Where you live should not determine whether you live. — Dr. Martin Luther King Jr.

There is a kind of emergency that does not announce itself with sirens. It settles instead into the permanent infrastructure of a city into shelter intake forms, into eviction court dockets, into the quiet calculus of a family deciding which bill goes unpaid this month so the rent does not. It becomes, over time, not an emergency at all but a condition: expected, budgeted for, managed at the margins, never resolved. Black homelessness in America has become that kind of emergency. It is measured every January, reported every summer, and addressed with the institutional energy of a problem that everyone has agreed, without saying so directly, will not be solved.

On a single night in January 2024, the federally mandated Point-in-Time census counted more than 240,000 people experiencing homelessness who identified as Black, African American, or African. That figure represented 31.6 percent of everyone sleeping in shelters, tents, cars, or on city streets in a country where Black Americans represent 13.7 percent of the population. The disproportionality is not new. What is new is the magnitude: 2024 produced the largest raw count of unhoused Black Americans ever recorded in the Department of Housing and Urban Development’s modern Point-in-Time series. The trend line does not suggest an aberration. It suggests a permanent condition whose scale is still expanding.

The arithmetic of the crisis is straightforward. Zillow’s national rental index placed the average advertised lease at approximately $2,100 per month in early 2025. A parallel Apartment List survey, which strips luxury units from its methodology, pegged the median at $1,398. A reasonable blended figure sits near $1,700 per month or $20,400 per year. That is not the price of comfort. It is the price of a mailing address, a bathroom that locks, and a bed that belongs to no one else. Multiply that annual cost by 240,000 unhoused Black individuals and the minimum annual bill for basic housing stability comes to $4.9 billion. Finance professionals design endowments to distribute approximately 5 percent of principal annually without eroding real value. The corpus required to generate $4.9 billion in perpetuity is approximately $98 billion, call it $100 billion. That is the number. It is not an estimate or an aspiration. It is arithmetic.

To understand why that number has never been assembled, it is necessary to understand what produced the crisis it would address. The Census Bureau defines households paying more than 30 percent of income toward housing as cost-burdened. In 2023, 56.2 percent of Black renter households met that definition. The Federal Reserve’s 2022 Survey of Consumer Finances reported median Black household wealth at $44,900, roughly 15 percent of the $285,000 median for white households. The Black homeownership rate sits between 44 and 45 percent, compared to 74 percent for non-Hispanic white households. Home equity is the primary mechanism by which American families absorb life shocks — job loss, illness, family dissolution — without falling into housing instability. A community with a homeownership rate 30 points below the national white average has 30 points less cushion against every emergency that precedes homelessness. This is not a coincidence of individual financial behavior. It is the compounded output of subsidized mortgage programs that excluded Black borrowers, exclusionary zoning that confined Black families to undervalued land, and GI Bill benefits that built the white middle class while systematically denying equivalent access to Black veterans. The policy record is not ambiguous. The consequences are still being counted every January.

The community’s own financial institutions offer the starkest measure of the structural gap. According to HBCU Money’s 2024 African American Owned Bank Directory, African American-owned banks hold $6.4 billion in total assets across 18 institutions. The 2025 African American Owned Credit Union Directory documents 205 active credit unions holding $8.15 billion in assets serving 726,929 members. The entire African American-owned financial institution sector between every bank, every credit union in the country, combined controls approximately $14.5 billion. The endowment required to permanently resolve Black homelessness is seven times that figure. African American households hold $7.1 trillion in total assets according to HBCU Money’s 2024 Annual Wealth Report, and command approximately $1.8 trillion in annual buying power, yet corporate equities and mutual fund shares, the asset class that most reliably converts income into intergenerational capital, represent less than 5 percent of African American holdings and a mere 0.7 percent of total U.S. household equity assets. Consumer credit has climbed to $740 billion, now approaching parity with Black mortgage debt of $780 billion, a near 1:1 ratio that represents a fundamental inversion of healthy household finance (3:1 being seen as the baseline for a health household finance). The topline wealth figures are real. The structural vulnerabilities beneath them are equally real. A community whose financial institutions control $14.5 billion in assets is not positioned to self-capitalize a $100 billion endowment, not now, and not without a generational shift in how African American institutional capital is accumulated, retained, and deployed.

