“Dear Young Black Males… Always remember to hold your head up high, and NEVER doubt who you are. Believe in yourself SO much that other people’s negative words, opinions, and energy won’t discourage or hinder you.” – Stephanie Lahart

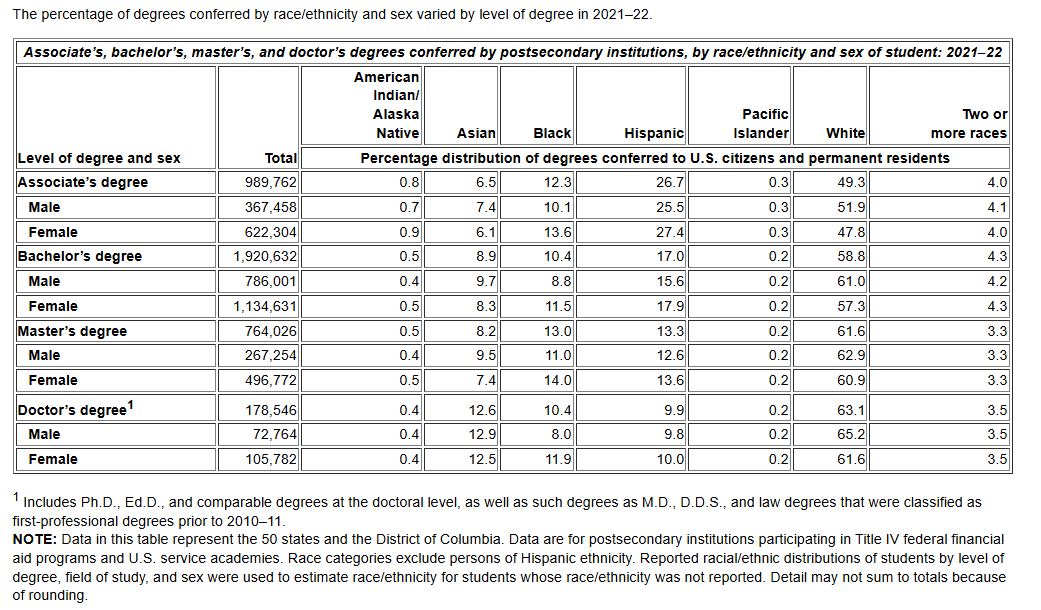

African Americans continue to be the only group where the women outnumber the men in terms of employment. The systemic reasons for this abound and not particularly the focus in this piece, but one of those areas is certainly educational obtainment. Whereas African American girls are in large part taught to focus on mental and academic achievement as a means of success, African American boys are taught to focus on physical and athletic achievement as a means of success. The two most notable gaps are at the Associate’s degree and Doctor’s degree levels where there is a difference of 350 basis points and 390 basis points, respectively. While it would be nice to see more African American young men getting Bachelor’s degrees, from an economic reality, simply getting more of them with an Associate’s is cheaper and faster in terms of return on investment for the community.

Enter the 10 HBCUs that are community or technical colleges along with UDC who has community college division while still being a 4-year institution. This collection of HBCUs represents a network of community and technical colleges dedicated to providing accessible, affordable education and workforce development opportunities. Focused on serving African American communities, these institutions offer associate degrees, certificates, and vocational training programs. There is also the opportunity to create a pipeline to four-year HBCUs or direct entry into the workforce. They emphasize community enrichment, economic mobility, and leadership development, often incorporating faith-based or mission-driven values. Collectively, they play a vital role in empowering individuals and strengthening the communities they serve.

As of 2021-2022 according to NCES, there is an approximately 50,000 Associate’s degree gap between African American Women and Men (Table Below) with women obtaining almost 85,000 Associate degrees annually and men obtaining just over 37,000 Associate degrees annually. The major obstacle to these 10 HBCUs closing the gap is what ails most systemic issues facing African America – finances. These 10 HBCUs have an average tuition cost of $6,500 and median tuition cost of $5,300. But in order cost of attendance is a far more accurate because it includes the ability to pay for residence be it on-campus or off-campus, meal plans, books, and other necessities of educational obtainment. The average and median for that related to these 10 HBCUs is approximately $20,000 which is inclusive of the tuition and fee cost. This cost of attendance is due to both the low cost of tuition at two-year institutions in general and these HBCUs being located in affordable towns as a whole. However, it maybe a lot to ask if the goal is to truly incentivize enough African American Men to take two years if they were not intending to and by the numbers many clearly are not intending to go to college even for an Associate’s degree without a cherry on top. Simply ensuring they have full tuition and room/board is enticing, but it is likely not enough. If we look at this as a salary, then paying African American Men $20,000 a year to be students is probably not going to cut it. However, pushing that number to say $30,000 a year with a disposable income of $10,000 per year could be enough to bring many into the fray.

Here is the math of getting to $30 billion. Assuming our endowment for this program can generate 5% annually, then it would take $600,000 in principal to generate the $30,000 necessary per student. That is $600,000 times the 50,000 gap we need to close annually or $30 billion. Enough to generate $1.5 billion in interest. At current, there are no African American institutions that are either non-profit or for-profit valued at $30 billion. Howard University has the largest African American non-profit endowment and it is just under $1 billion. World Wide Technology is the most valuable for-profit firm at $20 billion and its African American ownership in the firm at 59 percent makes his stake worth approximately $12 billion.

