Note: These data are based on colleges, universities, affiliated foundations, and related nonprofit organizations that volunteered to participate in NACUBO’s endowment study series.

A year after Howard University became the first HBCU to break the $1 billion endowment value mark, four other HBCUs have reached the $100 million mark. It is a complicated celebration when the NACUBO report shows 89 PWIs who have at least $2 billion in endowment value. A few notable HBCUs who reported last year like Morehouse College, North Carolina A&T and Meharry Medical College who have been regular NACUBO participants, are all absent from this year’s list. An HBCU favorite, the University of Virgin Islands returned after an absence in 2024. The reality on the ground with the looming crisis in admissions is for most HBCUs, $500 million is the endowment floor and only two HBCUs (Howard and Spelman) are above that mark. With not as many students graduating K-12, that means HBCUs who are heavily reliant on tuition revenue will see acute strains in the coming decade. It is not a matter of if, but when. Strong endowments are often the only thing that can see institutions through times of stress. That currently includes political stress that all colleges and universities are facing as it relates to state and federal funding. The lack of urgency among HBCU alumni continues to be concerning. Many HBCU alumni think their institution is in better financial shape than it is with no real landscape of higher education economics and the factors that create vulnerability. Using HBCU Alumni Associations and Chapters as more aggressive investment vehicles that can benefit an HBCU’s foundation and endowment are paramount to long-term stability. But this means seeing them as more than social clubs. HBCUs like all African American institutions are in perilous times and continued reliance on lottery philanthropy that may or may not come from non-alumni driven philanthropy (see Mackenzie Scott, Michael Bloomberg, etc.) is as dangerous as hoping to pay your bills every month with scratch off lottery tickets.

“This year’s report shows how important well-managed endowments are to colleges and universities,” said Kara D. Freeman, NACUBO President and CEO. “Endowments help fuel innovation and serve as a stable foundation for institutions. Because of challenges in the economy, some institutions relied more heavily on their endowments—but that additional spending benefited students, faculty, staff, research, operations, and more. Endowments make college possible and more affordable, and contribute to better lives for all.”

NACUBO HIGHLIGHTS:

Top 10 HBCU Endowment Total – $2.4 billion*

Top 10 PWI Endowment Total – $340.0 billion

Number of PWIs Above $2 billion – 89

Number of PWIs Above $1 billion – 169

Number of HBCUs Above $1 billion – 1

Number of HBCUs Above $100 million – 4*

678 colleges, universities, and education-related foundations completed NACUBO’s FY25 survey and those institutions hold $953.7 billion of endowment assets with an average endowment of $1.4 billion and median endowment of $259.9 million.

HBCUs comprised 1.4 percent of NACUBO’s reporting institutions and 0.3 percent of the reporting endowment assets.

PWI endowments (32) with endowments over $5 billion hold 57.4 percent of the $953.7 billion in endowment assets.

**The change in market value does NOT represent the rate of return for the institution’s investments. Rather, the change in the market value of an endowment from FY24 to FY25 reflects the net impact of: 1) withdrawals to fund institutional operations and capital expenses; 2) the payment of endowment management and investment fees; 3) additions from donor gifts and other contributions; and 4) investment gains or losses.

SOURCE: NACUBO

Take a look at how an endowment works. Not only scholarships to reduce the student debt burden but research, recruiting talented faculty & students, faculty salaries, and a host of other things can be paid for through a strong endowment. It ultimately is the lifeblood of a college or university to ensure its success generation after generation.

“To be a poor man is hard, but to be a poor race in a land of dollars is the very bottom of hardships.” — W.E.B. Du Bois

