African Americans navigating their financial lives are operating inside two fundamentally different types of institutions, and understanding that difference is not academic it is strategic. JPMorgan Chase, the largest bank in the United States with over $3.9 trillion in assets, is a publicly traded corporation owned by shareholders. Its mandate is profit. It can accept corporate deposits, underwrite municipal bonds, finance international trade, issue letters of credit that move goods across oceans, syndicate billion-dollar loans, and operate in 100 countries. When a city government needs to finance a new highway, when a developer needs to close on a $200 million mixed-use project, when a corporation needs to hedge currency risk across three continents — JPMorgan is in that room. Navy Federal Credit Union, the largest credit union in the United States with approximately $180 billion in assets, is a member-owned cooperative. Its mandate is service to its members, who must meet eligibility requirements tied to military affiliation. It offers mortgages, car loans, checking accounts, and credit cards often at better rates and lower fees than JPMorgan but it cannot write a commercial real estate construction loan for a developer, cannot underwrite a municipal bond for a city, cannot finance an export contract for a manufacturer shipping goods to West Africa, and has no presence in international capital markets. Navy Federal is a powerful institution for what it does. It simply does not do what JPMorgan does, and JPMorgan does not do what Navy Federal does at the community level. For African Americans, this distinction carries enormous consequence. A community with only credit unions has access to consumer financial products; mortgages, auto loans, personal savings but lacks the commercial banking infrastructure needed to finance business growth, real estate development, institutional deposits, and economic expansion. A community with only banks, and specifically only large national banks with no cultural accountability, has access to products but not necessarily to equitable underwriting, community reinvestment, or the trust that comes from shared ownership. The absence of an African American-owned bank in Ohio or Wisconsin is not just symbolic. It means no institution with a community mandate is positioned to finance the next African American developer, fund the next HBCU-adjacent business corridor, or serve as a depository for the growing institutional wealth of Black organizations in those states.