There is even an argument that should this miraculous endowment appear if it should be spent on African American men ages 18-40 or if it should be focused on African American boys where you could provide supplemental education and academic investment at a far earlier age where you would need to spend a fraction of the $30,000 to get impactful long-term results. While there is a firm argument for this, my answer is resoundingly no. It should and would need to be spent on the 18-40 year old age group. The reason why is simple. African American Women need help now. The gap that has existed for sometime now has caused a crisis in the community with African American women being unable to find African American men that are suitable partners, the overweight responsibility of economic burden they carry, and much more. The closing of the gap is worth $7,700 in increased earnings per African American man who upgrades from a high school diploma to an Associate’s degree or $385 million annually if simply brought in balance with the number of Associate’s that African American Women earn.

The burning question of course is where we get $30 billion in assets from that can produce $1.5 billion annually (a 5 percent return). Unless someone is secretly hiding 300,000 bitcoins, they bought for $0.01 many years ago that are now worth $30 billion there may be no real solid answers. Time is of the essence so the notion that we are going to slow roll our way there as we do with most everything else financially is a nonstarter and just more of the same issues. Government funding is also almost certainly not an option given that regardless of political party very little has been done to rectify systemic issues that face African America. One party would like to give us nothing despite the fact that we pay into the tax system and the other party gives us symbolic and lip service. For context, there are only 5 university endowments that are greater than $30 billion.

In the end, the truth of the matter is this will not be solved by a single endowment or a single organization. However, $30 billion in a collective effort across multiple organizations coordinating with this goal may in fact be possible and pragmatic. With almost $2 trillion in buying power in theory the resources are there – sort of. Buying power can be very misleading because it does not actually speak to disposable income of the African American community. The money that is leftover after the bills are paid. Much of African America’s $2 trillion has very little leftover once you account for needs and necessities of African American households. This actually speaks quite a bit to African America’s buying power only account for almost 11 percent of America’s $18.5 trillion in buying power, but accounting for almost 14.5 percent of the American population. The $2 trillion should be closer to $2.7 trillion. That is $700 billion essentially “missing” from the African American households. Needless to say, it would a lot easier to find that $30 billion there.

A collective and strategic effort is necessary to bridge the Associate’s degree gap between African American men and women. While a $30 billion endowment seems daunting, the solution lies not in a single source of funding but rather in a coordinated approach involving multiple organizations, institutions, and innovative financial strategies. Leveraging partnerships with HBCUs, African American financial institutions, and philanthropic networks can help mobilize the resources needed to generate meaningful change. Furthermore, targeted outreach to influential individuals, businesses, and community leaders can catalyze fundraising efforts.

The focus must remain on providing African American men with the financial support necessary to pursue educational opportunities. By directly investing in their economic advancement, the ripple effect will extend beyond individuals to families and communities. The $385 million annual increase in earnings resulting from closing the Associate’s degree gap underscores the profound economic impact of this initiative. Equally important, this investment addresses the broader social and relational imbalances that have burdened African American women for decades.

Achieving this ambitious goal will require innovative thinking, sustained advocacy, and bold financial commitment. However, with collaboration and purpose, empowering African American men through education can yield lasting benefits for the entire community, fostering stability, opportunity, and generational wealth.

Tracking Black Economic Stakes in America’s Economic Indicators and Central Bank Signals

Monday, May 26 – Memorial Day

No scheduled economic events While markets rest, Black workers—especially in essential sectors—continue to labor under wage suppression. National holidays often illuminate persistent labor disparities where African Americans overrepresent in underpaid, underprotected service roles.

Tuesday, May 27

Minneapolis Fed President Neel Kashkari Speech (Tokyo, 4:00 AM & 8:00 PM ET)

Known for his dovish leanings, Kashkari may highlight global risks to U.S. growth. For African Americans, particularly those vulnerable to job cuts in an economic slowdown, his tone on future rate cuts is critical.

Durable-Goods Orders (Apr): -7.8% (Prev: +9.2%)

A sharp plunge signals weakening investment and manufacturing demand. This contraction could hit Black industrial workers and logistics employees, especially those in Southern and Midwestern states.

Durable-Goods Minus Transportation (Apr): Data Pending

A flat reading here would confirm broad weakness beyond aerospace and autos, hurting smaller suppliers and minority-owned industrial businesses.

Case-Shiller Home Price Index (Mar): Data Pending (Prev: +4.5%)

Rising home prices continue to push African Americans out of first-time homeownership, especially in major urban markets like Atlanta, D.C., and Charlotte, where HBCU alumni are concentrated.

Consumer Confidence (May): 86.0 (No Change)

Flat confidence underscores persistent economic anxiety. For Black households carrying higher debt loads and experiencing lower wealth levels, stagnation in sentiment suggests limited consumption growth and continued vulnerability.

Wednesday, May 28

Minneapolis Fed President Neel Kashkari Speech (Tokyo, 4:00 AM ET)

Expect continued remarks on global financial coordination. The impact of any global tightening or deflation trends could ripple into U.S. credit markets, disproportionately hurting communities already locked out of affordable loans.

