Land is the only thing in the world that amounts to anything, for it’s the only thing in this world that lasts. It’s the only thing worth working for, worth fighting for… – Ted Turner

Raw land is among the oldest and most durable asset classes available to private investors. For the HBCU community — individuals, families, alumni associations, and institutional partners — it is also among the most underutilized.

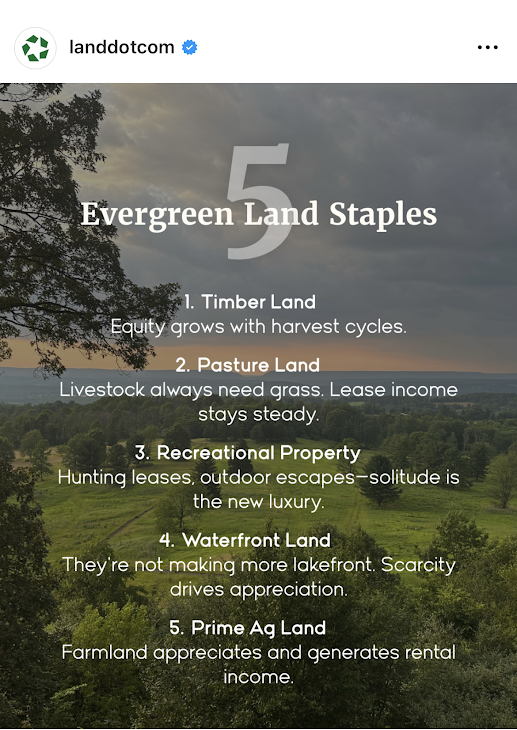

There is a social media post circulating in land investment circles that reads simply: “Forget the luck of the Irish. We prefer the certainty of a deed.” Beneath that caption sits a framework titled “5 Evergreen Land Staples” — timberland, pastureland, recreational property, waterfront land, and prime agricultural ground — each chosen for the same fundamental quality: enduring income or appreciation that does not require the daily volatility management of equities or the tenant fragility of residential real estate. The post is from Land.com, a mainstream marketplace catering primarily to rural landowners. The audience it implicitly addresses is white, rural, and generationally landed. Yet the analytical framework it articulates is precisely what the African American institutional ecosystem needs to operationalize and the HBCU community, with its networks of graduates, alumni chapters, and anchor institutions spread across the American South and beyond, is uniquely positioned to execute it at scale.

The stakes are not trivial. As the Federation of Southern Cooperatives Land Assistance Fund has documented, African Americans own less than 1% of all privately owned rural land in the United States. That figure represents one of the most consequential economic collapses in modern American history, a loss that accelerated across the 20th century through discriminatory lending, heirs’ property dispossession, and the systematic exclusion of Black farmers from federal agricultural credit systems. Between 1910 and 2020, African American land ownership fell by roughly 90%, from an estimated 15–16 million acres to less than 2 million today. Reversing even a fraction of that trajectory requires not only individual decision-making but coordinated institutional action. This article maps a practical framework anchored in the five evergreen land categories for how African Americans at every life stage, and HBCU-affiliated institutions at every organizational level, can begin to build durable land portfolios through structures that keep capital inside the ecosystem.

Before addressing who should invest and how, it is worth establishing why the five categories on that social media post represent genuinely strategic holdings rather than speculative fashions. Timberland is distinctive because its primary asset — standing timber — continues growing in value as long as it stands. As one institutional investor noted at the 2009 Timberland Investment World Summit, timber was the only major asset class not to decline during the Great Recession: “As long as the sun is shining trees will grow and your timber’s value will increase.” For long-horizon investors, which includes endowments, alumni foundations, and family trusts, timberland offers inflation protection, biological growth as a return mechanism, and periodic harvest income that can be timed to liquidity needs. Pastureland generates recurring lease income from ranchers and livestock operators with relatively low management overhead, while the underlying land appreciates over time and the lessee carries operational risk. For a first-generation land investor or a young family with limited bandwidth for active management, a leased pasture parcel generates cash flow from day one. Recreational property, including hunting and fishing grounds, has benefited from the structural shift toward experiential consumption, outdoor recreation spending in the United States now exceeds $780 billion annually and the demand for private access through leased hunting rights or short-term rentals has made rural recreational parcels a viable income source even at modest scale. Waterfront land commands a persistent scarcity premium, as lakefront, riverfront, and coastal parcels face an absolute supply constraint that no amount of construction can remedy, with appreciation rates for quality holdings historically outpacing inland equivalents by substantial margins. Prime agricultural land, the fifth category, combines appreciation and income in proportions that no other asset class consistently replicates, with farmland producing positive real returns in nearly every decade since World War II while the growing global demand for food production adds a structural tailwind that shows no sign of abating.

