“Too many people spend money they haven’t earned, to buy things they don’t want, to impress people they don’t like.” — Will Rogers

In a consumer culture that equates success with spending, African America remains uniquely vulnerable. The historical denial of access to capital and economic agency has not merely constrained African Americans’ ability to accumulate wealth it has warped the cultural psychology of money itself, bending consumption from a utilitarian act into something closer to an identity claim. Now, a small but growing movement within the community is embracing a deliberate counteroffensive: minimalism. The philosophy is straightforward of less spending, less clutter, fewer financial obligations, and more intentional deployment of resources. But the more consequential question is whether this aesthetic and lifestyle ethos can be converted into a durable institutional strategy for wealth building, and whether the infrastructure exists to capture and redirect the capital it might free.

The structural context for this argument is more specific — and more damning — than the familiar headline figures suggest. African American household assets reached $7.1 trillion in 2024, a half-trillion-dollar increase that might appear encouraging at first glance. But the composition of that wealth exposes the mechanism of the problem: corporate equities and mutual fund shares, the asset class that generated the year’s fastest growth at 22.2%, represent less than 5% of African American holdings and a mere 0.7% of total U.S. household equity assets. The community is, in other words, almost entirely absent from the compounding wealth engine that most reliably converts income into intergenerational capital. On the liability side, consumer credit has surged to $740 billion, now representing nearly half of all African American household debt and approaching parity with home mortgage obligations of $780 billion, a near 1:1 ratio that represents a fundamental inversion of healthy household finance. For white households, the ratio stands at approximately 3:1 in favor of mortgage debt over consumer credit. The African American community stands alone in this precarious position. The debt itself flows almost entirely outward: with African American-owned banks holding just $6.4 billion in combined assets, the vast majority of $1.55 trillion in African American household liabilities flows to institutions outside the community, meaning that interest payments, fees, and the wealth-building potential of lending relationships are systematically siphoned away from Black-owned financial institutions. The historical dimension compounds the structural one. Black farmers owned more than 16 million acres of land in 1910; by 1997 they had lost more than 90% of it through state-sanctioned violence and discriminatory structures, a compounded loss estimated at $326 billion. From 1992 to 2002 alone, 94% of Black farmers lost part or all of their farmland, three times the rate at which white farmers lost land. What minimalism confronts, then, is not merely a spending habit. It is a balance sheet in structural retreat where African American households are asset-poor, debt-heavy, and systematically drained by the institutions that hold the debt.

Minimalism is not simply about having fewer possessions or a tidier apartment. It is a structural challenge to compulsive consumption. But for African Americans, consumption frequently functions as both a status signal and a psychological buffer. The legacy of economic exclusion has produced what some economists describe as compensatory consumption purchasing to claim affirmation in a society that has historically devalued Black presence. Designer goods become cultural armor. The latest consumer technology becomes a credential of arrival. Automobiles are more than vehicles; they are visible declarations of survival and dignity. This dynamic has its own historical coherence. In the early twentieth century, Harlem’s “Sunday Best” was less an act of religious observance than a form of public defiance, a counter-narrative to pervasive images of African American poverty and invisibility. The twenty-first-century iteration of that impulse has been systematically captured by brands whose ownership and supply chains are entirely removed from the community’s economic interests. To embrace minimalism, then, is to confront not only consumer capitalism but also the psychological architecture that colonialism and exclusion built. It demands a community-wide renegotiation of what economic success actually looks like and for whom it is being performed.

The utility of minimalism as a wealth-building mechanism is not merely philosophical it is arithmetically demonstrable. A household reducing monthly discretionary spending by five hundred dollars, through fewer restaurant meals, less fast fashion, and deferred consumer electronics, could redirect six thousand dollars annually into productive instruments: a college savings plan, a real estate investment trust with Black ownership, Treasury bonds for capital preservation, equity crowdfunding platforms supporting Black-led ventures, or a direct contribution to an HBCU endowment fund. Over a decade, with even modest returns, that redirected capital compounds into a six-figure investment position. Scaled across one million African American households practicing this discipline, the aggregate represents a wealth transfer of historic proportions initiated not by policy intervention or philanthropic rescue, but by the community’s own redirected consumption decisions. The distinction between compulsive and intentional spending is not a luxury concern. It is the difference between subsidizing someone else’s institutional power and building your own.

The most direct application of minimalism is also the most legible: the household balance sheet. A family that eliminates one financed vehicle and opts for a used purchase outright removes both a monthly payment and an interest obligation, freeing several hundred dollars a month that compound differently when redirected. Choosing a duplex over a single-family home and renting the second unit transforms the primary residence from a consumption asset into an income-producing one — the kind of structural move that converts homeownership from a wealth symbol into a wealth mechanism. Retirement contributions left at the employer match rather than maximized represent another form of consumption by inertia; households that treat the gap between the match ceiling and the IRS contribution limit as a monthly target are effectively building a tax-advantaged investment position that most never access. The same logic applies to life insurance: the difference between a term policy and a whole-life policy, redirected into an index fund over twenty years, is not a marginal decision. These are not sacrifices. They are reallocations — the substitution of visible, depreciating expenditure for invisible, compounding position-building. At scale, if HBCU alumni associations or community organizations created coordinated vehicles to receive and deploy this redirected capital — endowment contributions, community development financial institutions, Black-owned bank deposits — the household discipline becomes institutional fuel. But the household is where the discipline begins and where it is most immediately actionable.