FOMC Meeting Minutes (2:00 PM ET)

This will reveal how serious the Fed is about easing policy. Delay in rate cuts prolongs high borrowing costs, keeping homeownership and business investment out of reach for many African Americans and HBCUs.

Minimal movement masks deeper problems; Black unemployment remains higher than national averages, and layoffs still skew toward underrepresented groups in precarious industries.

GDP (Q1 First Revision): -0.3%

A contracting economy, even marginally, means slower hiring and investment. For African American workers and business owners already operating with less margin for error, the pressure will rise.

Richmond Fed President Tom Barkin Speech (8:30 AM ET)

Representing a region with many HBCUs and Black rural towns, Barkin’s remarks could preview whether the Fed sees these communities as economic priorities or statistical footnotes.

Pending Home Sales (Apr): -0.4% (Prev: +6.1%)

Slumping pending sales point to ongoing housing market stress. This especially harms African American families trying to transition from renters to owners amid high mortgage rates.

Chicago Fed President Austan Goolsbee Speech (10:40 AM ET)

Goolsbee’s economic pragmatism could bring a dose of realism on inequality. If he signals concern over underperformance in low-income markets, that could hint at future support for inclusive growth.

Fed Governor Adriana Kugler Speech (2:00 PM ET)

Kugler may touch on labor market disparities and wage equity. Her background in labor economics makes her one of the more likely Fed voices to mention economic stratification directly.

San Francisco Fed President Mary Daly Speech (4:00 PM ET)

Daly often discusses inclusion and systemic barriers—her speech could reinforce the need for policy tools that close gaps in employment, housing, and education for Black communities.

Dallas Fed President Lorie Logan Speech (8:25 PM ET)

Logan oversees a region with growing Black populations in cities like Dallas and Houston. Her take on regional growth and monetary policy could influence credit access and labor demand in these hubs.

Friday, May 30

Personal Income (Apr): +0.3% (Prev: +0.5%)

Income growth slowing means wage pressures are easing—a problem for African American households already earning less and struggling with rising living costs.

Consumer Spending (Apr): +0.2% (Prev: +0.7%)

Weaker spending growth reflects household caution. Black consumers, often with fewer financial safety nets, are pulling back out of necessity—not choice.

Inflation is slowing but still above target. High price persistence in areas like housing and food continues to affect African American families, who spend a larger share of income on essentials.

Advanced U.S. Trade Balance (Apr): Data Pending (Prev: -$163.2B)

A massive trade deficit signals continued reliance on imports. U.S.-based Black manufacturers and exporters remain sidelined by structural inequalities in scale, capital, and global market access.

Advanced Retail Inventories (Apr): Data Pending (Prev: -0.1%)

Inventory declines suggest caution among retailers, which could mean reduced orders for minority-owned suppliers and less hiring in warehouse/logistics sectors with strong Black labor representation.

Advanced Wholesale Inventories (Apr): Data Pending (Prev: +0.4%)

If inventories keep rising, distributors may slow purchasing cycles, tightening cash flow for small suppliers—particularly those without banking relationships or supplier diversity contracts.

Chicago Business Barometer (PMI, May): 45.5 (Prev: 44.6)

A sub-50 reading indicates contraction. For African American professionals and businesses in Midwest metro markets, sluggish growth can stall economic progress and widen existing gaps.

Consumer Sentiment (Final, May): 50.8

Still hovering at recessionary levels, sentiment continues to reflect fear. Among Black households facing persistent inflation and limited safety nets, pessimism may trigger more cautious economic behavior.

San Francisco Fed President Mary Daly Speech (4:45 PM ET)

Her final remarks of the week may reinforce the theme of inclusive recovery—or warn of economic divergence. Either way, Daly remains a Fed leader worth watching for HBCU communities and Black policymakers.

HBCU Money Insight: This week’s economic data confirms what many in Black America already feel—stagnant wages, expensive goods, and unaffordable homes. Despite easing inflation, the lack of meaningful policy response to racial economic disparities remains glaring. As Fed voices speak from Tokyo to Texas, the African American economy remains in the shadows of the headlines.

“I built a conglomerate and emerged the richest black man in the world in 2008 but it didn’t happen overnight. It took me 30 years to get to where I am today. Youths of today aspire to be like me but they want to achieve it overnight. It’s not going to work. To build a successful business, you must start small and dream big. In the journey of entrepreneurship, tenacity of purpose is supreme.” — Aliko Dangote

It could be argued that many HBCUs do not see themselves as African American institutions. They just happen to be a college where African American students are the predominant student population – for now. A place where you may happen to find more African American professors than you would elsewhere. But in terms of intentionally being a place looking to serve the social, economic, and political interests of African America and the African Diaspora as a whole not so much. Schools like Harvard and the Ivy League in general seek to serve WASP interests, BYU and Utah universities serve Mormon interests, there is a litany of Catholic universities led by the flagship the University of Notre Dame serving Catholic interests, and around 30-40 women’s colleges serving women’s interests. Arguably, none are more intentional though than Jewish universities who seek to serve Jewish Diasporic interests. They do so intentionally and unapologetically. It is highlighted in two prominent dual programs.

Brandeis University, “founded in the year of Israel’s independence, Brandeis is a secular, research-intensive university that is built on the foundation of Jewish history and experience and dedicated to Jewish values such as a respect for scholarship, critical thinking and making a positive difference in the world.”

