The function of freedom is to free somebody else. — Toni Morrison

There is a brownstone on a tree-lined block in Prospect Heights, Brooklyn that television once made sacred. Between 1993 and 1998, Living Single gave Black America something it had rarely seen in prime time: six young professionals, rooted in community, living with intention and ambition in one of the most historically Black neighborhoods in the United States. Khadijah James was building a media company. Kyle Barker was moving markets. Maxine Shaw was winning courtrooms. Régine Hunter was shaping aesthetics. Synclaire James was cultivating audiences. Overton Wakefield Jones was holding the physical infrastructure together.

Television, however, being what it is, treated these characters as a collection of charming personalities rather than what they actually were: a fully staffed, vertically integrated holding company waiting to happen. This is the story of what they should have built.

To understand the magnitude of the missed opportunity, one must first inventory the human capital assembled inside that Brooklyn brownstone. Khadijah James ran Flavor magazine as editor, publisher, and chief revenue officer — all without the title or the equity structure to match. She possessed the rarest combination in media: editorial vision and the operational will to execute it. Her Howard University classmate and best friend, Maxine Shaw, was a Howard Law-trained attorney with a litigation record and a strategic mind sharp enough to cut through any corporate structure. Kyle Barker held a Series 7 license and worked on Wall Street at a time when fewer than 3% of stockbrokers in the United States were Black. Régine Hunter was a boutique buyer with a finely calibrated eye for brand, trend, and consumer psychology — skills that today command mid-six-figure salaries in brand strategy and fashion consulting. Synclaire James, often underestimated, possessed the one asset that no business school can manufacture: an authentic connection to an audience. And Overton Jones, the building’s maintenance man, was a master of the physical built environment — a man who could fix, build, assess, and manage real property with technical expertise and institutional loyalty. Six people. Six distinct competencies. One address. The question is not whether they had what it took. The question is why no one ever suggested they combine it.

Flavor Group Holdings would have been organized as a Delaware C-Corporation with six co-founders holding equal equity tranches of 16.67% each at founding, subject to standard four-year vesting schedules with a one-year cliff. The governance structure would have assigned each founder a role corresponding to their demonstrated competency. Khadijah James would serve as Chief Executive Officer and Publisher — the company’s public face, editorial driver, and primary relationship manager with advertisers and distribution partners. Flavor magazine, already generating revenue, becomes the flagship asset and the brand that anchors everything else. Maxine Shaw would hold the role of General Counsel and Chief Legal Officer. Every media company transaction, every real estate deal, every employment contract, every licensing agreement passes through Maxine’s desk. She is not simply the lawyer on retainer — she is the institutional immune system, the person whose job is to ensure the company never gives away more than it receives. Kyle Barker would serve as Chief Financial Officer and Head of Capital Markets — not simply managing the company’s books, but building the capital architecture, structuring debt instruments, managing the investment portfolio, identifying accretive acquisitions, and positioning the company for institutional funding. His Wall Street credentials are the bridge between Khadijah’s vision and the capital required to scale it.

Régine Hunter would become Chief Brand Officer and Head of Consumer Products. She is not a boutique buyer anymore — she is the architect of Flavor Group’s brand extension strategy, governing licensing, merchandising, fashion partnerships, and eventually a Flavor-branded lifestyle vertical that monetizes the audience Khadijah has spent years cultivating. Her later work as a wedding planner reveals a service orientation and event production skill that would translate directly into the company’s live event and experiential revenue line. Synclaire James would serve as Chief Creative Officer and Head of Talent Relations. Her acting background and relational warmth make her uniquely suited to manage the talent ecosystem that a media company depends upon: writers, photographers, contributors, brand ambassadors, and eventually the television personalities that Flavor would feature as its audience expanded. Synclaire is also the company’s institutional memory — the one who ensures that the culture of the organization never loses the warmth that built the audience in the first place. Overton Wakefield Jones would hold the role of Chief Operating Officer and Head of Real Property. This is perhaps the most analytically underappreciated appointment. His role is not merely to fix things — it is to acquire, maintain, and develop the physical infrastructure that gives Flavor Group Holdings its most durable long-term asset base. In 1995, Prospect Heights brownstones were selling for between $150,000 and $250,000, a fraction of the $2 million to $4 million valuations they command today. A systematic acquisition strategy of three to five properties in the immediate vicinity of their original building, executed between 1995 and 2002, would alone represent an unrealized asset base worth between $8 million and $18 million at current market.

Flavor Group Holdings would have operated across three mutually reinforcing business pillars. The first is media and content. Flavor magazine remains the core asset, but the strategy evolves. The magazine is not simply a publication — it is an audience aggregation platform. By 1998, with digital distribution beginning to reshape print media economics, Khadijah and Kyle would have recognized that the magazine’s value lay not in its paper but in its subscriber list, its advertiser relationships, and its brand authority in Black urban culture. A digital transition, executed early, would have positioned Flavor Group as one of the first Black-owned digital media properties at scale — preceding by nearly a decade the consolidation that would eventually hollow out Black print media. Synclaire’s talent relationships would have fueled a podcast network and video content vertical by 2005, and Régine’s consumer product instincts would have monetized the audience through branded partnerships that competitors lacked the cultural credibility to execute.

The second pillar is legal and advisory services. Maxine Shaw’s legal practice does not remain a solo operation — it becomes the institutional anchor of a Flavor Group legal advisory subsidiary focused on serving Black-owned businesses, entertainment clients, and creative professionals. The model here is not unlike what entertainment law firms built around the music and television industries of the 1990s and 2000s. Maxine’s Howard Law network provides the talent pipeline. The brand provides the client pipeline. The business generates revenue independent of the media operation while deepening the company’s institutional relationships across industries. The third pillar is real estate and facilities management. Under Overton’s direction, Flavor Group Properties becomes a systematic accumulator of commercial and residential real estate in gentrifying Brooklyn neighborhoods — Prospect Heights, Crown Heights, Bedford-Stuyvesant. The strategy is not speculative flipping. It is long-hold, income-producing property management that generates the stable cash flow required to fund the more volatile media operation during lean advertising cycles. The 1995-to-2010 window of Brooklyn real estate acquisition represents one of the most dramatic wealth-creation opportunities in modern American urban history. An institution that held even ten properties through that period with leverage appropriate to the cash flows would have emerged with a portfolio worth north of $30 million.

Kyle Barker’s Wall Street experience would have been decisive in assembling the capital stack, and not simply for its technical value. His credibility in institutional financial circles — rare for a Black professional in the mid-1990s — would have opened access to Small Business Administration lending, community development financial institution financing, and eventually the early-stage venture capital that began flowing into minority-owned media businesses following the success of companies like Black Entertainment Television and Essence Communications. A conservative five-year financial projection for Flavor Group Holdings, incorporating magazine advertising revenue of $2.5 million annually, property management income of $400,000 annually from a six-property portfolio, and legal advisory fees of $800,000 annually, would have produced aggregate revenue of approximately $18.5 million between 1995 and 2000. With disciplined reinvestment — consistent with the capital retention philosophy that separates institutional builders from lifestyle operators — that revenue base would have funded a real estate portfolio, a media technology transition, and a legal services expansion that by 2010 would have generated a company valued conservatively at $75 million to $120 million. For context, Essence Communications, a comparable Black women’s magazine brand, was acquired by Time Inc. in 2000 for a reported $170 million. Flavor Group Holdings, with its diversified revenue model and real estate holdings, would have been a more complex and arguably more defensible asset.

