have become gathering points for African Americans seeking a life unburdened by the particular cruelties of the American racial experience. The sentiment is understandable. In many ways, it is noble.

But sentiment is not a development strategy, and exhaustion is not a foreign policy. If the African American engagement with Africa is to produce something durable, something that genuinely advances the interests of both communities and begins to reverse five centuries of enforced separation it must be rebuilt on a foundation that the current movement, for all its energy, largely lacks: institutional architecture, geopolitical literacy, and a clear-eyed understanding of what Africa actually needs from its diaspora.

The longing to return is ancient and legitimate. It is rooted in the singular horror of the Middle Passage, in the deliberate erasure of language, lineage, and tribal identity that made the enslaved African in America a person without a past. For generations, Africa has served as both symbol and salve, a place of imagined wholeness in the face of a history designed to fragment. That emotional current is not to be dismissed. But it must be disciplined. The history of diaspora engagement with Africa is not uniformly redemptive. It contains within it a cautionary architecture that deserves serious examination before the next wave of African Americans boards a plane with a one-way ticket and a venture capital pitch deck.

Liberia remains the most instructive example in this tradition. Conceived in the early nineteenth century with the support of the American Colonization Society as a destination for freed African Americans, Liberia was presented as the fulfillment of Pan-African possibility, a sovereign Black republic on African soil. In practice, it became something considerably more complicated. The Americo-Liberian settlers who arrived brought with them not only their ambitions but their cultural frameworks, legal structures, and social hierarchies; frameworks that often positioned indigenous Liberians as lesser participants in their own land. The result was not liberation but stratification. Decades of resentment between settler elites and indigenous communities contributed directly to the political instability that eventually consumed the country in civil conflict. The lesson embedded in that history is not that return is wrong, but that return without humility, without partnership, and without institutional reciprocity carries the seeds of its own failure.

The current generation of returning African Americans is making, in updated form, some of the same structural errors. The dominant architecture of today’s return movement is personal, not institutional. It is driven by influencers, entrepreneurs, lifestyle architects, and individual investors; people moving with personal capital and personal vision, without the enduring infrastructure that serious engagement with sovereign nations requires. Europeans operating on the African continent do not arrive with YouTube channels and branding strategies. They arrive with state-backed development agencies, sovereign wealth instruments, bilateral trade agreements, and long-term infrastructure commitments. China’s engagement with Africa over the past two decades whatever its own contradictions and extractive tendencies has been defined by institutional presence: development banks, construction conglomerates, diplomatic missions, and educational exchange programs operating at scale. African Americans, who possess over $1.8 trillion in annual spending power according to Federal Reserve data, have no comparable institutional platform for continental engagement. That asymmetry is not incidental. It is the central strategic problem.

The geopolitical dimension of this failure is more consequential than most discussions of African American return acknowledge. Africa is, at this moment, one of the most intensely contested arenas in the contemporary great power competition and it is a competition in which no African nation currently holds great power status. The United States, China, Russia, France, Turkey, and the Gulf states are all actively vying for strategic positioning across the continent, deploying capital, military arrangements, media influence, and diplomatic pressure to shape African governance in directions that serve external interests. France maintains a network of military bases and monetary arrangements across francophone West Africa that amount to a continuation of colonial economic control. China’s Belt and Road infrastructure investments, while filling genuine gaps, have generated significant debt obligations and have been structured in ways that prioritize Chinese labor and supply chains over African employment and industrial development. Russia’s Wagner Group, rebranded but operationally continuous under successor arrangements, has traded security for mineral access across the Sahel. The United States, through AFRICOM and shifting aid priorities, conducts its own version of strategic competition under the language of partnership and democracy promotion.

In this environment, Africa is not a blank landscape awaiting diasporic idealism. It is a geopolitical battleground in which African nations are fighting, with varying degrees of success and sovereignty, to chart independent developmental paths. The African Union’s Agenda 2063 represents an ambitious framework for continental self-determination encompassing economic integration, infrastructure development, digital transformation, and political union. But frameworks do not build themselves. They require capital, technical capacity, institutional support, and allies who are genuinely interested in African sovereignty rather than in African resources. African Americans, if they are serious about return, must understand themselves as potential actors in this geopolitical landscape not as refugees from American racism seeking personal sanctuary, but as a diaspora with institutional capacity, democratic literacy, and strategic interests that are genuinely aligned with African self-determination in ways that no other external actor can claim.

