“Power grows when it circulates. If only one HBCU rises, none of us truly rise.”

MacKenzie Scott’s philanthropy has reshaped the HBCU landscape in ways that few could have imagined a decade ago. When her unrestricted gifts began landing across the sector, they offered something rare in Black institutional life: immediate liquidity, strategic freedom, and the assumption that HBCUs knew best how to use the capital given to them. Institutions like Prairie View A&M, Tuskegee, Winston-Salem State, Spelman, Morgan State, and others seized this moment to strengthen balance sheets, expand programs, retire debt, and set in motion long-term visions often delayed by years of underfunding.

But while headlines celebrated these historic gifts, another truth ran quietly beneath the surface many of the smallest, oldest, and most financially fragile HBCUs received nothing. Texas College, Voorhees, Morris, short-funded religiously affiliated colleges, and two-year HBCUs were notably absent from the list. Their exclusion was not due to a lack of mission, quality, or need. It was due to visibility, a structural inequality baked into the philanthropic landscape.

Large and mid-sized HBCUs possess communications offices, audited financial statements, national reputations, and alumni networks large enough to keep their names in circulation. Small HBCUs often have one person doing the work of an entire department, no national brand presence, and no full-time staff dedicated to donor engagement. Philanthropy at scale tends to flow to institutions already “discoverable,” which means the colleges that need the money most are often the least visible to donors like Scott. This is not a critique of her giving; she has done more for HBCUs than any private donor in a generation. Where the African American donors of consequence is a another article for another day. It is an indictment of a philanthropic system that confuses visibility with worthiness.

Unrestricted capital, however, changes power dynamics. When an HBCU receives $20 million, $40 million, or $50 million with no strings attached, it is receiving not just money but institutional autonomy. It is gaining the ability to build, to plan, to hire, to innovate, and to settle the long-deferred obligations that drain mission-driven organizations. This autonomy carries with it an important question: what responsibility does an HBCU have to the larger ecosystem when it receives this kind of power?

HBCUs often describe themselves as part of a shared lineage, a collective built from necessity and sustained by interdependence. If that is true, then institutions that receive transformative gifts have a responsibility to circulate a portion of that capital to the HBCUs that remain structurally invisible. This is not a matter of charity; it is a matter of ecosystem logic. A rising tide only lifts all boats if every institution has a boat capable of floating.

Even a small redistribution—2 to 5 percent of unrestricted gifts—would represent a meaningful shift. A $50 million gift becomes a $1–2.5 million contribution to a collective pool. A $20 million gift becomes $400,000–$1 million. A $5 million gift becomes $100,000–$250,000. Spread across the dozens of HBCUs that received Scott’s funds, such a strategy could generate $40–60 million in shared capital almost immediately. For a small HBCU with a $12 million budget, even a $500,000 infusion can stabilize operations, hire essential staff, or stave off accreditation risks. And for two-year HBCUs—critical institutions that often serve first-generation and working-class students—$250,000 can transform workforce programs or upgrade classroom technology.

When unrestricted money flows into the ecosystem, it should not be seen as belonging solely to the institution receiving it. It should be viewed as a rare chance to strengthen the entire system that sustains Black educational capacity. That means revisiting the historic practices of resource sharing that once defined HBCUs. There was a time when faculty were exchanged, when larger institutions lent administrators to smaller ones, and when collective survival was at the center of institutional strategy. Financial scarcity eroded much of that ethos over time; unrestricted capital can revive it.

The need for this kind of intra-HBCU investment becomes even more urgent when we consider how philanthropy shapes public perception. When a small HBCU faces financial distress, politicians and media often use its weakness as a reason to question the entire sector. But when a small HBCU strengthens, expands, and stabilizes, it lifts the credibility of the collective. The fate of one HBCU inevitably influences the political and philanthropic fortunes of the others. Strengthening the weakest institutions is not optional it is a strategic imperative for the strongest ones.

Shared capital also opens the door to new structures that benefit the entire ecosystem. Larger HBCUs could help create a visibility accelerator that provides grant-writing support, marketing expertise, budgeting assistance, and donor engagement tools for smaller institutions. They could establish a joint endowment fund where smaller HBCUs gain access to investment managers they could never otherwise afford. They could create emergency liquidity pools to help institutions weather short-term cash shortages that often cascade into long-term crises. They could co-sponsor research initiatives, faculty exchanges, and new academic programs at institutions that have the vision but lack the staff or funding to execute.

These are not theoretical ideas; they are practices used by well-resourced universities and nonprofit networks across the country. Major universities routinely fund pipeline schools, partner institutions, and community colleges. Corporations build up their suppliers. Regional governments pool funding to strengthen smaller municipalities. In almost every sector except the HBCU sector, power is used to build the ecosystem, not just the institution.

One of the most overlooked consequences of Scott’s gifts is the cultural message they send: large HBCUs are now in a position to move beyond survival mode and into builder mode. They can start thinking not just about their own campuses but about the health of the entire HBCU network. They have the resources to help smaller institutions become discoverable to future donors, to strengthen donor reporting infrastructure, to modernize back offices, and to raise their visibility in national conversations.

Redistribution is not about guilt. It is not about moral obligation. It is about strategic logic. Large HBCUs cannot thrive in a sector where small HBCUs collapse. For the ecosystem to have political leverage, credibility in national policy debates, and a future pipeline of Black scholars and professionals, the entire network must be strong. When an HBCU closes or falters, opponents of Black institutional development use that failure as proof of irrelevance. When an HBCU grows even a small one it becomes a success story that benefits the whole landscape.

The Scott gifts represent a once-in-a-generation financial turning point, but they are only a starting point. If HBCUs treat them as isolated blessings, the impact will be uneven and short-lived. If they treat them as seed capital for an ecosystem-wide transformation, the impact could reshape Black educational power for decades. Large HBCUs must decide whether they will be institutions that simply grow or institutions that help the entire sector evolve.

Smaller HBCUs cannot increase visibility alone. They cannot hire full development teams or produce 50-page donor reports without capital. They cannot expand new programs without bridge funding. They cannot modernize their infrastructure without partners. But the HBCUs that did receive unrestricted capital can change the landscape for them and by doing so, they strengthen the entire ecosystem.

This moment is not just about money. It is about whether HBCUs will use new wealth to reproduce old hierarchies or to build new pathways for collective power. In a philanthropic world that rewards visibility, the institutions that already stand in the light now have the responsibility and the means to illuminate the rest.