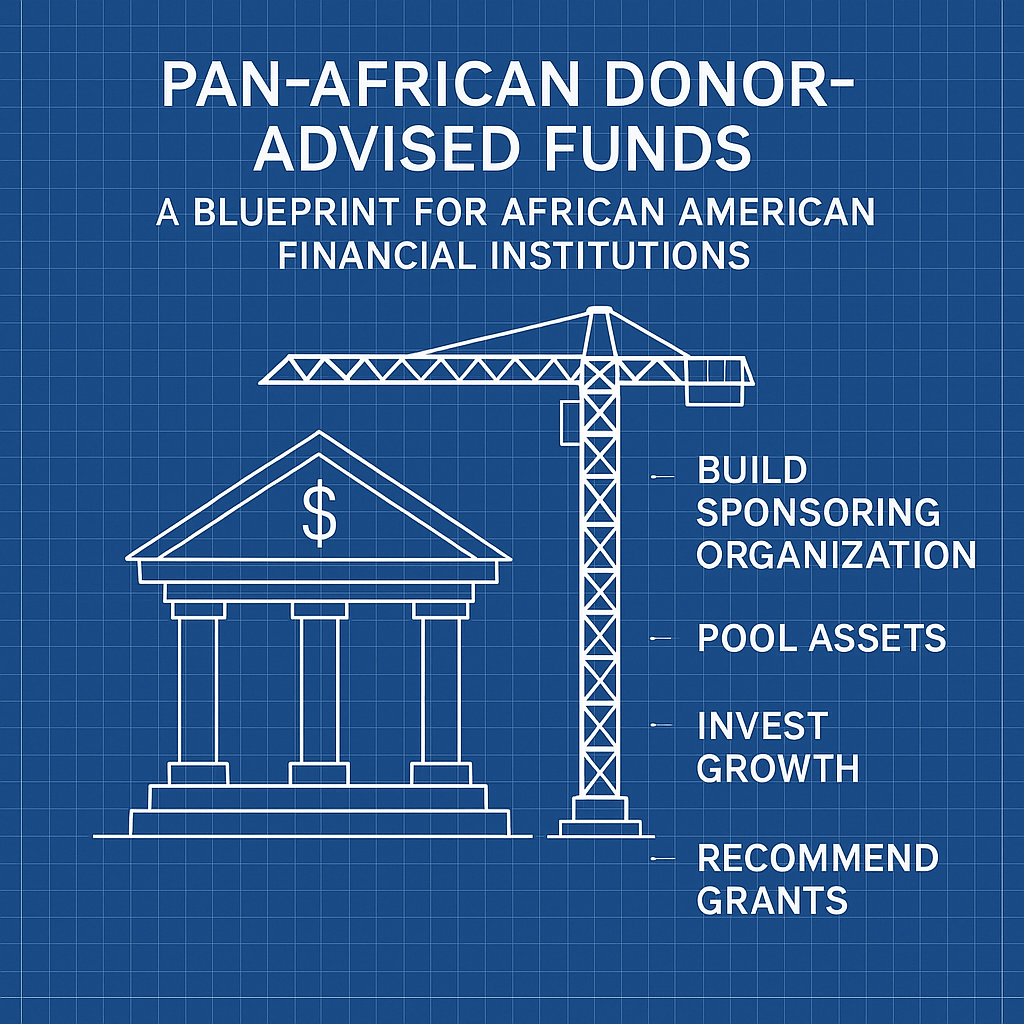

Philanthropy, at its best, is not only about generosity but also about power. For African America and the broader African Diaspora, philanthropy has too often been reduced to the goodwill of outsider corporations, foundations, and billionaires whose dollars arrive with priorities and strings attached. If African American financial institutions are to play a central role in reshaping the destiny of our people, they must learn to wield the tools of modern philanthropy at scale. Chief among these tools is the donor-advised fund.

A donor-advised fund, or DAF, is a charitable giving vehicle hosted by a sponsoring public charity. Donors contribute assets such as cash, securities, or real estate, receive an immediate tax deduction, and then recommend grants to nonprofit organizations over time. These funds are often described as “charitable investment accounts,” because once assets are placed inside them they can be invested for tax-free growth, providing donors the flexibility to make grants years or even decades later. Unlike private foundations, DAFs do not carry heavy administrative costs, reporting requirements, or annual payout mandates. That combination of flexibility, efficiency, and tax benefit has made them the fastest-growing vehicle in philanthropy, with more than $229 billion in assets managed in the United States by 2022.

The technical mechanics are straightforward, but the implications for African American institutional power are profound. When majority institutions host DAFs, they not only manage the assets and collect the fees but also strengthen their institutional position in the broader philanthropic ecosystem. If African American banks, credit unions, and HBCUs were to host their own DAF platforms, they would retain both the capital and the influence. They would also ensure that those assets circulate internally, building the capacity of Black institutions rather than reinforcing external ones.

The Pan-African case for donor-advised funds grows out of both history and strategy. The African Diaspora is scattered across North America, the Caribbean, South America, Europe, and Africa. Despite cultural variations, there is a shared experience of enslavement, colonization, and systemic exclusion that has left us fragmented and underdeveloped institutionally. A Pan-African DAF would allow African America’s wealth to pool with Diasporic wealth, creating a philanthropic capital base that could fund initiatives from Harlem to Havana, from Lagos to London. Imagine a Spelman alumna in Atlanta, a banker in Kingston, and a tech entrepreneur in Nairobi all contributing to the same Pan-African DAF. The fund’s assets grow through coordinated investment, and the grants sustain HBCUs, African universities, Diaspora think tanks, hospitals, and cooperative businesses. Philanthropy would move beyond sporadic generosity into a coordinated, long-term Diasporic strategy.

African American financial institutions are uniquely positioned to lead in building these vehicles. Black-owned banks could create DAF platforms, allowing depositors and wealthier clients to establish accounts, with the bank managing the assets and directing grants into curated pools of African American and Diaspora institutions. HBCUs could build DAFs under their endowment arms, offering alumni the chance to contribute not just to individual schools but to collective vehicles that support Black higher education broadly. Credit unions, already rooted in cooperative traditions, could create member-based DAFs that channel contributions into scholarships, healthcare clinics, or Diaspora research projects. A Pan-African exchange could even emerge, allowing African American donors to support African institutions and African donors to support African American initiatives, breaking down silos and creating reciprocity.

The impact on philanthropy would be transformative. Pooling resources through Pan-African DAFs would reduce fragmentation and administrative waste. A single DAF with $1 billion in assets could deploy $50 million in annual grants while continuing to grow its capital base. Instead of thousands of scattered donations, these funds would strategically target long-term capacity-building institutions like universities, hospitals, and think tanks. They would also allow families to pass advisory privileges to children and grandchildren, embedding intergenerational philanthropy into family legacies. By linking U.S. tax benefits with Diaspora impact, Pan-African DAFs would connect global Black institutions across borders in ways never before achieved.

