My experiences at Princeton have made me far more aware of my ‘blackness’ than ever before. I have found that at Princeton, no matter how liberal and open-minded some of my white professors and classmates try to be toward me, I sometimes feel like a visitor on campus; as if I really don’t belong. – Michelle Obama

A look at enrollment statistics from the National Center for Education Statistics show that currently of the HBCUs that receive federal funding (colleges such as Chicago State, Malcolm X College, and a few colleges are excluded because of the federal definition* of what an HBCU is defined as.) The problem of course with not amending that definition leaves no room for the evolution or expansion of the funding. It also continues to mean that others define us more than we define us. The acute tragedy of it means more importantly that money designated for building of African America’s higher education interest is being siphoned off by other communities. In some cases extremely so and that extreme is that on our list seven of the ten HBCUs listed have less than 50 percent of their student body being of African descent.

T1. Saint Philip’s College (TX) – 9.2%

T1. West Virginia State University (W. VA) – 9.2%

2. Bluefield State College (W. VA) – 9.5%

3. Gadsden State Community College (AL) – 17.2%

4. Shelton State Community College (AL) – 35.2%

5. Lincoln University of Missouri (MO) – 46.2%

6. University of the District of Columbia School of Law (D.C.) – 47.5%

7. Central State University (OH) – 52.7%

8. Bishop State Community College (AL) – 58.9%

9. Fayetteville State University (NC) – 59.6%

10. Edward Waters College (FL) – 61.8%

These schools are the worst of the bunch, but by no means isolated. There are a number of HBCUs where the trend line shows a decreasing population of African descent against the total population of the school and were we to increase our cutoff to 70 percent, a considerable number of additional schools would have been added. This trend is in line with the recent release from the NCES stating, “The percentage of Black students enrolled at HBCUs fell from 18 percent in 1976 to 8 percent in 2014 and then increased to 9 percent in 2020.” What does it mean for African America’s higher educational interest that HBCUs are seeing their leadership and recruitment focused on taking ethnic diversity to a potential extreme? To the point where the school’s would no longer hold or be a cultural asset to African America? These are the questions that need to be asking in urgency, because for the institutions that remaining an African American institution is important too, then strengthening their K-12 pipeline for African American high school graduates is an urgent conversation to be had. That HBCUs do not focus on an Afrocentric definition of diversity, people of African descent from different parts of the Diaspora, African Americans from different geographies, economic backgrounds, religious backgrounds, etc. would still provide diversity shows we often take our cues for higher educational direction from PWIs and not a collection of our own thoughts.

It also more importantly begs the question that if an HBCU is only Black in historic terms only, should their federal funding be redistributed to HBCUS/PBIs who are still serving the higher educational interest of African America. The HBCUs listed (excluding UDC’s law school) received $280 million of the $2.7 billion in federal funding from American Rescue Plan Investment in Historically Black Colleges and Universities most recently, but given their populations, arguably very little is going to help African American students, their families, or our communities. Is the goal for the funding to be substantive to African American higher education development or just symbolic because without absolute consideration to that point, then we are simply getting more of the latter and not the former.

“Whatever you into, your woman gotta be into, too, and vice versa… or the [thing] ain’t gonna work. lt ain’t gonna work. That’s right. lf you born-again, your woman gotta be born-again, too. lf you a crackhead, your woman gotta be a crackhead, too… or the [thing] won’t work. You can’t be like, ”l’m going to church, where you going?” ”Hit the pipe!” That relationship ain’t going nowhere, but two crackheads can stay together forever.” – Chris Rock

We all know the statistics. The number one cause of divorce is MONEY. And why it is money comes in all kinds of forms from a partner who does not help with the bills, disagreement about financial roles, spends too much, disinterested in their financial future, takes too much risk with the money they have earned (or too little), and the list goes on and on and on. For African Americans money is even more complicated when it comes to partnering. African Americans are dead last in median income, median wealth, and the only ethnic group where the women outnumber the men in employment. All of which leads to an already complicated issue of partnering with someone for the long-term even more so. Money brings about extremely strong emotions in people and African Americans are no exception. In fact, one could argue that because are financial situation is so dire that it adds even more stress and complexity than most. The majority of us are brought up with the stresses of money as the only conversations about money we have ever overheard – because we certainly were not allowed to participate in family conversations about money besides, “put that back, you know we can not afford that”. That along with a strong religious undertone of money being the root of all evil it is no wonder that the median net worth of African Americans has not moved in over four decades and is by some accounts trending downwards. So who you partner with and their attitudes towards money, as Chris Rock so eloquently put it, need to be aligned. We decided to put together four questions to help you determine whether the he, she, or they is right for you. A clarity you should try your best to establish before you even enter into a relationship.

