“Talent without institutions is a pipeline to someone else’s profit.” – William A. Foster, IV

In a pivotal scene from the film Moneyball, Billy Beane stares across the table at a room of seasoned scouts and executives, asking again and again, “What’s the problem?” The men fumble for surface-level answers—lost players, declining performance, tight budgets—but Beane cuts through the noise with surgical precision: “You’re not even looking at the problem.” His frustration isn’t simply about baseball; it’s about the failure to reframe strategy in the face of structural disadvantages. It’s about institutions mistaking symptoms for causes.

That same failure of vision and the urgent need for a paradigm shift applies not just to baseball, but to African America’s quest for economic power, institutional wealth, and self-determined sovereignty.

African America’s greatest minds, labor, and capital are often deployed outside of African American institutions. In essence, the community is fielding players, but not for its own teams. Valedictorians enroll at predominantly white institutions. Brilliant entrepreneurs pitch to Silicon Valley venture capitalists. Top athletes build billion-dollar empires for Nike, not Actively Black. The irony is that African America is not talent-poor. It is institution-poor. And that distinction is everything.

The most misunderstood problem in African American wealth-building discourse is not the racial wealth gap, it is the institutional wealth gap. African America commands over $1.6 trillion in consumer spending power annually, yet circulates less than 2% of that inside its own institutions before it exits the community entirely. Compare this to Jewish Americans, who circulate an estimated 8 to 12 times within their institutional networks, or East Asian Americans at 6 to 12 times, or even Latino Americans at 4 to 6. The velocity of African American economic energy leaves almost immediately. Another financial literacy seminar cannot fix this. What is required are financial institutions that keep wealth anchored in the community and institution-to-institution cooperation that builds collective power rather than isolated individual net worth.

Much like Billy Beane confronting baseball’s scouting orthodoxy, African America must confront its deep obsession with prestige, particularly the pursuit of inclusion in institutions that were never designed for its empowerment. The community still celebrates when African Americans “break barriers” into historically exclusive spaces: the first Black partner at a global law firm, the first Black president of an Ivy League university, the first Black billionaire appointed to a PWI board. These are symbolic gestures, not systemic gains. They are the equivalent of drafting a slugger with a high batting average while ignoring his low on-base percentage. It may photograph well, but it does not win championships.

Meanwhile, African American institutions like HBCUs, Black-owned banks, credit unions, media companies, foundations remain undercapitalized and under-circulated. According to FDIC data, African American banks account for less than 0.03% of the U.S. banking system’s total assets, despite serving millions of customers. Most carry assets under $500 million, while PNC, JPMorgan Chase, and Bank of America each hold hundreds of billions in Black consumer deposits alone. The community is putting elite players on the field just not on its own team.

One of the most damaging consequences of the post-civil rights integration era has been the illusion of proximity to power. Inclusion into dominant systems has led many African Americans to feel they are participating in the architecture of power, when in reality they are consumers of it, not owners. The institutions that determine economic direction in this country like investment firms, insurance conglomerates, think tanks, and lobbying organizations remain largely absent African American leadership at the structural level. While the public fixates on celebrity billionaires, it rarely accounts for institutional billionaires: universities with $40 billion endowments, banks with $3 trillion balance sheets, pension funds managing hundreds of billions in assets. Harvard University’s endowment, at roughly $50 billion, generates more annual passive income than the top 20 HBCUs combined in operating budgets. The Ivy League is not competing with African America. It operates on an entirely different playing field.

The data makes the scale of the gap unmistakable. As of 2022, the median net worth of a white household exceeded $188,000. For African American households, the figure was $24,100. But the institutional gap is even more stark. The top 10 predominantly white universities hold over $200 billion in combined endowments. The top 10 HBCUs hold less than $3 billion combined. In the philanthropic sector, the contrast is equally severe: the Gates Foundation manages nearly $8 billion in annual revenue and over $80 billion in assets. Meanwhile, even foundations attached to African American billionaires often operate at a fraction of that capacity. When African Americans are high earners individually, they frequently exist within ecosystems of institutional fragility—fragile schools, fragile banks, fragile civic organizations. This fragility makes individual wealth vulnerable, disperses influence, and mutes policy impact. The community continues to negotiate from positions of dependence.

The strongest ethnic and national economies do not simply focus on internal wealth generation, they construct infrastructure for internal circulation and cooperation. That means Black-owned banks financing Black developers. HBCUs recruiting faculty trained at other HBCUs rather than defaulting to PWI pipelines. Black foundations endowing Black hospitals, think tanks, and research centers. Black technology firms building hiring relationships with HBCU STEM programs. Black media outlets directing advertising budgets toward Black-owned businesses rather than relying on revenue from Google and Pepsi. Currently, this kind of circulation is sporadic and disorganized. Too often, African American institutions function as isolated islands, each struggling independently in a competitive environment that rewards scale and coordination. What is needed is a federation mindset of institutions operating in genuine symbiosis, where growth is strategic rather than accidental. Consider the compounding effect if every HBCU committed 20% of its endowment to Black-owned financial institutions, or if every African American megachurch directed 10% of its annual budget toward a Black-owned insurance provider. These institution-to-institution agreements would create forms of institutional wealth that accumulate quietly but with enormous strategic consequence.

Billy Beane’s genius in Moneyball was not merely contrarianism. It was data literacy. He saw what others refused to acknowledge: that reaching base was more valuable than batting average, and that the traditional metrics of scouting obscured the actual drivers of winning. African America must apply the same discipline to its institutional life. That requires building institutional balance sheets that honestly account for asset and liability structures; capital flow maps that trace where African American money goes after it is earned; circulation velocity metrics that measure how many times a dollar moves among Black institutions before exiting; and influence indexes that evaluate which African American institutions actually shape policy, capital markets, and media narratives. Without that data infrastructure, the community will continue to feel prosperous in moments while remaining fragile in structure and celebrating the anecdote while missing the trend.

Talent allocation is the other dimension of the problem that demands a strategic reframe. Just as the scouts in Moneyball chased big names and home run statistics, African American institutions often pursue talent without connecting it to long-term institutional strategy. Celebrity partnerships, honorary degrees, and gala appearances generate visibility but rarely feed institutional growth. A Tuskegee graduate built the foundations of American agricultural science. But talent, without institutions to give it depth, direction, and deployment, is ultimately portable. It gets recruited away, diluted, or co-opted. The community does not simply need more talented individuals. It needs to scout differently, train differently, and deploy those individuals in ways that compound institutional strength rather than individual achievement.

The question of narrative control is inseparable from the question of institutional power. Of the top twenty media companies in the United States, none are Black-owned. Most African American narratives in news, entertainment, and advertising are filtered through non-Black ownership and editorial priorities. This means political discourse is easily hijacked, cultural capital is regularly commodified without equity stakes, and social movements are routinely defanged by outside interests with different agendas. Reclaiming narrative sovereignty requires sustained investment in Black-owned media, particularly digital platforms and local investigative journalism. More critically, it requires routing advertising dollars toward Black media institutions rather than treating them as secondary channels. Even the most incisive voices will remain echoes if they are amplified through someone else’s infrastructure.

The genius of Billy Beane was not discovering undervalued players, it was reframing the entire game. African America has been operating under a set of assumptions that no longer serve its institutional interests, if they ever did. It has been trying to win with outdated tactics, sentimental strategies, and a persistent belief that the core problem is individual rather than structural. Fighting racism is necessary but insufficient. Engineering sovereignty is the work. That begins with an honest diagnosis: African America is building talent for other people’s institutions. It is celebrating inclusion while surrendering control. It is mistaking prestige for ownership. And it continues to treat the gap as primarily personal when the evidence points overwhelmingly to institutional causes.