Much of the analysis of Black wealth destruction focuses on what was taken. Less attention is paid to what was structurally never built — and therefore never available to be taken or transmitted. A C-Corporation structure with six co-founders and a disciplined shareholder agreement would have accomplished several things that individual success cannot. It would have created a legal entity with perpetual existence, meaning the company survives the death, departure, or London relocation of any single founder. It would have created a mechanism for profit distribution and reinvestment insulated from any individual’s spending behavior. It would have established a board governance structure capable of recruiting outside expertise as the business scaled. And it would have created a transferable asset — something that could be sold, taken public, or bequeathed to the next generation.

Kyle’s decision to accept a job in London and Régine’s eventual departure to marry Dexter Knight are, in the television version of their lives, personal choices with only romantic consequences. In the Flavor Group Holdings scenario, they are governance events — managed by the shareholder agreement, addressed by the board, with equity buyout provisions and employment transition protocols already in place. The institution does not collapse when an individual leaves. That is the entire point of building one.

The argument for taking these characters seriously as institutional builders rather than television archetypes is not merely imaginative — it is instructive. The Living Single cast represented, with remarkable precision, the full professional profile required to build a durable Black enterprise: media, law, finance, brand, talent, and real property. These competencies are not accidental. They are the precise functions that every successful institutional structure requires. The lesson is not that Khadijah James should have been more ambitious. She was, by any measure, already ambitious. The lesson is that ambition without institutional structure dissipates with time, while institutional structure — even modest institutional structure — compounds. The S&P 500 teaches this principle in the financial markets. The same principle governs human capital and organizational design. There is a Flavor Group Holdings waiting to be built in every city where six talented Black professionals happen to share proximity, trust, and complementary skills. The brownstone is not metaphorical. The talent is not hypothetical. The only thing missing is the deliberate choice to convert a social network into an institutional one. Flavor magazine told its readers what was happening in the culture. Flavor Group Holdings would have told the culture what was possible. That is a different kind of editorial mission. And it is long overdue.

Disclaimer: This article was assisted by ClaudeAI.

Land is the only thing in the world that amounts to anything, for it’s the only thing in this world that lasts. It’s the only thing worth workingfor, worth fighting for… – Ted Turner

Raw land is among the oldest and most durable asset classes available to private investors. For the HBCU community — individuals, families, alumni associations, and institutional partners — it is also among the most underutilized.

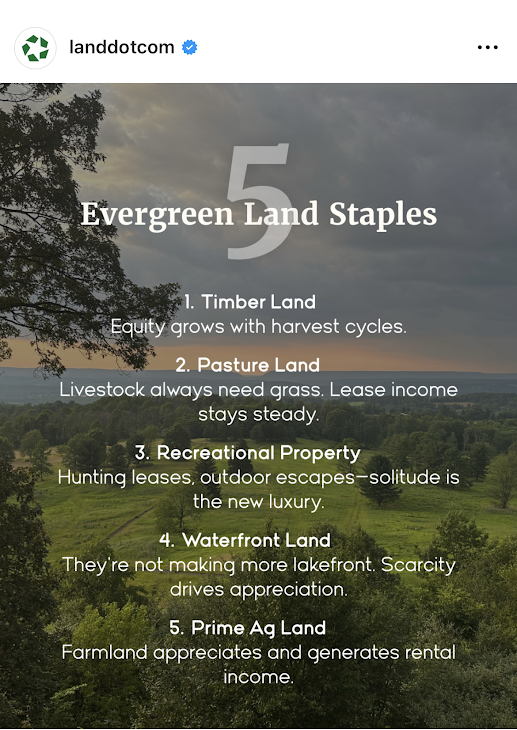

There is a social media post circulating in land investment circles that reads simply: “Forget the luck of the Irish. We prefer the certainty of a deed.” Beneath that caption sits a framework titled “5 Evergreen Land Staples” — timberland, pastureland, recreational property, waterfront land, and prime agricultural ground — each chosen for the same fundamental quality: enduring income or appreciation that does not require the daily volatility management of equities or the tenant fragility of residential real estate. The post is from Land.com, a mainstream marketplace catering primarily to rural landowners. The audience it implicitly addresses is white, rural, and generationally landed. Yet the analytical framework it articulates is precisely what the African American institutional ecosystem needs to operationalize and the HBCU community, with its networks of graduates, alumni chapters, and anchor institutions spread across the American South and beyond, is uniquely positioned to execute it at scale.

The stakes are not trivial. As the Federation of Southern Cooperatives Land Assistance Fund has documented, African Americans own less than 1% of all privately owned rural land in the United States. That figure represents one of the most consequential economic collapses in modern American history, a loss that accelerated across the 20th century through discriminatory lending, heirs’ property dispossession, and the systematic exclusion of Black farmers from federal agricultural credit systems. Between 1910 and 2020, African American land ownership fell by roughly 90%, from an estimated 15–16 million acres to less than 2 million today. Reversing even a fraction of that trajectory requires not only individual decision-making but coordinated institutional action. This article maps a practical framework anchored in the five evergreen land categories for how African Americans at every life stage, and HBCU-affiliated institutions at every organizational level, can begin to build durable land portfolios through structures that keep capital inside the ecosystem.

Before addressing who should invest and how, it is worth establishing why the five categories on that social media post represent genuinely strategic holdings rather than speculative fashions. Timberland is distinctive because its primary asset — standing timber — continues growing in value as long as it stands. As one institutional investor noted at the 2009 Timberland Investment World Summit, timber was the only major asset class not to decline during the Great Recession: “As long as the sun is shining trees will grow and your timber’s value will increase.” For long-horizon investors, which includes endowments, alumni foundations, and family trusts, timberland offers inflation protection, biological growth as a return mechanism, and periodic harvest income that can be timed to liquidity needs. Pastureland generates recurring lease income from ranchers and livestock operators with relatively low management overhead, while the underlying land appreciates over time and the lessee carries operational risk. For a first-generation land investor or a young family with limited bandwidth for active management, a leased pasture parcel generates cash flow from day one. Recreational property, including hunting and fishing grounds, has benefited from the structural shift toward experiential consumption, outdoor recreation spending in the United States now exceeds $780 billion annually and the demand for private access through leased hunting rights or short-term rentals has made rural recreational parcels a viable income source even at modest scale. Waterfront land commands a persistent scarcity premium, as lakefront, riverfront, and coastal parcels face an absolute supply constraint that no amount of construction can remedy, with appreciation rates for quality holdings historically outpacing inland equivalents by substantial margins. Prime agricultural land, the fifth category, combines appreciation and income in proportions that no other asset class consistently replicates, with farmland producing positive real returns in nearly every decade since World War II while the growing global demand for food production adds a structural tailwind that shows no sign of abating.

For the African American individual investor, particularly recent HBCU graduates entering the workforce, raw land is rarely the first investment that financial advisors recommend. Equities, retirement accounts, and residential real estate occupy the conventional hierarchy. This is understandable but strategically incomplete. Raw land, particularly rural parcels in the 10–100 acre range, is far more accessible in price terms than most urban professionals realize. In many parts of the rural South and Midwest, quality pastureland or timberland can be acquired for $1,500–$4,000 per acre, meaning a 20-acre parcel may require a down payment comparable to what urban renters spend in twelve months on housing. The critical discipline for individual investors is to treat the first land acquisition not as a lifestyle purchase but as a strategic asset. A 20-acre timberland parcel generates modest income while the timber matures but builds balance sheet equity that can later be pledged as collateral for subsequent acquisitions, a mechanism that generationally landed families have used for centuries. The key to making this work is choosing land that produces some income immediately, whether through a hunting lease, a hay-cutting arrangement, or a grazing license, so that carrying costs do not exceed cash flow while long-term appreciation accrues. Structurally, individuals should acquire rural land through a single-member LLC rather than in personal name, for both liability protection and eventual transfer efficiency. The LLC structure also allows for the clean addition of family members as equity holders over time, laying the legal groundwork for the next stage of ownership.