The measure of true power within the HBCU ecosystem is not what one institution accumulates. It is what the ecosystem can create together what none of its institutions could build alone. The future of HBCU philanthropy will depend on whether those blessed with unrestricted gifts choose to expand their own shadows or choose instead to cast light.

It’s tough for all farmers, but when you throw in discrimination and racism and unfair lending practices, it’s really hard for you to make it. – John Boyd, Jr., Founder of the National Black Farmers Association

America’s oldest financial divide is agricultural. Once, the majority of African Americans lived and labored on land; now, less than 1.4% of the nation’s 3.4 million farmers are African American. The disappearance of Black farmers is not only a human story—it is a story of capital deprivation, institutional neglect, and the collapse of an ecosystem that once linked land, education, and community credit. To reverse this, imagine if each of the 19 land-grant institutions in the 1890 HBCU system committed $1 million from their endowments and alumni associations to create a unified private lending fund. This $19 million “1890 Fund” would not sit passively in treasuries or bond portfolios but circulate directly through African American banks and credit unions, financing African American farmers and food producers across the country. Such a fund would be modest in scale but revolutionary in concept, a self-directed act of institutional cooperation that reconnects three critical arteries of African American economic life: land-grant HBCUs, African American financial institutions, and Black agricultural producers.

The 1890 HBCUs, institutions such as Tuskegee University, Prairie View A&M, North Carolina A&T, and Florida A&M were established as part of the Second Morrill Act of 1890 to serve African Americans excluded from the original land-grant colleges. Their purpose was not abstract scholarship but applied science: to teach, research, and extend knowledge about agriculture, engineering, and the mechanical arts. Over time, many of these schools evolved into comprehensive universities. Yet the decline of Black farmers and the consolidation of farmland under non-Black ownership represent a direct erosion of the very population these universities were created to serve. Between 1910 and 2020, African American land ownership fell by roughly 90%, from an estimated 15–16 million acres to less than 2 million today. The structural dispossession through discriminatory lending, heirs’ property laws, and USDA bias has left African American farmers with less access to credit and fewer pathways to generational land retention. HBCUs were founded to be a shield against such vulnerability. The 1890 Fund would revive that founding spirit, transforming their agricultural programs and extension centers into engines of financial empowerment rather than merely research hubs dependent on federal grants.

Each 1890 HBCU would allocate $1 million from a combination of its endowment and alumni association reserves, with matching commitments encouraged through philanthropic donors or corporate partners. The pooled fund $19 million at launch would be professionally managed under a cooperative structure, similar to a community development financial institution or business development company. The fund would not make direct loans itself but would place its capital into African American-owned banks and credit unions identified in HBCU Money’s 2024 African American-Owned Bank Directory. Institutions such as OneUnited Bank, Industrial Bank, Citizens Trust Bank, and smaller but vital credit unions like FAMU Federal Credit Union or Hope Credit Union would serve as the lending conduits. In effect, the 1890 Fund would function as the “wholesale” capital pool of low-interest (but profitable), long-duration deposits or certificates placed with African American banks that, in turn, originate and service loans to qualified African American farmers, cooperatives, and agri-businesses. Loans would range from $25,000 micro-lines for new producers to $500,000 or more for established operations seeking equipment, irrigation, or land expansion. Priority would be given to farmers with relationships to HBCU agricultural programs such as those who have completed workshops, extension training, or student partnerships. Each bank or credit union participating would commit to transparent reporting, with loan performance and demographic data shared annually with the 1890 Foundation. The revolving structure of repayments would ensure that as farmers succeed, their payments replenish the pool for new borrowers creating a regenerative loop of institutional and community wealth.

Routing the fund through African American financial institutions is not symbolic it is structural. Historically, Black farmers were denied access to credit through traditional banks and faced redlining by federal programs. Even today, USDA lending disproportionately benefits white farmers. African American banks and credit unions remain among the few institutions with both the cultural understanding and community trust necessary to underwrite these borrowers responsibly. Moreover, these banks themselves are chronically undercapitalized. With combined assets of roughly $7.5 billion across the sector, African American banks represent barely 0.001% of total U.S. banking assets, insufficient to exert meaningful influence in national credit markets. By placing deposits into these banks, HBCUs would strengthen their liquidity ratios, reduce dependence on volatile retail deposits, and expand lending capacity far beyond the fund’s nominal amount through fractional reserve leverage. In short, every dollar committed by an HBCU could translate into $7–$10 in agricultural lending capacity once multiplied through the banking system.

HBCU alumni associations hold untapped potential as financial intermediaries. While endowments must operate under fiduciary and investment constraints, alumni associations often have greater flexibility. They can act as private limited partners in the 1890 Fund, contributing capital from dues, life membership funds, or targeted campaigns such as “Adopt-a-Farmer.” Imagine an alumni chapter of Florida A&M underwriting 10 acres of hydroponic greens for a local farmer who agrees to hire FAMU agriculture graduates. Or Prairie View alumni pooling funds to purchase cold-chain trucks for dairy producers across Texas. These actions extend the HBCU brand into the real economy transforming loyalty into tangible economic development. Each alumni association could also create its own micro-fund linked to the central 1890 Fund, mirroring the “chapter endowment” concept used by major universities. This networked structure would democratize investment and bring the broader African American middle class into the process of agricultural renaissance.

Lending alone does not sustain farmers; ecosystems do. The 1890 Fund would operate most effectively if it integrated with the broader HBCU agricultural and business infrastructure. HBCU agricultural economists could conduct continuous impact analysis tracking how capital access affects yields, profitability, and land retention. Their findings would strengthen advocacy for increased African American private capital. Extension programs could pair loan recipients with agronomists and soil scientists to ensure that capital is used productively and sustainably. HBCU-affiliated food labs, hospitality programs, and dining services could prioritize procurement from funded farmers, creating closed-loop demand. Business schools could develop crop insurance products and risk models tailored to small producers, mitigating the vulnerability that has historically devastated African American farms. Student internships in finance, agriculture, and data science could be embedded in the fund’s operations training the next generation of agricultural financiers and analysts. This approach transforms the 1890 Fund from a mere loan pool into a comprehensive agricultural development platform.

The greatest strength of the 1890 Fund lies in its multiplier effect. Consider: $19 million revolving annually at a conservative 6% loan rate generates roughly $1.1 million in annual interest income—income that can be reinvested or partially distributed back to participating universities to grow the fund. If repayments are recycled annually, the fund could underwrite over $100 million in cumulative loans within its first decade. The macroeconomic ripple is job creation, land retention, and input purchases that would expand rural GDP in African American counties and increase deposit growth for the participating banks. Contrast this with the status quo: endowment funds largely held in Wall Street instruments that yield moderate returns but generate no localized impact. By re-directing even a fraction of assets into mission-aligned community lending, HBCUs align their investments with their historic purpose of educating and empowering the descendants of those who built the land.