Historically, African America has deployed its dollars as a political instrument. The Montgomery Bus Boycott extracted direct economic cost from a segregated transit system. The 2020 Blackout Day redirected consumer attention toward Black-owned businesses and away from corporations that profited from Black spending without reciprocal investment in Black communities. Minimalism extends this tradition into daily economic practice. It is a sustained withdrawal from the consumption patterns that extractive industries have engineered to capture Black income. Consumer surveillance capitalism studies African American spending behavior in granular detail, refining the advertising systems designed to push more debt, more aspirational luxury, and more financial dependency. Opting out methodically is not merely frugality — it is a form of information asymmetry disruption, denying data that feeds systems designed to work against Black institutional interests.

The objection that minimalism is a privilege of the already comfortable misreads the proposition. For lower-income households, intentional resource management is not a new concept — it is frequently a survival discipline already in practice. What is missing is not the behavior but the infrastructure to leverage it: institutions capable of receiving redirected capital, community platforms that make collective commitment visible and accountable, and frameworks that connect household choices to institutional outcomes. Minimalism as a communal strategy must also extend its frame of reference. Digital minimalism can reduce the tech dependency being engineered into younger generations at enormous cost to family finances. Food minimalism can recalibrate spending patterns distorted by food desert geography. Spatial minimalism can encourage shared community investment over the overcapitalized private home as the primary wealth vehicle. None of these requires material sacrifice — all of them require institutional infrastructure to translate reduced consumption into coordinated capital formation.

Minimalism will not, by itself, undo redlining, reverse discriminatory lending, or equalize inherited wealth. It is a tool, not a solution — one component of a coordinated institutional strategy that also requires political leverage, legal infrastructure, and sustained endowment growth. But it is a tool African America has yet to fully institutionalize. The community already possesses the spending mass. What it requires is the institutional architecture to redirect that mass with precision. The question is not whether African America can afford to consume less. The question is whether it can afford not to.

I would rather earn 1% off a 100 people’s efforts than 100% of my own efforts. – John D. Rockefeller

The contrast is stark and telling. On one screen, a promotional poster for a docuseries about Black wealth features accomplished individuals—entrepreneurs, entertainers, and personal finance influencers. On another, the Bloomberg Invest conference lineup showcases representatives from Goldman Sachs, BlackRock, sovereign wealth funds, and central banks. This visual juxtaposition reveals a fundamental problem in how African American wealth building is conceived, discussed, and ultimately constrained in America: we’re having an individual conversation while everyone else is having an institutional one.

When African American wealth is discussed in mainstream media and even within our own communities, the focus overwhelmingly centers on individual achievement and personal financial literacy. The narrative typically revolves around budgeting tips, entrepreneurship stories, side hustles, and the importance of “building your own.” While these elements certainly matter, they represent only a fraction of how wealth is actually created, preserved, and transferred across generations in America.

Compare this to how other communities approach wealth building. Bloomberg conferences don’t feature panels on how to save money or start a small business. Instead, they convene institutional investors managing trillions of dollars, central bankers who set monetary policy, executives from asset management firms overseeing pension funds, and sovereign wealth fund managers representing entire nations’ financial interests. The conversation isn’t about individual wealth accumulation it’s about institutional capital allocation, market infrastructure, regulatory frameworks, and systemic wealth generation. This isn’t merely a difference in scale; it’s a difference in kind. Individual wealth building, no matter how successful, operates within a system. Institutional wealth building shapes that system.

The economic implications of this gap are staggering. Consider the arithmetic presented in the text message exchange: if approximately 95% of African American debt is held by non-Black institutions, and that debt carries an average interest rate of 8%, African American households collectively transfer roughly $120 billion annually in interest payments to institutions that have no vested interest in Black wealth creation or community reinvestment. This figure isn’t just large it’s transformative. To put it in perspective, $120 billion annually exceeds the GDP of many nations. That likely at least 10% of African America’s $2.1 trillion in buying power is leaving the community for interest before a single bill is paid or single investment can be made. It represents capital that flows out of Black communities without generating corresponding wealth-building infrastructure within those communities. This is the cost of institutional absence.

When communities lack their own lending institutions, investment banks, insurance companies, and asset management firms, they become permanent capital exporters. Every mortgage payment, every car loan, every credit card balance becomes a wealth transfer rather than a wealth circulation mechanism. Other communities long ago recognized this dynamic and built institutional frameworks to capture, recycle, and multiply capital within their own ecosystems.

Institutional wealth building operates on fundamentally different principles than individual wealth accumulation. It involves capital pooling and deployment, where institutions aggregate capital from thousands or millions of sources and deploy it strategically for returns that benefit the collective. Pension funds, for instance, don’t teach their beneficiaries how to pick stocks they hire professional managers to generate returns that secure retirements for entire workforces. Large institutions don’t just participate in markets; they shape them. They influence interest rates, capital flows, regulatory frameworks, and investment trends. When BlackRock or Vanguard shifts their investment thesis, entire sectors respond.

Institutions are designed to outlive individuals. They create mechanisms for wealth transfer that transcend personal mortality, ensuring that capital accumulates across generations rather than dispersing with each estate. By pooling resources, institutions can absorb risks that would devastate individuals, enabling them to pursue longer-term, higher-return strategies that individuals cannot access. Perhaps most importantly, institutional capital commands political attention and shapes policy in ways that individual wealth, however substantial, simply cannot.