Master of Arts in Jewish Professional Leadership and Social Impact MBA In partnership with the Heller School for Social Policy and Management: “If you want to become a Jewish community executive, this program will give you the skills and expertise you need: a strong foundation in both management and nonprofit practices, as well as a deep knowledge of Judaica and contemporary Jewish life. You’ll take courses taught by scholars across the university, including management courses focused on nonprofit organizations and courses specific to the Jewish community.”

Master of Arts in Jewish Professional Leadership and Master in Public Policy: “If you want to become a professional leader who can effect positive change for the Jewish community at the policy level, you’ll need policy analysis and development skills as well as knowledge of Judaic studies and contemporary Jewish life — all of which our MA-MPP track is designed to impart. This track will teach you how to both assess policy and practice and design and implement strategic solutions.”

In the United States, the racial wealth gap remains stubbornly wide. For every dollar of wealth held by the average white household, the average Black household holds just 14 cents, according to the Federal Reserve. While policy debates rage on, a quieter revolution could be ignited in the lecture halls and boardrooms of Historically Black Colleges and Universities (HBCUs). It is time for these institutions to take the lead in launching a new kind of MBA—one rooted in African American entrepreneurship.

This would not be a symbolic gesture of representation. Rather, it would be a radical recalibration of business education in service of economic sovereignty. The proposed African American MBA, anchored at HBCUs, would fuse conventional business acumen with a deep focus on building and scaling Black-owned enterprises—injecting capital, credibility, and cultural context into the fight for economic justice.

A Different Kind of MBA

Traditional MBA programs—whether in Boston, Palo Alto, or London—have long celebrated entrepreneurship, but they rarely address the distinct structural barriers faced by African American founders: racialized lending, limited intergenerational capital, and investor bias, among others. An African American MBA would tackle these head-on.

Students would learn to navigate venture capital ecosystems that have historically excluded them, build business models designed for resource-scarce environments, and craft growth strategies anchored in community reinvestment. The curriculum would include case studies of Black-owned business successes and failures, from the Johnson Publishing Company to the modern fintech startup Greenwood Bank.

Such a program would not just train entrepreneurs; it would cultivate what economist Jessica Gordon Nembhard refers to as “economic democracy”—an ownership-driven economy where Black communities produce and own the value they generate.

From Theory to Practice

For this model to work, HBCUs must go beyond coursework. They must build ecosystems.

At the core of the program would be university-based business incubators providing capital, mentorship, and workspace. Students could launch ventures with real funding—from alumni-backed angel networks or Black-owned community development financial institutions (CDFIs). Annual pitch competitions would create visibility and momentum, offering grants, equity investment, or convertible notes to top-performing student ventures.

A tight integration with Black-owned businesses, supply chains, and financial institutions would form the scaffolding. Students might spend time embedded in legacy enterprises like McKissack & McKissack, or cutting-edge startups in healthtech, agritech, and media.

These ecosystems would provide fertile ground for venture creation while catalyzing local job growth. In doing so, they would re-anchor HBCUs as engines of regional economic development, not just academic training grounds.

The HBCU Edge

HBCUs are uniquely positioned to own this space. They already produce 80% of the nation’s Black judges, half of its Black doctors, and a third of its Black STEM graduates. Yet despite this outsized impact, their business schools have yet to consolidate around a unifying purpose.

By championing entrepreneurship explicitly tailored to African American realities, HBCUs could claim a domain left underserved by Ivy League and flagship public institutions.

Moreover, HBCUs benefit from strong community credibility, a network of engaged alumni, and access to philanthropic capital increasingly earmarked for racial equity. With ESG mandates guiding corporate philanthropy and DEI budgets under scrutiny, there is untapped potential for long-term partnerships with companies seeking measurable social impact through supplier diversity, mentorship, or procurement commitments.

Risks and Realities

Skeptics will ask: Will such a degree be taken seriously in the broader market? Will it pigeonhole students into “Black businesses” instead of the Fortune 500? The answer lies in the performance of the ventures it produces. Success, not symbolism, will be the ultimate validator.

Indeed, many of the world’s most transformative businesses have emerged from institutions that bet on community-specific models. Consider how Stanford’s proximity to Silicon Valley allowed it to incubate global tech companies—or how Israel’s Technion helped power a startup nation.

An African American MBA need not limit its graduates to one demographic. Rather, it provides a launchpad from which Black entrepreneurs can build scalable, inclusive ventures rooted in lived experience. And in doing so, change the face of entrepreneurship itself.

The Road Ahead

If a handful of HBCUs lead the way—Howard, Spelman, North Carolina A&T, and Texas Southern come to mind—they could collectively establish a national center of excellence for African American entrepreneurship. Over time, this could grow into a consortium offering joint degrees, online programming, and cross-campus business accelerators.

The long-term vision? A Black entrepreneurial ecosystem rivaling that of Cambridge or Palo Alto, but infused with the resilience, cultural currency, and social mission uniquely forged by African American history.

This would not merely be an academic experiment. It would be a new chapter in a centuries-old story—one where the descendants of slaves become the architects of capital.