“You’re not even looking at the problem,” Beane said.

It is past time to look.

Disclaimer: This article was assisted by ClaudeAI.

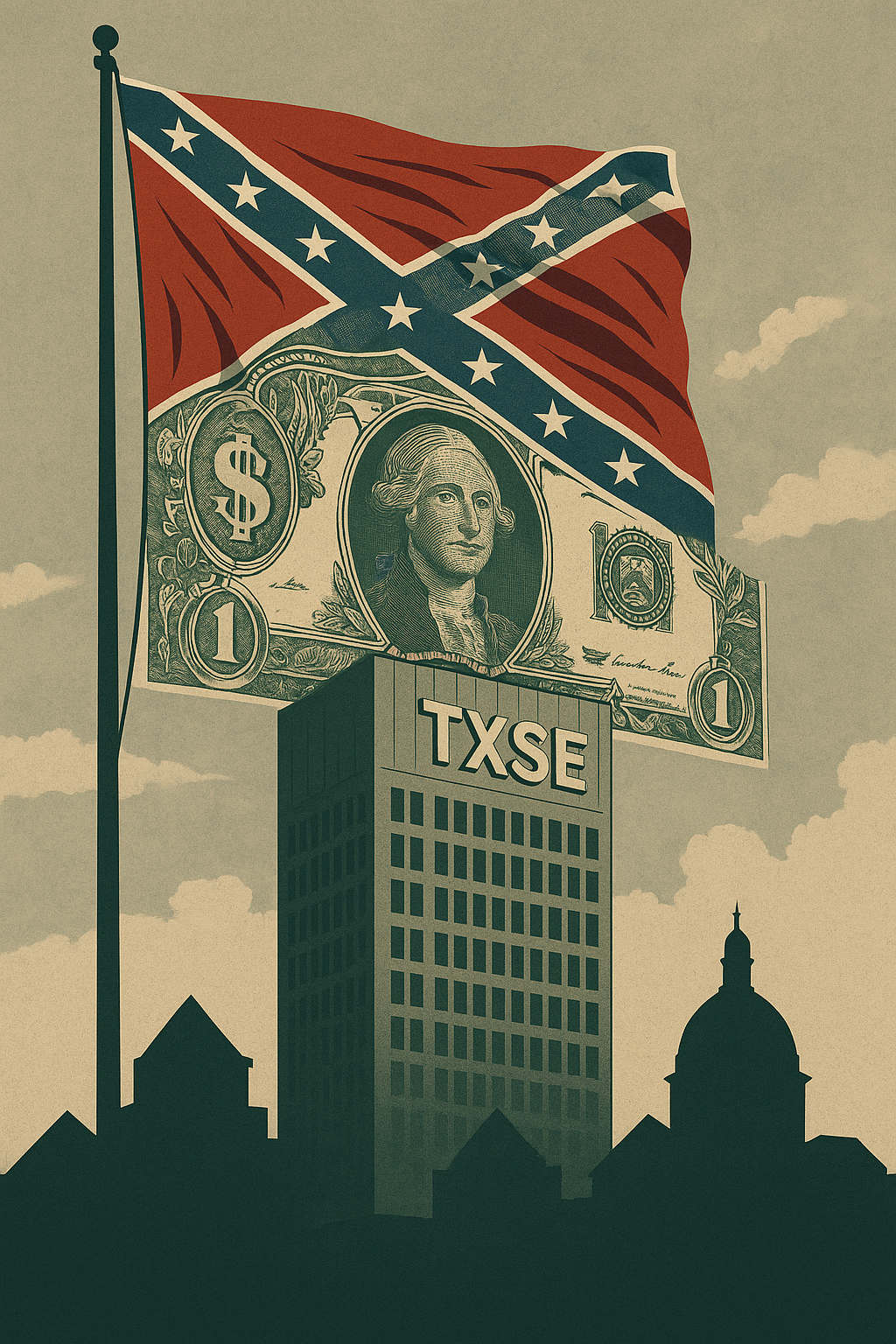

The South never stopped fighting the Civil War. It was the Cold War before the Cold War with USSR and it has been the Cold War after the USSR collapsed. America’s greatest war has always been within. The North, then and for too long thereafter thought it could give an inch and welcome its southern brethren back, but a mile and then some were taken. At this moment, all that remains for the South to conquer is the taking of the North’s financial capital from New York and it will have – checkmate. The South has risen and won. – William A. Foster, IV

The United States has never had a single center of financial power, but it has never had one this far south either. The Texas Stock Exchange — TXSE — formally launching in 2025, is not a regional curiosity. It is the institutional centerpiece of a coordinated effort to reshape who controls the rules of American capital markets, and the African American institutional ecosystem has not yet reckoned with what that means for its long-term economic position.

Founded in 2023 and capitalized with $120 million in initial funding from investors including BlackRock, Citadel Securities, Charles Schwab, and Virtu Financial, TXSE is aiming directly at the New York Stock Exchange and Nasdaq. Its headquarters are in Dallas. Its leadership includes former Texas Governor Rick Perry and former Dallas Federal Reserve President Richard Fisher. Its pitch to potential issuers is a governance environment that its founders describe as more CEO-friendly: reduced compliance requirements, streamlined listing rules, and a posture explicitly hostile to the accountability frameworks that have, however imperfectly, created some structural space for African American institutional participation in mainstream capital markets. For the African American institutional ecosystem — HBCUs, Black-owned banks and credit unions, Black-owned companies, professional associations, and the community development financial institutions that serve communities mainstream finance has historically ignored — this is not a distant policy question. It is a direct threat to the ownership architecture that the community is still trying to build.

To understand TXSE requires understanding the political economy of the modern South, and that requires a historical anchor. During Reconstruction, African Americans built consequential institutional infrastructure against enormous opposition: Black-owned banks, insurance companies, newspapers, and colleges that competed credibly in American economic and civic life. That infrastructure was not dismantled by market forces. It was dismantled by the same mechanism that has constrained African American institutional ownership in every era — control the rules of the game, and you control who benefits from playing it. The Freedman’s Savings Bank collapsed after federal mismanagement stripped depositors of $3 million in assets. The Greenwood District of Tulsa, the most concentrated expression of African American commercial ownership in the country’s history, was burned in 1921 with official sanction. Across the South and beyond, Black-owned enterprises were regulated out of existence, denied credit access, or destroyed. The consistent instrument was institutional architecture — the deliberate construction of financial rules that embedded the interests of one group at the expense of another. The Texas Stock Exchange is that instrument, updated for the twenty-first century.

Texas has rapidly positioned itself as the national headquarters of the movement to strip social and governance accountability from investment and corporate decision-making. In 2023, Governor Greg Abbott signed legislation banning state contracts with any firm that considers environmental, social, or governance factors in its investment decisions. The state legislature has moved to constrain public pension fund managers from incorporating anything beyond narrow financial return metrics, explicitly prohibiting the mission-aligned investing frameworks that community development financial institutions and HBCU-linked endowment vehicles depend on to justify participation in community-anchored development projects. Florida has enacted parallel restrictions. Oklahoma’s state treasurer blacklisted more than a dozen financial institutions for their stated climate commitments. Tennessee, Georgia, and a growing list of other states are constructing the same legal and financial infrastructure, all oriented toward the same goal: a parallel financial order governed by Southern political priorities, insulated from federal regulatory oversight and from the investment norms of the institutions that have grudgingly made room for African American institutional participation. What HBCU Money has documented over years of covering African American institutional finance by highlighting the slow erosion of Black-owned banks, the chronic undercapitalization of HBCU endowments, the failure of institutional capital to circulate within the African American ecosystem is now confronting a coordinated counterforce operating with the full backing of state governments, sovereign-scale endowments, and the largest names in global finance.