More than philanthropy, DAFs are about institutional power. Hosting our own funds would allow African America to retain capital that otherwise circulates through majority institutions. The act of managing billions in philanthropic assets would increase the legitimacy, visibility, and bargaining power of African American banks and credit unions in the national financial system. Control over DAFs also allows agenda-setting: funding HBCU graduate schools, African healthcare systems, Diaspora media, or land ownership initiatives. With sufficient scale, Pan-African DAFs would fund the think tanks, advocacy networks, and policy shops that shape legislation and strategy across the Diaspora. They would also strengthen interdependence between Black banks, universities, and cooperatives, weaving a tighter institutional ecosystem. And globally, they would reframe African American philanthropy as not merely domestic but as a force shaping development across Africa, the Caribbean, and beyond.

Mainstream philanthropic firms offer lessons. Fidelity Charitable, Schwab Charitable, and Vanguard Charitable collectively manage tens of billions in DAF assets, attracting donors with ease of use, professional management, and trusted brands. But they also embody the critique that DAFs can warehouse wealth indefinitely, giving donors immediate tax deductions without ensuring timely disbursement to communities. A Pan-African DAF must avoid this trap by committing to clear disbursement expectations, perhaps requiring annual grantmaking of 7 to 10 percent of assets. It must also invest in building trust and branding. Fidelity and Schwab are household names; African American financial institutions must cultivate similar reputations for professionalism, security, and vision if they are to attract donors at scale.

The roadmap to implementation is straightforward. Institutions must establish DAFs under existing nonprofit or financial arms with full compliance to IRS rules. They must develop Pan-African investment strategies that allocate assets into African American-owned funds, African sovereign bonds, and Diasporic infrastructure projects. They need technology platforms that allow donors to open accounts, contribute assets, recommend grants, and track impact with ease. Partnerships with vetted institutions across the Diaspora are essential, ensuring that grants reach trusted universities, hospitals, and cooperatives. Above all, a compelling public narrative must frame participation in Pan-African DAFs as not just philanthropy but as an act of liberation and institution building. Families should be encouraged to use DAFs to teach the next generation about philanthropy and responsibility, embedding giving as a permanent part of Diasporic culture.

The vision for the future is clear. By 2045, African American banks could be managing $100 billion in Pan-African DAFs, with $7–10 billion flowing annually into HBCUs, African universities, hospitals, and think tanks. Fee revenues from managing these assets would sustain our financial institutions, while the grants would expand the capacity of Diasporic institutions. The Pan-African DAF could become one of the most powerful philanthropic vehicles in the world, rivaling Gates, Ford, and Rockefeller. But unlike those entities, it would not be rooted in charity; it would be rooted in sovereignty. It would represent a Diaspora using philanthropy to build freedom, not dependency.

Donor-advised funds are not new, but their potential for African American and Pan-African institutions has yet to be realized. For too long, our wealth has flowed outward, strengthening others’ institutions while leaving ours fragile. By developing Pan-African DAFs, African American banks, credit unions, and HBCUs can capture that wealth, grow it, and deploy it across the Diaspora to increase our power. This is not simply about philanthropy; it is about sovereignty, agenda-setting, and survival. The next century will not be decided by who receives charity but by who controls the institutions that give it.

The four-year graduation rate is often presented as a benign statistic tucked inside higher education reports, but for institutions serving African America, it is not benign at all. It is the lever on which long-term wealth, institutional survival, and multigenerational stability subtly depend. Wealthy universities treat the four-year graduation rate not as an outcome but as an engineered product, backed by endowment might, operational discipline, and capital-rich ecosystems. Their students finish on time because the institution ensures they are shielded from interruption. Meanwhile, HBCUs navigate a different reality: the same students who possess the intellectual capacity to thrive are too often delayed not by academics but by the economic turbulence that disproportionately defines their journey. It is here between the idea of talent and the machinery of capital that the four-year graduation rate becomes a revealing measure of African America’s structural position in the American economic hierarchy.

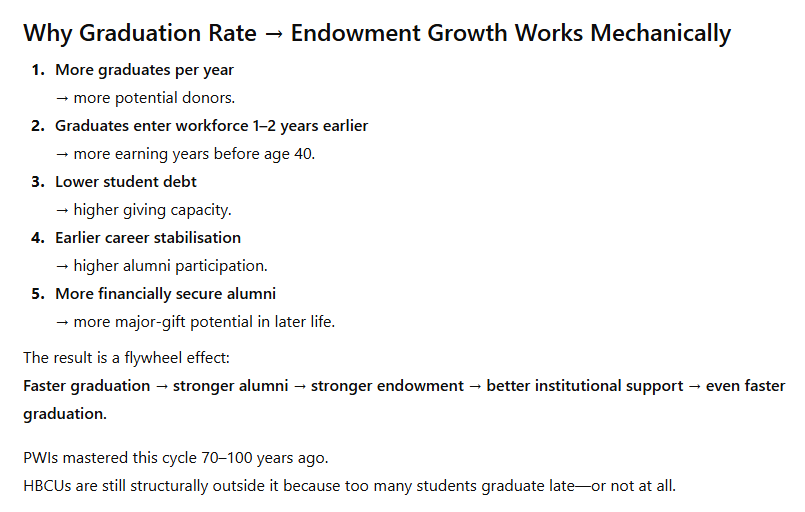

A delayed degree carries a cost structure that compounds aggressively. Extra semesters are not simply tuition bills; they are opportunity-cost accelerants. A student who graduates at 22 enters the workforce two to three years ahead of a peer who reaches the finish line at 24 or 25. Those early earnings fund retirement accounts earlier, compound longer, support earlier homeownership, and create the financial runway that future philanthropy relies upon. For African American students who statistically begin college with fewer financial reserves and exit with higher student debt those lost years are wealth years. They represent not only diminished individual prosperity but the slowed creation of a donor class that HBCUs and other African American institutions depend on to build endowment strength and institutional sovereignty.