A young family with children faces a different calculus than a single investor. The time horizon extends to 30 or 40 years, the need for tax-efficient transfer becomes relevant, and the question of heirs’ property known as the informal, undivided ownership arrangement that has caused the dispossession of millions of acres of Black-owned land must be proactively addressed from the first deed. Heirs’ property arrangements leave undivided interests in land vulnerable to partition sales, through which any one heir can force a sale often to outside buyers at below-market prices. A young family acquiring land today should structure the purchase inside a family LLC or land trust from inception, with a clear operating agreement specifying decision-making rights, buyout provisions, and management authority. This structural discipline costs several hundred dollars in legal fees at formation but eliminates the single greatest mechanism by which Black-owned land has historically been lost. For young families, pastureland and prime agricultural ground are the most suitable of the five categories. Leased to a working farmer on an annual or multi-year cash rent arrangement, these parcels generate predictable income typically $100–$300 per acre annually in productive regions while the family’s equity compounds. Agricultural land near HBCUs, particularly the 1890 land-grant institutions with active extension programs, offers an additional advantage: the university’s agronomic and soil science resources can improve the land’s productivity and rental value over time, particularly where a formal university-farmer partnership exists.

For African American households in the wealth-accumulation or pre-retirement phase, typically those between 45 and 65 with existing equity in residential real estate or retirement accounts, raw land fills a specific portfolio gap. It provides non-correlated returns, inflation protection, and estate planning flexibility that equity-heavy portfolios lack. At this stage, the five-category framework can be pursued more deliberately. Waterfront land and timberland, which require longer holding periods to realize full appreciation, are most appropriate for mature investors who do not need near-term liquidity. A modest timber holding, held for 20 years through a managed investment timberland organization, can produce both periodic harvest income and terminal land value appreciation that substantially outpaces a bond portfolio over the same horizon. Conservation easements on qualifying land parcels offer an additional mechanism: by granting a qualified land trust a permanent easement that restricts development, the landowner receives a federal income tax deduction equal to the value of the development rights surrendered, a tool that high-income African American professionals have underutilized relative to white rural landowners who have deployed it extensively. This is also the stage at which entry into private Real Estate Investment Trust structures becomes viable. A private REIT organized around agricultural or timberland holdings allows a group of accredited investors like friends, family members, or professional associates to pool capital into a formal investment vehicle with a shared land portfolio, professional management, and pass-through tax treatment. Unlike publicly traded REITs, a private land REIT can be sized for a community of 10–50 investors, managed by a professional trustee, and built specifically around the five evergreen categories. The formation cost is meaningful but amortizes quickly across the investor pool, and the structure creates a formal institutional container for what would otherwise remain fragmented individual decisions.

Not every land investment begins with a formal institutional structure. Some of the most durable private wealth in America was built by small groups of trusted individuals such as former college roommates, fraternity and sorority members, professional cohort peers who pooled capital informally before any institution took notice. For the HBCU community, this peer-to-peer investment model is both historically familiar and structurally underdeployed. A group of five former classmates, each contributing $10,000, creates a $50,000 acquisition fund. In rural land markets across the South, that capital is sufficient to purchase 15–30 acres of quality pastureland or recreational property with room for closing costs and an operating reserve. The land is titled inside a jointly owned LLC, the operating agreement governs decision-making and buyout rights, and the group begins building a shared balance sheet that none of them could have assembled individually on the same timeline. The social infrastructure already exists. HBCU alumni networks are among the most tight-knit in American higher education, and the bonds forged between classmates across Greek organizations, residence halls, student government, and athletic programs carry the relational trust that small investment partnerships require above all else. What is missing is not the social capital but the financial framework to convert it into land equity. The practical steps are straightforward: the group agrees on an investment policy covering land category, geographic focus, minimum hold period, and income distribution schedule; forms an LLC with an operating agreement drafted by a real estate attorney; designates a managing member responsible for vendor relationships, lease management, and annual reporting; and commits to a first acquisition within a defined timeframe, preventing the initiative from dissolving into indefinite planning. Over time, these peer land partnerships can grow through reinvested income, additional capital calls, and the addition of new members at formally appraised entry valuations. A group that begins with five classmates and 25 acres can, within a decade of disciplined reinvestment, hold a diversified portfolio spanning multiple land categories across several states anchored not by institutional mandate but by the simple decision of like-minded people to build something together.

HBCU alumni associations sit at the intersection of institutional loyalty and latent investment capital. Most chapters hold reserve funds that have been accumulated through dues, fundraising, and event revenue that are parked in bank accounts earning negligible interest. Very few chapters have formalized investment policies, and this represents one of the most tractable missed opportunities in the HBCU ecosystem. An alumni chapter with $200,000 in reserves can, with proper legal structuring, become a founding limited partner in a private land REIT or a land investment LLC alongside other chapters. Five chapters pooling $200,000 each creates a $1 million acquisition fund capable of purchasing 250–500 acres of quality pastureland, timberland, or agricultural ground in rural markets adjacent to HBCUs. That land, leased and managed professionally, generates annual income that returns to the chapters while the underlying asset appreciates. Over a 15-year horizon, the portfolio can be refinanced to fund new acquisitions replicating the leverage cycle that institutional endowments have used with alternative assets for decades. The governance structure matters enormously. An alumni land partnership should be organized as a limited partnership or private REIT with an independent general partner or trustee, clear investment policy statements, annual audited financial statements, and a defined liquidity event horizon. The informality that characterizes most alumni chapter finances is incompatible with institutional land ownership at scale. But with proper structuring, the alumni network becomes what it has always had the potential to be: a distributed institutional investor class with shared objectives and collective bargaining power. Nationally coordinated alumni associations, the general alumni bodies of the major HBCU systems, are positioned to act at an even larger scale. A national alumni association with 50,000 dues-paying members and a modest per-member investment program could capitalize a seven-figure land acquisition fund within a single fiscal year. Structured as a private REIT with a land-grant mission overlay, specifically acquiring land adjacent to 1890 HBCU campuses or in counties with high concentrations of African American agricultural heritage, such a fund would generate financial returns while simultaneously reinforcing the geographic and economic footprint of the institutions themselves.

The structure of land acquisition matters as much as the acquisition itself, and for the African American investor at every level — individual, family, peer partnership, or alumni association — the financing institution is a strategic choice, not merely a transactional convenience. African American-owned banks hold just $6.4 billion in assets, while African American credit unions hold $8.2 billion, meaning these institutions together control less than $15 billion in combined lending capacity despite serving a market of more than 40 million people — insufficient to exert meaningful influence in national credit markets without deliberate capital infusion from within the community itself. When an African American investor finances a land purchase through a Black-owned bank or credit union rather than a mainstream white-owned lender, the mortgage deposit strengthens that institution’s liquidity ratio, expands its lending capacity through fractional reserve multiplication, and keeps the interest income circulating within the ecosystem rather than exiting to a Wall Street balance sheet. Every dollar deposited into an African American financial institution can translate into multiples of additional lending capacity once multiplied through the banking system — meaning that the collective financing decisions of HBCU alumni and community investors are not merely personal financial choices but acts of institutional capitalization. A community that builds land equity through Black-owned financial institutions simultaneously strengthens two pillars of its economic architecture: the land base that generates long-term wealth and the banking infrastructure that finances the next generation of acquisition.

