“Since new developments are the products of a creative mind, we must therefore stimulate and encourage that type of mind in every way possible.” – George Washington Carver

In the financially stratified ecosystem of American higher education, institutions are increasingly confronted with a binary tension: to invest in athletic visibility or academic viability. For universities across the NCAA spectrum, especially those in the MEAC and SWAC conferences compared to their counterparts in the SEC and Big Ten, this decision is less about preference and more about resource constraints and strategic direction. Yet, data reveals a persistent imbalance in how these priorities manifest, and more critically, the long-term costs of these choices.

Conference Dynamics: Institutional Identity and Capital Exposure

The MEAC and SWAC are defined by institutions that are predominantly Historically Black Colleges and Universities (HBCUs). These universities have traditionally operated under capital scarcity, navigating chronic underfunding while serving as incubators of social mobility for African American communities. Their mission, often grounded in equity and community uplift, limits their ability to generate large commercial revenues through athletics. This is not due to a lack of talent or audience, but because media deals, booster contributions, and government funding disproportionately favor PWI institutions.

By contrast, the SEC and Big Ten represent the economic elite of collegiate athletics and academia. With flagship state universities at their helm, these conferences are buttressed by multi-billion-dollar endowments, large donor bases, and lucrative broadcast contracts. Their budgets allow for investments in both athletics and research without having to cannibalize one to fund the other. In essence, they play the game with more capital and fewer trade-offs.