The global contest for food security is intensifying. Nations that control food production, water, and soil fertility will control the future. For African America, regaining agricultural capacity is not nostalgic it is strategic. Every acre restored to productive use by African American farmers increases food sovereignty and reduces dependence on foreign or corporate supply chains. If HBCUs act collectively through the 1890 Fund, they position themselves as key players in regional and national food policy. They could partner with African universities for climate-resilient crop research, link with Caribbean agricultural cooperatives for trade, and develop transatlantic agribusiness ventures under the banner of Black institutional power. Such cooperation would redefine “land-grant” for the 21st century not as a relic of American expansion but as a global model of Pan-African capital deployment.

The road to building the 1890 Fund will not be smoothed by political cooperation. The federal and state governments that oversee the 1890 land-grant system are, in many cases, openly hostile toward African American advancement. Most of the 1890 HBCUs operate in states where racial resentment, austerity politics, and legislative interference remain the norm. These are states that have withheld or delayed millions in matching funds, imposed discriminatory audits, and used political appointments to keep HBCUs subordinate to their predominantly white peers. Under such conditions, the 1890 Fund is not merely an investment vehicle it is a form of institutional defense. Federal and state policy cannot be relied upon to sustain African American agriculture or financial independence. The only realistic path forward is one where HBCUs, alumni associations, and African American banks coordinate their own internal economy of capital, shielded from political manipulation.

This is where the 1890 Foundation becomes indispensable. Established to support the collective mission of the 1890 universities, the Foundation already exists as a neutral, centralized, and professionally managed entity capable of administering joint initiatives on behalf of all 19 institutions. Tasking it with managing the 1890 Fund would provide immediate credibility, legal infrastructure, and continuity. The Foundation could structure the fund as a private, revolving loan pool, capitalized through contributions from university endowments, alumni associations, and strategic partners, while remaining beyond the reach of hostile state legislatures. Governance through the 1890 Foundation would also protect participating universities from political retaliation. Rather than each HBCU appearing to act independently potentially inviting scrutiny from governors or state boards the fund’s activities could be coordinated under the Foundation’s national charter. This collective structure would allow for scale, professional risk management, and a unified investment policy aligned with the long-term interests of African American farmers and institutions.

Nevertheless, challenges remain. Some university boards, especially those with state-appointed trustees, may hesitate to commit endowment dollars to what they perceive as politically sensitive or unconventional investments. The uneven size of endowments ranging from under $50 million at smaller 1890s to more than $200 million at the largest could create tensions over proportional contributions. And while the 1890 Foundation provides an ideal governance structure, it would still need to secure regulatory clarity and investment expertise to manage a multi-million-dollar lending operation through external financial institutions. These risks, however, are outweighed by the opportunity to build economic sovereignty in an era of state hostility. The very conditions meant to weaken HBCUs like political obstruction, financial starvation, and bureaucratic oversight can become the catalysts for collective independence. If the 1890 Fund channels its capital through African American banks and credit unions, it strengthens two institutional pillars simultaneously: HBCUs regain control over how their endowments circulate, and Black-owned financial institutions gain the liquidity and leverage they need to expand.

The political hostility surrounding 1890 HBCUs should not be seen as a deterrent, but as confirmation of why this fund must exist. It demonstrates that African American progress, even in the 21st century, cannot depend on state benevolence. By empowering the 1890 Foundation to manage a private, self-sustaining fund, HBCUs would be acting in the same spirit of independence that defined their creation in 1890 when the federal government forced states to either open their existing land-grant colleges to Black students or create new ones for them. The 1890 Fund would be the modern continuation of that act of defiance transforming exclusion into enterprise. Through the 1890 Foundation’s leadership, African American endowments, farmers, and banks could finally operate in unison, beyond the grasp of state control. In doing so, they would build not just a lending mechanism, but a shield—a financial structure capable of outlasting political hostility and securing the long-term survival of Black agricultural and institutional power.

If the 1890 Fund fulfills its purpose, its long-term success should evolve into something even greater, a joint venture between the 1890 Foundation, African American banks, and African American credit unions that establishes a new national financial institution: one modeled on the Farm Credit System but existing independently from it to preserve full financial sovereignty. The Farm Credit System is a government-sponsored network of cooperative lenders that provides over $400 billion in loans and financial services to farmers, ranchers, and agricultural businesses across the United States. Its reach is vast and influential, covering roughly 40% of all agricultural debt in the country. Yet African American farmers have historically been excluded from its benefits. The FCS, like much of American agricultural policy, was built in an era when Black ownership was being systematically dismantled. It became a backbone for white rural wealth while African American farmers were left to navigate a labyrinth of local banks, discriminatory USDA programs, and predatory lending.

A successful 1890 Fund would prove that African American institutions: universities, banks, and credit unions can design a credit network capable of rivaling the FCS’s effectiveness, without its dependencies or racial exclusions. Over time, this collaboration could be formalized into a joint enterprise: the African American Agricultural Credit Alliance: a cooperative, member-driven, nationwide system built to finance not just farms but the entire food and fiber value chain. Like the FCS, it could be composed of multiple regional lending cooperatives, each capitalized by a blend of HBCU endowment investments, bank deposits, and credit union member capital. At its center would sit a national coordinating body responsible for liquidity management, risk pooling, and bond issuance. But unlike the FCS, this alliance would be entirely private and its governance drawn from the 1890 Foundation, the African American Credit Union Coalition, and the National Black Farmers Association. The goal would not be to replicate the FCS’s structure exactly but to rival its scale, providing affordable credit, insurance, equipment financing, and agri-business investment under the umbrella of Black-owned control.

Refusing to integrate into the existing Farm Credit System is not a rejection of efficiency it is a declaration of sovereignty. The FCS, though cooperative in name, ultimately answers to federal regulators, congressional committees, and a system of oversight that has never prioritized Black agricultural survival. Independence ensures that capital allocation decisions remain rooted in African American priorities—restoring land, building ownership, and sustaining communities rather than maximizing short-term returns. Financial sovereignty also allows for creative lending models that the FCS cannot adopt under federal restrictions, such as cooperative land trusts, heirs’ property buyouts, carbon-credit-backed collateral, or blockchain-based agricultural exchanges.