At the institutional tier, the strategic imperative is even more pronounced. As of 2014, Tuskegee University controlled approximately 5,000 acres, ranking 12th among all American colleges in total land holdings, while Alabama A&M (2,300 acres), Alcorn State (1,756 acres), Prairie View A&M (1,502 acres), Kentucky State (915 acres), and Southern University (884 acres) collectively controlled more than 12,000 acres, placing all six among the top 100 college landowners in the United States. Those figures have not been comprehensively updated in the intervening decade, and the actual current land position of these institutions accounting for acquisitions, dispositions, and reclassifications likely differs. What has not changed is the strategic imperative to treat that land base as a productive investment asset rather than passive institutional real estate. A coordinated commitment of $1 million from each of the nineteen 1890 land-grant HBCUs would create a $19 million revolving fund capable, through its placement in African American banks and credit unions, of generating $7–$10 in agricultural lending capacity for every dollar committed financing not just land acquisition but the full productive cycle of African American farming. That mechanism addresses credit access. The complementary challenge is equity accumulation: deploying HBCU endowment capital, alongside alumni and friends’ capital, into the five evergreen land categories through a structured private REIT. An HBCU-anchored land REIT, capitalized with institutional endowment commitments as the senior tranche and alumni association and individual investor capital as subordinate tranches, would create a properly tiered investment structure with aligned incentives. The endowment’s priority return on its senior capital is protected; alumni investors participate in the upside above that hurdle; and the land itself remains in community-aligned ownership regardless of which investor class holds primacy at any given moment. Over time, the REIT’s land holdings can be diversified across all five evergreen categories — timberland for long-horizon appreciation, pastureland and agricultural ground for current income, waterfront parcels for high-appreciation positioning, and recreational property for near-term income generation — creating a portfolio whose income streams are non-correlated and whose asset values compound independently of equity market cycles.

The five evergreen land categories are individually sound investment ideas. Their strategic power for the HBCU community, however, lies not in isolated individual transactions but in the construction of a layered, coordinated ecosystem from the 22-year-old HBCU graduate purchasing her first 20-acre pasture parcel in Alabama, to the alumni chapter launching a multi-state agricultural REIT, to the 1890 HBCUs deploying endowment capital as the institutional anchor of a Black-managed timberland fund. At the most fundamental level, virtually every economic system man has ever created relies on one undeniable truth: whoever controls the land controls the system. The African American institutional ecosystem has the networks, the talent, and increasingly the structured financial vehicles to re-enter land ownership at meaningful scale. What it requires now is the strategic coordination to treat land not as a nostalgic aspiration but as a compounding institutional asset — one deed, one acre, one fund at a time.

Disclaimer: This article was assisted by ClaudeAI.

“The most important investment you can make is in yourself.” – Warren Buffett

There is a financial contradiction embedded in the romantic lives of African Americans that most personal finance commentators decline to address directly, because addressing it directly is uncomfortable. The contradiction is this: African Americans, as a group, occupy the most economically precarious position of any major demographic in the United States, which makes the cost of courtship a genuine strategic burden — and yet marriage, and the household formation it produces, remains one of the most powerful wealth-building mechanisms available to individuals operating without inherited capital. African Americans cannot afford to date the way the broader culture has normalized dating. And they cannot afford not to.

This is not a romantic observation. It is an institutional and economic one, and it deserves to be examined as such.

The arithmetic is brutal when you sit with it. According to a February 2025 survey by BMO Financial Group, the average American adult spends $2,279 on dates per year, with the all-in cost of a single date from pre-date grooming to gas money estimated at nearly $168. At one date per week, that annualized figure climbs well past $8,700. Set that against an African American median household income that, per the most recent Census data, sits at roughly $52,000 — still last among all major ethnic groups — and courtship is consuming somewhere in the range of 16 to 17 percent of African American median income. No other major demographic group faces that proportional burden. The cumulative cost is not simply personal; it is communal, because money extracted from the African American household through consumption-oriented dating is money that does not compound, does not build equity, and does not circulate within Black institutional ecosystems.

The crisis is compounded by employment fragility. African American men between the ages of 20 and 24 have historically carried unemployment rates roughly double those of their white male peers and these are the years during which romantic partnerships form with the most frequency and social intensity, and also the years of maximum economic vulnerability for the demographic most burdened by the cultural expectation of financing courtship. The collision of maximum relational pressure and minimum economic stability is not accidental. It is structural, and the consequences of navigating it poorly leading to the accumulating debt in pursuit of performed affluence, or deferring the relational investments that ultimately build household wealth reverberate for decades.

What is rarely said plainly enough is that courtship itself, when conducted without financial discipline, functions as a form of capital extraction. Every dollar spent performing prosperity in a relationship like the unnecessary dinner, the performative gift, the vacation financed on credit is a dollar transferred out of a community already operating with the thinnest capital base in the country. The African American community has constructed, over generations, a rich institutional infrastructure: HBCUs, Black-owned financial institutions, fraternities and sororities, professional associations, religious organizations, and community development organizations. The health of that infrastructure depends, at its foundation, on the accumulation of wealth within African American households. Romance, conducted poorly, undermines that foundation directly.

And yet the opposite error of treating financial precarity as a reason to defer relational commitment indefinitely is equally destructive, and arguably more so at the institutional level. Marriage, sociologists have long established, is not merely a romantic arrangement. It is the primary non-institutional mechanism through which ordinary Americans build wealth. The two-income household produces compounding effects on savings capacity that single-income households simply cannot replicate. The married couple that directs dual incomes toward an investment portfolio, a property, a business capitalization, or a child’s education produces generational effects that individual accumulation, however disciplined, rarely matches. Economists studying the racial wealth gap have identified the marriage rate differential between African Americans and other groups as one of the structural contributors to the persistence of that gap not because marriage is morally superior to other arrangements, but because household formation is a capital formation mechanism, and lower rates of stable household formation mean lower rates of capital accumulation across the community.

The data on African American marriage rates is now well established. Black Americans marry at lower rates than any other major demographic group in the country, and those who do marry do so later. The causes are multiple and structural with high male incarceration rates, chronic unemployment disparities, elevated student debt burdens concentrated among Black women who have simultaneously outpaced Black men in educational attainment but the consequences operate as a compounding disadvantage. Every generation that forms fewer stable households is a generation that produces less transferable wealth. Every household that dissolves under financial stress and financial incompatibility remains among the most commonly cited causes of relationship dissolution is a household that fails to produce the institutional legacy it might have otherwise built.

The tension, then, is genuinely bilateral. Dating as currently practiced by too many African Americans is financially unsustainable and institutionally corrosive. But the instinct to disengage from romantic partnership altogether, whether from economic discouragement or cultural frustration, forfeits the most accessible wealth-building mechanism available to people without inherited capital. The resolution of this tension is not a lifestyle choice. It is a strategic discipline.