Endowments, which serve as the economic lungs of a university, breathe differently depending on how quickly their alumni progress into stable earning years. A university that graduates students in four years rather than six gains an alumni base that stabilizes earlier, saves earlier, invests earlier, and gives earlier. A philanthropic ecosystem is essentially a long-term consequence of time management: the more years an alumnus spends debt-free and employed, the more predictable their giving pattern becomes. Elite institutions leverage this fact elegantly. HBCUs, despite producing extraordinary alumni under significantly harsher financial conditions, remain constrained by the delayed timelines imposed by student financial fragility.

Financial fragility is a central explanatory variable in the HBCU graduation gap. It is not uncommon for a student to miss a semester because of a $300 balance or a transportation breakdown that derails their schedule. In the broader American economic system, such modest shocks rarely jeopardize a wealthy student’s trajectory. But within the HBCU ecosystem, they represent the sharp edges of institutional undercapitalization meeting the exposed nerves of household vulnerability. The four-year graduation rate is therefore not simply a metric of academic navigation but a map of where the Black household economy intersects with American higher education’s structural inequities.

This makes alumni involvement not a sentimental tradition but an economic necessity. Alumni can narrow the financial fragility gap more efficiently than any other stakeholder group. Microgrant funds, even modestly capitalized, are capable of eliminating the most common disruptions that extend time-to-degree. A $250 emergency grant can protect $25,000 in long-term student debt. A $500 intervention can guard a student’s four-year trajectory and thus preserve two additional years of post-graduation earnings that ultimately benefit both the graduate and the institution’s future endowment. Alumni-funded tutoring, advising enhancements, STEM support programmes, and paid internships create artificial endowment-like effects: stabilizing student progression even when the institutional endowment itself is undersized.

Yet HBCU alumni cannot focus solely on the university years if the goal is a structurally higher four-year graduation rate. The process begins far earlier within K–12 systems that shape academic readiness long before students set foot on campus. The elite institutions that boast 85–95 percent on-time graduation rates are drawing from K–12 ecosystems with intense capital saturation: high-quality teachers, advanced coursework, stable households, well-funded enrichment programmes, and neighborhoods that function as multipliers of academic preparedness. HBCU alumni have an opportunity to influence this pipeline through investments that are often modest in individual scope but transformational in aggregate impact. Funding reading centres, coding clubs, college-prep academies, robotics labs, literacy coaches, and after-school tutoring programmes plants the seeds of future four-year graduates years before college entry.

Indeed, a strong K–12 foundation reduces the need for remedial coursework, accelerates major declaration, strengthens performance in gateway courses like calculus and biology, and diminishes the likelihood that students need extra semesters to satisfy graduation requirements. When alumni support dual-enrollment initiatives, sponsor early-college programmes, or build partnerships between HBCUs and local school districts, they enlarge the pool of college-ready students whose likelihood of completing on time is structurally higher. In this sense, investing in K–12 is not philanthropy it is pre-endowment development.

The economic implications of strengthening both ends of the education pipeline are enormous. A 20–30 percentage-point improvement in four-year completion rates across the HBCU ecosystem would reduce student loan debt burdens by billions, accelerate African American household wealth accumulation, raise the number of alumni earning six-figure incomes before age 30, and increase the philanthropic participation rate across Black institutions. Over decades, such shifts ripple outward: stronger alumni lead to stronger HBCUs, which lead to stronger civic, cultural, and economic institutions in African American communities, which themselves create more stable families, more prepared K–12 students, and more future college graduates. The system feeds itself when time is efficiently managed.

In the HBCU Money worldview, where institutional power is the only reliable safeguard against structural marginalization, time-to-degree represents one of the clearest and most overlooked levers of collective economic advancement. In a Financial Times context, the four-year graduation rate appears as a liquidity indicator—showing how quickly an institution converts educational investment into economic output. In The Economist’s framing, it reveals the mismatched capital structures between wealthy universities and historically underfunded ones, and how those mismatches reproduce inequality in slow, quiet, compounding increments.

For African America, the conclusion is unmistakable. The four-year graduation rate is not merely a statistic. It is a wealth mechanism. It is an endowment accelerator. It is an institutional survival tool. And it is a community-level economic strategy that begins in kindergarten and culminates with a diploma. If HBCU alumni wish to see their institutions strengthen, their communities accumulate wealth, and their young people enter the economy with maximum velocity, then they must make both K–12 investment and four-year graduation obsession-level priorities. Institutions rise with the financial stability of their graduates. Ensuring those graduates complete degrees on time is one of the most effective—and least discussed—strategies available for building African American institutional power across generations.