If you had to pick a number, how much would you like to be financially worth? Do not let them be vague on this. They can not say rich, wealthy, or comfortable. There has to be a number. Rich, wealthy, or comfortable means very different things to different people. Two people can say they want to be rich, but one thinks that means being worth $5 million and the other may think that means $50 million. The further those numbers are apart or closer together will give you some valuable insight.

Why do you want to be worth that much? This is vital to give you insight on a person’s priorities. If they tell you they want to be able to buy whatever they want, acquire all the latest fashions, travel the world, they want to be able to send their children to the best schools, or they want to donate $25 million to their HBCU over their lifetime. This questions will all give you insight to their motivations and if those motivations align with yours.

Would you be willing to live with our parents, have roommates when we got married, or share a car for a few years? This is a question of sacrifice gauging a person’s sacrifice level. How badly do they want to get to that number to do that thing they said they want? The early years of financial sacrifice for a couple make all the difference in the world and while many say they want to achieve something, many are not willing to do the hard and uncomfortable things

What is your risk tolerance? Risk. Reward. They go hand in hand when it comes too investing and financial building. If one of you wants to start a business and the other just wants to save money in your savings account, then you are world’s apart when it comes to risk. There are obvious compromises to risk. Perhaps you agree to hit a certainly dollar amount in your savings account before pursuing business. Or perhaps you agree that owning a rental property portfolio is the middle ground. Whatever it is, your risk tolerance needs to be understand and agreed upon. This is particularly important because things can and often will go wrong, that is why it is called risk. When it does go wrong does it create a wedge between the two of you or does it cause you both to dig in and work together through it?

In the end, it is often hard for people to talk about money when they meet someone they like. It is even harder to realize that your financial views maybe so far apart that you simply do not make a good team and at the end of the day to be financially successful it requires teamwork. One of you can not be playing basketball and the other playing soccer. Financial goals being aligned will dictate so much of how you live your lives that to not have them aligned is a sure fire way to kill a relationship and yet many people do not think to discuss money until after they are together and sometimes not even then. They do not realize the detriment of differences until it rears its ugly head. In this new era of mental health, make sure you discuss what it will take to have financial health as well.

Owning a home is a keystone of wealth – both financial affluence and emotional security. – Suze Orman

Poor people know they are poor. Unfortunately, it is the African American working and middle class who do not know they are also poor. The problematic reality that because you can buy something does not mean you can afford it plagues much of African America’s working and middle class. These tend to be households who have higher education, higher incomes, and higher homeownership rates – but they also tend to have financial net worths that are just as poor as – well, the poor. Why? They tend to be more acutely indebted due to their education, home, car, and consumer poor, just as financially illiterate, and almost always just as asset poor as their poor counterparts in the African American community. However, any conversation about passive or investment income or financial health as a pillar in line with mental health and other priorities of a well functioning household is often met with angst or disgust. The prioritization of asset accumulation over consumption is met with more resistance than Americans against British taxation without representation – and we know how that ended. But not to worry, there seems to be no revolution brewing here (sarcasm). African American wealth accumulation continues to be an afterthought of the African American household. Upper middle class, affluent, rich, or wealthy being a thought of more as something for “others” and not ourselves. The achievement of degrees, a house, cars, and consumption is all we seem to believe life requires. Should times get tough, many within the community will tell you that a second job, a better paying job, or more education is more times than not the answer to a “better” life. Again, wealth and asset accumulation not so much.

How dire is the wealth situation for African America? Bloomberg recently reported that Black-White wealth gap has not budged in the past 40 plus years and is actually trending worse. McKinsey and Company report that nearly 20 percent of African American households have a negative net worth. The National Community Reinvestment Council’s report shows, “African Americans, who in many categories have the greatest gender economic equality, have the greatest gender wealth disparity though still having little wealth compared to Whites. Single Black men’s median wealth was $10,100, compared to Single Black women’s median wealth of $1,700.” An immense issue when one considers that the majority of African American households are headed up by single African American women. One would certainly suggest that because women are the load bearers for raising and providing for African American children and often extended family that this has also severely hampered their ability to accumulate wealth. An issue that is not as prevalent for African American men. None the less, it proves dire for the community as a whole that this is the case. Last but certainly not least (or all), there is the matter that African American homeownership has never breached above 50 percent which for the majority of families serves as the foundation that a lot of intergenerational wealth is built upon.