TXSE’s proposed listing standards deserve careful scrutiny because their effect on African American institutional economic participation is structural, not incidental. The exchange plans to impose earnings tests and revenue thresholds that would disqualify an estimated thirty percent or more of companies currently listed on Nasdaq, a category that includes a disproportionate share of minority-led, cooperatively structured, mission-driven, and early-stage enterprises. The cooperative structures, community development financial institutions, and early-stage technology firms that represent the growth edge of African American institutional economic activity are precisely the kinds of entities these standards are calibrated to exclude. Simultaneously, Texas has enacted legislation limiting shareholder lawsuits unless investors own at least three percent of a company’s shares. That threshold effectively neutralizes most activist shareholders, including African American pension funds, HBCU endowment investment vehicles, and minority-focused fund managers that rarely accumulate the concentrated positions necessary to meet that bar. The combination is a governance architecture designed to concentrate power among already-powerful institutional insiders and to diminish the accountability levers that African American institutional investors have worked to develop. This is not an accident of design. It is the design.

The University of Texas Investment Management Company — UTIMCO — manages the combined endowments of both the University of Texas System and the Texas A&M System. Together, these pools constitute one of the largest publicly managed academic endowment complexes in the United States, surpassing Harvard in combined assets under management. UTIMCO has, under sustained pressure from the Texas conservative political establishment, moved aggressively to align its investment posture with the ideological priorities of state leadership. It has reduced exposure to investment vehicles that incorporate social or governance accountability factors and directed assets toward domestic energy production, real estate, and financial instruments consistent with what its political overseers consider appropriate. UTIMCO’s scale gives it significant market-moving influence. Its alignment whether formal or informal with the TXSE project represents a formidable concentration of institutionally managed capital operating explicitly outside the accountability frameworks that African American institutional investors have built their participation strategies around. HBCU endowments hold a combined base that, while growing, remains dwarfed by what UTIMCO alone commands. The strategic implication is direct: when the largest endowment systems in the South are operating with an investment philosophy that excludes the governance accountability frameworks African American institutions depend on, the negotiating position of those institutions in the broader capital market is weakened.

The direct risks to African American institutional ownership are compounding across three distinct dimensions. The first concerns the exclusion of Black-led enterprises from the visibility, liquidity, and valuation premiums that accompany public market access. HBCU Money has documented that African American-owned employer businesses generated $212 billion in combined revenue in 2022 — a figure that, while representing meaningful growth, amounts to 0.43 percent of total U.S. business revenue for a community that constitutes over fourteen percent of the population. The exchange listing premium with the ability to attract institutional capital, establish a public valuation, and access the equity markets for growth financing has historically been one of the structural mechanisms that translates enterprise scale into compounding institutional wealth. TXSE’s listing standards are calibrated against the cooperative enterprises, CDFIs, and early-stage technology firms at the growth edge of African American institutional economic activity. Without access to a major exchange platform, these firms face persistent disadvantages in attracting the institutional capital that would allow them to scale. Over time, this structural exclusion deepens the ownership gap not through any single discriminatory act, but through the cumulative operation of market design.

The second dimension of risk concerns HBCU endowments and the broader African American institutional investment ecosystem. As HBCU Money has reported, African American-owned banks currently hold approximately $6.4 billion in combined assets — down from forty-eight institutions in 2001 to just seventeen today, and down from a peak share of 0.2 percent of total U.S. banking assets in 1926 to 0.027 percent today. HBCU endowments are managed, in most cases, through large fund managers some of whom are direct investors in the TXSE. As the exchange scales and as its listed companies grow in market capitalization, passive investment vehicles and actively managed funds will increasingly hold TXSE-listed assets as a matter of index composition and portfolio construction. HBCU endowment pools, pension funds serving African American public employees, and investment vehicles managed on behalf of Black institutional clients could find themselves indirectly capitalizing an exchange whose structural design, governance philosophy, and political alignment work against African American institutional interests. Annual interest payments transferred from Black households to non-Black financial institutions are estimated at approximately $120 billion — more than half of what all Black-owned businesses generate in revenue in an entire year. TXSE’s governance model is structured to compound that dynamic, not to reverse it.

The third and most consequential dimension concerns the governance architecture within which African American institutional ownership operates in publicly listed companies more broadly. The decades-long effort to increase African American representation in corporate governance, to build institutional investor coalitions capable of pressing for equitable accountability, and to develop shareholder advocacy tools that translate institutional capital into institutional voice has depended on an exchange and regulatory environment that, however reluctantly, created minimum conditions for accountability. TXSE’s governance philosophy centered on limiting shareholder litigation, reducing disclosure requirements, and eliminating the governance frameworks that allowed accountability advocacy to function would, if it achieves the national scale it is pursuing, erode the leverage that African American institutional investors have slowly accumulated. This is not a threat to abstract norms. It is a threat to the concrete mechanisms through which African American institutional capital translates into institutional power.

There is a cultural branding dimension to TXSE that should not be dismissed as mere marketing, because culture and capital are not separate categories they are the same category expressed differently. TXSE supporters have embraced the ‘Y’all Street’ branding, positioning Dallas as the spiritual and institutional opposite of what they call ‘woke capital.’ The slogans — ‘Texas roots. Global reach,’ ‘Built for CEOs, not bureaucrats’ — are explicit declarations of institutional identity. They communicate to potential issuers what governance norms the exchange will enforce, and they communicate to African American institutional stakeholders what norms will be conspicuously absent. An exchange that markets itself as the home of American finance divorced from social accountability is not making a neutral statement about regulatory philosophy. It is announcing its constituency. For the African American institutional ecosystem, that announcement should carry the same interpretive weight as any other structural signal about where capital will and will not flow.

The strategic response available to African American institutions is not the construction of a competing exchange. That framing misreads both the competitive dynamics of exchange infrastructure and the actual leverage points available. Exchanges are winner-take-most infrastructure. TXSE enters the market with $120 million in capitalization, the institutional backing of the largest names in global finance, and the network effects of a state government willing to direct sovereign-scale endowment capital in its direction. A Black-led exchange starting from zero cannot compete with that on equivalent terms in the near term, and proposing otherwise is not strategy — it is aspiration dressed as a plan. The more consequential response is coordinated institutional non-participation: the deliberate, organized withdrawal of African American institutional capital from TXSE’s orbit, combined with the systematic redirection of that capital toward institutions and instruments that serve African American ownership interests. This is not the high road. It is the only road with actual traction.

Executing that response, however, requires an honest accounting of which African American institutions are actually free to act and that accounting begins with the distinction between public and private HBCUs. The majority of HBCUs are public institutions, and the majority of public HBCUs are located in precisely the Southern states that are constructing the Southern Capital Doctrine. Southern University operates under the authority of the Louisiana Board of Regents. Florida A&M is a Florida state institution. North Carolina A&T, Prairie View A&M, Alabama State, Jackson State each operates within a state governance structure that gives hostile state legislatures direct leverage over budget, investment policy, and institutional positioning. These institutions cannot unilaterally reallocate endowment assets, cannot take public institutional positions against the financial policies of their host states, and in many cases cannot even direct their banking relationships without navigating state procurement rules that route dollars away from Black-owned institutions. Asking public HBCUs to lead the charge against TXSE is asking institutions to act against the direct interests of the governments that control their operating budgets. That is not a realistic foundation for strategy.