What that discipline requires, practically, begins with a fundamental reorientation of what courtship is for. In the broader American consumer culture, dating has been commodified into a performance, a sequential escalation of expenditure designed to signal value, demonstrate seriousness, and compete for desirability. That model was designed for, and is subsidized by, demographics with higher income floors and different capital structures. African Americans who adopt it wholesale are importing a financial logic that was never calibrated for their economic reality. The more productive frame is to understand courtship as what it has always been, beneath the cultural noise: an evaluation of partnership potential. The question that dating should answer is not who can perform affluence most convincingly but who can build alongside you most effectively.

The previous guidance this publication offered to HBCU men to be honest about your finances, maintain an emergency fund scaled to the specific vulnerability of African American employment, set expectations within a budget rather than beyond it, and resist the conflation of income with wealth remains sound, but it is incomplete if read only as personal financial advice. Its deeper implication is institutional. The man or woman who enters a serious relationship without financial honesty, without emergency reserves, and without a clear orientation toward asset accumulation is not simply making a personal error. They are entering a partnership that is structurally likely to fail under economic stress, and the failure of that partnership will remove another household from the African American wealth-building ecosystem. The stakes are communal, not merely personal.

The same logic applies to partner selection. This is a dimension of the conversation that cultural politeness often forecloses, but institutional analysis cannot afford to ignore. The choice of a romantic partner is, among other things, a capital allocation decision. A partnership between two individuals who are aligned on financial values, who are both oriented toward asset accumulation rather than consumption performance, and who are capable of the financial transparency that stable households require, produces outcomes that misaligned partnerships simply do not. The HBCU graduate who selects a partner based on emotional chemistry while ignoring or minimizing financial incompatibility is not being romantic they are being strategically imprecise about one of the most consequential decisions they will make. Given the compounding nature of household economics, imprecision here has long time horizons.

This is not an argument for mercenary partnership or the subordination of genuine affection to spreadsheet optimization. It is an argument that the dichotomy between romance and financial strategy is false, and that maintaining it as if it were real is a luxury African Americans, as a community, cannot afford. Other communities have understood for generations that courtship and institutional continuity are related phenomena. The institution of marriage among Jewish American families, which social scientists have identified as one of the structural contributors to that community’s remarkable intergenerational wealth transfer, is not simply an artifact of religious tradition. It is reinforced by a dense network of institutional expectations, community norms, and financial literacy frameworks that treat household formation as a community-level priority rather than a purely private one. The same patterns, in different cultural registers, appear in other communities that have achieved disproportionate wealth accumulation relative to their initial American circumstances.

African American institutions such as HBCUs, fraternities, sororities, religious organizations, professional associations have the capacity to play this coordinating role. The HBCU campus, which has historically served not merely as an educational institution but as a marriage market and professional network, is an underutilized asset in this regard. When two HBCU graduates form a household, they are not just creating a family. They are activating a set of institutional networks, alumni relationships, professional associations, and community commitments that have real capital value. When that household builds wealth, and directs that wealth through Black-owned financial institutions, invests in Black-owned enterprises, and contributes to HBCU endowments, it completes a capital circulation loop that strengthens the entire ecosystem. The household is not the end of the story. It is the seed of a much larger institutional project.

But the institutional infrastructure currently available to support that project is insufficient to the scale of the problem. Providing personal finance guidance to individual graduates, or hosting mixers within existing alumni networks, addresses symptoms rather than causes. What is actually required are new institutions purpose-built to treat relationship formation and household financial stability as interconnected civic priorities and the African American community is now beginning to conceptualize what those institutions might look like.

One framework that has emerged from this conceptual work is the proposed Ossie Davis and Ruby Dee Trust, a nonprofit structure designed to treat Black relationship formation as essential civic infrastructure. Rather than addressing individual behavior, it embeds an Institutional Matchmaking Network inside existing Black institutions such as HBCUs, Black Greek-letter organizations, and Black professional societies organizing participants into cohorts around values alignment and life stage rather than the transactional logic of dating apps. Institutional partners would be evaluated not by attendance but by households formed over time. Alongside this, the Trust’s proposed Black Marriage Economic Stabilization Fund directly attacks the structural barriers to marriage formation: student loan interest relief for married participants, down payment matching grants, emergency household stabilization funds, and cooperative legal planning tools. If society subsidizes corporate capitalization through tax structures and preferential credit, there is no principled argument against subsidizing household formation among the demographic most systematically denied access to those same structures.

A second emerging framework addresses what enters the household economically at the moment of formation. The proposed HBCU Alumni Trust would provide every HBCU graduate, at graduation, with a beneficial interest in a professionally managed irrevocable trust generating monthly income distributions for life, with 75 percent accessible and 25 percent mandatorily reinvested, and underlying assets protected by spendthrift provisions for a ten-year vesting period. Its purpose is not primarily about returns. It is about changing the conditions under which graduates enter the courtship market. A graduate carrying a monthly income stream is a categorically different actor than one entering post-graduation life with $40,000 in student debt and no liquidity buffer less likely to perform prosperity they do not possess, less likely to make partnership decisions driven by economic desperation, and more likely to be the kind of financially stable partner around whom a wealth-building household can actually be built.

The version of dating that is making African Americans broke, therefore, is not simply an individual failure of financial discipline. It is a community failure to have built and sustained the normative frameworks, the matchmaking infrastructure, and the financial tools within which courtship is understood as institutional preparation rather than consumption performance. Young African Americans inherit a culture of dating that was not designed with their economic realities or institutional interests in mind. The Ossie Davis and Ruby Dee Trust, the HBCU Alumni Trust, and the broader institutional imagination they represent are attempts to change that inheritance not through cultural policing or moral instruction, but through the construction of institutions that make the financially disciplined, partnership-oriented approach to courtship the path of least resistance rather than the path of greatest sacrifice.

The calculation, ultimately, is not whether African Americans can afford to date. They can, if they do it with discipline, honesty, and a clear-eyed understanding of what partnership is for. The calculation is whether African Americans can afford to continue treating courtship as a consumption category rather than a capital formation strategy and whether the institutions that serve African American life are willing to accept responsibility for building the infrastructure that makes the difference. The evidence of seven decades of compounding wealth gaps suggests, emphatically, that they cannot afford the former. The emergence of institutional frameworks designed to address the structural conditions of Black household formation suggests, cautiously, that some are beginning to accept the latter.

Disclaimer: This article was assisted by Claude AI.

When you can do the common things of life in an uncommon way, you will command the attention of the world. – George Washington Carver

In Washington, the phrase “support for HBCUs” has become one of the most reliable applause lines in American political life. Presidents invoke it. Appropriations committees cite it. Press releases are issued, summits are convened, and photographs are taken with smiling institutional presidents. And then, year after year, the National Center for Science and Engineering Statistics releases the Higher Education Research and Development (HERD) Survey, the most comprehensive longitudinal dataset tracking university research investment in the United States, and the applause gives way to the same uncomfortable arithmetic.

In FY 2024, 59 HBCUs and affiliated institutions spent a combined $929.2 million on research and development. That is a large number in isolation. It is a devastating number in context. The total national higher education R&D enterprise that same year amounted to $117.7 billion. HBCUs accounted for 0.79% of it which is less than eight-tenths of one percent of the nation’s research investment, for institutions that produce a disproportionate share of Black STEM graduates, pre-medical students, and humanities scholars. The gap between what this figure is and what it should be is not a rounding error. It is a policy failure of the first order. But before laying the entirety of that failure at Washington’s feet, it is worth asking a harder question: how much of it is also self-inflicted?