A Tale of Two Virginias:

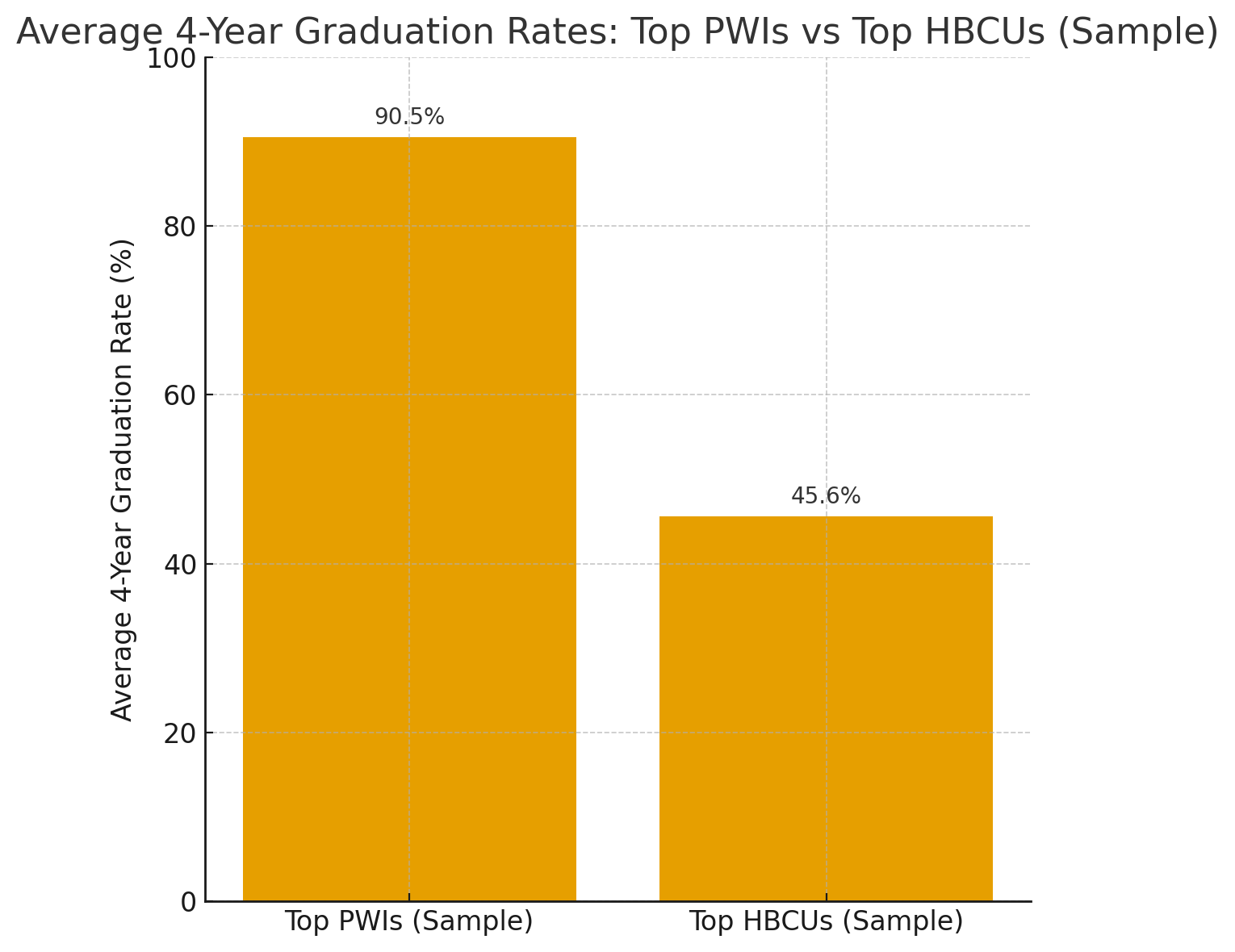

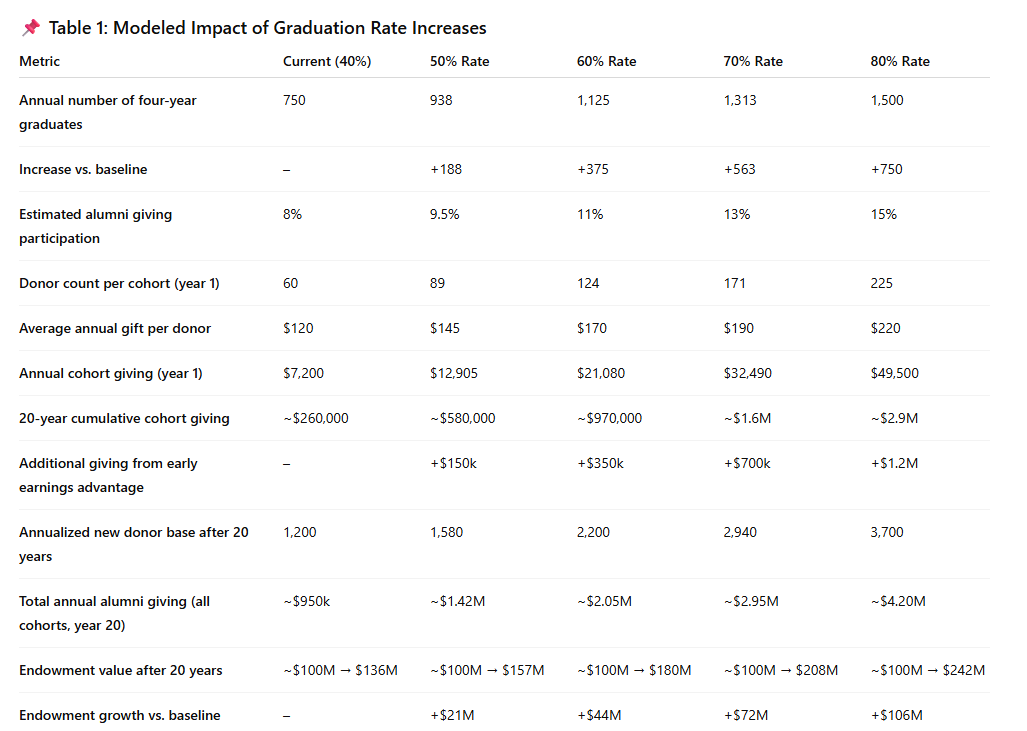

A revealing contrast in American higher education can be observed by examining two institutions that sit just 120 miles apart: Virginia State University (VSU) and the University of Virginia (UVA). NACUBO estimates VSU’s endowment at approximately $100 million for around 5,000 students, producing an endowment-per-student of roughly $20,000. According to U.S. News, VSU graduates 27% of its students in four years. UVA, one of the most heavily capitalized public universities in the world, possesses an endowment of roughly $10.2 billion for about 25,000 students, an endowment-per-student of approximately $410,000, more than twenty times the capital density VSU can deploy. Its four-year graduation rate stands at 92%.

The gulf between the two institutions reflects not a difference in student talent but a difference in institutional resource density and shock absorption capacity. A VSU student must personally carry far more academic and financial fragility. A single $300 expense can knock them off their semester plan. A delayed prerequisite can add a year to their degree. Limited advising bandwidth means problems are often discovered only after they have already extended time-to-degree. UVA faces the same categories of issues, but its endowment, staffing, and operating budgets act as buffers absorbing shocks before they disrupt academic progress.

Endowment-per-student, therefore, is not merely a balance-sheet statistic; it is a proxy for how much risk the institution can carry on behalf of its students. UVA carries most of the risk. VSU students carry most of their own. UVA’s 92% four-year graduation rate is a reflection of institutional cushioning. VSU’s 27% rate reflects its absence.

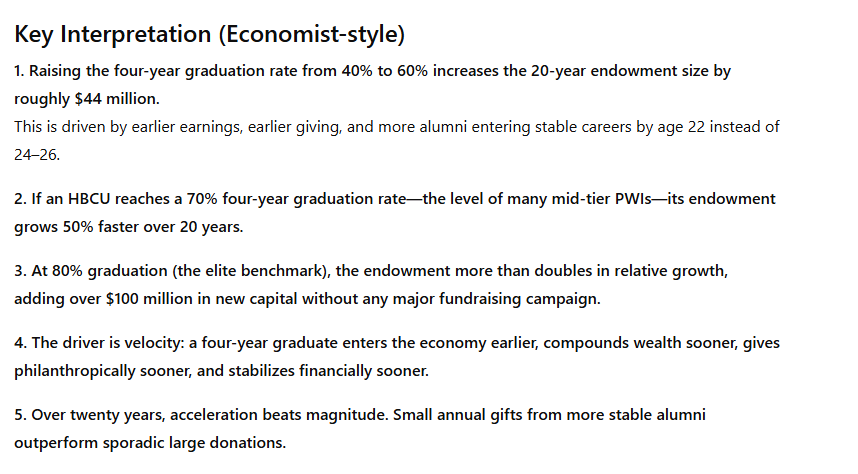

Yet to understand the true economic cost of the graduation gap, it is useful to model what would happen if VSU improved its four-year graduation rate—first to a plausible mid-term target such as 50%, and then to a UVA-like 90%. Both scenarios dramatically change the trajectory of the institution.