The private HBCUs occupy a structurally different position. Howard, Morehouse, Spelman, Hampton, Tuskegee, Xavier, Dillard, and their peer institutions have independent governance, control their own endowment investment decisions, and face no state legislative veto over their financial positioning. They are the tier of the HBCU ecosystem with the freedom to act directly to reallocate endowment capital away from fund managers backing TXSE, to direct institutional deposits toward Black-owned banks, to take explicit public positions on exchange governance policy, and to convene the broader institutional conversation that a coordinated response requires. The scale of their endowments, while modest relative to their peer institutions in the broader higher education landscape, is sufficient to establish meaningful momentum if directed in concert. Howard University’s endowment alone, if managed with the strategic intentionality that this moment demands, could anchor a coalition capable of making market-visible moves. Private HBCUs have the freedom that public HBCUs do not. The question is whether they will exercise it.

But the public HBCU ecosystem is not, for this reason, strategically irrelevant. It simply operates through a different institutional layer one that is frequently overlooked precisely because it does not appear on the official organizational chart. Every public HBCU has an alumni association that is legally and operationally independent of the institution itself. Every public HBCU has a foundation, a separately incorporated philanthropic entity with its own board, its own investment decisions, and its own capacity to act without state legislative approval. The Prairie View A&M National Alumni Association is not a Texas state agency. The Southern University Foundation is not subject to the Louisiana Board of Regents. The alumni associations and foundations of public HBCUs can bank with Black-owned financial institutions, direct philanthropic capital toward CDFIs, take public positions on financial policy questions, and coordinate with private HBCUs in ways that the institutions themselves cannot. If that coordination is sufficiently explicit and sustained, the functional effect is equivalent to the institution acting even though technically it is not. This is not a workaround. It is how every other community with sophisticated institutional strategy operates. The university cannot endorse a candidate. The alumni PAC can. The university cannot divest from a financial institution. The foundation can choose where to bank. The structure already exists. It simply has not been deployed with this level of strategic intention.

This layered architecture suggests a three-tier framework for the African American institutional response to TXSE. The first tier consists of private HBCUs acting as direct institutional agents reallocating endowment capital, directing deposits, and convening the policy conversation. The second tier consists of public HBCU alumni associations and foundations acting as coordinated proxy agents making the investment and banking decisions the institutions themselves cannot make, in deliberate alignment with the strategic direction being set by private HBCUs in the first tier. The third tier consists of the broader African American institutional network — Black-owned banks and credit unions, Black-owned firms, the Thurgood Marshall Fund and UNCF, the HBCU Faculty Development Network, African American professional associations, and African American-controlled pension and foundation assets — functioning as the connective tissue that allows the first two tiers to operate in concert without requiring any single institution to take a politically exposed position alone. Jewish American institutional strategy has operated through exactly this kind of layered coordination for generations. Korean rotating credit associations, Indian American technology sector networks, and Irish American political machines have each built equivalent structures calibrated to their specific institutional contexts. The African American community has all of the institutional components. It has not yet assembled them into a coordinated response mechanism.

On the question of regulatory engagement, intellectual honesty requires acknowledging the political environment directly. Petitioning the current Securities and Exchange Commission for intervention in TXSE’s governance standards is not a realistic near-term lever. The present administration’s posture toward exchange regulation, and toward the financial accountability frameworks that any such petition would invoke, makes meaningful regulatory relief under current leadership implausible. The more strategically sound approach is to build the legal and analytical record now to commission the research, document the structural exclusions, develop the regulatory theory, and position African American institutional stakeholders to arrive at a future administration’s SEC with a fully developed dossier rather than a reactive complaint. This is not passivity. It is the institutional discipline of building for the long game. Every dollar spent on legal analysis and regulatory documentation today is leverage that compounds when the political environment changes. TXSE is not going away. Its governance standards will be litigated and legislated over decades, not months. The community that has done the analytical work in advance will have the most influence over how that process resolves.

The parallel long-term aspiration deserves to be named more precisely than a vague commitment to Black-led exchange infrastructure and the most strategically coherent version of that aspiration points not inward but outward, across the Atlantic. The American Depository Receipt, the financial instrument that allowed foreign companies to list on U.S. exchanges without a full domestic registration, was built on a single insight: capital markets are not inherently bounded by national borders, and the right legal architecture can bridge them. That insight has historically flowed in one direction toward the United States, which offered the world’s deepest and most liquid capital markets, and therefore attracted the world’s enterprises seeking valuation and investor access. The generational goal for African American institutional finance is to reverse that directionality. Not to build a competing domestic exchange that fights TXSE on its home turf, under SEC jurisdiction, subject to the same regulatory environment TXSE is actively reshaping in its favor but to develop what might be called African Depository Receipts: a parallel instrument that would allow African American enterprises to list on African exchanges, access African institutional capital, and build the financial architecture of a genuinely transnational diaspora economy.

The mechanics of this idea deserve serious analysis rather than dismissal. The Ghana Stock Exchange, the Johannesburg Stock Exchange, the Nigerian Exchange Group, and the Rwanda Stock Exchange each represent meaningfully different regulatory environments, liquidity profiles, and investor bases and none of them, individually, yet offers the depth of the U.S. exchanges. These are not trivial complications. Currency risk, repatriation structures, cross-border regulatory compliance, and the still-developing institutional investor base on the continent are real structural challenges that any African Depository Receipt framework would need to address directly. But the original American Depository Receipt confronted equivalent complications when it was developed in 1927 to allow British investors to hold shares in American companies without navigating U.S. custodial arrangements directly. The instrument was built to solve exactly the kind of cross-border structural problem that an African Depository Receipt would need to solve today. The complications are engineering problems, not fundamental objections.

What makes this more than a financial instrument is the diaspora dimension that no domestic exchange alternative can replicate. African American businesses listing on African exchanges are not merely accessing a different pool of capital they are creating the institutional infrastructure for transnational capital flows that currently have no formal mechanism. They are building the financial architecture of the relationship between the African continent and its diaspora that has been gestured at politically and culturally for generations but never operationalized at the level of institutional ownership and capital markets. An African American technology firm listed on the Ghana Stock Exchange is not making a symbolic statement about Pan-African solidarity. It is creating a vehicle through which Ghanaian pension funds, South African institutional investors, and Nigerian family offices can hold ownership stakes in African American enterprises and through which African American institutional capital can flow toward African markets with the legal infrastructure, fiduciary accountability, and liquidity mechanisms that serious institutional investment requires. This is the financial architecture of diaspora strategy. It is what other transnational communities have built, in their own ways, over generations. The Irish American political machine was not just about elections it was about building the institutional relationships that made capital flow between Ireland and its diaspora. The Indian American technology network is not just about talent it is about the ownership and capital relationships that connect Silicon Valley to Bangalore. African American institutional finance has the community, the capital base, and increasingly the institutional sophistication to build an equivalent structure. The African Depository Receipt is the mechanism through which that structure becomes real.

This is honestly a twenty-year project. It requires the diplomatic groundwork of building formal relationships between African American institutional stakeholders and African exchange regulators and finance ministries. It requires the legal architecture of cross-border custodial arrangements, currency hedging instruments, and repatriation structures that protect both issuers and investors. It requires the development of African institutional investor capacity — African pension funds, sovereign wealth funds, and family offices — to the point where they can absorb meaningful African Depository Receipt issuance. And it requires the cultivation of African American enterprises of sufficient scale and governance maturity to make credible exchange listings. None of that is impossible. All of it takes time. The community should be building toward it now through the HBCU international programs and African studies centers that can develop the human capital, through the Black-owned financial institutions that can begin building the correspondent banking relationships, and through the private HBCU leadership that can convene the cross-institutional conversations this kind of generational commitment requires while executing the near-term response to TXSE through the levers it actually controls today: institutional non-participation in TXSE’s capital orbit, coordinated redirection of African American institutional deposits and endowment capital, and proxy action through alumni associations and foundations.