HBCU campuses are not observers of this crisis. They are inside it. A 2020 Hope Center survey of nearly 5,000 students at 14 HBCUs found that 46 percent had experienced food insecurity in the prior 30 days, 55 percent had experienced housing insecurity in the prior year, and 20 percent had been homeless at some point during that academic year. One in five students at institutions whose entire institutional mission is economic mobility trying to complete coursework from a couch, a car, or a shelter. The 2021 Howard University student occupation of the Blackburn Center brought national visibility to conditions that students at dozens of HBCUs navigate without cameras: mold, rodent infestation, deferred maintenance that years of constrained operating budgets cannot absorb. At institutions like Alcorn State University, Coppin State University, and Edward Waters University, the competition between student housing needs and every other institutional priority is not a policy question. It is a weekly budget decision. An HBCU cannot produce the physicians, engineers, and policy architects that African American communities require if the students admitted to those programs cannot secure the stability that sustained academic work demands.

The conventional philanthropic response to a crisis of this scale would invoke a combination of federal investment, corporate giving, and foundation capital. That architecture has not assembled for Black housing, and the current environment offers no evidence that it will. Federal housing policy has moved in the opposite direction from what the scale of Black housing instability requires. Corporate philanthropy directed toward racial equity initiatives contracted sharply following 2023, as major corporations withdrew or quietly defunded commitments made in 2020. Foundation capital, while more durable, has never operated at the scale this problem requires and has shown no institutional appetite to do so. The community has waited across multiple political cycles for external capital to arrive at the necessary scale. It has not arrived. There is no credible reason, given the current political and philanthropic environment, to expect that it will.