For the African American individual investor, particularly recent HBCU graduates entering the workforce, raw land is rarely the first investment that financial advisors recommend. Equities, retirement accounts, and residential real estate occupy the conventional hierarchy. This is understandable but strategically incomplete. Raw land, particularly rural parcels in the 10–100 acre range, is far more accessible in price terms than most urban professionals realize. In many parts of the rural South and Midwest, quality pastureland or timberland can be acquired for $1,500–$4,000 per acre, meaning a 20-acre parcel may require a down payment comparable to what urban renters spend in twelve months on housing. The critical discipline for individual investors is to treat the first land acquisition not as a lifestyle purchase but as a strategic asset. A 20-acre timberland parcel generates modest income while the timber matures but builds balance sheet equity that can later be pledged as collateral for subsequent acquisitions, a mechanism that generationally landed families have used for centuries. The key to making this work is choosing land that produces some income immediately, whether through a hunting lease, a hay-cutting arrangement, or a grazing license, so that carrying costs do not exceed cash flow while long-term appreciation accrues. Structurally, individuals should acquire rural land through a single-member LLC rather than in personal name, for both liability protection and eventual transfer efficiency. The LLC structure also allows for the clean addition of family members as equity holders over time, laying the legal groundwork for the next stage of ownership.

A young family with children faces a different calculus than a single investor. The time horizon extends to 30 or 40 years, the need for tax-efficient transfer becomes relevant, and the question of heirs’ property known as the informal, undivided ownership arrangement that has caused the dispossession of millions of acres of Black-owned land must be proactively addressed from the first deed. Heirs’ property arrangements leave undivided interests in land vulnerable to partition sales, through which any one heir can force a sale often to outside buyers at below-market prices. A young family acquiring land today should structure the purchase inside a family LLC or land trust from inception, with a clear operating agreement specifying decision-making rights, buyout provisions, and management authority. This structural discipline costs several hundred dollars in legal fees at formation but eliminates the single greatest mechanism by which Black-owned land has historically been lost. For young families, pastureland and prime agricultural ground are the most suitable of the five categories. Leased to a working farmer on an annual or multi-year cash rent arrangement, these parcels generate predictable income typically $100–$300 per acre annually in productive regions while the family’s equity compounds. Agricultural land near HBCUs, particularly the 1890 land-grant institutions with active extension programs, offers an additional advantage: the university’s agronomic and soil science resources can improve the land’s productivity and rental value over time, particularly where a formal university-farmer partnership exists.

For African American households in the wealth-accumulation or pre-retirement phase, typically those between 45 and 65 with existing equity in residential real estate or retirement accounts, raw land fills a specific portfolio gap. It provides non-correlated returns, inflation protection, and estate planning flexibility that equity-heavy portfolios lack. At this stage, the five-category framework can be pursued more deliberately. Waterfront land and timberland, which require longer holding periods to realize full appreciation, are most appropriate for mature investors who do not need near-term liquidity. A modest timber holding, held for 20 years through a managed investment timberland organization, can produce both periodic harvest income and terminal land value appreciation that substantially outpaces a bond portfolio over the same horizon. Conservation easements on qualifying land parcels offer an additional mechanism: by granting a qualified land trust a permanent easement that restricts development, the landowner receives a federal income tax deduction equal to the value of the development rights surrendered, a tool that high-income African American professionals have underutilized relative to white rural landowners who have deployed it extensively. This is also the stage at which entry into private Real Estate Investment Trust structures becomes viable. A private REIT organized around agricultural or timberland holdings allows a group of accredited investors like friends, family members, or professional associates to pool capital into a formal investment vehicle with a shared land portfolio, professional management, and pass-through tax treatment. Unlike publicly traded REITs, a private land REIT can be sized for a community of 10–50 investors, managed by a professional trustee, and built specifically around the five evergreen categories. The formation cost is meaningful but amortizes quickly across the investor pool, and the structure creates a formal institutional container for what would otherwise remain fragmented individual decisions.