The evolution from the 1890 Fund to a fully realized agricultural credit system would expand capital from millions into billions. Once the fund demonstrates consistent performance, its track record could attract institutional investors like African American foundations, pension funds, and even sovereign funds from the African diaspora seeking mission-aligned, asset-backed investments. Through securitization and bond issuance, the alliance could channel long-term capital into rural Black communities, funding everything from precision agriculture and agroforestry to food processing and logistics. This would make agriculture once again an attractive sector for young entrepreneurs and HBCU graduates. Over time, the 1890 Fund could thus mature into an ecosystem capable of reindustrializing Black rural America through ownership and control of capital.

The creation of such a system would carry global implications. It could link with agricultural cooperatives in Africa and the Caribbean, forming a transatlantic agricultural finance corridor and positioning African American institutions as both lenders and investors in global food systems. The founding of the 1890 Fund, therefore, would not be an endpoint but the beginning of a long journey toward financial nationhood. The eventual establishment of an independent agricultural credit alliance would mark the institutionalization of economic sovereignty—a transformation from temporary coordination to permanent capacity.

The 1890 Fund embodies the principle that power comes from ownership, not participation. For too long, African American institutions have waited for external validation or federal rescue. The tools for rebuilding agricultural sovereignty already exist: universities with land and research infrastructure, banks with local lending channels, and farmers with generational knowledge. When linked together, these elements form a complete ecosystem capable of restoring both land and leverage. The $1 million commitment from each 1890 HBCU would not be a gift it would be a strategic investment in self-determination. If executed, within a generation the 1890 Fund could help reclaim millions of acres, incubate thousands of Black-owned farms, and expand the asset base of African American financial institutions. It would also serve as a model for other sectors like manufacturing, housing, and technology demonstrating how collective capital deployment transforms a marginalized community into a nation within a nation.

As Dr. Booker T. Washington once observed, “No race can prosper till it learns that there is as much dignity in tilling a field as in writing a poem.” The modern corollary is that no people can be free until they can finance their own fields. The 1890 Fund is not only a mechanism for loans it is a blueprint for liberation through institutional coordination. Its success could lay the groundwork for a sovereign financial architecture that, like the land it seeks to reclaim, will belong entirely to the people who cultivate it.

If you think you’re tops, you won’t do much climbing. — Arnold Glasow

Hip-hop was born out of necessity. A sonic rebellion against poverty, violence, and systemic neglect, it emerged from the Bronx as a raw reflection of life in America’s forgotten corridors. But over the past four decades, it has transformed from cultural resistance into commercial royalty. Once recorded with borrowed turntables in community centers, it now echoes across Super Bowl halftime shows, luxury brand campaigns, and billion-dollar corporate balance sheets. Artists who once stood on corners are now seated at boardroom tables. The culture won. But the community did not.

The statistics tell a story of growth at the top and stagnation at the bottom. Hip-hop is now a $16 billion industry. It has created artists turned entrepreneurs who have expanded into liquor, fashion, tech, and sports. The music dominates global charts, sets fashion trends, and influences everything from algorithms to political campaigns. Yet this immense cultural capital has not translated into economic sovereignty for the African American community. Instead, the concentration of wealth in a few hands has often disguised the lack of institutional power. For all the charts conquered and headlines generated, African American banks, endowments, universities, and asset management firms remain modest, if not endangered.

At the heart of this failure lies a devastating contradiction. While rappers flaunt wealth more publicly than any generation before them, the economic conditions in many African American communities remain dire. The median net worth of Black households, as of 2022, stands at $44,100 compared to $284,310 for White households—a gap that has barely moved in decades. Hip-hop has become the most visible face of African American success, but that visibility is not backed by scale. There are no Black equivalents to BlackRock or Vanguard. No hip-hop-funded HBCU research lab. No Goldman Sachs of rap. Even the highest echelon of Black-owned investment firms manage a fraction of their white counterparts. Vista Equity Partners, the most prominent, oversees $103.8 billion, an extraordinary feat, yet still a rounding error next to BlackRock’s $10.5 trillion.

And even this level of institutional success is an outlier. Most Black-owned investment firms manage less than $10 billion. Most HBCUs have endowments below $50 million. The largest Black bank, OneUnited, holds roughly $650 million in assets, while Bank of America manages over $2.5 trillion. What hip-hop has delivered in influence, it has not delivered in capital. Instead of building institutions, it has made individuals rich. But those individuals exist within a system that continuously siphons wealth away from their communities.

This is not to say that artists bear the blame for economic injustice. But hip-hop has become a tool of seduction as much as expression. Its dominance in the global marketplace has aligned it with the poor man’s logic of capitalism celebrating consumption, rewarding individualism, and elevating spectacle. In this model, buying a Bugatti becomes a symbol of power, while the absence of a Black mutual fund managing $100 billion barely registers. Lyrics obsess over fashion houses like Balenciaga, but rarely name Black-owned real estate firms or venture capital funds. The dream has shifted from ownership of blocks to ownership of Birkin bags.

This performative wealth is not just cultural; it’s systemic. The music industry itself is structured to extract more than it distributes. Record labels, streaming services, and publishing houses are disproportionately owned by entities with no allegiance to Black institutions. A 2023 report by Rolling Stone noted that artists receive less than $0.004 per stream on major platforms. Even when a track is streamed millions of times, the majority of profits flow to tech firms and record conglomerates, not to the creators or their communities. The money flows up and out. It is the same pattern that defines the broader African American economic experience: labor and creativity are extracted, while ownership and equity are denied.

The disparity is especially stark when one examines capital circulation. A dollar in the Black community circulates for less than 6 hours, according to HBCU Money, while in Jewish and Asian communities, it circulates for 17 and 20 days respectively. The consequence is an economy that is constantly depleted, reliant on external institutions for everything from finance to food. Hip-hop, despite its earnings, has not altered this trajectory. The Bugatti may be new, but the bank that financed it is old—and white.

This failure to institutionalize wealth is not accidental. It reflects deeper structural barriers, including a lack of access to financial infrastructure, intergenerational capital, and legal expertise. But it also reflects a shift in priorities within the culture itself. The era of Public Enemy and X-Clan once channeled music toward collective uplift. The current era often measures success by proximity to luxury, not impact on community. The metrics of power have changed from organization to ostentation.

Still, there are exceptions that point to what is possible. But these efforts remain underfunded and under-celebrated. There is no coordinated movement among hip-hop elites to pool capital, fund cooperative ventures, or launch institutional vehicles capable of rivaling their white counterparts. What could a $1 billion hip-hop endowment fund do for HBCUs? For land ownership? For venture funding of African American startups? These questions are never asked because the Bugatti is louder than the balance sheet.