The current institutional deficit in African American communities isn’t accidental it’s the product of deliberate historical forces. During the early 20th century, Black communities did build impressive institutional infrastructure. Black Wall Street in Tulsa, thriving business districts in Rosewood, Florida, and numerous Black-owned banks, insurance companies, and investment firms represented genuine institutional wealth building. These were systematically destroyed sometimes literally, as in the Tulsa Race Massacre of 1921, and sometimes through discriminatory policies, denial of business licenses, exclusion from capital markets, and targeted regulatory enforcement. The institutions that survived faced existential challenges during desegregation, as the most affluent Black customers gained access to white institutions that had previously excluded them. The result is that African Americans today face a unique challenge: rebuilding institutional infrastructure in a mature capitalist economy where the institutional landscape is already dominated by established players with centuries of accumulated capital, networks, and political influence.

Given this context, why does African American wealth discourse remain so focused on individual action? Several factors contribute to this pattern. American culture celebrates individual achievement and self-made success. This narrative is particularly seductive for African Americans seeking to overcome discrimination through personal excellence. However, it obscures the reality that most substantial wealth in America is institutional, not individual. Teaching people to budget or start a business is concrete and actionable. Discussing the need for African American-owned asset management firms managing hundreds of billions in capital is abstract and seemingly impossible for most people to influence. Individual success stories make compelling content. Institutional finance is complex, technical, and doesn’t generate the emotional engagement that drives social media metrics and television ratings.

Institutional finance is deliberately exclusionary, with high barriers to entry, specialized knowledge requirements, and established networks that are difficult to penetrate. This makes it harder for diverse voices to participate in and shape these conversations. Moreover, focusing on individual responsibility can deflect attention from systemic inequalities and the need for institutional reform. If wealth gaps are framed as the result of individual choices rather than institutional access, the solution becomes personal change rather than structural change.

The problem is that individual wealth building, while important, simply cannot close the wealth gap or address the capital hemorrhage happening through institutional absence. You cannot budget your way to institutional power. You cannot side-hustle your way to sovereign wealth fund influence. Closing the institutional gap would require coordinated action across multiple domains. This means growing and creating Black-owned banks, credit unions, insurance companies, asset management firms, and investment banks capable of competing at scale—institutions managing not millions but billions and eventually trillions in assets.

It requires ensuring that the substantial capital in public pension funds, university endowments, and foundation assets that serve African American communities is managed with intentionality about wealth creation within those communities. Building investment funds that can provide growth capital to Black-owned businesses beyond the startup phase, enabling them to scale to institutional size, becomes essential. Creating institutions that can acquire, develop, and manage commercial and residential real estate at scale, capturing appreciation and rental income for community benefit, must be prioritized. Developing institutional voices that can effectively advocate for policies that support Black wealth building, from community reinvestment requirements to procurement set-asides to tax structures that favor long-term capital formation, is critical.

This isn’t a call to abandon individual financial responsibility or entrepreneurship both remain important. Rather, it’s a recognition that these individual efforts need institutional infrastructure to support them, multiply their effects, and prevent the constant capital drain that currently undermines them. The Bloomberg conference model reveals what serious wealth building conversations look like among communities that already possess institutional power. The participants aren’t there to learn how to balance their personal checking accounts they’re there to discuss macroeconomic trends, regulatory changes, emerging markets, and trillion-dollar capital allocation decisions.

African American communities need forums that operate at the same level of institutional sophistication. This means convening the leaders of Black-owned financial institutions, pension fund managers, university endowment chiefs, foundation presidents, private equity partners, and policymakers to discuss not individual wealth tips but institutional strategy. It means asking questions like: How do we coordinate capital deployment across Black-owned financial institutions to maximize community impact? How do we leverage public pension fund capital to support Black wealth building without sacrificing returns? What regulatory changes would most effectively support Black institutional development? How do we build the pipeline of talent needed to manage billions in institutional capital?

The real challenge can be distilled into three interconnected imperatives: individually Black people must get wealthier, there must be an increase in Black institutional investing, and the overall wealth of Black people as a whole must increase. All three are important, yet the current discourse focuses almost exclusively on the first element while neglecting the second and third. The reality is that without institutional infrastructure, individual wealth gains will continue to leak out of the community rather than accumulating into collective wealth.

A fundamental truth that much of African American wealth discourse has yet to fully internalize is that wealth is created through institutions. There exists a critical misalignment between how wealth is actually built and how we talk about building it. We prioritize individual wealth accumulation without recognizing that the causality runs in the opposite direction—institutional infrastructure creates the conditions for sustainable individual and collective wealth building, not the other way around. We can celebrate individual achievement, teach financial literacy, promote entrepreneurship, and encourage personal responsibility all we want. But until African American communities build and control institutions that can pool capital, shape markets, influence policy, and deploy resources strategically across generations, the wealth gap will persist and likely widen.

A docuseries about successful individuals may be inspiring. But inspiration without infrastructure leads nowhere. Other communities learned this lesson generations ago (from us) and built accordingly. A critical question cuts to the heart of the matter: Who in these wealth-building conversations is representing an African American institution? When wealth dialogues feature only individuals representing themselves or individual brands rather than institutions representing collective capital and community interests, we’re having the wrong conversation at the wrong altitude.

It’s time for African American wealth conversations to graduate from the individual focus to the institutional imperative. The Bloomberg model isn’t just for other people it’s a template for how serious wealth building actually works. The question isn’t whether African Americans can produce individually wealthy people we’ve proven that repeatedly. The question is whether we can build the institutional infrastructure that turns individual success into collective, multigenerational wealth. That’s the conversation we should be having, and it needs to happen at the same level of sophistication and institutional focus that other communities take for granted. Until then, we’re simply rearranging deck chairs while hundreds of billions if not trillions flow out of our communities annually, enriching institutions that have no stake in our collective prosperity.

Disclaimer: This article was assisted by ClaudeAI.