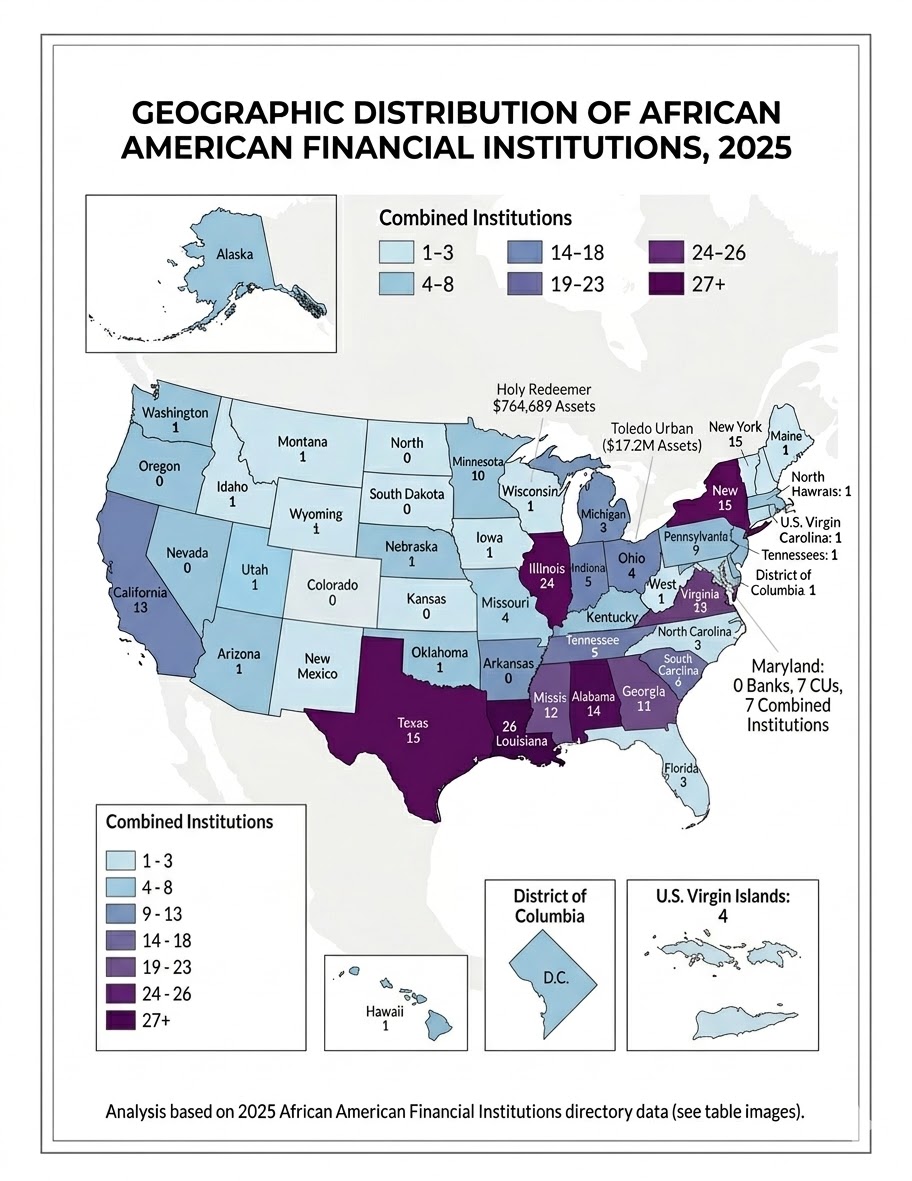

When the geography of African American banks and credit unions is examined together, a more complete — though still incomplete — picture of Black financial infrastructure emerges across the United States. The 2025 African American Owned Bank Directory covers 17 institutions across 15 states and territories. The 2025 NCUA data on African American credit unions adds 205 institutions across 29 states and territories, carrying $8.15 billion in assets and serving approximately 727,000 members. Combined, the two sectors represent over 220 institutions and more than $14.8 billion in assets operating across 31 states and territories. But geography, not just totals, is where the real story lives.

Thirteen states have both an African American-owned bank and at least one African American credit union: Alabama, the District of Columbia, Georgia, Illinois, Louisiana, Michigan, Mississippi, North Carolina, Oklahoma, Pennsylvania, South Carolina, Tennessee, and Texas. These are the states with the fullest financial ecosystem — where a community member can choose between a bank product and a credit union product from an institution with cultural roots in their community. Louisiana stands out, with one bank and 25 credit unions, the most of any state in the credit union count. Illinois follows with one bank and 23 credit unions.

Two states have African American banks but no African American credit unions in the NCUA data: Massachusetts, home to OneUnited Bank, and Utah, newly represented by Redemption Bank. These institutions serve their communities without the complementary infrastructure of a credit union network. Conversely, 16 states and territories have African American credit unions but no African American-owned bank: Arkansas, California, Connecticut, Delaware, Florida, Indiana, Maryland, Minnesota, Missouri, New Jersey, New York, Ohio, Virginia, the U.S. Virgin Islands, West Virginia, and Wisconsin.

The cases of Ohio and Wisconsin, discussed at length in the bank directory analysis, illustrate the limits of credit union coverage as a substitute for bank presence. Ohio has four African American credit unions with combined assets of approximately $18.3 million: Mahoning Valley in Youngstown, Mt. Zion Woodlawn in Cincinnati, Cleveland Church of Christ in Cleveland, and Toledo Urban in Toledo. Of these, Toledo Urban is the only institution of meaningful scale at $17.2 million in assets with 4,324 members. The other three are micro-institutions, each under $600,000 in assets and under 400 members. Wisconsin’s single credit union, Holy Redeemer Community of SE Wisconsin based in Milwaukee, holds just $764,689 in assets and serves 239 members. For a city where African Americans comprise roughly 39 percent of the population, that represents an institutional void that one small credit union cannot fill. Neither Ohio nor Wisconsin has an African American financial institution capable of writing a commercial real estate loan, funding a startup, or underwriting a mortgage for a first-generation homebuyer at any meaningful scale.