Focusing an African American MBA program offered by HBCUs on entrepreneurship could be transformative for fostering economic growth and self-sufficiency within the Black community. Here’s how such a program might look:

Program Vision and Goals

Empower Black Entrepreneurs: Equip students with the tools and networks to build successful businesses that create wealth and opportunities within African American communities.

Address Systemic Barriers: Focus on overcoming challenges like access to capital, discriminatory practices, and underrepresentation in high-growth industries.

Build Community Wealth: Promote entrepreneurship as a pathway to closing the racial wealth gap and revitalizing underserved areas.

Curriculum Highlights

Core MBA Foundations:

Finance for Entrepreneurs: Teach how to secure funding, manage cash flow, and create financial models tailored to African American small and medium enterprises (SMEs).

Marketing and Branding: Strategies for building culturally relevant brands that resonate with diverse audiences.

Operations and Scaling: Guidance on running efficient operations and scaling businesses sustainably.

Specialized Courses:

Tomorrow’s Entrepreneurship: Building ventures with dual goals of profit, community impact, and focus on industries of the future.

Navigating VC and Angel Investments: Training on pitching to investors, negotiating terms, and understanding equity structures.

Black-Owned Business Case Studies: Analyze successes and failures of prominent African American entrepreneurs. Much like the Harvard Business Review that sells case studies there would be an opportunity for HBCU business schools to create a joint venture for the HBCU Business Review and sell case studies relating to African American entrepreneurship.

Hands-On Experiences

Business Incubator:

A dedicated incubator at the HBCU to provide seed funding, mentorship, and workspace for students to develop their ventures.

Real-World Projects:

Partner students with local Black-owned businesses to solve real business challenges.

Annual Pitch Competitions:

A platform for students to showcase business ideas to potential investors, with prizes and funding opportunities.

Partnerships and Networks

Corporate and Community Collaborations:

Partnerships with companies that prioritize supplier diversity programs to provide procurement opportunities for graduates.

Collaborations with established Black entrepreneurs for mentorship and guest lectures.

Access to Capital:

Establish a dedicated fund or partnership with Black-owned financial institutions to provide startup capital.

Measurable Outcomes

Startups Launched: Track the number of new businesses started by graduates.

Jobs Created: Measure the economic impact of those businesses in local communities.

Community Investment: Monitor how much revenue is reinvested into underserved neighborhoods.

In contrast to institutions that intentionally serve specific cultural, religious, or ideological communities, many HBCUs appear to operate as predominantly African American in demographic composition rather than as institutions deeply invested and intentional in advancing the collective social, economic, and political interests of African Americans and the African Diaspora. While other universities—whether Ivy League institutions catering to elite WASP traditions, religious universities fostering faith-based leadership, or Jewish universities purposefully cultivating Jewish communal leadership—explicitly align their missions with the advancement of their respective communities, HBCUs often lack this same level of strategic intent. If HBCUs wish to remain vital and relevant in the future, they may need to more deliberately embrace their role as institutions committed to the upliftment of African American communities, not just as spaces where Black students and faculty are well-represented, but as powerful engines of social transformation.

Centering the Black Economic Lens on Federal Reserve Movements and Economic Indicators

Monday, May 19

New York Fed President John Williams Speech (8:45 AM ET)

Williams’ comments on inflation and growth will be closely watched. As a key voice in rate-setting, any hawkish signals could delay relief for African American borrowers already paying higher credit premiums.

Fed Vice Chair Philip Jefferson Speech (8:45 AM ET)

Jefferson, the Fed’s first African American Vice Chair, may emphasize equitable employment and inclusive policy. His framing will matter for HBCUs and Black communities relying on federal support and labor stability.

U.S. Leading Economic Indicators (Apr): -0.9% (Prev: -0.7%)

A steeper decline signals weakening momentum. This typically translates into fewer job openings, reduced wage growth, and tighter lending—especially damaging for African American workers and businesses still lagging in recovery.

Tuesday, May 20

Richmond Fed President Tom Barkin Speech (9:00 AM ET)

Barkin’s region includes southern states with high African American populations. His insights could indicate whether regional policy and economic support are filtering down to underserved communities.

Boston Fed President Susan Collins at Fed Listens (9:30 AM ET)

One of the few women of color leading a Fed bank, Collins’ presence at Fed Listens may bring attention to community feedback. Expect mentions of wealth inequality, which remains sharpest for Black Americans.

St. Louis Fed President Alberto Musalem Speech (1:00 PM ET)

As a new voice in the Fed, Musalem’s outlook could influence policy leanings that shape access to capital—particularly relevant in Missouri and the Mississippi Delta region, home to several HBCUs and Black rural communities.

Fed Governor Adriana Kugler Speech (5:00 PM ET)

Kugler’s focus on inclusive employment metrics may touch on disparities in Black unemployment and wage stagnation, helping guide equitable macroeconomic planning.

Wednesday, May 21

Fed Listens Event: Barkin & Bowman (12:15 PM ET)

These sessions are critical opportunities to elevate Black institutional voices—including HBCUs, Black banks, and civil society groups. The listening format also reflects whether the Fed is serious about closing racial wealth gaps through policy.

Little movement here masks a troubling truth: Black unemployment remains higher than national averages, and layoffs in service sectors often disproportionately affect African American workers.