Assume that VSU today produces roughly 1,350 graduates every four years (based on a 27% rate). If it increased its four-year graduation rate to 50%, VSU would instead graduate 2,500 students every four years, an increase of 1,150 additional on-time graduates, each entering the workforce two years earlier, with lower student debt, earlier retirement contributions, earlier homeownership, and earlier philanthropic capacity. Even if only a modest fraction of these additional graduates contributed $50–$150 annually to VSU’s endowment, the compounding effect across 20 years would be substantial. Under conservative assumptions with basic donor participation growth and average returns of 7% VSU’s endowment could plausibly grow from $100 million to $155–$170 million over two decades, powered largely by the increased velocity and increased number of earning alumni.

Now consider the UVA-like scenario. A four-year graduation rate of 90% at VSU would mean roughly 4,500 on-time graduates every four years or over three times the current output. This scale of early, debt-lighter graduates would fundamentally transform VSU’s financial ecosystem. Even minimal alumni participation say, 12–15% giving $100–$200 annually would translate into millions in annual recurring contributions. Over two decades, with investment returns compounding, VSU’s endowment could grow not to $150 million but potentially to $300–$400 million, depending on participation rates and gift sizes. That would triple the institution’s financial capacity without a single major donor campaign, capital campaign, or extraordinary windfall. The key variable is simply graduation velocity.

This comparison illustrates a broader truth: endowment growth is not just a function of investment strategy but of how quickly a university converts students into earning alumni. A student who graduates at 22 gives for 40–50 years. A student who graduates at 25 gives for 30–35 years. A student who drops out does not give at all. VSU’s current 27% four-year graduation rate is not merely an academic statistic—it is an endowment drag factor. UVA’s 92% rate is an endowment accelerant.

The financial distance between the two universities appears vast, but it is governed by a formula that HBCUs can influence: more on-time graduates → more early earners → more consistent donors → more endowment growth → more institutional cushioning → more on-time graduates. VSU today sits at the fragile end of this cycle. A graduation-rate increase to 50% would move it into a position of stability. A leap to 90% would place it into an entirely different institutional category—one where it begins to accumulate capital in the same compounding manner that allows institutions like UVA to weather downturns, attract top faculty, and protect students from the shocks that so often derail academic momentum.