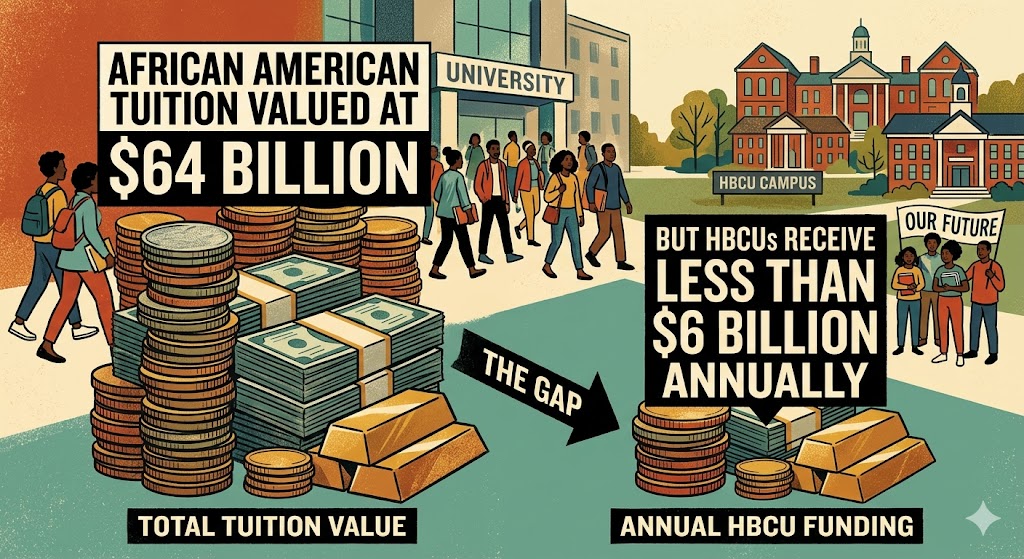

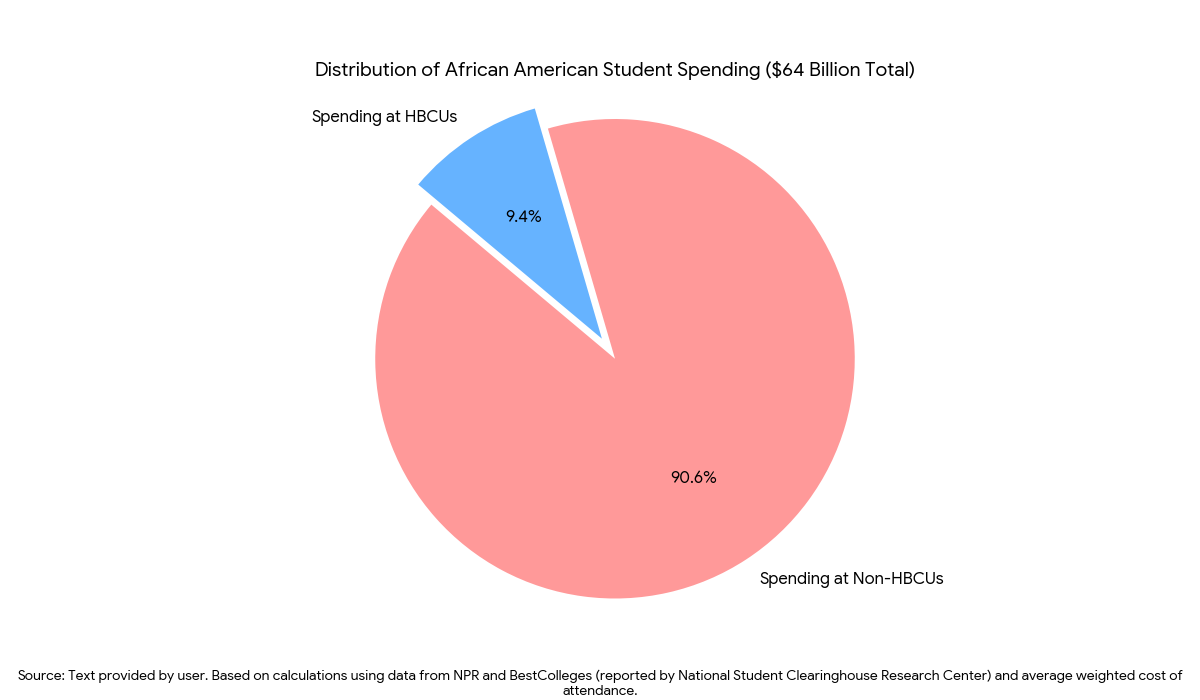

What remains, then, is the harder question, the one that the data forces and that no external institution is positioned to answer. African American households hold $7.1 trillion in assets. African American consumers generate $1.8 trillion in annual spending, $64 billion of which flows into higher education, much of it leaving the Black institutional ecosystem entirely. The financial infrastructure of 205 credit unions and 18 banks exists, undercapitalized but functional, as a potential deployment mechanism for any capital that could be directed toward it. The institutional networks of HBCUs, Black nonprofits, and community land trusts represent governance capacity that has been demonstrated across generations. None of this adds up, in its current configuration, to $100 billion. But it raises the question that Black institutional leadership has not yet had to answer at this scale: what would it take to get there from within, and what is the cost, measured in bodies counted each January, of not trying.

That question does not have a comfortable answer. The honest answer may be that the problem is larger than what any single generation of institutional actors can resolve, that the structural deficit created by four centuries of policy violence cannot be closed by the institutions those policies were designed to prevent from forming. That possibility deserves to be named plainly rather than papered over with funding architectures that do not exist. What can be said with equal plainness is this: the external path has been tried across multiple administrations, multiple philanthropic cycles, and multiple corporate giving moments. The count goes up every January. Whatever the solution is, if one exists at this scale, it will have to be generated from within the African American community and our institutions whose members are being counted. There is no other honest conclusion available from the data.

The Sliding Scale: 10 Infrastructure Categories

1. African American Emergency Shelter Networks

The Salvation Army, Catholic Charities, and Gospel Mission dominate this space almost entirely. There is no Black-led national shelter network equivalent. Individual Black churches operate shelter programs locally but with no coordination, no shared data, and no pooled capital. This is the most visible absence and arguably the easiest to begin at city level — a single congregation with property can open beds. The barrier is operating capital, not concept.