That alignment, however, only becomes geopolitically meaningful if it is expressed institutionally. Individual African Americans relocating to Accra or investing in Rwandan real estate do not register as actors in great power competition. A coordinated network of HBCU research partnerships, the seventeen African American-owned banks and approximately two hundred and five African American credit unions that together hold roughly $15 billion in assets forming correspondent banking relationships across the continent, professional associations running formal mentorship and knowledge-transfer pipelines, and diaspora development funds deploying patient capital into African infrastructure is a presence that registers. That is the difference between a cultural moment and a strategic movement. And the strategic geography of that movement must extend beyond Africa alone. The Caribbean represents an underutilized first frontier in the construction of African American institutional power abroad. Nations like Jamaica, Trinidad and Tobago, Barbados, Haiti, and the Bahamas are majority African-descended, hold seats in the United Nations, cast votes in multilateral institutions, and exercise sovereign influence over global negotiations on trade, climate, and finance. They share history, culture, and bloodlines with African Americans, and they face structural challenges like undercapitalization, climate vulnerability, debt dependency, and narrow economic bases where HBCU expertise in agriculture, engineering, public health, and law is directly applicable. By establishing enduring institutional partnerships with Caribbean governments, African American institutions can extend their effective reach onto the world stage before attempting the more complex architecture of continental African engagement. Through these connections, African America ceases to operate as an isolated domestic minority and begins to function as part of a larger bloc of African-descended sovereign power. The Jewish community offers a relevant comparative model here: its global institutional influence was built not only through domestic lobbying but through sustained formal ties with Israel and institutional networks across multiple continents, fusing homeland and diaspora into a single field of coordinated action. African America has the population, the spending power, the intellectual infrastructure, and the historical relationships to construct an equivalent architecture, one that runs from Kingston to Accra, from Port of Spain to Lagos, from Bridgetown to Nairobi. What has been absent is the institutional will to formalize these connections into channels of durable power. HBCUs, with their transcontinental alumni networks and demonstrated capacity for international academic partnership, are the logical anchors of that architecture. The question is whether their leadership is prepared to govern accordingly, not merely as presidents of universities, but as stewards of institutions with genuinely global strategic responsibilities.

The financial architecture of that movement begins with an honest accounting of what African America currently controls and what it could deploy. The seventeen African American-owned banks and approximately two hundred and five African American credit unions that together hold roughly $15 billion in assets represent a modest sum measured against the balance sheets of the institutions that currently dominate African lending; the Industrial and Commercial Bank of China ($7.6 trillion), the European Investment Bank ($553 billion), or the constellation of French financial institutions that retain structural influence across francophone Africa. But scale is not the only relevant variable in development finance. African nations, and particularly smaller economies across the Caribbean and Africa Core, are not simply starved of capital in the aggregate. They are starved of capital that arrives without the political conditionalities, debt structures, and supply chain requirements that characterize lending from the IMF, the World Bank, and bilateral creditors with their own strategic agendas. A correspondent banking network anchored by African American financial institutions would not need to outcompete Chinese or European capital in volume to be strategically significant. It would need only to offer an alternative, one structured around developmental priorities rather than extraction, governed through relationships of genuine partnership rather than creditor leverage, and oriented toward building the local financial infrastructure that African economies require to reduce their dependency on external financing altogether. A Pan-African diaspora ETF, co-managed by African American asset managers and African financial institutions, would allow retail investors to participate in African market growth while ensuring that the governance structure reflects African stakeholder interests rather than reproducing the extractive dynamics of Western investment vehicles. These are not futuristic proposals. They are applications of existing financial infrastructure to a strategic purpose that currently lacks coordination.

The economic complementarity between African America and Africa is more substantial than is commonly recognized on either side of the Atlantic. African Americans collectively generate over $259 billion in discretionary spending power. The African continent, for its part, represents one of the most significant growth frontiers of the twenty-first century: the African Development Bank projects the continent’s collective GDP will exceed $29 trillion by 2050, driven by a young and rapidly urbanizing population that will constitute roughly a quarter of humanity within that same timeframe. Africa’s agricultural sector alone constrained by underinvestment in technology, irrigation, and storage infrastructure feeds over a billion people today while operating at a fraction of its productive potential. Its renewable energy resources, from solar across the Sahel to geothermal in the East African Rift Valley, are among the largest underdeveloped clean energy reserves on the planet. Its digital economy, growing at rates that consistently outpace global averages, is producing a generation of fintech innovators, software developers, and technology entrepreneurs who are building financial and commercial infrastructure largely from scratch. African America, with its concentrations of professional expertise in medicine, law, engineering, agriculture, and finance produced in disproportionate measure by HBCUs is positioned to contribute technical capacity across precisely these sectors.