African American household wealth reached $5.6 trillion in 2024, marking a half-trillion-dollar increase that signals both progress and persistent structural challenges in the nation’s racial wealth landscape. While the topline growth appears encouraging, the composition reveals a familiar pattern: wealth remains overwhelmingly concentrated in illiquid assets, with real estate and retirement accounts comprising nearly 60% of total holdings. The year’s most dynamic growth came from corporate equities and mutual fund shares, which surged 22.2% to $330 billion—yet this represents less than 5% of African American assets and a mere 0.7% of total U.S. household equity holdings, underscoring how far removed Black households remain from the wealth-generating mechanisms of capital markets.

The liability side of the ledger tells an equally sobering story. Consumer credit climbed to $740 billion in 2024, now representing nearly half of all African American household debt and growing at more than double the rate of asset appreciation. This shift toward unsecured, high-interest borrowing—particularly as it outpaces home mortgage debt—suggests that rising asset values are not translating into improved financial flexibility or reduced economic vulnerability. What makes this dynamic even more troubling is the extractive nature of the debt itself: with African American-owned banks holding just $6.4 billion in combined assets, it’s clear that the vast majority of the $1.55 trillion in African American household liabilities flows to institutions outside the community. This means that interest payments, fees, and the wealth-building potential of lending relationships are being systematically siphoned away from Black-owned financial institutions that could reinvest those resources back into African American communities, perpetuating a cycle where debt burdens intensify even as the capital generated from servicing that debt enriches institutions with no vested interest in Black wealth creation.

ASSETS

In 2024, African American households held approximately $7.1 trillion in total assets, an increase of more than $500 billion from 2023, with corporate equities and mutual fund shares recording the fastest year-over-year growth from a relatively small base, even as wealth remained heavily concentrated in real estate and retirement accounts—together accounting for more than 58% of total assets.

Real Estate

Total Value: $2.24 trillion

Definition: Real estate is defined as the land and any permanent structures, like a home, or improvements attached to the land, whether natural or man-made.

% of African America’s Assets: 34.2%

% of U.S. Household Real Estate Assets: 5.1%

Change from 2023: +4.3% ($100 billion)

Real estate remains the dominant asset class for African American households, accounting for over one-third of total household assets. While modest appreciation continued in 2024, ownership remains highly concentrated in primary residences rather than income-producing or institutional real estate, limiting liquidity and leverage potential.

Consumer Durable Goods

Total Value: $620 billion

Definition: Consumer durables, also known as durable goods, are a category of consumer goods that do not wear out quickly and therefore do not have to be purchased frequently. They are part of core retail sales data and are considered durable because they last for at least three years, as the U.S. Department of Commerce defines. Examples include large and small appliances, consumer electronics, furniture, and furnishings.

% of African America’s Assets: 8.8%

% of U.S. Household Durable Good Assets: 6.2%

Change from 2023: +3.3% ($20 billion)

Corporate equities and mutual fund shares

Total Value: $330 billion

Definition: A stock, also known as equity, is a security that represents the ownership of a fraction of the issuing corporation. Units of stock are called “shares” which entitles the owner to a proportion of the corporation’s assets and profits equal to how much stock they own. A mutual fund is a pooled collection of assets that invests in stocks, bonds, and other securities.

% of African America’s Assets: 4.7%

% of U.S. Household Equity Assets: 0.7%

Change from 2023: +22.2% ($60 billion)

Defined benefit pension entitlements

Total Value: $1.73 trillion

Definition: Defined-benefit plans provide eligible employees with guaranteed income for life when they retire. Employers guarantee a specific retirement benefit amount for each participant based on factors such as the employee’s salary and years of service.

% of African America’s Assets: 24.4%

% of U.S. Household Defined Benefit Pension Assets: 9.7%

Change from 2023: +7.5% ($40 billion)

Defined contribution pension entitlements

Total Value: $880 billion

Definition: Defined-contribution plans are funded primarily by the employee. The most common type of defined-contribution plan is a 401(k). Participants can elect to defer a portion of their gross salary via a pre-tax payroll deduction. The company may match the contribution if it chooses, up to a limit it sets.

% of African America’s Assets: 12.4%

% of U.S. Household Defined Contribution Pension Assets: 6.0%

Change from 2023: +4.8% ($40 billion)

Private businesses

Total Value: $330 billion

% of African America’s Assets: 4.7%

% of U.S. Household Private Business Assets: 1.8%

Change from 2023: +3.1% ($10 billion)

Other assets

Total Value: $770 billion

Definition: Alternative investments can include private equity or venture capital, hedge funds, managed futures, art and antiques, commodities, and derivatives contracts.

% of African America’s Assets: 10.9%

% of U.S. Household Other Assets: 2.7%

Change from 2023: +6.9% ($50 billion)

LIABILITIES

“From 2023 to 2024, African American household liabilities rose by approximately $100 billion, with consumer credit, now representing nearly 48% of all liabilities, driving the majority of the increase and reinforcing structural constraints on net wealth accumulation despite rising asset values.”

Home Mortgages

Total Value: $780 billion

Definition: Debt secured by either a mortgage or deed of trust on real property, such as a house and land. Foreclosure and sale of the property is a remedy available to the lender. Mortgage debt is a debt that was voluntarily incurred by the owner of the property, either for purchase of the property or at a later point, such as with a home equity line of credit.