It’s not just about what rappers buy. It’s about what they build or more accurately, what they have not built. For every luxury watch, there could be a community-owned grocery store. For every $30 million home, there could be a regional loan fund or student scholarship pipeline. The failure to institutionalize success means that when an artist dies, their wealth often dies with them dispersed among heirs or recaptured by the state or private corporations. There is no hip-hop university. No national Black credit union seeded by artists. No sovereign wealth fund of the culture.

Arnold Glasow’s warning—“If you think you’re tops, you won’t do much climbing”—rings like an indictment. The culture believes it has arrived, but the destination is superficial. It has conquered billboards but not balance sheets. The climbing left to do is immense: building a generation of lawyers, financiers, real estate developers, and economists who can institutionalize the gains of cultural dominance. Without this, hip-hop’s economic contribution will remain symbolic, not structural. The world will continue to dance to the music, while Black America stays undercapitalized.

A Bugatti depreciates. Institutions compound. Until hip-hop’s economic power stops ending with the individual and starts building for the collective, the community will remain stuck in a loop of representation without accumulation. The corner coffee shop that became Starbucks is not owned by the block. And the music booming from its speakers will not change that. Not unless the wealth it generates is used to build not just to boast.

“Control of credit is control of destiny. Until Our institutions decide where Our capital sleeps and wakes, Our freedom will remain on loan.” – William A. Foster, IV

The African diaspora’s greatest unrealized financial potential may lie not in Wall Street, but in the vast and growing debt markets of Africa. Across the continent, nations are negotiating, restructuring, and reimagining how they fund development. At the same time, African American banks and financial institutions, small but strategically positioned in the global Black economic architecture, stand largely on the sidelines. This disconnection is more than a missed investment opportunity; it is a failure of transnational financial imagination. If the descendants of Africa in America wish to secure true sovereignty, interconnectivity, and global influence, engaging African debt markets is not optional it is imperative.

Africa’s debt profile is as complex as it is misunderstood. Many Western narratives frame African debt in crisis terms, yet that view ignores the sophistication of African capital markets and the diversity of creditors. The continent’s public debt stood around $1.8 trillion by 2025, but much of this borrowing has gone toward infrastructure and industrial expansion. The key shift in recent years has been away from traditional multilateral lenders toward bilateral and market-based finance particularly through Chinese, Gulf, and private bond markets. Countries like Kenya, Ghana, Nigeria, and Ethiopia have issued Eurobonds in recent years, often at higher interest rates due to perceptions of risk rather than fundamental insolvency. Others, such as Zambia, have undergone restructuring efforts designed to rebalance repayment with growth. In each case, Africa’s economic story remains one of ambition constrained by external debt conditions, a pattern reminiscent of the post-Reconstruction era Black South, when capital starvation and dependency on non-Black lenders limited autonomy and intergenerational power. That parallel matters deeply for African Americans. The same global financial order that restricts African nations’ fiscal independence also limits the growth of African American financial institutions. The tools that could change both realities already exist within the diaspora: capital pools, credit analysis expertise, and shared strategic interest in sovereignty.

African American banks—roughly 18 federally insured institutions as of 2025—control an estimated $6.4 billion in combined assets. While that is a fraction of what one mid-sized regional white-owned bank manages, these institutions hold a symbolic and strategic power far greater than their balance sheets suggest. They remain the custodians of community trust, the anchors of small-business lending in historically neglected markets, and potential conduits for international financial collaboration. Historically, African American banks were created to fill a void left by exclusionary financial systems. But in the 21st century, their mission can evolve beyond domestic community lending toward global financial participation. The African debt market, currently dominated by Western institutions that extract value through high interest and credit rating manipulation, offers a natural arena for African American engagement. If Black banks can collectively participate through bond purchases, underwriting partnerships, or diaspora-focused sovereign funds they could help shift Africa’s dependence from Western and Asian creditors toward diaspora-based capital flows. This would not only stabilize African economies, but also create transnational linkages that reinforce both African and African American economic self-determination.

Consider the power of mutual indebtedness as a political tool. When nations or institutions lend to each other, they form durable relationships governed by trust, negotiation, and shared interest. For too long, the African diaspora’s relationship with Africa has been philanthropic or cultural rather than financial. That model, however well-intentioned, is structurally disempowering and it reinforces dependency rather than partnership. Debt, properly structured, reverses that dynamic. If African American financial institutions were to purchase or underwrite African sovereign and municipal debt, they would create financial obligations that tether African states to diaspora capital, not to exploit but to interdepend. This is the foundation of modern sovereignty: the ability to borrow and invest within your own cultural and political network rather than through intermediaries who extract value and dictate terms. Imagine, for instance, a syndicated loan or bond issuance where a consortium of African American banks, credit unions, and philanthropic financial arms partner with African development banks or ministries of finance. The terms could prioritize developmental outcomes like affordable housing, small business lending, renewable energy while generating steady returns. The instruments could even be marketed domestically as “Diaspora Sovereign Bonds,” accessible through digital platforms. The impact would be twofold: African American banks would diversify their portfolios and tap into emerging market yields, while African governments would gain access to capital free from neocolonial conditions.

Historically Black Colleges and Universities (HBCUs) stand at the crossroads of intellect, finance, and heritage. Their institutional capacity, academic talent, and alumni networks make them natural architects for a new financial relationship between the African diaspora and the African continent. Yet this potential comes with risk, particularly for public HBCUs, whose visibility and state dependency could make them targets of political and financial backlash. If a public HBCU were to openly participate in or advocate for engagement with African debt markets, it would likely face scrutiny from state legislatures, regulatory bodies, and entrenched financial interests. Such activity would be perceived by non–African American–owned banks and state-level policymakers as a challenge to existing capital hierarchies. The idea of Black public institutions developing transnational financial alliances outside traditional Western frameworks threatens not only market control but ideological narratives about where and how Black institutions should operate. To navigate this terrain, public HBCUs must be strategic, creative, and stealth in execution. Their participation in African financial engagement cannot be loud; it must be layered. They can do so through consortia, research collaborations, and investment partnerships that quietly build expertise and influence without triggering overt resistance. For example, an HBCU economics department could conduct African sovereign credit research under a global development initiative, while a business school could host “emerging market” investment programs that include African debt instruments without explicitly branding them as Pan-African.

Private HBCUs, freer from state oversight, can play a more overt role forming partnerships with African banks, hosting diaspora finance summits, and seeding funds dedicated to Africa-centered investments. But public institutions must operate with a subtler hand, leveraging think tanks, foundations, and alumni networks to pursue the same ends through indirect channels. Creativity will be their shield. Collaboration with African American–owned banks, credit unions, or diaspora investment funds can serve as intermediary structures allowing HBCUs to channel research, expertise, and even capital participation without placing the institutions themselves in direct political crossfire.