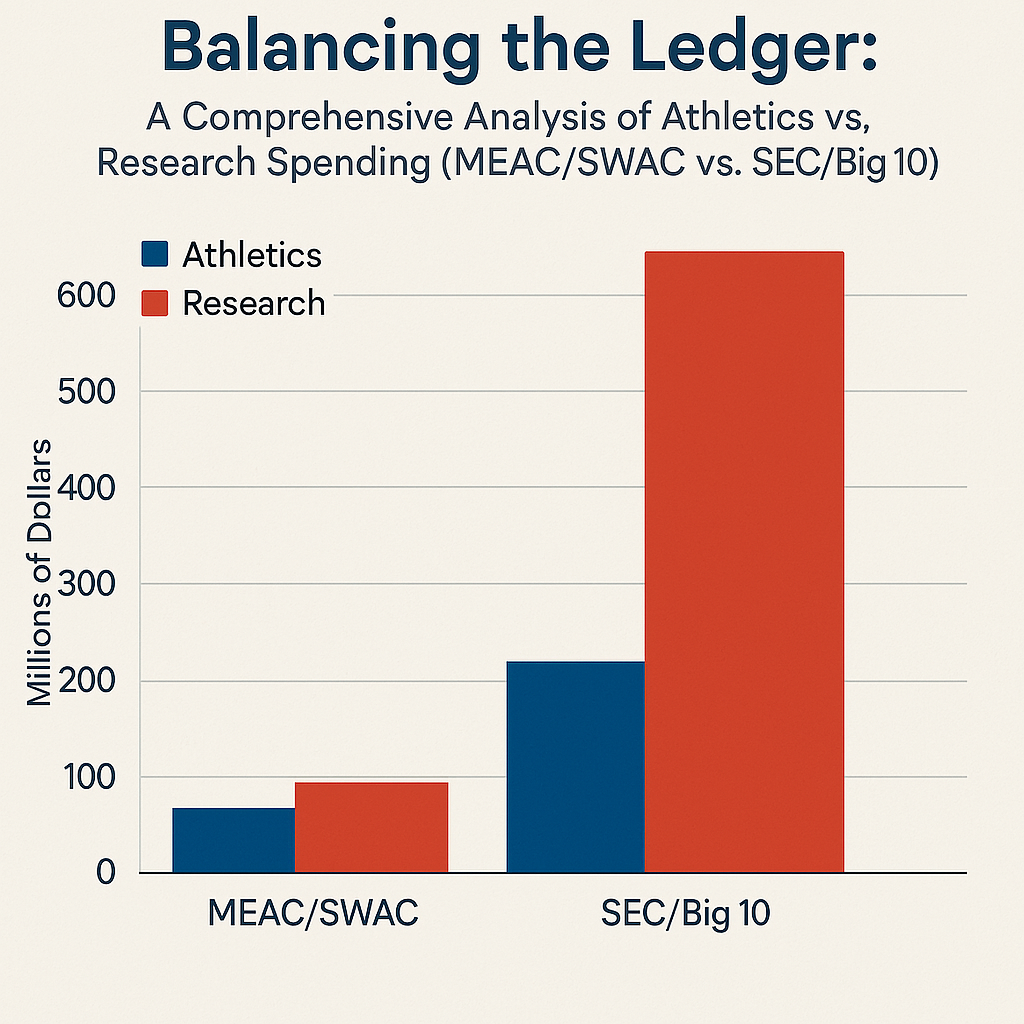

Athletics Budgets: Symbolism vs. Strategy

MEAC and SWAC institutions report average athletics expenditures between $11 million and $12 million annually. Notable programs like North Carolina A&T and Prairie View A&M may hover slightly higher, but Mississippi Valley State and others operate on budgets as low as $3.9 million. These figures pale in comparison to SEC schools like Alabama or Texas A&M, where athletic spending exceeds $150 million. The Big Ten’s Ohio State leads all with $215 million dedicated to athletics alone.

While athletic programs at HBCUs serve as cultural centers and enrollment drivers, their limited revenue-generating capacity renders them economically unsustainable without substantial subsidization. Many are forced to divert institutional funds, raise student fees, or solicit local donations just to keep programs afloat. In contrast, SEC and Big Ten programs function as media properties, brand engines, and financial assets, often contributing revenue back to their academic institutions.

Athletics at HBCUs carry significant intangible value, cultural pride, alumni engagement, community identity, but these cannot substitute for financial sustainability. The opportunity cost of maintaining expensive athletic programs without equivalent return on investment demands strategic scrutiny.

Research Spending: The Forgotten Core

Where the real divergence occurs is in research investment. MEAC and SWAC research expenditures are overwhelmingly modest. With the exceptions of Howard University ($122 million) and Florida A&M ($41 million), most institutions sit between $2 million and $25 million in annual research activity. These figures reflect decades of underinvestment and insufficient infrastructure, not a lack of capacity or talent.

Meanwhile, SEC and Big Ten institutions routinely surpass $500 million in annual research outlays. Schools like Michigan ($1.67 billion), Wisconsin ($1.36 billion), and Penn State ($996 million) operate on a scale comparable to government agencies and national labs. They attract large NIH, NSF, and Department of Defense grants. They lead clinical trials, generate patents, and build interdisciplinary research parks.

This disparity is not simply numerical; it is strategic. Research drives federal grants, patents, corporate partnerships, and endowment growth. It also attracts high-performing faculty and students, serving as the foundation of institutional longevity and economic influence.

The Ratio That Tells the Future

The athletics-to-research spending ratio offers a lens into institutional philosophy:

- Norfolk State: 2:1 athletics to research

- Jackson State: 0.7:1

- Mississippi Valley State: 6:1

- Alabama: 0.15:1

- Michigan: 0.11:1

- Wisconsin: 0.11:1

While SEC and Big Ten schools spend more on athletics than HBCUs, they also spend exponentially more on research. The imbalance within HBCUs is a reflection not of poor prioritization, but of systemic capital deprivation. These ratios also underscore how HBCUs are often forced to choose between visibility and viability, between entertainment and innovation, because they lack the financial bandwidth to pursue both.

Research as Revenue: Commercialization and the Innovation Economy

University research is not merely an academic endeavor it is a gateway to commercialization. Inventions born in labs often become patents. Patents become licensing agreements. Licensing revenue, in turn, flows back into the institution. The University of Florida’s development and commercialization of Gatorade yielded more than $280 million over time. Stanford’s involvement in launching Google and Hewlett-Packard has helped fuel its $36 billion endowment. Wisconsin’s WARF fund manages $4 billion in research-derived assets.

This model is not just aspirational; it is replicable. But replication requires infrastructure, policy, and intention.

Building the Infrastructure: A Two-Track Strategy for HBCUs

Campus Infrastructure

- Strengthen Technology Transfer Offices (TTOs): These serve as the conversion points from research to revenue. TTOs are responsible for managing patents, evaluating commercial potential, and negotiating licensing agreements.

- Invest in Innovation Facilities: Makerspaces, incubators, wet labs, and data science centers can all be built in underused buildings or retrofitted spaces.

- Embed Commercialization in Curriculum: Courses in IP law, venture creation, product development, and ethics should be available to both undergraduates and graduate students.

- Create Campus Accelerators: Provide seed funding, pitch competitions, and alumni mentorship. These accelerators can be industry-specific (e.g., AgTech at Tuskegee, FinTech at Howard).