% of African America’s Liabilities: 50.3%

% of U.S. Household Mortgage Debt: 5.8%

Change from 2023: +4.0% ($30 billion)

Consumer Credit

Total Value: $740 billion

Definition: Consumer credit, or consumer debt, is personal debt taken on to purchase goods and services. Although any type of personal loan could be labeled consumer credit, the term is more often used to describe unsecured debt of smaller amounts. A credit card is one type of consumer credit in finance, but a mortgage is not considered consumer credit because it is backed with the property as collateral.

% of African American Liabilities: 47.7%

% of U.S. Household Consumer Credit: ~15.0%

Change from 2023: +10.4% ($70 billion)

Other Liabilities

Total Value: $30 billion

Definition: For most households, liabilities will include taxes due, bills that must be paid, rent or mortgage payments, loan interest and principal due, and so on. If you are pre-paid for performing work or a service, the work owed may also be construed as a liability.

“Let us put our moneys together; let us use our moneys; let us put our moneys out at usury among ourselves, and reap the benefits ourselves.” – Maggie L. Walker, pioneering African American banker and businesswoman:

It is not enough to cheer from the stands. IIt is not enough to cheer from the stands. If HBCU women entrepreneurs and the institutions that produced them are serious about building generational wealth, influence, and visibility in the global sports economy, then ownership, not participation, must be the goal. The emergence of the Women’s Pro Baseball League (WPBL) offers just such a moment. Four inaugural franchises in Los Angeles, San Francisco, New York, and Boston mark the first professional women’s baseball league in the United States since 1954. And yet, amid this historic announcement, one question should echo across the HBCU landscape: Who will own a piece of it?

Ownership in sports is about more than trophies it’s about capital, culture, and control. While athletes inspire, it is owners who shape the economic ecosystem: negotiating television contracts, setting standards for pay equity, deciding where teams are located, and determining which communities benefit from their presence. In American sports, Black ownership remains vanishingly rare. Fewer than a handful of African Americans have ever held majority stakes in professional teams across all major leagues. Among women, ownership representation is even smaller. Yet the HBCU ecosystem comprising over a hundred institutions, $4 billion in endowment capital (though still dwarfed by their PWI counterparts), and a growing class of wealthy and capable alumni possesses both the human and institutional capital to change that reality. Buying a WPBL franchise would be a powerful signal: that African American women are no longer content to merely play or support the game, but to own the infrastructure of it.

The WPBL represents a once-in-a-century opportunity. The last women’s professional baseball league folded in 1954 when postwar America reverted to its gendered labor norms and refused to institutionalize women’s success on the field. Today, that same sport returns in a vastly different economy one defined by media fragmentation, digital storytelling, and institutional investing that rewards niche audiences and strong narratives. Women’s sports are on the rise. The WNBA just received a $75 million investment round from Nike, Condoleezza Rice, Laurene Powell Jobs, and others. Women’s college basketball ratings have exploded, drawing more viewers than some men’s sports. The National Women’s Soccer League has seen team valuations grow fivefold in the past five years. Investors are realizing what the data already shows: undervalued leagues often yield outsized returns once visibility and infrastructure catch up.

The WPBL sits at this exact inflection point. Early investors will not just shape the league they will define its culture, inclusivity, and profitability. This is why HBCU women entrepreneurs, backed by HBCU endowments and alumni capital, should move swiftly. Ownership here is not a vanity project it is a long-term equity position in the fastest-growing frontier of professional sports.

Start-up sports franchises are not the billion-dollar investments of the NFL or NBA. The WPBL’s initial teams are expected to sell for figures in the mid-seven to low-eight figures: expensive, yes, but feasible through a syndicate model combining entrepreneurial capital and institutional backing. A $15 million franchise, for instance, could be financed with $5 million in equity from HBCU women entrepreneurs, $3 million in matching commitments from HBCU endowments through a joint-venture investment arm, $5 million in debt financing via an African American–owned bank or credit union consortium, and $2 million in naming rights, sponsorship pre-sales, and city incentives.

Such a structure distributes risk while maximizing institutional leverage. It also allows for a reinvestment loop: returns from franchise appreciation, media deals, or merchandising could feed back into the endowments that helped fund the acquisition, growing HBCU wealth through private equity in sports. At a modest ten percent annualized return over fifteen years, a $3 million endowment investment could grow to more than $12.5 million, even before accounting for franchise appreciation. The social return of visibility, leadership, and influence would be immeasurable.

HBCU women entrepreneurs already lead some of the most innovative ventures in the country from fintech to fashion to wellness. They have built companies with leaner budgets, higher risk tolerance, and community-driven missions. That same acumen could translate seamlessly into sports ownership. A women-led ownership group rooted in HBCU culture would bring authenticity to a league whose audience is already primed for inclusive storytelling. They would not merely own a team they would shape its identity around empowerment, intellect, and cultural sophistication. Imagine a team whose executive suite reflects Spelman’s academic rigor, Howard’s creative dynamism, and FAMU’s entrepreneurial grit.

Moreover, the investment aligns with HBCU women’s long history of institution building. From Mary McLeod Bethune’s founding of Bethune-Cookman University to Maggie Lena Walker’s creation of the first Black woman–owned bank, African American women have always been at the forefront of merging mission with market. Buying a professional sports franchise is simply a modern continuation of that legacy.

Most HBCU endowments remain undercapitalized. Collectively, they total roughly $4 billion, compared to Harvard’s $50 billion alone. That gap underscores why traditional endowment investing centered on conservative asset classes may not close the wealth chasm. Sports equity, particularly in emerging women’s leagues, represents a hybrid investment: cultural capital meets growth asset. Endowments could carve out a modest allocation for strategic co-investment vehicles aimed at ownership in minority- or women-led sports ventures. Such a move would not only produce potential returns but reposition HBCU endowments as active agents in wealth creation, mirroring how elite universities use their endowments as venture capital arms. The same institutions that once nurtured the first generations of African American scholars could now nurture the first generation of African American women sports owners.

