We are watching the absolute collapse of African American institutions and our absolute dependency on Others’ institutions. It once felt like a slow train wreck, now it feels like a supersonic missile. – William A. Foster, IV

The 2025 African American Owned Bank Directory carries an absence that numbers alone cannot fully convey. Two institutions that appeared in last year’s listing — Columbia Savings and Loan Association of Milwaukee, Wisconsin, and Adelphi Bank of Columbus, Ohio — are no longer among the ranks of African American-owned financial institutions. Together, they represented nearly $130 million in assets: Columbia Savings at approximately $22 million and Adelphi Bank at approximately $106 million. Their departure is not merely a bookkeeping change. It is a geographic and community wound, one that leaves both Ohio and Wisconsin without a single African American-owned bank.

Founded on January 1, 1924, Columbia Savings and Loan Association was one of the oldest African American-owned financial institutions in the United States. A savings and loan chartered over a century ago in Milwaukee, it survived the Great Depression, the urban upheavals of the mid-20th century, the savings and loan crisis of the 1980s, and the 2008 financial collapse. It did not survive 2025. In our 2024 directory, Columbia carried $24,097,000 in assets, already down 12.0 percent from the prior year. By the time 2025 data was compiled, its assets had further declined to approximately $21,998,000 — a figure that, alongside declining capital levels, signaled an institution under extraordinary strain. For a savings and loan of its size, operating in a competitive market without the capital buffers available to larger institutions, the math had become unforgiving.

Milwaukee’s African American community is substantial, Black residents make up roughly 39 percent of the city’s population and yet they now have no African American-owned bank to call their own. This is not a small thing. African American-owned banks and savings institutions have historically served as anchors for communities that mainstream financial institutions have underserved or outright ignored. They have written mortgages in redlined neighborhoods, provided small business loans to entrepreneurs who couldn’t get a second meeting at a downtown bank, and offered a financial home to people who needed more than a transaction they needed trust.

If the loss of Columbia Savings is a story of a century-old institution exhausted by time and capital constraints, the loss of Adelphi Bank carries a different kind of grief. Founded on January 18, 2023, in Columbus, Ohio, Adelphi was the newest African American-owned bank in the country at the time of our 2024 directory. Prior to its founding, no new African American-owned bank had been chartered in 23 years. Adelphi’s launch was celebrated for exactly that reason: it represented a renewal, a sign that the community had not given up on building the financial infrastructure it needs.

In 2024, Adelphi reported $68,154,000 in assets, up 55.1 percent from the year prior, a remarkable growth trajectory for a de novo bank. By 2025, that figure had risen further to $106,369,000. And yet, despite that asset growth, the bank was no longer majority African American-owned by the time 2025 statistics were compiled. A growing balance sheet does not automatically translate into ownership stability. New banks are capital-intensive, and the pressures to bring in outside investors can, over time, dilute or displace founding ownership structures.

The result is that Ohio, the state that just two years ago was celebrating the founding of its first new African American-owned bank in over two decades, now has none. Columbus, the state capital and one of the fastest-growing cities in the Midwest, has no African American-owned bank. And critically, neither does the surrounding region that includes two of Ohio’s most important Historically Black Colleges and Universities: Central State University and Wilberforce University.

The relationship between African American-owned banks and HBCUs has long been identified by HBCU Money as one of the most underdeveloped partnerships in the Black economic ecosystem. HBCUs are intellectual and economic anchors for their communities. African American-owned banks are the financial connective tissue that can translate education, entrepreneurship, and homeownership aspirations into capital. When both are present in a region, the possibilities compound. When one disappears, the other is diminished.

Central State University and Wilberforce University sit in Greene and Xenia, Ohio, both within the orbit of Columbus and Dayton. Their students, faculty, staff, and alumni represent tens of thousands of people who need mortgages, small business loans, car notes, savings accounts, and lines of credit. Without an African American-owned bank anywhere in Ohio, those needs will be met if they are met at all by institutions with no particular relationship to their communities, no cultural competency born of shared experience, and no structural incentive to reinvest in the neighborhoods and towns these HBCUs serve. And if they are met, the profits and institutional ownership and influence will be to the benefit of Others and not the African American ecosystem. Once again, we will be subsidizing everyone else.