VSU cannot replicate UVA’s wealth in the short term. But by increasing on-time graduation, it can replicate the mechanism through which wealthy universities become wealthier. And that mechanism—graduation velocity—is one of the few levers fully within reach of alumni, leadership, and institutional partners.

Here are four strategic, high-impact actions HBCU alumni associations or chapters can take to directly raise four-year graduation rates and strengthen institutional wealth:

1. Create a Permanent Emergency Microgrant Fund (The “$300 Fund”)

Most delays in graduation arise from small financial shocks: balances under $500, transportation failures, book costs, or housing gaps.

Alumni chapters can formalize a permanent, locally governed microgrant fund offering rapid-response support (48–72 hours).

A chapter raising just $25,000 per year can prevent dozens of delays, each shielding students from additional semesters of debt and protecting the institution’s future alumni giving pipeline.

This is low-cost, high-yield institutional intervention.

2. Fund Paid Internships and Alumni-Mentored Work Opportunities

Students who work long hours off campus are more likely to fall behind academically, switch majors repeatedly, or extend enrollment.

Alumni chapters can create paid internships, stipends, or alumni-hosted part-time roles tied directly to students’ majors.

Each position:

reduces the student’s financial burden

keeps them academically aligned

accelerates pathways to stable post-graduate employment

This lifts graduation rates and increases alumni earnings—expanding the future donor base.

3. Build K–12 Pipelines in Local Cities That Feed Directly Into HBCUs

Four-year graduation begins long before freshman year.

Alumni chapters can adopt 2–3 local schools and support:

literacy acceleration programs

SAT/ACT prep

dual enrollment partnerships

STEM and robotics clubs

early-college summer institutes hosted by their own HBCUs

Better-prepared students require fewer remedial courses, retain majors longer, and graduate on schedule, raising institutional performance and future endowment sustainability.

This is pre-investment in the future alumni base.

4. Pay for Summer Courses After Freshmen Year to Build Early Credit Momentum

After their first year, many students fall off the four-year pace due to light credit loads, failed gateway courses, or sequencing issues that a single summer class could easily correct. Yet for many HBCU students, summer tuition—often just one or two courses—is financially out of reach.

Alumni chapters can establish a Freshman Summer Acceleration Grant to pay for up to two summer course immediately after freshman year, allowing students to:

close early credit gaps,

retake or accelerate critical prerequisites,

reduce future semester overloads,

create a credit cushion for unexpected disruptions,

stay aligned with four-year degree maps.

A small investment of summer tuition produces an outsized institutional return: students enter sophomore year on pace, avoid bottlenecks in upper-level coursework, and dramatically increase their likelihood of graduating in four years. This is an early-stage compounding effect—protecting momentum before delays become expensive and permanent.

“We must invest in ourselves. Without our own institutions, we will always be at the mercy of others.” – Mary McLeod Bethune

In the long arc of African American economic life, a recurring pattern emerges: the institutions most critical to our survival are consistently starved of capital, while the broader society thrives off of our labor, culture, and creativity. From Reconstruction-era mutual aid societies to the undercapitalized HBCUs of today, the struggle has never been whether African Americans are generous, but whether that generosity is systematically directed into institutions that can build durable power.

The Give Black App, founded by David C. Hughes, Alexus Hall, and Fran Harris, positions itself at this inflection point. It is not simply an app but a digital strategy—one attempting to reshape the flow of African American philanthropy and donations by curating, centralizing, and amplifying support for Black-led institutions.

The Context of Underfunding

African American nonprofits receive disproportionately less funding compared to their White counterparts. A 2020 Bridgespan study found that unrestricted net assets of White-led nonprofits were 76% larger than those of Black-led nonprofits, while revenues were 24% higher. These disparities compound over time. For HBCUs, the story is even starker: the endowments of all 100+ HBCUs combined is less than 1/10th of Harvard University’s alone.

Despite African America’s estimated $1.8 trillion in annual buying power, only a fraction is captured by its own institutions. Much of African American giving remains individual-to-individual or church-centered, providing immediate relief but not the kind of long-term institutional scaffolding needed to compete with White or global capital. Platforms like Give Black attempt to redirect that generosity into a framework where dollars reinforce permanence.

Building the Infrastructure of Giving

Give Black’s strength lies in infrastructure, a word often overlooked in philanthropy. The app operates as a digital gatekeeper, cataloguing Black-led nonprofits and enabling donors—whether individuals, alumni associations, or grassroots organizations—to find and fund them with ease.

This may seem simple, but its implications are profound. In an environment where discoverability is one of the greatest barriers for Black-led organizations, Give Black centralizes attention. For the countless nonprofits that lack robust marketing budgets, development officers, or national visibility, the app provides a seat at the table they would otherwise be denied.

The team itself reflects intentional design. Hughes, a Morehouse and Prairie View alumnus, carries the academic gravitas to engage institutions; Hall, with a background in cybersecurity and software sales, grounds the platform’s technical operations; Harris, a lifelong advocate of Black love and economic empowerment, provides the cultural grounding and marketing voice. Alongside them stand directors rooted in community engagement, finance, athletics, and science. Together, they represent a cross-section of African American life that mirrors the very community the app seeks to serve.