One of the general wedges to the wealth gap is asset ownership. Two-thirds of African American wealth according to Bloomberg is held in housing and very little in other asset classes like stocks in particular. This has presented an acute problem over the past 70 years as Bloomberg reports, “stocks have appreciated five times as much as housing prices.” However, the complexity of wealth without a conversation around income and disposable income which is income left over after expenses that can be used for savings and investing is vital to the conversation. African American median income is $45,870 according to Statista, the highest it has been in the past 30 years. The problem of course is that it remains the lowest of all four ethnic groups tracked (see graph below) with Latinos, European, and Asian Americans having median incomes of $55,321, $74,912, $94,903, respectively. Unfortunately, there is not a high enough savings rate that could truly overcome this lack of income. Despite the perception, African Americans are savers in line with their European American counterparts. Again, you can not catch up in a race running at the same speed as someone who is 100 yards ahead of you. This is the problem for African America. We are trying to save and invest at the same rate as those who have in most cases six times our wealth. So if home ownership is already our largest asset, then why are we suggesting that African American couples prioritize having two going into a marriage rather than one after they get married?

Every HBCU state except for Pennsylvania offers a homestead exemption. What is the homestead exemption? According to Investopedia, “The homestead exemption is a way to minimize property taxes for homeowners. It is also a legal provision offered in most states that helps shield a home from some creditors following the death of a homeowner’s spouse or the declaration of bankruptcy. The homestead tax exemption can provide surviving spouses with ongoing property tax relief, which is done on a graduated scale so that homes with lower assessed values benefit the most. The homestead exemption is helpful since it is designed to provide both physical shelter and financial protection, which can block the forced sale of a primary residence.” A person or couple can only have one homestead at a time, unless they both enter into the marriage with their own homestead. At which point, both parties are allowed to retain their individual homesteads. This means both properties will be taxed at a reduced rate creating more disposable income. Something they would not be able to do if they simply purchased a second home later in the marriage. What is that second homestead worth potentially?

According to Mortgage Calculator, the average annual property taxes in the United States is approximately $3,800. The homestead exemption typically saves approximately $500 off of that tax bill. That $500 invested annually for 30 years at 8 percent return is worth over an extra $60,000 to a household and that is just the tax savings reinvested. Naturally, the second homestead would be rented out by the couple and used to generate additional passive income. Assuming the couple could generate a profit of $200 per month or $2,400 annually off that second property, they now have $2,900 to invest annually which over the course of 30 years at 8 percent return is worth over $350,000. We have not even added on the building of the equity from appreciation or the extremely low interest rates that accompany homestead properties versus traditional investment properties. Banks are far more likely to see a homestead property as a lower risk than investment properties which they believe a borrower is more likely to walk away from than those that are homesteaded. Equity borrowed from the home could be used to reduce the households general tax bill overall further, leveraged to purchase non-homestead investment properties, or simply borrowed and used to invest in the stock market and because it is seen as “debt” does not carry tax liability on it. In other words, if a couple borrows $50,000 of equity out of their homestead property and make $10,000 on it, then they would only be paying taxes on the $10,000 but you still actually have $60,000 at your disposal. Whereas if you saved $50,000 and then made $10,000 on it, then you would be paying taxes on the entire $60,000. That almost $3,000 per year that would be coming from that property would also be an increase of 6 percent on the African American median income.

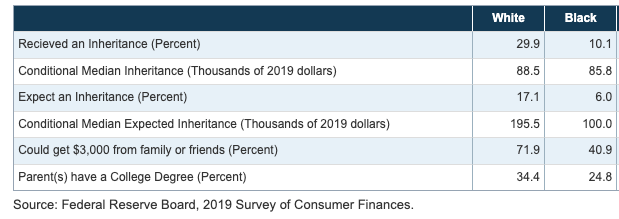

In the end of it all, assets and income go hand in hand. The more assets a family has the more income they produce and vice versa. In some ways, it is the epitome of the chicken and the egg conversation. For most African Americans, whom we see are highly unlikely to receive inheritance (see graph above) it becomes all about their family’s initial income and the race to acquire assets. Grievously, far too many African American families get the income and never convert it into assets. Taking advantage of prioritizing this little loophole can provide a family an extra $1 million in asset value and $80,000 in passive income if properly managed. An amount that currently would equal almost two times the African American median income. It is these small decisions that could have a monumental impact on the future of African American wealth and the closing of the wealth gap. In order for this to work as part of an overall strategy, HBCU alumni must prioritize having a sense of urgency about their finances and then be strategic about wealth and asset accumulation before tying the knot.