The Texas Stock Exchange is the latest iteration of a pattern that has defined African American economic history: rules written by others, in institutions controlled by others, to serve interests that have never included African American institutional ownership as a priority. The community’s $7.1 trillion in household assets, its $1.3 trillion in annual consumer spending, its $212 billion in employer-business revenue — none of that capital produces compounding institutional power without the ownership infrastructure to retain and redeploy it. African American-owned banks hold 0.027 percent of total U.S. banking assets. African American businesses generate 0.43 percent of total U.S. business revenue. HBCU endowments represent a fraction of what peer institutions hold. These are not cultural facts. They are ownership facts. And an exchange designed to deepen the concentration of institutional ownership among those who already hold it is not neutral infrastructure. It is a structural threat that demands a structural response not an aspirational one, but a concrete, coordinated, institutionally grounded one, built from the realistic assessment of which institutions are free to act, through which channels, and toward which ends.

The Confederacy never formally dissolved its ambitions. It adapted its instruments. Where it once used literacy tests to suppress political participation, it now uses listing standards and shareholder litigation thresholds to suppress institutional financial participation. Where it once burned Greenwood, it now writes exchange governance rules that make the next Greenwood structurally impossible to capitalize. African American institutions that understand this history have both the analytical framework and the institutional capacity to respond. The only remaining question is whether the community’s institutional leadership will treat the emergence of the Texas Stock Exchange with the strategic seriousness (threat) it deserves and whether it will organize that response through the institutions that are actually free to act, rather than waiting for the ones that are not.

Sidebar: A Three-Tier Response Framework for African American Institutions

Reallocate endowment capital away from fund managers backing TXSE; direct deposits to Black-owned banks; take public positions on exchange governance; convene cross-institutional strategy

Tier 2: Coordinated Proxy Actors

Public HBCU alumni associations and foundations (independent of state governance)

Bank with Black-owned financial institutions; direct philanthropic capital toward CDFIs; coordinate investment decisions in alignment with Tier 1 strategy; build public record on regulatory exclusions

Tier 3: Connective Tissue

Black-owned banks and credit unions; fraternities and sororities; NAACP; Urban League; African American professional associations; African American-controlled pension and foundation assets

Aggregate capital flows away from TXSE ecosystem; build and fund legal/analytical dossier for future regulatory engagement; sustain coordinated non-participation pressure across the institutional network

Note on regulatory strategy:

SEC engagement under the current administration is not a realistic near-term lever. The priority now is building the legal record, regulatory theory, and analytical documentation needed to engage a future administration’s SEC with a fully developed dossier. The generational goal is the development of African Depository Receipts — instruments allowing African American enterprises to list on African exchanges including the Ghana Stock Exchange, Johannesburg Stock Exchange, Nigerian Exchange Group, and others — creating the financial architecture of a transnational diaspora economy. This is a twenty-year project requiring diplomatic groundwork, cross-border legal architecture, and African institutional investor development. HBCU international programs, Black-owned correspondent banking relationships, and private HBCU leadership convening are the near-term building blocks.

Disclaimer: This article was assisted by ClaudeAI.

Love is or it ain’t. Thin love ain’t love at all. – Toni Morrison, Beloved

When Pittsburgh Steelers wide receiver DK Metcalf proposed to Grammy-nominated singer Normani in March 2025, everyone saw the romance. But few understood the deeper significance. Three years earlier, Russell Wilson and Ciara had orchestrated the introduction at a party where Ciara made sure Normani attended. “They was playing cupid, but it worked,” Normani later said. “If you could trust a couple [to set you up], that would be the couple.”

Four months later in July 2025, when NBA star Donovan Mitchell proposed to singer Coco Jones, the Wilsons were once again celebrating behind the scenes. Russell had helped plan the proposal, working with luxury event planners to create the perfect moment.

Two high-profile engagements. One couple quietly orchestrating connections. But this isn’t just celebrity matchmaking—it’s something more profound. Russell and Ciara Wilson are modeling what intentional Black love looks like, and the ripple effects could fundamentally reshape African American institutional capacity at a moment when our community desperately needs it.

What makes the Wilsons’ matchmaking significant isn’t the celebrity of the couples they bring together—it’s the deliberateness of it. They’re not hoping love happens. They’re creating the conditions for it. They’re investing three years of relationship before an engagement. They’re using their social capital to bridge different professional spheres, connecting successful Black professionals across industries who might never meet organically despite moving in similar circles.

This kind of intentionality around Black love has historical resonance. During the segregation era and Jim Crow, when every institution worked to keep Black families separated and destabilized, our communities survived by being deliberate about connection. Churches served as matchmakers. Family networks facilitated introductions. HBCUs became spaces where Black professionals met their future spouses. The community understood that strong marriages weren’t just about individual happiness—they were about survival and institutional building.

The data reveals something striking: marriage rates for Black adults were higher than for white adults in every U.S. Census from 1890 to 1940—the height of overt racism and segregation. Even in 1960, the marriage rate for Black adults was 61%, and two-thirds of Black children lived in two-parent households. Today, only 31% of Black Americans are married, and half have never been married at all.

What changed wasn’t racism—that existed then and persists now. What changed was the infrastructure of intentionality around Black love. The systems that deliberately brought people together, that supported young marriages, that made partnership formation a community priority—those eroded while the obstacles remained.

Understanding what the Wilsons are doing requires understanding what Black families have survived—and what continues to threaten our ability to build generational wealth and institutional power through stable partnerships.

The historical attacks on Black family formation were systematic and devastating. During segregation, redlining prevented Black families from buying homes in appreciating neighborhoods, which meant that even when Black couples married and saved, their wealth accumulated at a fraction of the rate of white families. Housing policies created by the federal government in the 1930s explicitly designated Black neighborhoods as too risky for mortgage lending, forcing Black families into predatory contracts that often ended in eviction.

But perhaps no threat has been more insidious than the systematic devaluation of Black women as romantic partners. Research consistently shows that Black women face unique marginalization in the dating market. Studies reveal that Black women receive the lowest desirability ratings on dating platforms from men of all races, with one 2014 OKCupid analysis finding Black women rated as “least attractive” compared to women of other races. These aren’t just numbers—they reflect deep-seated stereotypes that paint Black women as too masculine, too strong, too independent, too angry to be desirable partners.

The roots of these stereotypes trace directly to slavery, when Black femininity was deliberately contrasted against white femininity to justify Black women’s oppression and exploitation. When Black women assertively advocate for themselves, society—including some Black men—uses labels like “loud,” “angry,” and “emasculating” to question their worthiness for romantic relationships. The myth persists despite Black women’s clear desire for marriage and partnership.

This devaluation creates a devastating cycle. Black men face their own pressures and internalized racism, sometimes leading them to view relationships outside the Black community as aspirational—an “upgrade” that signals status and success. The data bears this out: among Black newlyweds with bachelor’s degrees, men are more than twice as likely as women to marry outside their race (30% versus 13%). Some Black men internalize colorism and Eurocentric beauty standards, further narrowing the pool of Black women they consider desirable partners.

When successful Black men choose partners outside the community without understanding the implications, they dilute the very networks and institutional capacity the Black community needs to build generational power. They reduce the already constrained supply of partners for Black women who, despite facing the most challenging dating environment of any demographic, remain the group most committed to intra-racial partnership. This isn’t about policing individual choice—it’s about recognizing that individual choices, aggregated across thousands of successful Black professionals, have community-level consequences for institutional sustainability.