The agricultural connection deserves particular attention because it is where the institutional architecture on both sides of the Atlantic most directly converges. The nineteen 1890 land-grant HBCUs, institutions such as Tuskegee University, Prairie View A&M, North Carolina A&T, and Florida A&M, were established precisely to develop applied expertise in agricultural science, soil management, and food systems. That expertise is directly transferable to Africa’s agricultural challenges. A financing model is already being conceptualized domestically: a proposed “1890 Fund” would pool $1 million commitments from each of the nineteen 1890 institutions into a unified lending vehicle, deployed through African American-owned banks and credit unions to finance Black farmers and agricultural producers. The logic of that model extends naturally across the Atlantic. The same cooperative lending architecture designed to recapitalize African American farmers facing discriminatory credit markets in the American South could be adapted to provide African smallholder farmers and agricultural cooperatives with access to capital that arrives without the conditionalities and structural dependencies that characterize lending from multilateral institutions with competing strategic agendas. A transatlantic agricultural finance corridor linking 1890 HBCU extension programs, African American financial institutions, and African agricultural ministries and cooperatives would position African American institutions as genuine development partners in one of the sectors where Africa’s need and African America’s institutional capacity most precisely align. The global contest for food security is intensifying, and nations that can finance, research, and govern their own food systems will occupy an increasingly strategic position in the twenty-first century order. African America and Africa, coordinating institutionally across this sector, would be building toward exactly that kind of sovereignty together. The relationship between the two communities is therefore not one of donor and recipient. It is one of complementary assets in search of coordinating institutions. What neither community has yet built is the architecture that would allow those complementary assets to find each other systematically, at scale, and on terms that serve both parties rather than the intermediaries who currently profit from their separation.

The institutional vehicles for this kind of engagement already exist in partial form and require scaling rather than invention from scratch. Historically Black Colleges and Universities represent the most important underutilized asset in this architecture. With over one hundred institutions spanning agricultural science, engineering, law, medicine, business, and the humanities, HBCUs possess precisely the intellectual and technical capacity that African development requires. The potential for joint degree programs between HBCUs and African universities is not speculative it is already happening, and the early results deserve serious attention. Claflin University, an HBCU in Orangeburg, South Carolina, and Africa University in Zimbabwe have formalized a collaboration that produced its inaugural cohort of graduates, young scholars awarded Master of Science degrees in Biotechnology and Climate Change through a fully online program bridging both institutions. The significance of that program extends beyond its enrollment numbers. By operating fully online, it sidesteps the prohibitive costs and restrictive visa policies that routinely prevent African students from accessing graduate education in the United States, allowing scholars to remain embedded in the communities they intend to serve rather than being uprooted from them. The field selection is equally deliberate. Biotechnology and climate change are not merely timely academic disciplines they are the strategic terrain on which African food sovereignty, public health infrastructure, and energy independence will be won or lost across the next generation. That Claflin and Africa University chose these fields as the foundation of their partnership reflects an institutional logic that is precisely the right one: knowledge production oriented toward African developmental priorities, governed cooperatively across the Atlantic, and structured to keep talent anchored in the communities that need it most.

What is missing is the coordinating architecture to scale what Claflin and Africa University have demonstrated is achievable. A formal Africa-HBCU higher education consortium, capitalized by endowment contributions and federal partnership funds, could systematize what is currently episodic faculty exchange, joint research agendas, curriculum co-development, and student pipelines that stretch continuously across the Atlantic rather than depending on the initiative of individual administrators and faculty champions. Recommendations emerging from analysis of this partnership include the development of joint endowment vehicles to fund shared programs and scholarships, reciprocal faculty exchange pipelines, and co-branded research institutes focused on climate change, food security, public health, and digital governance. A Pan-African accreditation framework capable of facilitating mutual degree recognition across diaspora institutions would remove one of the most persistent structural barriers to this kind of collaboration. Tuskegee University’s expertise in agricultural science is directly applicable to food sovereignty challenges facing West African nations. Howard University’s law school could anchor a transnational legal center focused on diaspora citizenship frameworks, international business law, and African Union policy development. Spelman and Morehouse, with their respective strengths in science, medicine, and leadership formation, could establish formal research partnerships with African institutions working on public health infrastructure. None of this requires waiting for a presidential administration to prioritize it. It requires institutional will, coordinating leadership, and the recognition that HBCU engagement with Africa is not a philanthropic gesture but a strategic imperative, one that Claflin University and Africa University have already proven is operational, replicable, and consequential.