The path to ownership would unfold in phases: coalition building, institutional partnerships, financial structuring, branding, and media engagement. The first step would be forming an HBCU Women Sports Ownership Council an alliance of HBCU alumnae entrepreneurs, investors, attorneys, and sports professionals. Its mission would be to identify a WPBL franchise opportunity, conduct due diligence, and negotiate terms. Next, endowments, foundations, and alumni associations could serve as anchor investors via a pooled HBCU Sports Ownership Fund. African American–owned financial institutions would provide credit facilities, ensuring that capital circulation strengthens Black banking. The team’s branding could reflect HBCU values of intellect, resilience, and excellence. Annual “HBCU Heritage Games,” scholarships for women in sports management, and partnerships with K–12 baseball programs would ensure the franchise deepens institutional impact.

By the time Opening Day 2027 arrives, the vision becomes real. A stadium in Atlanta or Houston cities with deep HBCU roots roars with excitement. The team, perhaps named The Monarchs in tribute to the Negro Leagues, takes the field in uniforms stitched by a Black-owned apparel company. The owner’s suite is filled not with venture capitalists, but HBCU women—founders, engineers, bankers, educators—raising glasses to history. Every ticket sold funds scholarships. Every broadcast includes HBCU branding. Every victory multiplies across the ecosystem, from the university’s endowment statement to the little girl in the stands whispering, “She looks like me.” That is the multiplier effect of ownership.

A defining mark of this ownership group’s legacy should not only be who owns the team but who benefits from it. When an HBCU-led syndicate buys a women’s professional baseball team, it must ensure that every dollar of the fan experience circulates through Black and HBCU-centered businesses. Ownership without ecosystem-building simply recreates dependency; real power multiplies through participation.

An HBCU women’s ownership group has the chance to build an authentically circular sports economy, where concession stands, catering services, and retail vendors reflect the same entrepreneurial DNA as the team itself. The model for this begins with women like Pinky Cole, founder of Slutty Vegan, who transformed plant-based dining into a cultural and economic phenomenon through purpose-driven branding and community investment. Her ability to merge food, culture, and empowerment offers a blueprint for how HBCU women entrepreneurs could anchor the ballpark experience in ownership and identity.

Complementing this vision is the role of HBCU-owned service enterprises like Perkins Management Services Company, founded by Nicholas Perkins, a Fayetteville State University alumnus and owner of Fuddruckers. Perkins Management operates food services across HBCUs and federal institutions, combining operational scale with cultural competence. Partnering with Perkins Management to run stadium concessions or hospitality would ensure that the team’s operations mirror the ownership group’s values efficiency, reinvestment, and excellence.

Such an approach would transform the stadium into an economic hub for HBCU enterprise. Food vendors would come from HBCU alumni-owned companies. Uniform suppliers could source from HBCU textile programs. Merchandise stands could feature HBCU student designs. Hospitality contracts would prioritize HBCU-affiliated culinary programs. The music during games could feature HBCU marching bands or alumni artists. Even the stadium’s artwork could highlight HBCU painters and photographers, ensuring every sensory detail honors the ecosystem that made the ownership possible. A fan buying food or merchandise would not just be a consumer they’d be participating in a shared mission to strengthen African American institutions.

This reimagined sports environment would also offer internships, apprenticeships, and consulting opportunities for HBCU students and faculty. Business students could study operations. Communication majors could intern with the PR team. Engineering departments could advise on stadium energy efficiency. Each partnership would turn the franchise into a living classroom of applied HBCU excellence.

At a time when major leagues outsource globally, a women’s baseball franchise owned by HBCU women could reimagine localization and reinvestment as competitive advantage. Every game day would circulate dollars through a self-sustaining ecosystem that feeds back into HBCU entrepreneurship. Because when the ballpark itself is powered by HBCU women’s enterprise from boardroom to concession stand it ceases to be a venue. It becomes a living institution.

If the Women’s Pro Baseball League truly takes off, early ownership will be the golden ticket. African American investors have often entered markets too late once valuations skyrocket and access narrows. Now, before the WPBL matures, is the time for HBCU institutions and their entrepreneurial alumnae to act collectively. The call is not for charity but for strategy. Pooling even a fraction of the capital that circulates annually among HBCU alumni could change the power dynamic in sports forever. Endowments could stake equity. Alumni could invest through private funds. Students could study the economics of their own institution’s franchise. The result would be a feedback loop of wealth, wisdom, and visibility.

The first women’s professional baseball league in seventy years deserves first-of-its-kind ownership and no community is more qualified to deliver it than HBCU women. Because when HBCU women own the field, the entire game changes.

“I know I got it made while the masses of black people are catchin’ hell, but as long as they ain’t free, I ain’t free.” – Muhammad Ali

The recent news that Intel will discontinue its $1 million annual funding of North Carolina Central University’s (NCCU) Technology Law and Policy Center is more than just a line item in the university’s budget. It is a sharp reminder of how precarious institutional development becomes when African American colleges and universities rely on the European American corporate cycle of generosity and withdrawal. Where is African American corporate philanthropy is a pertinent question, but an article for another day.