This is not a hypothetical harm. Research has consistently shown that African American-owned banks direct a greater share of their lending to African American borrowers and African American-owned businesses than Others’ institutions. They are not perfect, and they are not substitutes for broader policy change. But they are irreplaceable in the role they play, and their absence is felt in the very specific, very practical ways that matter most: a loan denied, a mortgage not written, a business that never got started.

The 2025 directory does carry one encouraging entry: Redemption Bank of Salt Lake City, Utah, founded February 20, 1974, and now appearing in the African American-owned bank listing with approximately $72,205,000 in assets under the FDIC’s San Francisco region. Its inclusion partially offsets the $128 million in assets lost with Columbia and Adelphi. Redemption Bank’s presence in Utah is notable given the state’s relatively small African American population and its distance from the major African American economic corridors. Its listing is a reminder that African American financial institution-building can and does happen in unexpected places.

But Redemption Bank’s $72 million in assets does not replace what was lost in Ohio and Wisconsin. It does not fill the geographic gap. It does not serve the students at Central State or Wilberforce, or the African American residents of Milwaukee’s north side. The net loss to African American institutional financial capacity in the Midwest is real, and no amount of welcome news from the Mountain West changes the map that communities in Columbus and Milwaukee are now looking at.

As noted in our 2024 directory, African American-owned banks hold approximately $6.4 billion of America’s $23.6 trillion in bank assets — roughly 0.027 percent. The apex of African American-owned bank assets, as a share of total U.S. banking, was 1926, when the sector held 0.2 percent — ten times today’s proportion. Nearly a century later, the sector has not recovered.

The structural disadvantages are well-documented: chronic undercapitalization, concentration in communities with lower median wealth, limited access to the interbank credit markets that larger institutions tap freely, and a customer base that has been systematically excluded from wealth-building for generations. These are not problems that individual bank managers can solve through hustle and grit alone. They require deliberate policy support, sustained community deposits, and coordinated investment from the HBCU ecosystem, African American businesses, and public-sector partners.

The post-2020 wave of corporate pledges to African American financial institutions provided some relief. Many of the banks in our directory saw asset growth between 2023 and 2024 partly as a result of those deposits. But corporate commitments are not permanent, and the institutions that did not receive them or that received too little too late remained exposed. Columbia Savings, with $24 million in assets and a 12 percent annual decline already in evidence by 2024, was unlikely to attract the kind of large-scale corporate or philanthropic deposit that might have stabilized it.

The loss of Columbia Savings and Adelphi Bank should be understood as a call to action, not an occasion for eulogy alone. Several things must happen.

First, the HBCU community in Ohio must begin conversations now about what it would take to support a new African American-owned financial institution in the state. Central State and Wilberforce cannot simply wait for the private sector to solve this. HBCU endowments, alumni associations, and institutional deposits are tools of economic development. Directing even a fraction of those resources toward a future Ohio-based African American-owned bank would be a meaningful first step.

Second, community organizations, African American business associations, and civic leaders in Milwaukee must assess whether a new chartered institution, a credit union, or a community development financial institution (CDFI) can fill some of the void left by Columbia Savings’ departure. Milwaukee’s African American community is large enough and its economic needs acute enough that the absence of a community-controlled financial institution is not sustainable.

Third, the national conversation about African American-owned banks must move from celebration to infrastructure. Every time a new institution is chartered, and Adelphi’s founding in 2023 was genuinely exciting, it must be supported with the capitalization, deposit commitments, and technical assistance that give it a fighting chance past its first few years. A bank that grows in assets but loses its founding ownership structure has not fulfilled its promise. The community has to be in the room, and at the table, not just at the ribbon-cutting.