African American Financial Institutions by State, 2025

| State | African American Banks | African American Credit Unions | Combined Institutions |

| Alabama | 2 | 12 | 14 |

| Arkansas | 0 | 3 | 3 |

| California | 0 | 1 | 1 |

| Connecticut | 0 | 3 | 3 |

| Delaware | 0 | 1 | 1 |

| District of Columbia | 1 | 10 | 11 |

| Florida | 0 | 3 | 3 |

| Georgia | 2 | 9 | 11 |

| Illinois | 1 | 23 | 24 |

| Indiana | 0 | 5 | 5 |

| Louisiana | 1 | 25 | 26 |

| Maryland | 0 | 7 | 7 |

| Massachusetts | 1 | 0 | 1 |

| Michigan | 1 | 4 | 5 |

| Minnesota | 0 | 2 | 2 |

| Mississippi | 1 | 11 | 12 |

| Missouri | 0 | 4 | 4 |

| New Jersey | 0 | 9 | 9 |

| New York | 0 | 15 | 15 |

| North Carolina | 1 | 2 | 3 |

| Ohio | 0 | 4 | 4 |

| Oklahoma | 1 | 1 | 2 |

| Pennsylvania | 1 | 8 | 9 |

| South Carolina | 1 | 5 | 6 |

| Tennessee | 1 | 5 | 6 |

| Texas | 1 | 14 | 15 |

| Utah | 1 | 0 | 1 |

| U.S. Virgin Islands | 0 | 4 | 4 |

| Virginia | 0 | 13 | 13 |

| West Virginia | 0 | 1 | 1 |

| Wisconsin | 0 | 1 | 1 |

Maryland presents a striking and instructive contrast. It has no African American-owned bank, a gap noted in the 2025 directory, yet it is the single largest state for African American credit union assets, hosting seven institutions with a combined $4.47 billion in assets. That figure is driven primarily by two institutions: Andrews Federal Credit Union in Suitland with $2.47 billion in assets and 142,076 members, and Municipal Employees Credit Union of Baltimore with $1.26 billion in assets and 98,358 members. Maryland’s credit union sector is, in asset terms, larger than the entire African American bank sector nationally. This is remarkable. It is also a reminder that credit unions and banks occupy different structural roles. Andrews Federal and MECU of Baltimore are large, sophisticated institutions with product offerings that approach commercial banking but they are member cooperatives, not banks, and their ownership structure, regulatory environment, and community lending mandates differ accordingly. Maryland’s absence from the bank directory is still a gap worth addressing, even with $4.47 billion in credit union assets in the state.

Virginia and Missouri follow a similar pattern to Maryland, albeit at smaller scale. Virginia has 13 African American credit unions with $471 million in assets but no African American-owned bank. Missouri has four credit unions with $481 million in assets, anchored by St. Louis Community Credit Union at $431.5 million, and also no bank. New York has 15 credit unions with $76 million in assets and no African American bank, a particularly stark figure given the size of New York’s African American population and its status as the financial capital of the country.

The states that are entirely absent from both the bank and credit union directories deserve attention. While the combined coverage of 31 states and territories is broader than either sector alone, large portions of the country remain without any African American-owned financial institution. States like Nevada, Arizona, Colorado, Washington, Oregon, and much of the Mountain West and Pacific Northwest have no representation in either directory. As African Americans continue to migrate to new metros — Las Vegas, Phoenix, Denver, Seattle — the absence of community-controlled financial institutions in those corridors becomes a growing concern.

The combined picture is this: African American banks and credit unions together hold approximately $14.8 billion in assets, serve over 700,000 credit union members and the deposit base of 17 banks, and operate across 31 states and territories. The credit union sector, at $8.15 billion in assets across 205 institutions, is actually slightly larger than the bank sector’s $6.72 billion across 17 institutions, a reflection of the credit union model’s greater accessibility and the longer runway some of these institutions have had to grow. But the two sectors are not interchangeable. Banks can hold commercial deposits, write business loans, issue letters of credit, and serve as the financial backbone of an entrepreneurial ecosystem in ways that most credit unions cannot. Credit unions, in turn, offer member ownership, lower fees, and community accountability that publicly or privately held banks may not. The African American community needs both, in every state where its population is substantial. Right now, it has neither in too many places that matter.

Sources: HBCU Money 2025 African American Owned Bank Directory; 2025 NCUA African American Credit Union Institutions data. Asset figures in U.S. dollars.

Disclaimer: This article was assisted by Claude (Anthropic).