S&P Flash U.S. Services PMI (May): 50.8 (Same as Forecast)

Marginal growth in services is a mixed bag. Black-owned service businesses may benefit from stable demand, but credit costs and supply chain inflation continue to eat into profits.

S&P Flash U.S. Manufacturing PMI (May): 49.8 (Below Forecast)

Contracting manufacturing output threatens industrial jobs—especially for African Americans in urban centers with historic manufacturing legacies and ongoing economic vulnerability.

Existing Home Sales (Apr): 4.12M (Prev: 4.02M)

An uptick in sales signals improved market activity, but high interest rates still lock out many African Americans from homeownership, exacerbating wealth inequality.

New York Fed President John Williams Speech (2:00 PM ET)

Williams’ second appearance may reinforce key monetary themes. If inflation remains the top concern, interest rates are unlikely to fall—delaying housing and business growth in communities that need it most.

Friday, May 23

Kansas City Fed President Jeff Schmid Speech (9:35 AM ET)

The Kansas City district includes Black communities in the Midwest. A pro-growth message from Schmid could be welcomed news for those hit hardest by disinvestment and population loss.

New Home Sales (Apr): 700,000 (Forecast: 724,000)

Falling slightly short of expectations, new home sales remain sensitive to mortgage rates. Limited access to credit and developer capital continues to stall Black homeownership and real estate entrepreneurship.

Fed Governor Lisa Cook Speech (12:00 PM ET)

The only African American woman on the Fed Board, Cook consistently advocates for equitable economics. Her remarks will likely address systemic financial exclusion and how monetary tools can close racial wealth gaps.

Though ceremonial, Powell’s remarks will be widely covered. If he speaks to opportunity and equity, HBCUs and Black institutions can press for tangible follow-through in monetary policy and research funding.

HBCU Money Insight: This week offers a mix of sobering and symbolic moments. With inflation slowing but economic indicators weakening, the question remains whether the Fed can pivot without sidelining Black workers, entrepreneurs, and institutions. For HBCUs and Black policymakers, these events are an opportunity to press for policy that doesn’t just stabilize the economy—but transforms who it works for.

“If you don’t find a way to make money while you sleep, you will work until you die.” — T. Harv Eker

Consider two farmers working adjacent plots of land. The first rises before dawn every morning, tills his soil by hand, plants his seeds, and harvests his crop himself. He is disciplined, tireless, and skilled. The second farmer also works diligently, but years ago he invested in irrigation systems, acquired additional acreage, and hired capable hands to manage the daily operations. Each morning, while both men are productive, the second farmer’s land is already generating yield before he laces his boots. By harvest season, the gap between them is not a matter of effort it is a matter of systems.

Now imagine that the first farmer was legally prohibited, for generations, from owning irrigation equipment. That he was denied title to additional acreage by the institutions that financed everyone else’s expansion. That every time he accumulated enough surplus to invest in infrastructure, external forces — legal, financial, social — interrupted the accumulation. By the time those prohibitions were lifted, the second farmer’s systems had compounded across decades. His children inherited not just land, but infrastructure. The first farmer’s children inherited his work ethic, and little else.

This is not a parable about laziness or ambition. It is a precise structural description of the passive income gap that defines African American economic life in the early twenty-first century and understanding it in those terms is the prerequisite to closing it.

In the American imagination, wealth is synonymous with work. The culture celebrates grit, discipline, and the relentless pursuit of the paycheck. Yet the country’s most economically durable families rarely labor for their living in the conventional sense. Their fortunes compound quietly through investments, dividend-paying equities, rental properties, and business interests that operate independent of their daily involvement. The accumulation of such passive income streams is not merely a personal finance preference it is the mechanism through which wealth reproduces itself across generations. And according to data from the U.S. Census Bureau and the Federal Reserve, African American households are more structurally excluded from that mechanism than any other major demographic group in the country.

Only approximately seven percent of Black households report receiving passive income of any kind whether from rental properties, interest-bearing instruments, dividends, or business ownership. By comparison, roughly twenty-four percent of white households report such income. The disparity in amounts is equally stark: the median passive income for Black families barely reaches two thousand dollars annually, compared to nearly five thousand dollars for white households. These are not marginal differences. They represent a fundamental divergence in how wealth is structured and reproduced and they do not emerge from differences in financial discipline or cultural values. They emerge from history operating through institutions.

The mechanics of that history are well documented, even if their ongoing consequences are frequently underestimated. For much of the twentieth century, the institutional infrastructure of American wealth-building was explicitly closed to Black participation. Federal mortgage programs underwrote suburban homeownership for millions of white families in the postwar decades while systematically excluding Black applicants through redlining and racially restrictive covenants. The GI Bill, nominally universal, was administered through local institutions that largely denied Black veterans access to its most wealth-generating provisions, the low-interest mortgages and business loans that seeded a generation of white middle-class asset ownership. Stock brokers ignored Black neighborhoods. Community banks serving Black depositors were chronically undercapitalized and disproportionately targeted for closure. The Freedman’s Savings Bank, established specifically to channel Black economic activity into formal financial infrastructure, was mismanaged into collapse within a decade of its founding, an early and formative lesson in institutional betrayal that resonates through surveys of Black financial trust to this day.