What is worse than the current number is the trajectory. In 2015, the HBCU share of national R&D stood at 0.82%. In 2024, it stands at 0.79%. Ten years, three presidencies, dozens of executive orders, and multiple congressional funding packages later, the needle has moved — backward. The absolute dollar figures have grown, from $565.8 million in 2015 to $929.2 million in 2024, an increase of roughly 64% over the decade. But that growth is illusory when measured against the expansion of the national enterprise itself. The entire higher education R&D sector grew from $68.7 billion to $117.7 billion over the same period, an increase of 71%. HBCUs did not keep pace. They ran, and the field ran faster.

This is not a partisan observation. The data is indifferent to party affiliation. Under the Obama administration in FY 2015, HBCUs held a 0.82% share. By FY 2016, Obama’s final full year, it had slipped to 0.80%. Under the first Trump administration, the share fell steadily from 0.75% in 2017 to a decade-low of 0.63% in 2020. The Biden era produced the strongest absolute growth — $929 million in 2024 against $542 million in 2020 — but even at its peak, the Biden era only recovered the share to 0.79%, still below the Obama-era baseline. No administration has treated parity as a governing imperative. No Congress has appropriated at the scale the problem requires.

The HERD data makes the scale of the problem legible in a way that press releases cannot obscure. To reach just 1% of national R&D investment, a number that is not ambitious but merely honest, given that HBCUs serve a population roughly 15% of the total undergraduate student body, annual HBCU research expenditures would need to reach $1.18 billion, a gap of $248 million from current levels. To reach 2%, still proportionally below HBCU enrollment weight, the number is $2.35 billion, a gap of more than $1.4 billion annually. At 5%, which is arguably the minimum threshold for serious institutional research competitiveness, the annual requirement rises to $5.89 billion. These are not fantastical projections. They are the arithmetic of what it costs to matter in the modern knowledge economy.

There is one additional data point that every HBCU president, board member, alumni association chair, and development officer should be required to sit with before any other conversation about strategy begins. In FY 2024, 39 individual PWIs each spent more on research and development than all 59 HBCUs combined. Not more per institution. More in total more than $929 million apiece, individually, at 39 separate universities, while the entire organized HBCU sector could not collectively match what any one of them spent alone. Johns Hopkins, the perennial top-ranked research university, spent $4.1 billion on R&D in FY 2024, an amount more than four times the combined output of every HBCU in the country. But Johns Hopkins is not the only comparison that should give pause. The University of Pennsylvania spent $2.2 billion, an amount more than twice the entire HBCU sector. The University of California San Francisco spent $2.1 billion. The University of Michigan spent $2.1 billion. The University of Wisconsin-Madison spent $1.9 billion. These are not the top five institutions in the country by research output simply because they are wealthier or more selective than HBCUs in some abstract sense. They are the top five because they decided, at an institutional level, that research was the primary mechanism through which a university generates long-term power — economic, political, and reputational — and they built accordingly. Each of those five institutions, on its own, individually outspends every HBCU in America combined by a factor of two or more. Ohio State. Texas A&M. These are not exotic outliers. Several of them are state universities with public missions not fundamentally dissimilar from many HBCUs. The difference is not that their researchers are more talented or their communities more deserving. The difference is that somewhere in their institutional histories, research became the mission not a supplement to it. That reorientation produced decades of compounding returns. HBCUs are still debating whether to begin.

The external funding gap is real. But it exists alongside and is partly enabled by a pattern of institutional self-neglect that the HBCU sector has been reluctant to examine with full candor. Too many HBCU administrations, particularly those overseeing graduate programs, have treated research not as a strategic priority but as a grant-chasing appendage: a necessary line item for federal reporting, a credential for accreditation purposes, something the provost manages while the president attends to enrollment and donor relations. The result is an institutional culture in which research infrastructure is perpetually undercapitalized, grant offices are understaffed, and the graduate school — the engine of every serious research university — is treated as a placeholder for undergraduates (the bulk of most HBCU graduate schools are their own undergraduates) rather than the economic generator it is designed to be. This is not an abstraction. It shows up directly in the HERD rankings.

Howard University, the flagship of HBCU research activity, spent $101.8 million in FY 2024, ranking 178th nationally. North Carolina A&T, which has made the most deliberate institutional bet on STEM research, spent $81.8 million and ranked 192nd. Morehouse School of Medicine spent $68.7 million and ranked 212th. Florida A&M spent $68.7 million and ranked 213th. These are the top tier four institutions spending a combined $321 million out of the sector’s $929 million total. The other 55 institutions divided the remaining $608 million, an average of just $11 million each. And that average flatters the distribution considerably. Grambling State University, one of the most storied names in HBCU history, spent $486,000 in FY 2024, ranked 811th nationally, in the 13th percentile. Shaw University spent $452,000. Coppin State spent $304,000. Mississippi Valley State spent $161,000. Jarvis Christian College spent $150,000. These are institutions with graduate programs, loyal alumni networks, and deep community roots. The research numbers they are producing are not the result of limited potential. They are the result of limited prioritization. There is a meaningful distinction between the two, and the sector has been too comfortable blurring it.

The comparison with peer land-grant and regional public universities is instructive and uncomfortable. A regional public university with comparable enrollment to Morgan State or Tennessee State will typically have a dedicated technology transfer office, a research commercialization incubator, multiple endowed research chairs, and a graduate school that is explicitly linked to the institution’s strategic revenue plan. These are not luxuries at those institutions. They are understood as core infrastructure. At too many HBCUs, they remain aspirational bullet points in strategic plans that are never fully funded.

The institutional neglect of research infrastructure does not exist in a vacuum. It is reinforced and in many ways perpetuated by a philanthropic culture among HBCU alumni that directs dollars toward the visible and the sentimental rather than the strategic. Ask an HBCU alumni association what its fundraising priorities are, and the answers are predictable: scholarships, athletics, the marching band, campus beautification, the homecoming experience. These are not illegitimate priorities. Scholarships keep students enrolled. A great homecoming is an institutional identity statement. But they are not the investments that build research universities, and the gap between where HBCU alumni philanthropy flows and where HBCU research infrastructure requires investment is one of the most consequential misalignments in Black institutional life.

The problem is structural and informational. HBCU alumni, by and large, do not know what their institutions’ research portfolios look like. They do not know that their alma mater ranks in the 13th percentile of national research expenditures. They do not know that the graduate school is operating without a dedicated technology licensing office. They have never been presented with a case for why endowing a research chair in computational biology or environmental science would generate more long-term institutional value than another scholarship fund. No one has made that case to them, because the institutions themselves have not fully internalized it. PWI alumni are regularly presented with precisely this framing. Major research universities run sophisticated campaigns explaining to their donor bases that an endowed professorship creates a permanent research income stream, that a gift to a technology commercialization fund can generate licensing revenue that multiplies the original gift, that an investment in graduate fellowships attracts research talent that then generates grant overhead that funds the next generation of infrastructure. The cause-and-effect chain from donation to institutional research capacity to economic output is laid out explicitly. HBCU development offices have, with notable exceptions, not made this case. The result is that HBCU alumni who are themselves scientists, engineers, physicians, and entrepreneurs give generously to scholarships while their institutions’ research infrastructure atrophies. They are loyal donors funding an incomplete vision of what their institutions could be.