2. African American Eviction Prevention Funds

Eviction is the primary on-ramp to homelessness for Black renters who are not chronically unhoused. Right-to-counsel programs — where they exist — reduce eviction rates 50–80 percent. African American-owned credit unions are the logical vehicle for rapid emergency rental assistance lending because they already have underwriting relationships in these communities. This is financial infrastructure, not charity: a revolving loan fund capitalized through credit unions and HBCU alumni networks could catch families before they hit shelters.

3. African American Tenant Legal Defense Organizations

The eviction court system is structurally adversarial. Landlords routinely appear with counsel; tenants routinely appear alone. Black bar associations in major cities — the Cook County Bar Association, the Wiley Branton Inn of Court in D.C., the Charles Houston Bar Association — have the professional infrastructure to organize pro bono tenant defense clinics. What they lack is a coordinated national framework and stable funding to make this a standing operation rather than an episodic volunteer effort.

4. African American Community Land Trusts

This is the one category with genuine Black institutional roots. The community land trust model traces directly to the Civil Rights Movement — New Communities Inc., founded in 1969 in Albany, Georgia, is credited as the original CLT model in the U.S., created specifically to prevent displacement of Black communities through community-owned land. The Africatown Community Land Trust in Seattle has established mixed-use spaces supporting Black-owned businesses and over 100 affordable rental units. The Crescent City Community Land Trust in New Orleans has focused on racial equity, permanently affordable housing, and restoring Black businesses in the Seventh Ward. The model works. It is undercapitalized and geographically fragmented. A national network of Black-led CLTs with pooled acquisition capital would be the most durable long-term housing infrastructure available.

5. African American-Owned Property Management Companies

This is an underexamined gap. Affordable housing units exist in Black communities. Who manages them determines where operating revenues go — and currently, most flows to firms with no institutional relationship to those communities. Black-owned property management companies operating within affordable housing portfolios would retain fees inside the ecosystem while also setting service standards in buildings that disproportionately house Black tenants.

6. African American Transitional Housing Organizations

Between emergency shelter and permanent housing is a gap that kills stability: transitional housing with wrap-around services for 6–24 months. This is where formerly incarcerated individuals, domestic violence survivors, and people exiting addiction treatment fall through. Black churches collectively hold the physical assets — underutilized buildings, parking lots, adjacent parcels — to host transitional housing at scale. The barrier is the operational and clinical infrastructure to run such programs, which requires coordination beyond what individual congregations can typically sustain.

7. HBCU Student Emergency Housing Funds

This is the most institutionally natural starting point for the network. HBCUs already have the administrative infrastructure, the student relationships, and the moral authority. A national HBCU Student Housing Emergency Fund — capitalized through alumni associations and administered through financial aid offices — would address the 20 percent homelessness rate the Hope Center documented without requiring new institutions. It requires only that existing institutions add a function.

8. African American Credit Counseling and Housing Stability Organizations

The path back from housing instability runs through credit repair, budgeting support, and landlord negotiation — skills that cost nothing to teach but require trusted institutional relationships to deliver. African American-owned credit unions already have member financial counseling as part of their charter obligations. Expanding and formalizing that function specifically around housing stability would leverage existing infrastructure at minimal additional cost.

9. African American Mental Health and Addiction Recovery Housing

Chronic homelessness — the population that does not resolve with a voucher or a loan — is disproportionately driven by untreated mental illness and addiction. This is the hardest category and the one where the African American institutional ecosystem has the least current capacity. Black-led behavioral health organizations exist in most major cities but are chronically underfunded and have no residential housing component. Sober living homes, recovery residences, and mental health step-down housing operated by Black-led organizations would address the population that no other category reaches.

10. African American Housing Data and Advocacy Infrastructure

None of the above can be built, funded, or defended without data. The Point-in-Time count is federal data collected by local Continuums of Care that are rarely Black-led. There is currently no African American-owned institution systematically tracking Black housing instability, eviction rates, credit denial rates, and shelter utilization at national scale and publishing it as a public resource. HBCU Money’s Annual Wealth Report is the closest thing. A dedicated African American Housing Data Collaborative — potentially housed within an HBCU research center — would give every other institution on this list the evidence base to make its case.

Disclaimer: This article was assisted by Claude AI.