When the Great Migration brought millions of Black families north seeking better opportunities, they found wages increasing but housing wealth eroding. Segregated housing markets meant Black families paid higher rents for deteriorating properties while watching their neighborhoods decline in value. The very act of Black families moving into a neighborhood triggered white flight, which collapsed property values. Homes that should have been vehicles for wealth accumulation became wealth traps.

Then came the deliberate destruction. The Tulsa Race Massacre of 1921 obliterated what was known as “Black Wall Street”—a thriving district where Black families owned land, operated businesses, and built wealth estimated at over $200 million in today’s dollars. Hundreds died, thousands were left homeless, and laws were passed to prevent survivors from rebuilding. This wasn’t unique. Chicago saw approximately 1,000 Black homes and businesses burned during the Red Summer of 1919. Across the country, thriving Black communities were systematically destroyed through racial violence that governments failed to prevent and often actively supported.

The wealth that did accumulate often couldn’t be transferred. Without access to estate planning services and facing discriminatory legal systems, many Black families lost property through “heirs property” designations that left land ownership unclear and prevented descendants from accessing the wealth their grandparents had built.

Today’s threats are more subtle but no less destructive. Mass incarceration has removed hundreds of thousands of Black men from their communities, destroying the gender balance needed for relationship formation. The student debt crisis hits Black families hardest—Black graduates owe an average of $25,000 more than their white peers—making the economic foundation for marriage more precarious. The wealth gap means young Black couples can’t fall back on family wealth during rough patches the way white couples can. Geographic dispersion means young Black professionals leave the high-marriage-rate states where HBCU ecosystems once facilitated connections, moving to cities where they’re isolated from institutional support networks.

But perhaps most damaging is the loss of cultural infrastructure around Black love. The deliberate community matchmaking of previous generations has largely disappeared. The social pressure and support for marriage has weakened. Dating apps have replaced friend introductions, optimizing for superficial attraction rather than shared values and compatible life goals. Young Black professionals, especially those who’ve left HBCU networks, often lack access to communities of Black peers navigating similar life stages.

The Wilsons understand something crucial: strong Black marriages aren’t just about personal fulfillment. They’re about building institutional capacity. When they facilitate a marriage between DK Metcalf and Normani, they’re not just creating a happy couple—they’re multiplying resources that could flow to Black institutions.

Consider the mathematics of it. Married couples don’t just have double the income of single individuals—they accumulate wealth exponentially faster. Black married couples have a median net worth of $131,000 compared to just $29,000 for single Black individuals. This isn’t because marriage magically creates money. It’s because marriage allows for coordinated financial strategy, shared expenses, combined networks, and the ability to take risks one income couldn’t support.

But the real multiplier effect extends beyond individual household wealth. Strong Black marriages create:

Coordinated Philanthropic Power: A married couple decides together where to direct resources. They create family foundations. They develop multi-year giving strategies to institutions they both value. They leverage their combined networks to recruit other donors. They become major benefactors rather than occasional contributors.

Intergenerational Institutional Commitment: Children from stable two-parent households inherit not just wealth but institutional loyalty. A child whose parents both attended HBCUs, both support Black cultural institutions, both invest in Black businesses—that child grows up with institutional commitment encoded in their identity. They become the next generation of supporters, leaders, and advocates.

Professional Network Effects: When two successful Black professionals marry, their networks merge. Different industries intersect, creating unexpected opportunities. Professional connections multiply. These network overlaps create opportunities for institutional partnerships, corporate sponsorships, business ventures, and talent pipelines that wouldn’t exist otherwise.

Resilience and Risk-Taking: Married couples can take risks single individuals cannot. They can invest in Black startups, fund untested ventures, support experimental programs, and make long-term commitments to institutions precisely because they have a partner sharing the risk. This risk-taking capacity is essential for institutional innovation and growth.

Cultural Modeling and Social Capital: Visible successful Black marriages change cultural narratives. They make marriage aspirational. They demonstrate what’s possible. They create social pressure in the positive sense—the expectation that successful Black professionals will find partners, build families, and invest in community. This cultural shift has compound effects across generations.

The geographic data supports this institutional impact. Seven of the top ten states with highest Black marriage rates—Virginia (34.0%), Maryland (33.2%), Texas and Delaware (32.8%), Florida and North Carolina (31.3%), and Georgia (30.9%)—are HBCU states. These states have thriving Black middle classes, strong African American institutions, and robust professional networks. The marriage rates aren’t coincidental—they’re evidence of how institutional ecosystems and family stability reinforce each other.

What the Wilsons are doing works because they understand marriage formation as network building. They’re not running a dating service. They’re curating a community of successful Black professionals who share values, understand each other’s pressures, and can build partnerships that transcend individual achievement.

Research shows people are still most likely to meet long-term partners through friends, family, or work rather than dating apps. The Wilsons are leveraging this truth at scale. Every couple they help create becomes a new node in an expanding network. Metcalf and Normani will introduce their single friends to each other. Mitchell and Jones will facilitate connections within their circles. The Wilsons’ nine-year marriage serves as the model and proof of concept.

This creates self-reinforcing cycles. Strong marriages produce stable families. Those families invest in institutions. Those institutions create spaces where the next generation forms relationships. Those relationships produce more strong marriages. The cycle builds momentum.

This is how communities accumulate power—not through individual success stories but through interconnected networks of families committed to collective advancement. During segregation, Black communities maintained this infrastructure deliberately because they had to. We knew that isolated success meant nothing if it couldn’t be transferred to the next generation or scaled across the community.

The Wilsons are reviving this model for the contemporary moment, when Black professionals are more economically successful than ever but often isolated from the institutional networks that would allow that success to compound.

Imagine if what the Wilsons are doing at the celebrity level was replicated across every tier of Black professional achievement. Imagine if young Black doctors, lawyers, engineers, educators, entrepreneurs were part of deliberate matchmaking networks that facilitated connections based on shared values and institutional commitment.

The compound effects would be staggering:

Economic Impact: Thousands of additional stable Black marriages would translate to billions in accumulated wealth. That wealth, properly channeled, could recapitalize Black institutions that have operated on shoestring budgets for generations. HBCUs could build endowments rivaling elite white institutions. Black hospitals could expand. Community development financial institutions could scale their lending. Black cultural institutions could thrive rather than merely survive.

Political Power: Married couples are more likely to vote, more likely to engage in civic life, more likely to serve on boards and run for office. A generation of politically engaged Black couples could fundamentally shift electoral dynamics and policy priorities in states with large Black populations.

Professional Advancement: The network effects of thousands of strategic Black marriages would create unprecedented opportunities for collaboration. Black entrepreneurs would have access to capital through their spouses’ networks. Black professionals would have insider information about opportunities through their partners’ connections. The “old boys network” that has excluded Black professionals for generations could be matched by networks of Black couples leveraging their combined social capital.

Cultural Renaissance: Stable Black families create the conditions for cultural production. Artists need economic security to take creative risks. Writers need time to develop their craft. Musicians need resources to experiment. When Black creative professionals have partners who can provide economic stability, the entire community benefits from their artistic output.

Institutional Sustainability: Perhaps most critically, networks of strong Black marriages ensure institutional continuity. When couples commit to supporting institutions together, those institutions can plan decades into the future. They can launch ambitious programs knowing they have committed donors. They can weather economic downturns because their supporter base is stable. They can dream bigger because their foundation is stronger.

But recognizing what’s possible raises uncomfortable questions about what’s missing. If the Wilsons can facilitate life-changing connections within celebrity circles, why doesn’t similar infrastructure exist for the thousands of Black professionals outside those circles? If marriage rates for Black adults were higher during Jim Crow than today, what infrastructure did we lose—and how do we rebuild it?