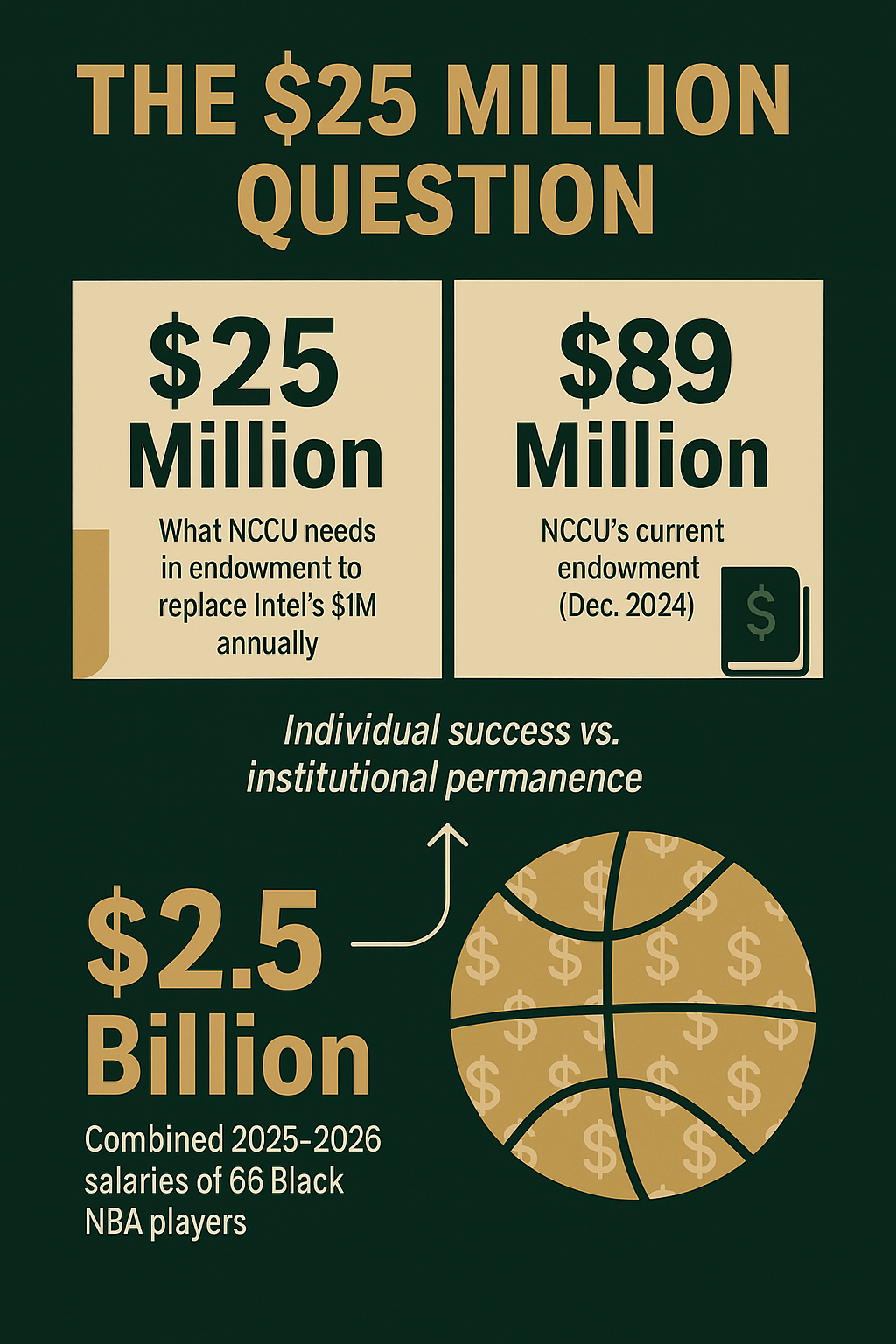

Intel’s departure leaves a gap that must now be filled through other means. But the mathematics of filling it points to a broader truth: without substantial, permanent endowments, HBCUs will remain vulnerable to the political and financial whims of European American corporations. To replace $1 million in annual program funding, NCCU would need to raise between $20 million and $25 million in endowment principal assuming a 4–5% annual spending rate, the standard in higher education finance.

The fact that an entire academic pipeline, designed to produce future African American lawyers and policymakers, can be destabilized by a single corporate decision underscores the fragility of HBCU institutional power. And it raises a haunting contrast: while 66 African American NBA players will together earn $2.5 billion in salaries this upcoming season, not a single African American university controls an endowment robust enough to insulate it from the kind of disruption Intel’s withdrawal has now caused.

The mechanics are straightforward. Endowments work by pooling donated capital, investing it, and spending a sustainable portion of annual returns—usually 4–5%. To replace Intel’s $1 million annual gift, NCCU must therefore build an endowment of $20–25 million. This is not extraordinary by university standards. At most predominantly white institutions (PWIs), a $25 million endowment is considered modest. At Harvard, Yale, or Stanford, it would not even make the footnotes. Yet for NCCU, an institution with an endowment of $89 million as of December 2024, the sudden need for another $20–25 million underscores the gap between HBCUs and their white peers.

The underlying truth is that corporate funding is inherently unstable. It ebbs and flows with market cycles, political administrations, and corporate priorities. Endowments, however, endure across generations. The very act of raising such capital is itself an exercise in institutional power: it demonstrates to the world that the university and its community can stand on their own financial feet.