Not every land investment begins with a formal institutional structure. Some of the most durable private wealth in America was built by small groups of trusted individuals such as former college roommates, fraternity and sorority members, professional cohort peers who pooled capital informally before any institution took notice. For the HBCU community, this peer-to-peer investment model is both historically familiar and structurally underdeployed. A group of five former classmates, each contributing $10,000, creates a $50,000 acquisition fund. In rural land markets across the South, that capital is sufficient to purchase 15–30 acres of quality pastureland or recreational property with room for closing costs and an operating reserve. The land is titled inside a jointly owned LLC, the operating agreement governs decision-making and buyout rights, and the group begins building a shared balance sheet that none of them could have assembled individually on the same timeline. The social infrastructure already exists. HBCU alumni networks are among the most tight-knit in American higher education, and the bonds forged between classmates across Greek organizations, residence halls, student government, and athletic programs carry the relational trust that small investment partnerships require above all else. What is missing is not the social capital but the financial framework to convert it into land equity. The practical steps are straightforward: the group agrees on an investment policy covering land category, geographic focus, minimum hold period, and income distribution schedule; forms an LLC with an operating agreement drafted by a real estate attorney; designates a managing member responsible for vendor relationships, lease management, and annual reporting; and commits to a first acquisition within a defined timeframe, preventing the initiative from dissolving into indefinite planning. Over time, these peer land partnerships can grow through reinvested income, additional capital calls, and the addition of new members at formally appraised entry valuations. A group that begins with five classmates and 25 acres can, within a decade of disciplined reinvestment, hold a diversified portfolio spanning multiple land categories across several states anchored not by institutional mandate but by the simple decision of like-minded people to build something together.

HBCU alumni associations sit at the intersection of institutional loyalty and latent investment capital. Most chapters hold reserve funds that have been accumulated through dues, fundraising, and event revenue that are parked in bank accounts earning negligible interest. Very few chapters have formalized investment policies, and this represents one of the most tractable missed opportunities in the HBCU ecosystem. An alumni chapter with $200,000 in reserves can, with proper legal structuring, become a founding limited partner in a private land REIT or a land investment LLC alongside other chapters. Five chapters pooling $200,000 each creates a $1 million acquisition fund capable of purchasing 250–500 acres of quality pastureland, timberland, or agricultural ground in rural markets adjacent to HBCUs. That land, leased and managed professionally, generates annual income that returns to the chapters while the underlying asset appreciates. Over a 15-year horizon, the portfolio can be refinanced to fund new acquisitions replicating the leverage cycle that institutional endowments have used with alternative assets for decades. The governance structure matters enormously. An alumni land partnership should be organized as a limited partnership or private REIT with an independent general partner or trustee, clear investment policy statements, annual audited financial statements, and a defined liquidity event horizon. The informality that characterizes most alumni chapter finances is incompatible with institutional land ownership at scale. But with proper structuring, the alumni network becomes what it has always had the potential to be: a distributed institutional investor class with shared objectives and collective bargaining power. Nationally coordinated alumni associations, the general alumni bodies of the major HBCU systems, are positioned to act at an even larger scale. A national alumni association with 50,000 dues-paying members and a modest per-member investment program could capitalize a seven-figure land acquisition fund within a single fiscal year. Structured as a private REIT with a land-grant mission overlay, specifically acquiring land adjacent to 1890 HBCU campuses or in counties with high concentrations of African American agricultural heritage, such a fund would generate financial returns while simultaneously reinforcing the geographic and economic footprint of the institutions themselves.