The result of these compounding exclusions is a wealth ecosystem structurally oriented toward earned income rather than asset income. Black households are more likely to rely entirely on wages and salaries, less likely to hold inherited financial assets, and more burdened by student loan debt, a combination that severely constrains the capital available for investment in income-generating assets. Asset inequality is, in this respect, more consequential than income inequality. A household can earn a substantial salary and still possess near-zero wealth if it holds no appreciating assets. Without passive income streams, every financial obligation must be met from current earnings, leaving no margin for accumulation, no buffer against disruption, and nothing to transmit to the next generation. The passive income gap is therefore not merely a measure of present financial well-being it is a structural indicator of generational economic capacity.

Chart: Chamber of Commerce using U.S. Census Bureau’s 2019 American Community Survey

The equity markets represent the most accessible entry point into passive income for households without inherited capital. The proliferation of low-cost index funds and exchange-traded funds has dramatically lowered the technical and financial barriers to market participation. A diversified position in a broad market index fund can now be established with modest, regular contributions, and fractional share platforms have effectively eliminated the minimum capital requirements that once made meaningful market participation inaccessible for many lower- and middle-income investors. Among Black households, market participation has increased measurably in recent years, accelerated in part by the financial disruptions and digital financial education that accompanied the pandemic period. Dividend reinvestment plans which automatically direct dividend payments into additional share purchases allow even small positions to compound without requiring additional capital contributions. These are not trivial instruments. Deployed consistently over time, they are the infrastructure through which institutional endowments and old-money family offices have maintained their positions across generations. They are now, for the first time in any meaningful sense, structurally available to households without inherited wealth.

Real estate has historically functioned as the second pillar of American household wealth accumulation, and its role in the passive income gap is correspondingly significant. The Black homeownership rate stood at approximately 44 percent as recently as 2022 — a figure notably lower than it was when the Fair Housing Act was passed in 1968, reflecting not merely the legacy of discriminatory exclusion but also the continuing structural disadvantages that Black households face in mortgage markets, including higher denial rates, less favorable loan terms, and reduced access to the equity-rich suburban markets where appreciation has been most concentrated. Homeownership is not, by itself, a passive income strategy but it is the entry point through which most households access the equity necessary to finance investment property acquisition. The ownership gap is therefore a compounding disadvantage: it reduces both wealth and the capacity to generate wealth-from-wealth.

Emerging platforms have begun to partially address this barrier through fractional real estate investment vehicles that allow individuals to acquire positions in income-generating properties without the capital requirements of direct ownership. Models built around real estate investment trusts provide exposure to rental income streams at low entry thresholds. More structurally interesting are the cooperative investment models emerging in cities including Birmingham, Baltimore, and Chicago, where Black investors are pooling capital to acquire multi-family residential properties and distributing rental income proportionally among participants. These arrangements draw on a long tradition of cooperative capital formation, the rotating savings circles and community lending mechanisms that have historically served as informal substitutes for formal financial infrastructure in excluded communities and are now being formalized and scaled through digital coordination tools and legal structures designed for collective ownership. The model is neither novel nor experimental in the broader historical context; variations on it have been used by Jewish, Chinese, and Caribbean diaspora communities as mechanisms for capital accumulation in the absence of full access to mainstream financial markets. Its resurgence in African American communities reflects both necessity and strategic clarity.

Business ownership represents perhaps the most consequential pathway to passive income, particularly for businesses structured to operate without requiring the founder’s continuous direct involvement. The income generated by a well-organized business is qualitatively different from wages as it is not capped by hours worked and can, in principle, be transmitted to heirs through equity transfer. Yet Black-owned businesses face systematic barriers to the capital necessary to reach the scale at which passive ownership becomes possible. A 2021 analysis by the Brookings Institution found that Black-owned businesses were roughly half as likely to receive funding as their white-owned counterparts, and received approximately one-third as much capital even when controlling for creditworthiness. The consequence is a concentration of Black entrepreneurship at the micro-enterprise level, where businesses are structurally dependent on the founder’s labor and consequently cannot generate the passive returns that characterize institutional-scale business ownership.

Digital business models have partially disrupted this barrier. Information products like online courses, subscription content, software tools, and digital publications require relatively low startup capital and can generate recurring revenue without proportional increases in labor. The emergence of platform infrastructure for content monetization has created genuine passive income streams for creators and educators operating at modest scale. These are not transformative institutional mechanisms on their own, but they represent a meaningful point of entry for households seeking to establish income streams beyond wages, and they are increasingly being pursued with strategic intentionality by individuals embedded in broader networks of Black financial education and community investment.

The cultural dimension of financial trust cannot be analytically separated from the structural picture. Survey data consistently document lower levels of trust in financial institutions among Black Americans — a pattern that persists even after controlling for income and education levels. This distrust is not irrational. It reflects an accurate historical assessment of institutional behavior: from the collapse of the Freedman’s Bank in 1874 to the predatory lending practices that concentrated subprime mortgage products in Black neighborhoods during the 2000s housing cycle, the relationship between Black households and formal financial institutions has been characterized by recurring exploitation and exclusion. The result is that a meaningful portion of the passive income gap reflects not ignorance of investment vehicles but rational caution about the institutions through which those vehicles are accessed. Closing the gap therefore requires not only financial education but institutional reconstruction, the development of Black-owned and Black-serving financial infrastructure that can provide access to capital markets through institutions whose incentive structures are aligned with their depositors’ and investors’ interests.