Both public and private HBCUs must also activate and empower their alumni associations as extensions of institutional sovereignty. Alumni associations exist in a different legal and political space and they are often registered as independent nonprofits, free from the direct control of state governments or university boards. This autonomy allows them to operate where the universities cannot. Through alumni associations, HBCUs can channel capital, intelligence, and partnerships in ways that stay outside the reach of regulators or political gatekeepers. Alumni bodies can create joint funds, invest in African debt instruments, or collaborate with African banks and diaspora enterprises. The understanding between HBCUs and their alumni networks must be clear and disciplined: the institution provides intellectual and structural guidance; the alumni associations execute the capital movement. This relationship becomes a discreet circulatory system of sovereignty with universities generating the vision and expertise, alumni executing the financial maneuvers that advance that vision.

HBCUs can further support this ecosystem by funneling institutional capital and intellectual property toward their alumni associations in strategic, deniable ways. Research centers can license data or consulting services to alumni-managed firms. Endowments can allocate small funds to “external collaborations” that, in practice, seed diaspora initiatives. Career and alumni offices can quietly match graduates in finance and development with African institutions seeking diaspora partners. These are small, legal, but potent acts of quiet nation-building. The success of this strategy depends on discipline, secrecy, and shared purpose. HBCUs, particularly the public ones, must move as institutions that understand the historical realities of Black advancement: every act of power must be both visionary and shielded. Alumni associations, meanwhile, must operate as the agile extensions of these universities, taking calculated risks on behalf of the larger mission. If executed carefully, this dual structure of HBCUs as the intellectual architects and alumni associations as the financial executors creates a protected channel for diaspora wealth creation. It allows public institutions to avoid political exposure while still advancing the collective objective: redirecting Black capital toward Africa and reestablishing a financial circuit of trust, obligation, and empowerment across the diaspora. In this model, the public HBCU becomes the hidden engineer, the private HBCU the visible vanguard, and the alumni network the financial hand. Together, they form an ecosystem of quiet innovation and a movement that builds transnational Black sovereignty not through protest or proclamation, but through precise and deliberate financial design.

Skeptics might argue that African American banks lack the scale or technical capacity to engage in sovereign lending. This concern, while not unfounded, can be addressed through collaboration. No single Black institution must go it alone. The path forward lies in consortium models of pooling resources, sharing risk, and leveraging collective bargaining power. Diaspora bond funds could be structured as partnerships between African American banks, HBCU endowments, and African development finance institutions such as the African Development Bank (AfDB) or Africa Export-Import Bank (Afreximbank). These organizations already have experience managing sovereign risk and would benefit from diaspora participation, which strengthens their political legitimacy. Furthermore, technology has lowered the cost of entry into complex financial markets. Digital banking, blockchain-based identity verification, and fintech partnerships can allow diaspora institutions to participate in cross-border finance with greater transparency and speed. The real obstacle, therefore, is not capacity it is vision. The diaspora’s capital remains trapped within Western financial systems that reward liquidity but punish sovereignty. Redirecting even a fraction of that capital toward Africa would shift the balance of global economic power in subtle but profound ways.

Sovereignty in the modern world is measured as much in capital access as in military or political power. Nations that cannot borrow on fair terms cannot build on fair terms. The same is true for communities. African Americans, long denied fair access to capital, should understand this truth intimately. The African debt question, then, is not a distant geopolitical matter it is a mirror. If African American banks and financial institutions continue to operate solely within the parameters of domestic credit markets, their growth will remain capped by a system designed to contain them. But if they extend their vision outward to the African continent, to Caribbean nations, to the global diaspora then they create new asset classes, new partnerships, and new pathways to power. Moreover, engagement with African debt markets enhances geopolitical influence. It positions African American institutions as interlocutors between Africa and global finance, enabling a collective voice on credit ratings, debt restructuring, and investment policy. That is the kind of influence that cannot be achieved through philanthropy or symbolism it is built through transactions, treaties, and trust.

Other diasporas have already proven this model works. Jewish, Indian, and Chinese global networks have long used financial interconnectivity as a tool of sovereignty. Israel’s government issues bonds directly to diaspora investors through the Development Corporation for Israel—a program that has raised over $46 billion since 1951. The Indian diaspora contributes billions annually in remittances and investments that underpin India’s foreign reserves. The African diaspora, by contrast, remains financially fragmented despite its vast size and income. With over 140 million people of African descent living outside Africa, the potential for coordinated capital deployment is immense. Even modest participation of say, $10 billion annually in diaspora-held African bonds would change the global conversation around African finance and diaspora economics. This scale of engagement requires trust, transparency, and accountability. African nations must commit to governance reforms and anti-corruption measures that assure diaspora investors of integrity. Likewise, African American institutions must build financial literacy and confidence around African markets, overcoming decades of Western media narratives portraying the continent as unstable or uninvestable.

The long-term vision is a self-sustaining ecosystem of diaspora credit: African American and Caribbean banks pool capital to buy or underwrite African debt; HBCUs model sovereign risk, publish credit analyses, and design diaspora finance curricula; African governments and regional banks issue diaspora-oriented financial instruments; fintech platforms connect diaspora investors directly to African projects; and cultural finance diplomacy transforms diaspora engagement into official national strategy. The ecosystem would allow wealth to circulate within the global African community rather than being siphoned outward through exploitative intermediaries. Over time, such networks could support not only debt financing but also equity investment, venture capital, and trade finance all under the umbrella of Black sovereignty economics.

At its core, this initiative is not merely about money. It is about the reconfiguration of power. The African diaspora cannot achieve full sovereignty while its economic lifeblood flows through institutions indifferent or hostile to its future. Engaging African debt markets transforms the diaspora from spectators of African development into its co-architects. It also transforms Africa from a borrower of last resort to a partner of first resort within its global family. For African American banks, this is the logical next chapter. The institutions that once shielded Black wealth from domestic exclusion now have the opportunity to project that wealth into international inclusion. It is a matter of strategic foresight aligning moral mission with financial opportunity. As the world edges toward a multipolar order where the U.S., China, and regional blocs vie for influence, the African diaspora must define its own sphere of power not through slogans but through balance sheets. A sovereign people must have sovereign finance.

Toward a Diaspora Credit Ecosystem

The long-term vision is a self-sustaining ecosystem of diaspora credit:

Diaspora Banks & Funds: African American and Caribbean banks pool capital to buy or underwrite African debt.