The structure of land acquisition matters as much as the acquisition itself, and for the African American investor at every level — individual, family, peer partnership, or alumni association — the financing institution is a strategic choice, not merely a transactional convenience. African American-owned banks hold just $6.4 billion in assets, while African American credit unions hold $8.2 billion, meaning these institutions together control less than $15 billion in combined lending capacity despite serving a market of more than 40 million people — insufficient to exert meaningful influence in national credit markets without deliberate capital infusion from within the community itself. When an African American investor finances a land purchase through a Black-owned bank or credit union rather than a mainstream white-owned lender, the mortgage deposit strengthens that institution’s liquidity ratio, expands its lending capacity through fractional reserve multiplication, and keeps the interest income circulating within the ecosystem rather than exiting to a Wall Street balance sheet. Every dollar deposited into an African American financial institution can translate into multiples of additional lending capacity once multiplied through the banking system — meaning that the collective financing decisions of HBCU alumni and community investors are not merely personal financial choices but acts of institutional capitalization. A community that builds land equity through Black-owned financial institutions simultaneously strengthens two pillars of its economic architecture: the land base that generates long-term wealth and the banking infrastructure that finances the next generation of acquisition.

At the institutional tier, the strategic imperative is even more pronounced. As of 2014, Tuskegee University controlled approximately 5,000 acres, ranking 12th among all American colleges in total land holdings, while Alabama A&M (2,300 acres), Alcorn State (1,756 acres), Prairie View A&M (1,502 acres), Kentucky State (915 acres), and Southern University (884 acres) collectively controlled more than 12,000 acres, placing all six among the top 100 college landowners in the United States. Those figures have not been comprehensively updated in the intervening decade, and the actual current land position of these institutions accounting for acquisitions, dispositions, and reclassifications likely differs. What has not changed is the strategic imperative to treat that land base as a productive investment asset rather than passive institutional real estate. A coordinated commitment of $1 million from each of the nineteen 1890 land-grant HBCUs would create a $19 million revolving fund capable, through its placement in African American banks and credit unions, of generating $7–$10 in agricultural lending capacity for every dollar committed financing not just land acquisition but the full productive cycle of African American farming. That mechanism addresses credit access. The complementary challenge is equity accumulation: deploying HBCU endowment capital, alongside alumni and friends’ capital, into the five evergreen land categories through a structured private REIT. An HBCU-anchored land REIT, capitalized with institutional endowment commitments as the senior tranche and alumni association and individual investor capital as subordinate tranches, would create a properly tiered investment structure with aligned incentives. The endowment’s priority return on its senior capital is protected; alumni investors participate in the upside above that hurdle; and the land itself remains in community-aligned ownership regardless of which investor class holds primacy at any given moment. Over time, the REIT’s land holdings can be diversified across all five evergreen categories — timberland for long-horizon appreciation, pastureland and agricultural ground for current income, waterfront parcels for high-appreciation positioning, and recreational property for near-term income generation — creating a portfolio whose income streams are non-correlated and whose asset values compound independently of equity market cycles.

The five evergreen land categories are individually sound investment ideas. Their strategic power for the HBCU community, however, lies not in isolated individual transactions but in the construction of a layered, coordinated ecosystem from the 22-year-old HBCU graduate purchasing her first 20-acre pasture parcel in Alabama, to the alumni chapter launching a multi-state agricultural REIT, to the 1890 HBCUs deploying endowment capital as the institutional anchor of a Black-managed timberland fund. At the most fundamental level, virtually every economic system man has ever created relies on one undeniable truth: whoever controls the land controls the system. The African American institutional ecosystem has the networks, the talent, and increasingly the structured financial vehicles to re-enter land ownership at meaningful scale. What it requires now is the strategic coordination to treat land not as a nostalgic aspiration but as a compounding institutional asset — one deed, one acre, one fund at a time.

Disclaimer: This article was assisted by ClaudeAI.