Community development financial institutions, Black-owned credit unions, and the financial operations of HBCUs themselves represent the institutional layer through which this reconstruction must occur. HBCU endowments, though modest relative to their peer institutions at predominantly white universities, serve as collective investment vehicles for the institutional community — and their growth is directly linked to the capacity of these institutions to generate passive income that funds scholarships, research, and operational independence. An HBCU with a three-hundred-million-dollar endowment generating a five-percent annual return has fifteen million dollars of non-tuition, non-appropriation income available for strategic deployment. An HBCU with a thirty-million-dollar endowment has one-tenth that capacity. The endowment gap is, at the institutional level, an exact structural analog of the household passive income gap and it carries the same generational implications. Institutions that cannot generate income from assets must perpetually depend on current revenue, limiting their strategic horizon to the immediate fiscal year and rendering them structurally unable to absorb disruption or invest in long-term capacity.

The policy dimension of this problem demands a more clear-eyed analysis than it typically receives, particularly given the political environment in which African American institutions now operate. The standard progressive policy toolkit — baby bonds, expanded retirement account access, first-time homebuyer assistance — rests on a premise that is increasingly difficult to sustain: that the federal government is a reliable or even neutral partner in the project of Black wealth-building. The current political configuration has demonstrated, with considerable consistency, that federal programs nominally universal in design are administered in ways that do not correct for existing disparities. Baby bonds are instructive precisely because their limitations reveal the problem. A program that provides every child an equal account at birth does not close a gap, it freezes it. A Black child beginning life in a household with negligible net worth, in a neighborhood with depressed property values, attending an underfunded school, and likely to carry disproportionate student debt into adulthood does not need the same starting account as a white child born into inherited equity and institutional access. Equal treatment applied to unequal conditions produces unequal outcomes. That is not a reform strategy. It is a restatement of the problem in more palatable language.

The more productive analytical frame is institutional self-sufficiency where the deliberate construction of economic infrastructure that does not depend on federal goodwill for its operation. This means directing capital toward Black-owned banks and credit unions capable of underwriting mortgages and business loans within the ecosystem, rather than routing every dollar of financial activity through institutions whose risk models and lending criteria systematically disadvantage Black borrowers. It means building the capitalization of HBCU endowments and community development financial institutions to the level where they can function as genuine sources of patient capital by financing real estate development, seeding early-stage enterprises, and providing the long-term investment infrastructure that currently exists almost exclusively outside the Black institutional ecosystem. And it means pursuing, at the state and municipal level, the targeted policy interventions that remain viable where federal action has become unreliable: land trusts, community investment tax credits, procurement preferences for Black-owned firms, and regulatory frameworks that support cooperative ownership structures. The political geography of the United States still contains jurisdictions where these instruments are achievable. The strategic priority is to concentrate and coordinate their use.

The passive income gap is ultimately a structural problem with structural solutions. For African American households, the accumulation of income-generating assets has been systematically disrupted across generations by explicit policy and institutional exclusion. What has emerged is a wealth ecosystem oriented almost entirely toward labor income — economically fragile, generationally limited, and structurally disconnected from the compounding mechanisms through which durable wealth reproduces itself. Addressing this gap requires coordinated action across multiple institutional levels: household investment behavior, community capital formation, HBCU endowment strategy, Black-owned financial infrastructure, and federal policy. No single mechanism is sufficient. The challenge is to build, simultaneously, the individual financial practices and the institutional architecture through which those practices can achieve scale.

The farmers in the opening parable were not separated by work ethic. They were separated by infrastructure — by access to the systems that allow effort to compound. The task before African American institutions and households is not to work harder. It is to build the irrigation.

Final Takeaways: Actionable Steps

🔹 Step 1: Open a brokerage account (Fidelity, Vanguard, or Charles Schwab) and start investing in stocks, ETFs, or REITs. 🔹 Step 2: If possible, buy a rental property or start with REITs for real estate exposure. 🔹 Step 3: Automate savings & investments through 401(k), Roth IRA, or Robo-advisors. 🔹 Step 4: Explore low-risk passive businesses. 🔹 Step 5: Consider group investing with family or community investment clubs.

This Week in the Economy: May 19–23, 2025

Centering the Black Economic Lens on Federal Reserve Movements and Economic Indicators

Monday, May 19

Tuesday, May 20

Wednesday, May 21

Thursday, May 22

Friday, May 23

Sunday, May 25

HBCU Money Insight:

This week offers a mix of sobering and symbolic moments. With inflation slowing but economic indicators weakening, the question remains whether the Fed can pivot without sidelining Black workers, entrepreneurs, and institutions. For HBCUs and Black policymakers, these events are an opportunity to press for policy that doesn’t just stabilize the economy—but transforms who it works for.

Leave a comment

Posted in Economics

Tagged African American Homeownership Trends, Black Economic Policy 2025, Black Small Business Economic Outlook, Black Unemployment Statistics, economy, Fed Interest Rates Impact on Black Communities, federal reserve, Federal Reserve and Black Wealth, finance, HBCU Financial Commentary, Inclusive Economic Growth Fed Listens, inflation, interest rates, Lisa Cook Federal Reserve Speech, Philip Jefferson Economic Equity