The competitive gap is widening not only in research expenditure but in the commercialization infrastructure that converts research into institutional wealth and nowhere is that gap more nakedly visible than in patent production. The National Academy of Inventors publishes an annual ranking of U.S. universities by utility patents granted. In 2024, the University of California system led the country with 540 patents. MIT produced 295. The University of Texas system produced 234. Purdue produced 213. Stanford produced 199. Not one HBCU appears anywhere in the top 100. Not Howard. Not NC A&T. Not Florida A&M. The list runs to 100 institutions and ends with universities holding 14 patents each. HBCUs could not place a single institution on it. This is not incidental. It is the downstream consequence of four and a half decades of abdication from the commercialization economy that the Bayh-Dole Act of 1980 made available to every research university in America. That legislation gave universities ownership of discoveries made with federal research funding — a structural gift that created the legal architecture for technology licensing offices, spinoff companies, and the university-based venture ecosystem that now anchors the innovation economies of entire regions. MIT’s technology licensing office has generated billions in cumulative revenue and been instrumental in creating hundreds of companies. Stanford’s equivalent has returned substantial royalty income to its operating budget and endowment for decades. The institutions that built aggressive commercialization infrastructure around Bayh-Dole are now compounding institutional wealth at a rate that has nothing to do with tuition receipts or annual federal appropriations. HBCUs have largely been bystanders to this transformation for forty-five years. Every year that an HBCU produces federally funded research without a pipeline for commercializing it is a year in which intellectual property that legally belongs to the institution is effectively abandoned. The patents are not filed. The licensing agreements are not negotiated. The spinoff companies are not formed. The wealth that research can generate, wealth that is independent of enrollment cycles, tuition sensitivity, and federal political winds is left on the table. When a major technology company funds a research center at MIT or Carnegie Mellon, it is making an investment in an ecosystem that has already demonstrated the capacity to convert that investment into commercially viable output. That ecosystem produced Google. It produced Genentech. It produced the foundational patents behind industries that did not exist a generation ago. The question for HBCUs is not how to be invited into that ecosystem. Invitation is not the goal, and dependence on the goodwill of institutions that have never prioritized Black wealth creation is not a strategy. The goal is to build a parallel ecosystem; one anchored in HBCU research infrastructure, capitalized through the African diaspora, and oriented toward producing the companies, the patents, and the intellectual property that generate Black institutional wealth on a generational time horizon. The African American community has spending power measured in the trillions. The African continent represents one of the fastest-growing concentrations of capital and technological ambition in the world. The Caribbean and broader diaspora hold resources, networks, and markets that no MIT spinoff has been designed to serve. An HBCU-anchored research commercialization ecosystem, built in genuine partnership with diaspora capital rather than in perpetual petition to federal appropriators, is the architecture through which an African American-owned Google becomes imaginable not as aspiration, but as institutional output. Stanford did not produce Google because it got lucky. It produced Google because it had spent decades building the research infrastructure, the technology transfer capacity, the graduate talent pipelines, and the investor relationships that made commercializable discovery an institutional inevitability rather than an accident. HBCUs have the community. They have the talent. They have, in the diaspora, a potential capital base that dwarfs what most research universities could claim at the moment they began building. What they have not yet built is the infrastructure that converts all of that latent capacity into compounding institutional power. That is the work. And it cannot begin until the sector decides that research is not an afterthought it is the foundation.

None of that ecosystem can be built, however, if the students arriving at HBCU research programs have spent their entire academic formation inside institutions that treated STEM as an afterthought. The research university does not begin at the graduate school. It begins at the pipeline that feeds it. The elite PWI research institutions that dominate the HERD rankings and the NAI patent list are not drawing their graduate talent from underfunded schools with overextended teachers and no competition culture. They are drawing from Phillips Exeter, Phillips Andover, and the constellation of elite preparatory institutions that have spent generations building exactly the kind of STEM competition infrastructure (doctoral-level coaches, state-of-the-art laboratories, national Olympiad pipelines) that produces the researchers who then generate the patents and the companies. The African American community once had more than 100 Black boarding schools. Four remain. The collapse of that infrastructure is not unrelated to the HERD data. It is part of the same story. Rebuilding a network of elite Black private day schools and boarding schools institutions explicitly designed as STEM pipelines into HBCUs and from HBCUs into the research economy is not a separate conversation from the one this article is having. It is the upstream chapter of it. An HBCU research ecosystem capable of producing commercially viable intellectual property requires a feeder system that has been preparing Black students for that level of scientific culture since before they arrive on campus. The Eight Schools Association does not produce Intel Science Fair winners by accident. Neither will HBCUs produce the next generation of research scientists, patent-holders, and technology entrepreneurs without building the institutional infrastructure that makes that outcome systematic rather than exceptional.

The deepest problem, however, is one that no federal grant program and no alumni campaign can solve on its own. It is a problem of institutional identity. Research at most HBCUs is understood as the work of a specific class of people: faculty with PhDs, graduate students, grant administrators. It is not understood as the work of the institution. This is a fundamentally impoverished conception of what a research university is, and it has real consequences for both the quantity and the quality of what gets produced. The most research-intensive universities in the world do not operate this way. At institutions where research is genuinely central to the mission, the orientation pervades the entire organization. The facilities management team understands that their work maintains the physical infrastructure on which research depends. Procurement staff understand that how they manage equipment acquisition and vendor relationships affects the cost-efficiency of the research enterprise. The administrative staff in grant offices understand themselves as investigators’ partners, not their compliance monitors. The groundskeepers and custodial staff who maintain the physical environment of laboratories and research spaces are part of an institution that takes seriously what happens inside those spaces. This is not sentimentality. It is operational culture. And it is the difference between institutions that treat research as a revenue center and those that treat it as a credential.

For HBCUs, the argument for this kind of whole-institution research identity is not merely operational. It is strategic and historical. The communities that HBCUs were built to serve have profound, unmet research needs: in environmental health, in medical outcomes, in economic development, in urban infrastructure, in food systems, in financial services. The proximity of HBCUs to those communities — geographic, cultural, institutional — is itself a competitive research advantage that no PWI can fully replicate. Community-engaged research, participatory research models, place-based longitudinal studies of Black American communities — these are areas in which HBCUs have natural authority. But capitalizing on that authority requires treating research as a whole-institution commitment, not a departmental function. It means building research literacy across every level of the institution. It means having honest conversations, from the boardroom to the grounds crew, about what research is, why it matters, and what the institution loses every year it is treated as secondary. Not because every employee will write a journal article, but because institutional culture is built through shared understanding of institutional purpose. When everyone connected to a campus understands that its long-term capacity to serve its community is tied to its research productivity, the institution begins to function differently. Budget priorities shift. Hiring decisions reflect research capacity. Alumni giving conversations expand beyond the sentimental to the strategic.

The institutions already gaining ground demonstrate the model. Morgan State’s growth from $13.6 million in 2015 to $55.5 million in 2024 — a 309% increase — did not come from waiting on Washington. It came from deciding that research was a strategic priority and building the administrative infrastructure to compete for it. Winston-Salem State’s 840% growth over the same period came from targeting federal health research dollars with institutional precision. Delaware State nearly tripled its portfolio. These trajectories prove the capacity exists.

