African American-owned credit unions hold more than $8.15 billion in assets and serve 726,929 members in 2025, more than doubling their asset base from $3.81 billion in 2016. That growth confirms that Black-owned cooperative finance remains a living, expanding sector — not a historical artifact. Yet placed against the broader credit union landscape, the numbers tell a more sobering story. The federally insured credit union system holds $2.37 trillion in total assets across 4,411 institutions. African American-owned credit unions, with 205 active institutions down from 318 in 2016, control just 0.34 percent of that total asset base. The sector’s 453 Minority Depository Institution-designated peers collectively hold $95.1 billion in assets; African American institutions account for less than 9 percent of that figure. The gap is not closing fast enough.

The structural challenges are as significant as the asset gap. The median African American-owned credit union holds approximately $2.47 million in assets and serves roughly 618 members placing it squarely in the asset tier where the national system is contracting most aggressively, with institutions under $10 million posting declines in assets, membership, and net worth year over year. Only 40 percent of these institutions maintain an active public website, rendering the majority functionally invisible to younger and mobile-first members. An estimated 30 percent are affiliated with religious congregations, compared to approximately 5 percent of all U.S. credit unions, introducing succession and governance risks that extend well beyond normal institutional turnover. Meanwhile, the HBCU-based credit union subsector has seen five of its eleven institutions close or be absorbed since 2020, leaving six survivors holding a combined $76.8 million in assets — institutions that represent the most direct expression of university-anchored Black financial infrastructure and are quietly disappearing without coordinated intervention.