What is also missing, and what no amount of capital alone can substitute for, is political literacy. Africa’s complexity resists the simplified Pan-African framing that much of the return movement relies upon. The continent encompasses fifty-four sovereign nations with distinct political economies, legal traditions, ethnic configurations, and developmental trajectories. Regional economic blocs; the Economic Community of West African States, the Southern African Development Community, the East African Community, each operate with their own governance structures and strategic priorities. The African Union, for all its aspirational architecture, remains constrained by the sovereignty tensions and resource disparities of its member states. Debt structures imposed through International Monetary Fund and World Bank conditionalities have shaped the fiscal space available to African governments in ways that any serious investor or institutional partner must understand. The mineral dependencies that underwrite the economic strategies of several African nations create both opportunities and vulnerabilities that diaspora capital must engage with carefully, avoiding the extractive logic that has characterized foreign engagement with African resources for two centuries.

There is also the uncomfortable reality of diaspora gentrification, which requires honest confrontation rather than dismissal. In Accra, in Kigali, in Mombasa, the arrival of middle-class and affluent African Americans empowered by Western wages and the mobility that American passports confer has produced dynamics that local residents describe with a vocabulary borrowed directly from the urban displacement literature of American cities. Rents rise. Local businesses are displaced by foreign-owned establishments marketed in Pan-African aesthetic language but managed with limited local inclusion. Communities that were affordable become stratified. The African American in this scenario occupies a structural position that mirrors, regardless of racial identity, the role of the external gentrifier. This is not an argument against African Americans living and investing on the continent. It is an argument for the structural disciplines that prevent individual mobility from producing collective harm: affordable housing investment rather than luxury development; employment and profit-sharing mechanisms that benefit local communities; governance structures for business ventures that include meaningful African stakeholder ownership rather than token consultation.

The media ecosystem that has driven much of the current return movement has not helped in this regard. Social media’s representation of Africa has been systematically curated toward the aspirational and the aesthetic—luxury compounds, Afrobeat concerts, safari experiences, and carefully framed images of cultural belonging. What is largely absent from this representation is Africa’s political complexity, its infrastructure challenges, its ongoing negotiations with the global order, and the voices of African people articulating what they actually want from their diaspora. African American media institutions like HBCU journalism programs, Black-owned digital platforms, and community broadcasters have an obligation and an opportunity to build genuine media partnerships with African counterparts that produce a more complete and more honest picture of continental life. The romanticization of Africa does not serve African Americans or Africans. It produces a generation of returnees unprepared for the actual work of partnership.

The framework that should govern this entire engagement is mutualism rather than rescue. There is a missionary tradition embedded in African American engagement with Africa one that predates the current movement by more than a century in which the diaspora positions itself as the bearer of civilization, modernity, or salvation to a continent imagined as waiting for external redemption. Today’s version arrives not with Bibles but with tech accelerators and wellness retreats, but the underlying logic is frequently unchanged: Africa as destination for the expression of diasporic benevolence rather than as a partner in a relationship of genuine reciprocity. Africa does not require rescue. It requires the kind of partnership that treats African institutions, African expertise, and African governance as co-equal participants in a shared project of development. The African diaspora in America has survived and produced extraordinary institutional achievement under conditions of extreme adversity. That experience carries real lessons about institution-building, legal strategy, and economic development under pressure, lessons that may be genuinely valuable to African partners. But the learning flows in both directions. Africa’s experience of independence movements, Pan-African political theory, community governance, and developmental economics offers knowledge that African Americans navigating their own institutional challenges would benefit from integrating. Partnership requires the humility to be taught as well as the confidence to teach.

The ultimate measure of the African American return movement will not be the number of people who relocate to the continent, or the volume of real estate transactions completed in Accra, or the number of cultural tours sold in Lagos. It will be the institutional infrastructure that this generation builds or fails to build—the universities linked across the Atlantic, the financial systems connected in ways that allow capital to serve development rather than extraction, the media partnerships that produce honest and complex representations, the legal frameworks that protect diaspora rights while respecting African sovereignty, and the political relationships developed at institutional levels that allow African Americans to function as genuine strategic allies in Africa’s navigation of great power competition. No African nation currently sits at the table where the rules of the twenty-first century order are being written. If the African diaspora in America is serious about return, then the most important contribution it can make is not to escape to Africa but to help build the architecture that gives African nations the institutional capacity, the financial sovereignty, and the strategic positioning to eventually claim that seat. That is a generational project. It begins not with a plane ticket, but with a plan.

Disclaimer: This article was assisted by ClaudeAI.