There are also signs that the sector is beginning to grasp the coordination imperative. On April 29, 2026, fifteen HBCUs announced the formation of the Association of HBCU Research Institutions (AHRI), a national coalition explicitly designed to accelerate research capacity, increase the number of HBCUs achieving R1 Carnegie Classification, and expand collective policy influence. The founding membership includes Howard, the sector’s only R1 institution, alongside thirteen R2 institutions: Clark Atlanta, Delaware State, Florida A&M, Hampton, Jackson State, Morgan State, NC A&T, Prairie View A&M, South Carolina State, Southern University, Tennessee State, Texas Southern, and Virginia State. Collectively, AHRI’s members account for roughly half of all competitively awarded federal research funding among HBCUs. The coalition is co-located with the Association of American Universities and has secured a three-year, $1 million grant from Harvard’s Legacy of Slavery initiative, with Harvard’s Office of the Vice Provost for Research providing technical assistance. The formation of AHRI is the most substantive structural move the HBCU research sector has made in a generation, and it deserves to be recognized as such. But one million dollars over three years, measured against a sector-wide research gap of hundreds of millions annually and a patent economy in which HBCUs hold zero of the top 100 positions, is a foundation, not a solution. The significance of AHRI is not the capital it has raised. It is the architecture it represents — fifteen institutions deciding that isolation is no longer a viable strategy. If that architecture is built upon seriously, capitalized at the scale the HERD data demands, and extended to the 44 HBCU/PBI institutions not yet in the coalition, it becomes the organizational infrastructure through which the ecosystem this article has described can actually be constructed. If it becomes another announcement without a follow-through funding strategy, the HERD Survey will record the same story in 2034 that it has recorded every year since 2015.

But the formation of AHRI also demands a harder question that the coalition’s announcement did not address: how much genuine institutional autonomy do its member institutions actually have? Research strategy is a function of institutional governance. An institution that cannot independently set its research agenda, control its own board appointments, or protect its leadership from politically motivated interference cannot build the kind of sustained, multi-year research infrastructure the HERD data demands regardless of what coalition it joins. This is not a hypothetical concern. Prairie View A&M, one of AHRI’s founding members, operates within the Texas A&M University System, a governance structure in which the flagship institution’s interests, priorities, and resource allocation decisions do not always align with those of a historically Black land-grant whose research mission serves a fundamentally different community. The degree to which Prairie View can pursue an independent research commercialization strategy, build its own technology transfer infrastructure, or make unilateral decisions about patent filing and licensing within that system is a question the coalition’s formation does not resolve. Texas Southern, another AHRI founding member, has experienced more direct interference: its board has been subject to hostile gubernatorial appointments that resulted in the termination of institutional leadership in ways that the broader HBCU community recognized as reflecting political interests rather than institutional ones. Tennessee State has faced comparable dynamics, with the state’s Republican-controlled legislature effectively vacating its board and replacing it with gubernatorial appointees, a maneuver that places the strategic direction of a public HBCU in the hands of an administration with no particular stake in HBCU research excellence. An HBCU that cannot protect its own president, control its own board, or govern its own research agenda is not positioned to build a serious research enterprise regardless of its AHRI membership. The coalition is only as strategically coherent as the institutional autonomy of its members. That autonomy, for several of its founding institutions, is not guaranteed. It is contested.

The structural argument that the data ultimately forces is this: no external actor — no administration, no Congress, no philanthropic initiative operating at current scales — has demonstrated the will to close a gap this large. Replicating and scaling what the sector’s fastest-growing research institutions have done requires HBCU administrations to stop treating their research enterprises as afterthoughts, HBCU alumni to stop treating their philanthropy as sentiment, and HBCU communities to start treating institutional research capacity as what it actually is — a long-term economic and political asset that compounds in value every year it is invested in, and deteriorates every year it is not.

The HERD Survey is updated annually. And annually, the same story is told. The question is whether the institutions that story concerns have finally decided to write a different one.

Data sourced from the National Center for Science and Engineering Statistics, Higher Education R&D Survey (HERD), FY 2015–2024; and the National Academy of Inventors, 2024 Top 100 U.S. Universities Granted U.S. Utility Patents. All HERD expenditure figures are in thousands of current dollars.

Disclaimer: This article was assisted by ClaudeAI.

If the Democrats can not hold the line of the Federal Reserve’s independence, then America as we know it is over. The U.S. dollar as the world’s reserve currency will be on life support and foreign countries will be expeditious in the pulling of the plug because trust in the U.S. financial system will be no more. – William A. Foster, IV

Jerome Powell leaves the Federal Reserve on May 15th. His likely successor, Kevin Warsh, is a wealthy former governor with convenient monetary views and a notable reluctance to say obvious things plainly. Democrats have the procedural votes to slow his confirmation. Whether they have the institutional will to use them is a different question and the answer matters more than most people realise.

The Federal Reserve does not often feature in discussions of HBCUs. It should. The interest rate at which a small Black-owned bank in Memphis can borrow money, the credit conditions facing a first-generation homeowner in Atlanta, the yield that a university endowment in Alabama can realistically expect on its bond portfolio: all of these are shaped, in ways direct and indirect, by the policy choices made inside the Eccles Building in Washington. The selection of a new Federal Reserve chair is, among other things, a decision about whose economy gets managed.

That is what makes the confirmation of Kevin Warsh, President Donald Trump’s nominee to succeed Jerome Powell, more consequential than the usual Washington pageant of hearings, hedged testimony, and partisan positioning. Warsh appeared before the Senate Banking Committee on April 21st. By the end of the day, a reasonably clear picture had emerged not just of his monetary philosophy, but of his character. It was not a flattering portrait.

Start with the money, because with Warsh the money is unavoidable. Financial disclosure forms filed ahead of the hearing placed his personal holdings at between $135 million and $226 million, concentrated heavily in two positions in the Juggernaut Fund LP, a vehicle associated with billionaire investor Stanley Druckenmiller, for whom Warsh has worked as a partner. His wife, Jane Lauder, granddaughter of cosmetics entrepreneur Estée Lauder, has an estimated personal fortune of around $1.9 billion. By comparison, Jerome Powell, the man Warsh would replace, disclosed assets of roughly $19.5 million, held mostly in index funds and municipal bonds. Ben Bernanke, who chaired the Fed during the 2008 financial crisis, stepped down in 2014 with assets of at most $2.3 million, mostly in retirement accounts. The message encoded in Warsh’s disclosure is not that rich people cannot run central banks. It is that the man who will make decisions about credit access for working Americans has never had occasion to worry about credit access himself.

The hearing did nothing to soften that impression. Warsh was asked, at one point, a question that should not require courage to answer: who won the 2020 presidential election? The answer is documented, certified by Congress, and not remotely in dispute among anyone operating in good faith. Warsh declined to say it plainly. He noted instead that “this body certified that election”—a formulation so carefully calibrated to avoid displeasing the president who nominated him that it managed to be both technically accurate and substantively evasive. Paul Krugman, the Nobel Prize-winning economist, called Warsh Trump’s “sock puppet.” Senator Elizabeth Warren used the same phrase. The comparison is uncharitable. It is also, on the evidence of the hearing, not easily rebutted.

Warsh was equally reluctant to defend Fed Governor Lisa Cook (Spelman), who faces politically motivated scrutiny from the administration, or to express support for Powell, who is the subject of a Justice Department investigation that Republican Senator Thom Tillis of North Carolina has used as a pretext to block Warsh’s own confirmation vote—a piece of procedural irony that illuminates just how thoroughly this nomination has been consumed by partisan mechanics. A nominee unable to defend his soon-to-be colleagues from transparently political attacks is, at minimum, a nominee who has chosen to demonstrate that loyalty to the president outranks loyalty to the institution he is asking to lead.