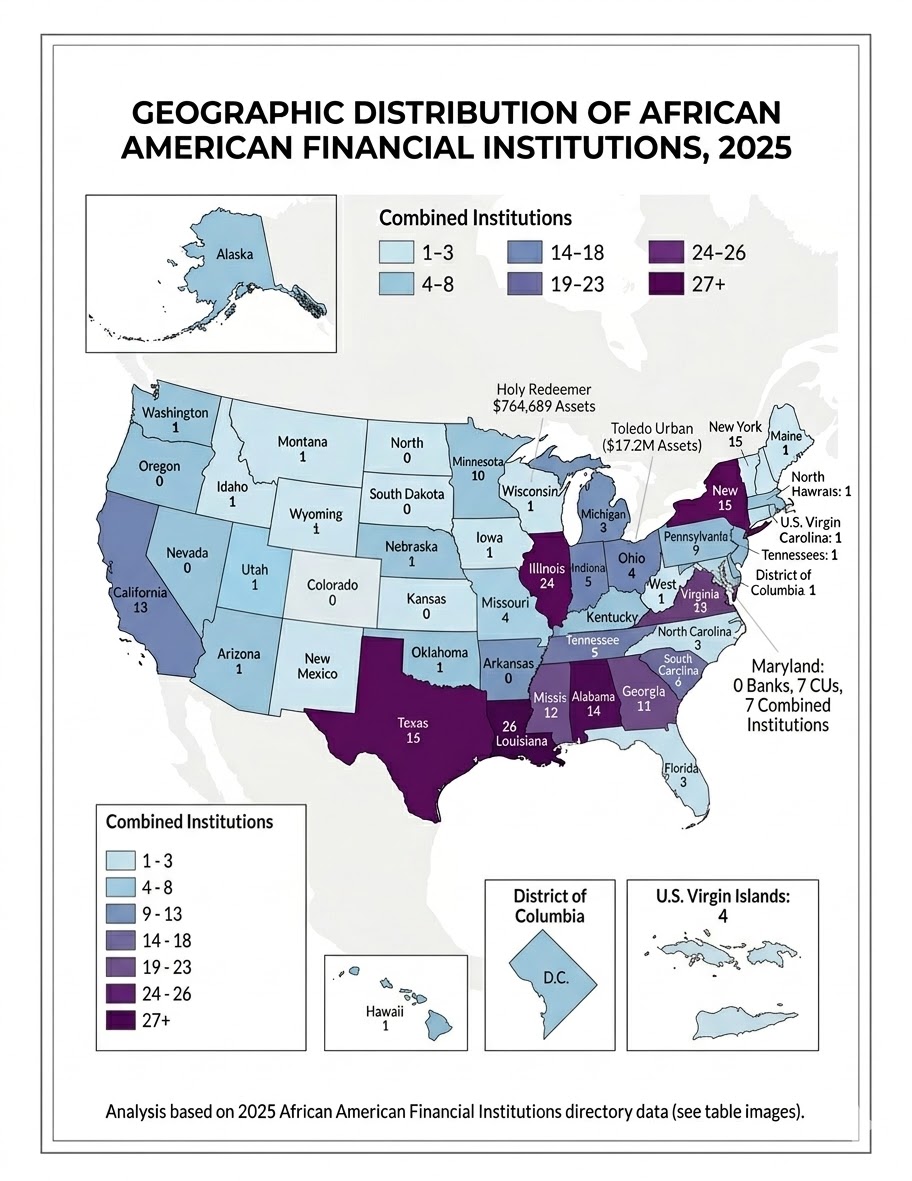

The sector’s geographic concentration compounds these institutional vulnerabilities. Maryland, Mississippi, Missouri, and Virginia together account for roughly 80 percent of all African American-owned credit union assets nationally, while states like California, Minnesota, and Wisconsin maintain only token institutional presences despite substantial African American populations. The South remains the geographic and institutional core, with Louisiana’s 25 institutions representing the largest state count and Mississippi’s Hope Credit Union standing as the sector’s clearest model of what scale and institutional commitment can produce. The path forward runs through consolidation where fragmentation cannot be reversed, digital investment where infrastructure is absent, geographic expansion where populations go unserved, and the fuller utilization of federal support mechanisms such as MDI designation, CDFI certification, and NCUA technical assistance that the sector has historically left on the table.

ADDITIONAL NOTES

- African American-owned credit unions now hold $8.15 billion in total assets across 205 active institutions, representing 0.34 percent of the $2.37 trillion held by all federally insured credit unions nationally.

- Total assets in the sector have more than doubled since 2016, rising from $3.81 billion — a 114 percent increase — while membership grew 39.5 percent from 521,078 to 726,929 members over the same period.

- AACUs average assets per institution: approximately $39.8 million. AACUs median assets per institution: approximately $2.47 million. The gap between the mean and median reflects a sector dominated at the top by a small number of large institutions while the majority operate at a scale that limits their competitive viability.

- AACUs average members per institution: approximately 3,546. AACUs median members per institution: approximately 618.

- Only 40 percent of African American-owned credit unions maintain an active public website, representing a critical digital infrastructure deficit in an era of mobile-first financial services.

- An estimated 30 percent of African American-owned credit unions are affiliated with religious congregations compared to approximately 5 percent of all U.S. credit unions introducing institutional succession risk as American religious participation continues its long-term demographic decline.

- Louisiana has the largest number of active African American-owned credit union institutions (25), followed by Illinois (23), New York (15), Texas (14), Virginia (13), and Alabama and the District of Columbia with 12 and 10 respectively. Maryland leads all states in total sector assets at $4.47 billion, followed by Mississippi at $1.05 billion and Missouri at $480 million.

- California — the most populous U.S. state and home to one of the largest African American populations in the country — has a single active African American-owned credit union with $318,105 in assets and 262 members, a presence that has contracted since 2016.

- The sector’s credit union count has declined from 318 institutions in 2016 to 205 active institutions in 2025, a reduction of 35 percent, driven primarily by closures, mergers into non-Black institutions, and voluntary dissolutions.

- For comparison, the national credit union system added 2.9 million members over the past year alone, reaching 143.2 million total members — nearly 200 times the total membership of all African American-owned credit unions combined.

African American Owned Credit Unions by State:

Source: NCUA