HBCU Research Hubs: HBCUs model sovereign risk, publish credit analyses, and design diaspora finance curricula.

Fintech Platforms: Secure, regulated digital systems connect diaspora investors directly to African projects.

Cultural Finance Diplomacy: Diaspora engagement becomes part of national policy—similar to how nations court foreign direct investment today.

The ecosystem would allow wealth to circulate within the global African community rather than being siphoned outward through exploitative intermediaries. Over time, such networks could support not only debt financing but also equity investment, venture capital, and trade finance all under the umbrella of Black sovereignty economics.

In 1900, at the First Pan-African Conference in London, W.E.B. Du Bois declared, “The problem of the twentieth century is the problem of the color line.” A century later, that color line has become a credit line. It is drawn not only across borders but across ledgers between who lends and who borrows, who owns and who owes. The African American bank and the African treasury are not distant cousins; they are parts of one economic body severed by history and waiting to be reconnected by will. Engaging African debt markets is not charity it is strategy. It is the financial expression of unity long preached but rarely practiced. The next stage of the African world’s freedom struggle will not be won merely in the streets or in the schools. It will be won in the boardrooms where capital chooses its direction. If African American finance chooses Africa, both sides of the Atlantic will rise together not as debtors and creditors, but as partners in sovereignty.

“The wealthiest boosters and donors to a PWI rarely ever played sports, but they did go build companies and a lot of wealth. Boosters spend hundreds of millions a year to compete with their friends and business competition from rival schools. The money spent is a bigger game than what happens on the field.” – William A. Foster, IV

Courtesy of The Rich Eisen Show

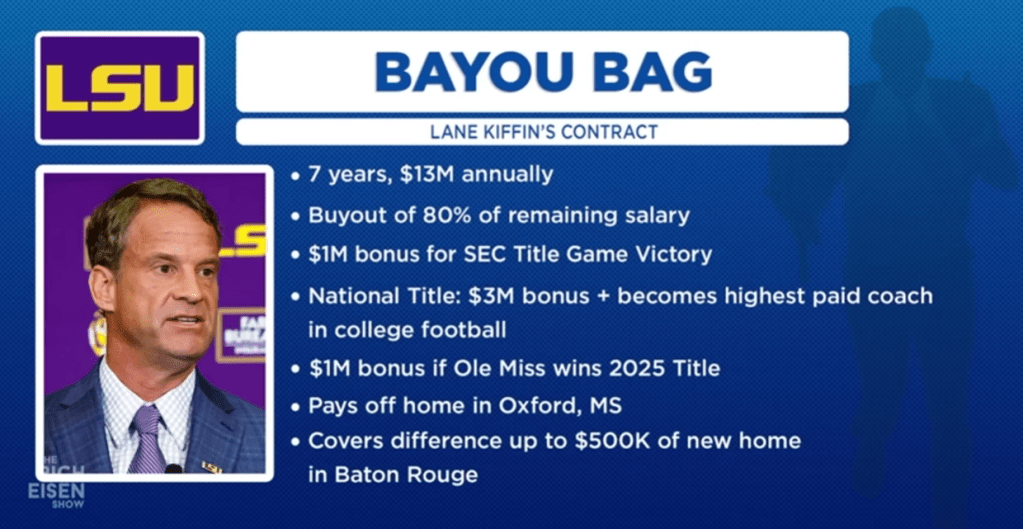

The image circulating across sports media this week says everything without trying to explain anything at all. LSU’s new contract offer to Lane Kiffin — seven years at $13 million annually, stacked with multimillion-dollar bonuses, home buyouts, and housing subsidies looks less like a coaching contract and more like a sovereign wealth transaction. It is the kind of deal only an institution backed by generational wealth, mega-boosters, and a national alumni base at the upper end of the economic ladder could produce. Yet every few months a familiar chorus resurfaces insisting that if “only the top African American athletes chose HBCUs,” the financial gap in college athletics would close. The narrative is compelling, emotional, and rooted in cultural longing, but it remains economically false.

The fantasy is seductive: if only more premier African American athletes chose HBCUs, our athletic programs could compete with Predominantly White Institutions (PWIs). If only we could land that five-star recruit, sign that top quarterback, or attract that elite basketball prospect, everything would change. The dream persists in alumni conversations, on social media, and in aspirational fundraising campaigns. But the dream is built on a fundamental misunderstanding of what actually drives college athletic success and it’s costing HBCUs resources they can’t afford to waste. The numbers tell a story that talent alone cannot rewrite.

Lane Kiffin’s new contract with LSU pays him approximately $13 million annually, making him one of the highest-paid coaches in college football. To put this in perspective, Southern University’s entire athletic department operates on total revenues of $18.2 million for fiscal year 2025-2026. One coach at a PWI earns over 70 percent of what an entire HBCU athletic department generates in revenue. This isn’t an aberration it’s the system working exactly as designed.

The disparity becomes even starker when you examine what funds these massive operations. According to an audit report, Southern University Athletics had total revenue of $17.3 million and expenses of $18.9 million in fiscal year 2023, creating a deficit of $1.5 million. Meanwhile, PWI athletic departments operate with budgets in the hundreds of millions. The athletes on the field, no matter how talented, cannot bridge this chasm.

What truly separates PWI athletic programs from HBCU programs isn’t the talent of 18-22 year-olds playing the games. It’s the economic power of the institutions behind them specifically, the size, wealth, and giving capacity of their alumni bases. According to Georgetown University, PWI graduates earn an average of $62,000 annually, compared to HBCU graduates who earn around $51,000. But the income gap is just the beginning of the story. The real disparity lies in generational wealth accumulation and the sheer number of potential donors.

Major PWIs have alumni bases numbering in the hundreds of thousands, often spanning generations of families who have accumulated significant wealth over decades. These institutions benefit from alumni who are CEOs, hedge fund managers, real estate developers, and executives at Fortune 500 companies. Their boosters can write seven-figure checks without blinking. When they want to retain a coach or upgrade facilities, they simply open their checkbooks.

HBCUs represent around 3% of America’s colleges, yet account for less than 1% of total U.S. endowment wealth. The endowment funding gap stands at approximately $100 to $1—for every $100 a PWI receives in endowment money, HBCUs receive $1. This isn’t just about annual giving; it’s about the compound interest of generational investment that HBCUs have never had the opportunity to build.