These questions don’t have simple answers, but they demand serious consideration:

How do we recreate the deliberate matchmaking infrastructure that sustained Black communities during segregation, adapted for contemporary circumstances? Church networks and family connections can’t carry the full weight when young Black professionals are geographically dispersed and disconnected from traditional institutions.

What would institutional investment in Black relationship formation look like? HBCUs, Black Greek organizations, professional associations, cultural institutions—these entities have the trust and access to facilitate connections. But do they recognize this as part of their mission? Do they allocate resources to it? Do they measure success by families formed, not just events hosted?

How do we address the structural barriers that make marriage economically precarious for young Black professionals? Student debt, wage gaps, wealth inequality, housing costs—these aren’t relationship problems, but they make relationship formation dramatically harder for Black Americans than for white Americans with similar educational attainment.

What role does media and culture play in shaping expectations around Black love? When the dominant narratives about Black relationships emphasize dysfunction and failure, when successful Black marriages are invisible, when young Black people grow up without models of healthy partnerships—this creates self-fulfilling prophecies that perpetuate the marriage gap.

How do we balance individual freedom and choice with community needs for strong families and institutions? Nobody should be pressured into marriage. But if the community loses the infrastructure that facilitates healthy relationship formation, individual freedom becomes isolation by default.

The Wilsons have shown what’s possible. Their intentional matchmaking, their sustained investment in couples’ success, their willingness to leverage their social capital for others’ benefit—this is the model. But celebrity circles can only accommodate so many couples. The question is how to scale this intentionality across the Black professional class.

The answer must be institutional, because only institutions can sustain infrastructure across generations. Individual matchmakers burn out. Informal networks fragment. But institutions—if properly designed and resourced—can maintain systems indefinitely.

What might institutional investment in Black love infrastructure look like?

HBCU Alumni Networks as Matchmaking Ecosystems: Alumni associations in major cities could host quarterly events specifically designed to facilitate connections among young Black professionals. Not awkward singles mixers, but sophisticated networking events, community service projects, cultural experiences where relationships form organically among people with shared backgrounds and values. Success could be measured not just by attendance but by marriages facilitated and families formed.

Black Professional Associations as Relationship Hubs: Organizations for Black lawyers, doctors, engineers, educators, entrepreneurs could recognize relationship facilitation as core to their mission. When successful Black professionals marry, their combined professional power benefits the entire community. These associations could create structured mentorship that pairs young professionals not just for career guidance but for life partnership modeling.

Technology Platforms Designed for Black Love: Dating apps optimize for engagement and superficial attraction. What if technology was designed specifically to facilitate meaningful connections among Black professionals committed to community building? Platforms that prioritize shared values, institutional loyalty, life goals, and cultural understanding over swipe-right dynamics.

Financial Incentives for Family Formation: What if institutions offered tangible support for young Black couples? Grants for couples pursuing marriage counseling. Low-interest loans for home purchases for alumni couples. Scholarships for children of HBCU alumni couples. These investments would pay dividends in institutional loyalty that compounds across generations.

Cultural Campaigns Celebrating Black Love: Media campaigns showcasing successful Black marriages, particularly among professionals committed to community advancement. Not aspirational fantasy but realistic portrayals of how successful couples navigate challenges, support each other’s growth, and invest in institutions. Make Black love visible, aspirational, and achievable.

Research Infrastructure: We lack basic data on what makes Black marriages successful. Which combinations of backgrounds, values, and life circumstances predict long-term partnership success? What interventions effectively support young Black couples through early marriage challenges? Hampton University’s National Center on African American Marriage and Parenting represents a start, but we need comprehensive research infrastructure that can inform evidence-based programming.

The answers won’t come from any single intervention but from a ecosystem of institutional support that makes Black love not just possible but probable. That makes stable marriages not just aspirational but expected. That makes family formation not just personal but communal.

Russell and Ciara Wilson didn’t set out to solve the Black marriage crisis or to transform African American institutional capacity. They’re simply two people who understand the value of healthy relationships and want to share that blessing with their friends.

But their efforts reveal what’s missing and what’s possible. They show that when influential people commit to facilitating connections within Black professional circles, life-changing partnerships form. They demonstrate that intentionality around Black love produces results that individual effort alone cannot achieve. They prove that building strong Black marriages is institution-building at its most fundamental level.

The viral social media pleas asking the Wilsons to expand their matchmaking aren’t just jokes. They reflect a genuine hunger for what the Wilsons provide—thoughtful facilitation of connections among Black professionals who share values and aspirations. They reveal the absence of infrastructure that our grandparents’ generation took for granted because it was built into the fabric of Black community life.

The declining marriage rate among African Americans isn’t inevitable. It’s the result of infrastructure collapse that can be reversed through deliberate institutional investment. The opportunity is to recognize that facilitating Black love isn’t tangential to institutional missions—it’s foundational to building the networks of stable families that will sustain Black institutions for generations.

Seven of the ten states with highest Black marriage rates are HBCU states, which means the foundation still exists. The communities are still present. The institutions still stand. What’s needed is leadership willing to acknowledge that the work of building Black institutional power begins with building Black families. That the work of building Black families requires intentional infrastructure. That the work of building that infrastructure is everyone’s responsibility who claims commitment to Black advancement.

The Wilsons are showing us what’s possible when two people commit to intentionally building Black love within their circles of influence. The question for the rest of us—for institutions, for leaders, for anyone with social capital and community commitment—is whether we’ll do the same within our own spheres. Whether we’ll recognize matchmaking as institution-building. Whether we’ll invest in the infrastructure that makes Black love not just possible but inevitable.

The fire is there. The Wilsons are fanning the flames. The question is whether the rest of us will add fuel until it becomes a blaze that lights the way for generations to come.

Disclaimer: This article was assisted by ClaudeAI.

A single twig breaks, but the bundle of twigs is strong. – Tecumseh

The tradition of giving runs deep in African American communities. From the mutual aid societies formed during enslavement to the church collections that funded the Civil Rights Movement, Black Americans have always understood that our collective survival depends on our willingness to invest in one another. Yet somewhere between necessity and aspiration, we’ve lost the language to teach our children that philanthropy isn’t charity—it’s power.

Teaching African American children ages 5-18 about philanthropy means doing more than dropping coins in a collection plate. It means helping them understand that strategic giving builds the institutions that will protect, educate, and employ them throughout their lives. It means showing them that every dollar they contribute to Black-led organizations is a vote for their own future.

Starting Early: Philanthropy for Elementary Ages (5-10)

Young children understand fairness instinctively. They know when something isn’t right, and they want to help fix it. This natural empathy creates the perfect foundation for introducing philanthropic concepts.

Begin with concrete examples from African American history. Tell them about the Free African Society, founded in 1787 by Richard Allen and Absalom Jones, which provided mutual aid to Black Philadelphians. Explain how enslaved people pooled resources to purchase freedom for family members. These aren’t abstract concepts they’re survival strategies that became institutional frameworks.

Create a family giving jar where children can contribute a portion of their allowance or gift money. Let them research and choose a Black-led organization to support quarterly. This could be a local youth program, a historical preservation society, or an HBCU scholarship fund. The key is giving them agency in the decision-making process. When children see their small contributions combine with others to create meaningful impact, they begin to understand collective power.

Use storytelling to illustrate how institutions are built. Talk about how HBCUs were created because white institutions excluded Black students. Explain how Mary McLeod Bethune started a school with $1.50 and turned it into Bethune-Cookman University. Show them that great institutions often begin with small, consistent contributions from people who understood the long game.

Middle School: Understanding Institutional Building (11-13)

By middle school, children can grasp more sophisticated concepts about how money moves and how power is built. This is when we introduce them to the difference between charity and institutional philanthropy.