Philanthropy Meets Technology

Unlike GoFundMe or Benevity, which serve broad audiences, Give Black narrows its focus: African American-led institutions. This specificity is both its greatest strength and its potential vulnerability. By making African American philanthropy visible and trackable, the app attempts to normalize institutional giving within the community itself.

African American donors, long used to personal giving—funeral funds, tuition help, emergency assistance—are now asked to see their dollars not just as charity but as investment. An app that allows for transparency, accountability, and impact measurement may finally bridge the gap between intent and sustained institutional support.

Technology also democratizes giving. Younger generations, accustomed to digital wallets and mobile donations, are unlikely to write checks or mail contributions. By existing where they already transact, Give Black normalizes philanthropy as part of daily life. With proper marketing, it could serve as a digital equivalent of the collection plate—except one that sends dollars to Black think tanks, schools, health clinics, and endowment foundations rather than solely to Sunday offerings.

The Role of Fran Harris

Much of the initial confusion about Give Black’s leadership arises from Fran Harris’s name. She openly jokes about it—she is not the Fran Harris who was a WNBA champion or Shark Tank winner, though many assume otherwise. Instead, she distinguishes herself as someone whose “entire life has been about Black love and economic empowerment.”

That distinction matters. Whereas celebrity often drives visibility in African American philanthropy, Harris positions herself not as a star but as a steward of a broader vision. Her work focuses on the storytelling and cultural marketing needed to align African American giving with institutional capital. In a sense, her humor in addressing the name confusion underscores the seriousness of her actual role: grounding the app’s message in authenticity rather than celebrity.

The Gaps in the Strategy

Despite its promise, Give Black faces hurdles. First, fundraising expertise at the highest level appears limited within the core team. Major philanthropy is an industry of its own, requiring seasoned development officers capable of cultivating seven- and eight-figure gifts. Without this, Give Black risks becoming a platform for small-dollar giving—important, but insufficient for closing institutional capital gaps.

Second, technological depth must match ambition. While Hall’s cybersecurity background provides operational credibility, scaling a fintech-style platform requires CTO-level leadership. Issues of compliance, data integrity, and user trust are not optional—they are the foundation of sustainability.

Third, policy and compliance matter. Donations intersect with financial regulations, nonprofit law, and IRS oversight. To become the definitive gateway for Black giving, Give Black must not only build a sleek front end but also a back-end architecture that can withstand regulatory scrutiny and instill donor confidence.

Where the Opportunities Lie

The greatest opportunities for Give Black lie in institutional self-reliance.

One clear pathway is through alumni networks. HBCU alumni giving rates remain in the single digits, compared to 20–30% at elite PWIs. If Give Black positioned itself as the official conduit for alumni donations, it could help double or triple those rates over time. That alone would shift millions into endowments and operating budgets across the HBCU ecosystem.

Another opportunity lies in membership-based organizations—from professional networks to civic associations. Instead of dues going solely toward programming, portions could be funneled into long-term institutional giving through Give Black, creating a culture of collective philanthropy.

The Pan-African Diaspora represents yet another opening. African and Caribbean communities abroad are increasingly connected digitally. Give Black could expand to become a Pan-African philanthropic bridge, enabling solidarity between African Americans and global Black communities. Diaspora donors, often seeking trustworthy channels for giving, could find in Give Black a centralized, transparent platform.

Finally, the most transformative opportunity is to integrate endowment-building features directly into the app. Too much African American giving is trapped in the cycle of operating expenses. By redirecting portions of donations into permanent capital funds, Give Black could help institutions create reserves that outlast political climates and economic downturns.

Lessons from History

The urgency of Give Black’s mission must be seen against history. During the early 20th century, White-controlled philanthropy dictated the survival of many HBCUs. Institutions like Hampton and Tuskegee often relied on Northern industrialists whose donations came with ideological strings attached. The absence of African American-controlled philanthropic infrastructure meant dependency—and dependency always meant vulnerability.

Today, African American institutions still operate under the shadow of that dependency. Foundation funding remains racially skewed, and government support is often politically weaponized. Give Black, by offering a decentralized and community-driven alternative, challenges that cycle.

But history also warns: movements that lack discipline or scale are easily absorbed or ignored. Just as the Negro Leagues produced baseball talent but lacked the capital to maintain independence, so too can African American philanthropy generate excitement but fail to sustain institutional life if it is not channeled strategically.

The Verdict

Give Black App is not merely a digital donation tool. It is a test case: can African America leverage technology to redirect its wealth into its own institutions? The team’s composition, heavy in HBCU roots, marketing authenticity, and community engagement, suggests it understands both the stakes and the culture.

Still, the app must avoid the trap of becoming a feel-good project without measurable institutional outcomes. Its long-term success will be determined by whether it can:

Secure partnerships with HBCUs, alumni associations, and membership-based organizations.

Develop deep fundraising and compliance infrastructure.

Normalize institutional giving across African American households.

If it does, Give Black could evolve into a cornerstone of African American institutional development—a kind of digital Freedman’s Bureau, redistributing not charity but power.

For African America, the stakes could not be higher. In an era where White nonprofits sit on multibillion-dollar endowments, while Black nonprofits scrape for survival, the question is not whether we are generous. It is whether our generosity is building the kind of institutions that ensure survival for centuries, not just survival for today.

Give Black, if scaled with vision and discipline, may finally provide the infrastructure to answer that question with a resounding yes.