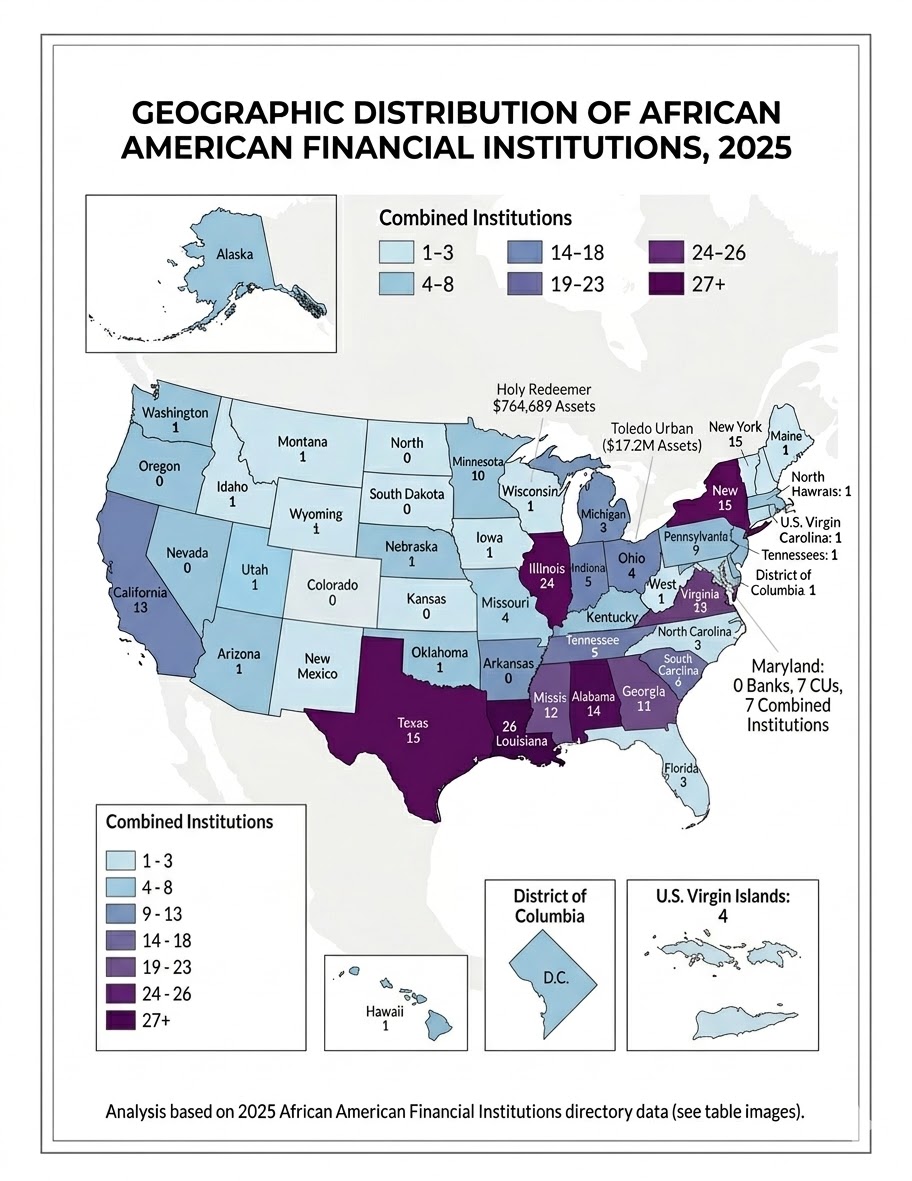

Finally, we should note what these two losses mean for the map of African American financial geography. States absent from our 2025 directory now include Ohio, Wisconsin, Maryland, Missouri, New York, and Virginia — a list that encompasses some of the largest African American urban populations in the country. That map is a challenge and an indictment in equal measure. African Americans live and work and build in every corner of this country. Their financial institutions should too.

Columbia Savings and Loan Association (Milwaukee, WI) — Founded January 1, 1924 | 2024 Assets: $24,097,000 | 2025 Assets: $21,998,000

Adelphi Bank (Columbus, OH) — Founded January 18, 2023 | 2024 Assets: $68,154,000 | 2025 Assets: $106,369,000

Redemption Bank (Salt Lake City, UT) — Founded February 20, 1974 | 2025 Assets: $72,205,000 [New to directory]

Disclaimer: This article was assisted by Claude (Anthropic).