Charity addresses immediate needs—feeding the hungry, clothing the poor. Institutional philanthropy builds the structures that create long-term change: schools, hospitals, community development corporations, legal defense funds, policy organizations. Both matter, but only institutional philanthropy shifts power dynamics.

Teach them about the NAACP Legal Defense Fund, established in 1940. Explain how sustained philanthropic support allowed lawyers like Thurgood Marshall to develop the legal strategy that led to Brown v. Board of Education. This wasn’t a one-time donation it was years of investment that transformed American society.

Introduce the concept of endowments and investment income. Too many African American organizations operate in perpetual crisis mode, chasing donations year after year. Show students the difference between an organization with a $100,000 annual budget that must be fundraised every twelve months and an organization with a $2 million endowment generating $80,000 annually in investment income. The second organization can focus on mission instead of survival.

Start a philanthropy club at school or in your community. Let students identify a need in their community and develop a giving circle to address it. They should practice everything: setting fundraising goals, researching organizations, making collective decisions, tracking impact, and understanding how their contributions grow through consistent giving. This hands-on experience transforms abstract concepts into practical skills.

High School: Strategic Power Building (14-18)

High school students are ready to understand philanthropy as a tool for social, economic, and political empowerment. They can analyze power structures and recognize how institutional support or the lack thereof shapes outcomes in Black communities.

Teach them to read institutional budgets and annual reports. Show them how to evaluate whether an organization has sufficient reserves, how much goes to programs versus overhead, and whether they’re building long-term sustainability. This financial literacy is essential for effective philanthropy.

Explore the concept of investment income in depth. Many students don’t realize that major institutions—universities, museums, hospitals—operate primarily on endowment income, not annual fundraising. Harvard’s endowment generated approximately $2.3 billion in investment income in recent years. Imagine if HBCUs collectively had similar resources. Explain that building Black institutional power requires moving beyond the donation mentality to an investment mindset.

Discuss how philanthropy intersects with political power. Show them how think tanks, policy organizations, and advocacy groups are funded. Explain that when Black communities don’t adequately fund our own policy organizations, others define the agenda affecting our lives. The Tea Party movement and its affiliated organizations received hundreds of millions in philanthropic support that reshaped American politics. What might be possible if African American communities invested similarly in organizations advancing our interests?

Examine collective philanthropy models. Traditional philanthropy often centers wealthy donors making large gifts. But collective giving where many people contribute smaller amounts has always been the African American philanthropic model. From church building funds to contemporary giving circles, we’ve understood that our strength lies in numbers. Today’s technology makes collective philanthropy more powerful than ever. A thousand people giving $100 monthly creates $1.2 million annually enough to endow a scholarship, support a community organization, or launch a new initiative.

Encourage students to start giving now, even if it’s $5 monthly to an organization they believe in. The habit matters more than the amount. A teenager who gives $10 monthly from age 16 to 66 contributes $6,000 in direct donations, but if that money is invested and earns average returns, it represents tens of thousands in institutional support.

Teaching African American youth about philanthropy means helping them understand its components and how they work together to build institutional power.

Educational Institutions: HBCUs, independent schools, scholarship funds, and educational support organizations create pathways to opportunity and preserve cultural knowledge. Sustained philanthropic support allows these institutions to build endowments, improve facilities, and attract top faculty and students.

Economic Development: Community development corporations, Black-owned business incubators, affordable housing organizations, and loan funds build wealth and economic stability. These institutions require patient capital and sustained support to create generational impact.

Legal and Policy Organizations: Civil rights organizations, legal defense funds, policy think tanks, and advocacy groups shape the rules that govern society. Inadequate funding in this sector means Black interests remain underrepresented in policy formation.

Cultural Institutions: Museums, historical societies, arts organizations, and media companies preserve our stories and shape narratives. Control over our cultural narrative requires institutional infrastructure that only sustained philanthropy can build.

Health and Social Services: Community health centers, mental health organizations, and social service providers address immediate needs while building the institutional capacity to serve Black communities long-term.

Each component requires different funding strategies. Some need operating support, others need capital for buildings or technology, many need endowment building. Teaching youth to think strategically about where and how they give helps them maximize impact.

The most important lesson we can teach African American children about philanthropy is that it’s not optional it’s essential. Every community that has built institutional power has done so through sustained, strategic philanthropy. Jewish communities support Jewish institutions. Asian American communities support Asian American institutions. African American communities must do the same.

Start conversations early. Make giving a family practice. Teach children to evaluate organizations critically. Help them understand that building Black institutional power is a marathon, not a sprint. Show them that their contributions, combined with others, create the schools, organizations, and institutions that will serve generations to come.

This isn’t about guilt or obligation. It’s about power, self-determination, and legacy. When we teach our children that philanthropy is institution-building, we give them tools to shape their own future rather than waiting for others to determine it for them.

The question isn’t whether African American communities can afford to invest in our institutions. The question is whether we can afford not to.

If you think you’re tops, you won’t do much climbing. — Arnold Glasow

Hip-hop was born out of necessity. A sonic rebellion against poverty, violence, and systemic neglect, it emerged from the Bronx as a raw reflection of life in America’s forgotten corridors. But over the past four decades, it has transformed from cultural resistance into commercial royalty. Once recorded with borrowed turntables in community centers, it now echoes across Super Bowl halftime shows, luxury brand campaigns, and billion-dollar corporate balance sheets. Artists who once stood on corners are now seated at boardroom tables. The culture won. But the community did not.

The statistics tell a story of growth at the top and stagnation at the bottom. Hip-hop is now a $16 billion industry. It has created artists turned entrepreneurs who have expanded into liquor, fashion, tech, and sports. The music dominates global charts, sets fashion trends, and influences everything from algorithms to political campaigns. Yet this immense cultural capital has not translated into economic sovereignty for the African American community. Instead, the concentration of wealth in a few hands has often disguised the lack of institutional power. For all the charts conquered and headlines generated, African American banks, endowments, universities, and asset management firms remain modest, if not endangered.

At the heart of this failure lies a devastating contradiction. While rappers flaunt wealth more publicly than any generation before them, the economic conditions in many African American communities remain dire. The median net worth of Black households, as of 2022, stands at $44,100 compared to $284,310 for White households—a gap that has barely moved in decades. Hip-hop has become the most visible face of African American success, but that visibility is not backed by scale. There are no Black equivalents to BlackRock or Vanguard. No hip-hop-funded HBCU research lab. No Goldman Sachs of rap. Even the highest echelon of Black-owned investment firms manage a fraction of their white counterparts. Vista Equity Partners, the most prominent, oversees $103.8 billion, an extraordinary feat, yet still a rounding error next to BlackRock’s $10.5 trillion.

And even this level of institutional success is an outlier. Most Black-owned investment firms manage less than $10 billion. Most HBCUs have endowments below $50 million. The largest Black bank, OneUnited, holds roughly $650 million in assets, while Bank of America manages over $2.5 trillion. What hip-hop has delivered in influence, it has not delivered in capital. Instead of building institutions, it has made individuals rich. But those individuals exist within a system that continuously siphons wealth away from their communities.

This is not to say that artists bear the blame for economic injustice. But hip-hop has become a tool of seduction as much as expression. Its dominance in the global marketplace has aligned it with the poor man’s logic of capitalism celebrating consumption, rewarding individualism, and elevating spectacle. In this model, buying a Bugatti becomes a symbol of power, while the absence of a Black mutual fund managing $100 billion barely registers. Lyrics obsess over fashion houses like Balenciaga, but rarely name Black-owned real estate firms or venture capital funds. The dream has shifted from ownership of blocks to ownership of Birkin bags.