Corporate sponsors don’t pay for athletic excellence they pay for eyeballs and access to affluent consumer bases. When companies decide where to invest their marketing dollars, they’re calculating the purchasing power and professional networks they can reach through an institution’s alumni base. A company sponsoring a PWI athletic program gains access to hundreds of thousands of alumni with significant disposable income and decision-making power in corporations. The athletes are just the entertainment that delivers this audience. The actual product being sold is access to the alumni network—for recruiting employees, marketing products, and building business relationships.

This is why even if every top African American athlete chose HBCUs, the sponsorship dollars wouldn’t automatically follow. The economic fundamentals would remain unchanged. Companies invest based on return on investment calculations that are tied to alumni wealth and network size, not solely to on-field performance.

The belief that athletic success drives institutional prosperity is perhaps the most dangerous delusion facing HBCU leadership. Even among PWIs, only a tiny fraction of athletic programs actually turn a profit. Most operate at a loss that’s subsidized by the broader university budget, student fees, and institutional transfers. Southern University’s budget shows $2.2 million in “Non-Mandatory Transfer” and $1.4 million in “Athletic Subsidy”—meaning the institution itself must subsidize athletics with nearly $3.6 million in institutional funds. This is money diverted from academic programs, faculty salaries, research, and student services to keep athletic programs afloat.

The PWI athletic model works for PWIs not because athletics are inherently profitable, but because they can afford the losses. They have massive endowments, substantial state funding, and alumni donor bases that can absorb deficits while still funding academic excellence. HBCUs don’t have this luxury. When an HBCU runs a $1.5 million athletic deficit while struggling to pay competitive faculty salaries, upgrade outdated classroom technology, or fund research initiatives, the opportunity cost is devastating. That deficit represents scholarships not awarded, professors not hired, and academic programs not developed.

Some HBCU advocates point to conference television deals and NCAA tournament appearances as potential revenue sources. But here again, the math is unforgiving. Major PWI conferences negotiate billion-dollar television contracts because they deliver large, affluent viewing audiences that advertisers covet. The Big Ten and SEC don’t command massive TV deals because their athletes are more talented they command them because their alumni bases represent valuable consumer demographics. The SWAC and MEAC can’t replicate these deals because they don’t deliver the same audience size and purchasing power, regardless of the talent on the field. Even if HBCUs somehow assembled teams that won national championships, the structural economic advantages would remain with PWIs.

Here’s what proponents of athletic investment don’t want to acknowledge: the marginal difference in talent between a five-star recruit and a three-star recruit is minimal compared to the massive difference in institutional resources. A slightly more talented roster cannot overcome a 10-to-1 or 100-to-1 resource disadvantage.

Consider the logistics: While an HBCU football program might struggle to afford charter flights for the team, PWI programs have dedicated planes, state-of-the-art training facilities, nutritionists, sports psychologists, and medical staffs that rival professional franchises. They have recruiting budgets that allow them to identify and court prospects nationally. They have video coordinators, analysts, and support staff that outnumber many HBCU athletic departments entirely. The game is won with infrastructure, coaching depth, medical support, nutrition, facilities, and recovery technology not just with the athletes on scholarship. And these resources require the kind of sustained, massive funding that only comes from large, wealthy alumni bases and major corporate partnerships.

There is an alternative model that makes sense for HBCUs: the Ivy League approach. Ivy League schools have chosen not to compete in the athletic arms race. They don’t offer athletic scholarships for football. They emphasize academic excellence while maintaining competitive but not dominant athletic programs. Their alumni networks and institutional prestige are built on academic achievement, research output, and professional success not athletic championships.

For HBCUs, this model offers a realistic path forward. Focus resources on academic excellence, research capabilities, and entrepreneurship. Build prestige through intellectual output, not athletic performance. Create value through what HBCUs have always done best: developing future leaders, producing groundbreaking research, and serving their communities.

The Ivy League proves that institutional prestige and alumni loyalty can thrive without major athletic success. No one questions Harvard’s or Yale’s institutional value because their football teams don’t win national championships. Every dollar spent trying to compete in the PWI athletic model is a dollar not invested in what could actually transform HBCU economic outcomes: research infrastructure, entrepreneurship programs, endowment building, and academic excellence.

Research shows that more than half of all students at HBCUs experience some measure of upward mobility, and upward mobility is about 50 percent higher at HBCUs than PWIs. This is the actual competitive advantage HBCUs possess their ability to transform the economic trajectories of students from under-resourced communities. This mission deserves full investment, not the scraps left over after athletic departments consume resources. If HBCUs invested the millions currently subsidizing athletic deficits into research grants, business incubators, technology transfer offices, and endowed professorships, they could create sustainable revenue streams while fulfilling their core mission. They could become engines of wealth creation for African American communities rather than junior varsity versions of PWI athletic programs.

Admitting you can’t win an unwinnable game isn’t defeat it’s strategic wisdom. HBCUs should stop trying to beat PWIs at a game rigged by structural economic advantages they will never possess. Instead, they should redefine success on their own terms.

This means:

Rightsizing athletic budgets to reflect institutional resources and priorities, accepting that competing for national championships in revenue sports isn’t financially viable or strategically wise.

Investing in niche sports and athletic experiences that can be competitive without massive resource requirements and that build campus community without drowning budgets.

Redirecting resources toward academic distinction, particularly in high-demand fields like STEM, healthcare, and technology where HBCU graduates can command premium salaries and build generational wealth.

Building research infrastructure that attracts grants, creates intellectual property, and establishes HBCUs as innovation centers rather than athletic also-rans.

Developing entrepreneurship ecosystems that turn students into business owners and job creators, building the kind of economic power that generates sustained institutional support.

Creating HBCU-specific tournaments and competitions where these institutions can showcase their talents to their communities without subsidizing PWI athletic departments through guarantee games.

The African American community’s love for HBCU athletics is real and deep. The pageantry of HBCU homecomings, the tradition of the bands, the pride of seeing young Black excellence on display these matter. But love sometimes means making hard choices about where to invest limited resources for maximum impact. The question isn’t whether HBCUs should have athletic programs. The question is whether they should bankrupt their academic missions chasing a competitive model they can never win, designed by and for institutions with 100 times their resources.

One coach earning $13 million. One entire athletic department operating on $18 million. The math isn’t subtle. The choice shouldn’t be either.

Until HBCUs build alumni bases with the size, wealth, and giving capacity to compete in the modern college athletic arms race, pursuing the PWI model isn’t ambition it’s financial suicide. The path to HBCU prosperity runs through classrooms and laboratories, not football stadiums and basketball arenas. It’s time to stop chasing someone else’s game and start winning our own.

Disclaimer: This article was assisted by ClaudeAI.