- Celebrate Wins: Every patent, startup, or licensing deal should be internally recognized and externally marketed. Visibility breeds validation and investment.

Capital Infrastructure

- Black-Owned Banks: Offer startup lines of credit and financial education embedded in innovation ecosystems. These institutions can also hold endowment funds or manage cash flow from royalty revenues.

- Diaspora Sovereign Wealth Funds: Channel African and Caribbean capital into HBCU startups and joint ventures. Funds like Nigeria’s NSIA or Pan-African VC firms could provide growth capital.

- HBCU Venture & Endowment Funds: Seeded by Black VC firms, family offices, and institutional investors. These funds can create co-investment syndicates for promising faculty or student ventures.

- Donor-Advised Funds (DAFs): Enable alumni to contribute to IP pipelines through tax-efficient giving. DAFs could also be matched by corporate sponsors or philanthropic partners.

Building Strategic Partnerships for Scale

HBCUs need not operate in silos. Strategic collaboration can accelerate commercialization and R&D outcomes:

- Inter-HBCU R&D Collaboratives: Morgan State and FAMU could co-sponsor patent consortiums.

- Cross-registration commercialization programs with PWIs like Johns Hopkins or Emory.

- Statewide HBCU innovation districts tied to workforce pipelines and rural development.

From the Lab to the Ledger: Case Studies in ROI

- University of Florida – Gatorade: In the 1960s, UF researchers developed a hydration drink to help football players endure Florida’s brutal heat. The result, Gatorade, has yielded over $280 million in licensing revenue. These funds helped UF build research infrastructure, attract top scientists, and grow its endowment.

- Stanford University – Silicon Valley: Stanford was not always wealthy. Its proximity to innovation and its open policies toward student and faculty entrepreneurship led to the creation of Google, Cisco, and more. Today, Stanford’s alumni-founded companies generate trillions in global market value.

- University of Wisconsin – WARF: Established in 1925, the Wisconsin Alumni Research Foundation has monetized research in Vitamin D, stem cells, and imaging. With over $4 billion in assets, WARF reinvests in faculty, students, and commercialization pipelines.

- MIT – Ecosystem Builders: MIT’s Deshpande Center and The Engine Fund act as innovation pipelines that commercialize tough tech. MIT startups have created over 4.6 million jobs globally.

What HBCUs Must Avoid: Dependency Without Ownership

Too often, HBCUs have served as intellectual suppliers while other institutions and corporations reap the financial rewards. Faculty develop ideas, only for those patents to be captured by universities with larger TTOs. Students build prototypes, only to license them under incubators unaffiliated with their home campus.

To shift this paradigm, ownership must be embedded from the start. That means building institutional IP portfolios and teaching students the economics of invention.

A Circular Ecosystem Rooted in Culture and Capital

| Stakeholder | Role in the Pipeline |

|---|---|

| Black-Owned Banks | Startup capital, credit access, and embedded finance literacy |

| Diaspora Wealth Funds | Strategic investment, global partnerships, and joint IP deals |

| African American NPOs | Stakeholder investors, endowment builders, and R&D supporters |

| Black Media & Alumni | Narrative shaping, promotional power, and advocacy |

| HBCU TTOs & Leadership | Patent management, research development, and startup formation |

Final Calculations: Wealth Is Institutional, Not Individual

The data from MEAC, SWAC, SEC, and Big Ten schools paints a vivid picture of the financial landscape of higher education. While SEC and Big Ten schools show that it is possible to be excellent in both athletics and academics, MEAC and SWAC institutions face tougher choices due to structural inequalities and historical underfunding.

As conversations around equity, student success, and public accountability continue, this kind of comparative data is essential. Whether aiming for a championship or a Nobel Prize, universities must remember that their ultimate mission is to educate, innovate, and uplift communities.

University research isn’t just about publications and academic prestige it’s a launchpad for innovation, economic growth, and financial sustainability. When strategically supported, it becomes a core driver of commercialization, entrepreneurship, and long-term prosperity through patents and endowment growth.

Many HBCUs and smaller institutions already are incubators of brilliance but they’ve been left out of the research-to-wealth pipeline due to underfunding and limited infrastructure. With targeted investments and smart policy, they can flip the script and become not just engines of education, but engines of innovation and wealth creation.

Disclaimer: This article was assisted by ChatGPT.