Intel did not single out NCCU maliciously. The company is undergoing a profound transformation, not least because the U.S. government has become its largest shareholder after a multi-billion-dollar deal with the Trump administration. Like other firms facing political scrutiny, Intel is quietly shedding high-profile DEI commitments. For NCCU, however, the effect is real. The Technology Law and Policy Center was designed to provide African American law students with training in emerging technology and policy—a space historically closed to Black lawyers. It also featured internships at Intel, summer placements, and the now-defunct “Intel Rule,” which required outside law firms to staff diverse teams if they wanted Intel’s business. Now, without a replacement funding mechanism, the Center risks contraction. Students will still enroll. Faculty will still teach. But the acceleration that Intel’s money provided—the ability to recruit nationally, to build cutting-edge programming, to give students exposure to high-tech legal practice—will slow.

Enter the paradox of the NBA’s 66 Black players earning $25 million or more in the upcoming season. Collectively, those 66 players will earn $2.5 billion in salary during the 2025–2026 season. Each of these players individually makes at least what NCCU would need to permanently replace Intel’s $1 million annual commitment through endowment. The collective sum is staggering: $2.5 billion in one season—enough to seed $25 million endowments at 100 HBCUs.

It is not about individual responsibility. No one player can be expected to save an institution. But collectively, the paradox points to the imbalance between African American individual wealth and African American institutional poverty. Even if just 10% of that wealth—$250 million—were organized and directed into HBCU endowments, the result could replace Intel’s contribution not only at NCCU but across multiple campuses. Yet there is no mechanism, no institutional strategy, no coordinated pipeline that directs such flows into African American universities. This is not new. For decades, African American excellence has been harvested at the level of the individual, while African American institutions have remained underfunded. The NBA is simply the latest, most visible example.

The Intel withdrawal reminds us of a hard truth: reliance on outside benevolence is not a strategy for power. It is, at best, a strategy for survival. Corporate giving is always the first budget item to shrink when recession looms or political winds shift. For HBCUs, this means programs rise and fall on decisions made in Silicon Valley or Wall Street boardrooms—far removed from Durham, Tallahassee, Baton Rouge, or Montgomery. The vulnerability is compounded when African American communities assume that the generosity of corporations will substitute for building our own endowments. The danger is not simply financial but cultural: it conditions us to believe that power comes from outside, not from within.

Intel’s $1 million a year was not charity—it was investment. It bought Intel goodwill, a trained pipeline of diverse lawyers, and reputational capital in the DEI era. Now that DEI is politically unpopular, the investment is deemed expendable. This is why endowments matter. They are not subject to the quarterly report or the election cycle. They anchor institutions in the long term.

Let’s be clear about the scale of the challenge. The combined endowments of all HBCUs hover around $4 billion, compared to more than $800 billion at PWIs. Harvard alone has an endowment of nearly $52 billion. NCCU’s endowment stands at $89 million. To raise an additional $20–25 million to replace Intel’s support would represent a 22–28% increase in its current endowment base. Such a leap is achievable—but it requires strategy. It means cultivating alumni giving systematically. It means leveraging African American wealth beyond alumni, drawing in professional athletes, entertainers, and entrepreneurs. It means creating vehicles—donor-advised funds, pooled endowments, institutional investment cooperatives—that make giving both efficient and impactful. Most of all, it means shifting mindset. We must stop thinking of endowments as luxuries reserved for Ivy League institutions. They are necessities. They are the only way to secure institutional independence.

The Intel decision can serve as a turning point, if we are willing to see it clearly. Corporations are not institutional guardians. They may play a role, but they will not underwrite our survival. Their goals are their own. When interests diverge, as they now have, funding vanishes. Individual wealth must be institutionalized. The contrast between NBA salaries and HBCU endowment poverty is not about shaming athletes. It is about building structures that make institutional giving the default, not the exception. Endowments are the only safety net. No government program, no corporate sponsorship, no philanthropic fad can substitute. Only endowments give institutions perpetual capacity to fund themselves.

What would it take, concretely, for NCCU to raise the $25 million needed? A handful of major gifts in the $2–5 million range from alumni, athletes, or African American business leaders could jump-start the campaign. NBA, NFL, and WNBA players could be recruited to create a pooled fund. Instead of individual gifts, imagine a collective “Athletes for HBCU Endowments” initiative. African American foundations and community funds could direct grants toward seed capital, matched by alumni. If every NCCU law graduate gave $1,000 a year for ten years, the cumulative effect would approach the tens of millions. NCCU could also partner with African American-owned banks and investment firms to maximize returns and circulate dollars within the community. The strategy would not only replace Intel but set a precedent: when outside money leaves, we do not shrink. We build.

The broader question is not whether NCCU will survive the loss of Intel’s support. It will. The real question is whether African American institutions will continue to live in the shadow of dependency—or whether we will use moments like this to chart a new course. The paradox of $2.5 billion in NBA salaries versus the need for a $25 million endowment is not just a rhetorical flourish. It is a mirror held up to African America. It asks whether we will continue to celebrate individual wealth while neglecting collective survival.

Every dollar of Intel’s withdrawal can be replaced. But only if African American wealth is organized. Only if alumni, athletes, and entrepreneurs see endowments not as gifts but as obligations. Only if we remember that the true measure of power is not what any one of us earns, but what we can build together.

Intel has reminded us of an uncomfortable truth: corporate giving is temporary. Endowments are permanent. To replace $1 million a year, NCCU needs $25 million in endowment. That number is not insurmountable. It is the equivalent of one NBA salary in a single season. There are 66 African American players earning at least that much this year alone, with combined salaries of $2.5 billion. The juxtaposition is stark: individuals flourish while institutions starve. The future of HBCUs—and the broader African American ecosystem—depends on closing that gap. Until African America learns to institutionalize its wealth, every Intel withdrawal will feel like a crisis. But the day we build our endowments, such exits will be footnotes. And our institutions will finally stand on the firm ground they have always deserved.