All banks are listed by state. In order to be listed in our directory the bank must have at least 51 percent African American ownership. You can click on the bank name to go directly to their website.

KEY FINDINGS:

12 of the 16 African American Owned Banks saw increases in assets from 2024.

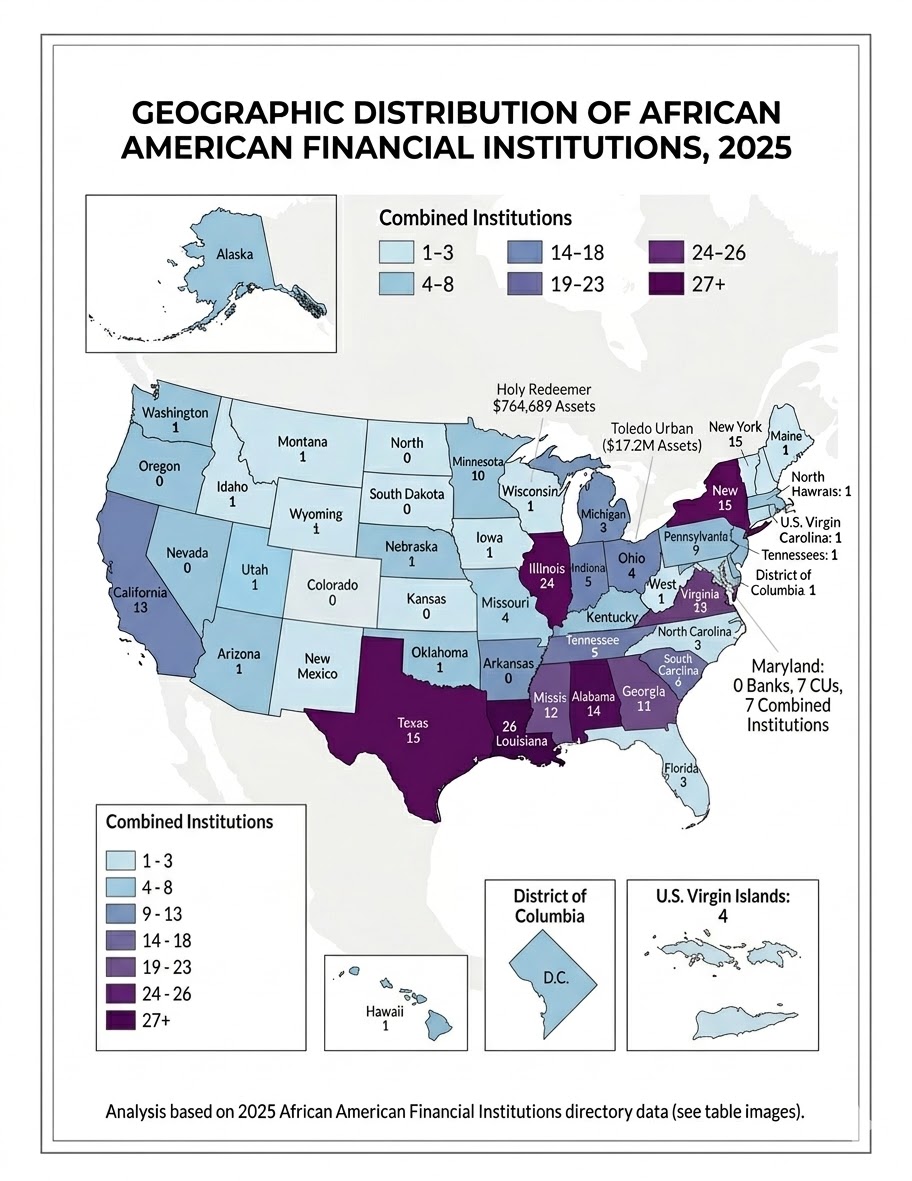

African American Owned Banks (AAOBs) are in 14 states and territories. Key states absent are Maryland, Ohio, Wisconsin, Missouri, New York, and Virginia.

With the loss of Adelphi Bank (OH) from majority African American ownership, no African American owned bank has been started in 26 years.

Alabama and Georgia each have two AAOBs.

African American Owned Banks have approximately $6.7 billion of America’s $24.9 trillion bank assets (see below) or 0.027 percent. The apex of African American owned bank assets was in 1926 when AAOBs held 0.2 percent of America’s bank assets or 10 times the percentage they hold today.

African American Owned Banks comprise 11 percent of Minority-Owned Banks (154), but only control 1.73 percent of FDIC designated Minority-Owned Bank Assets.

2025 Median AAOBs Assets: $255,112,000 ($191,590,000)

2025 Average AAOBs Assets: $395,554,000 ($355,448,000)

TOTAL AFRICAN AMERICAN OWNED BANK ASSETS 2025: $6,724,410,000 ($6,398,070,000)

African Americans navigating their financial lives are operating inside two fundamentally different types of institutions, and understanding that difference is not academic it is strategic. JPMorgan Chase, the largest bank in the United States with over $3.9 trillion in assets, is a publicly traded corporation owned by shareholders. Its mandate is profit. It can accept corporate deposits, underwrite municipal bonds, finance international trade, issue letters of credit that move goods across oceans, syndicate billion-dollar loans, and operate in 100 countries. When a city government needs to finance a new highway, when a developer needs to close on a $200 million mixed-use project, when a corporation needs to hedge currency risk across three continents — JPMorgan is in that room. Navy Federal Credit Union, the largest credit union in the United States with approximately $180 billion in assets, is a member-owned cooperative. Its mandate is service to its members, who must meet eligibility requirements tied to military affiliation. It offers mortgages, car loans, checking accounts, and credit cards often at better rates and lower fees than JPMorgan but it cannot write a commercial real estate construction loan for a developer, cannot underwrite a municipal bond for a city, cannot finance an export contract for a manufacturer shipping goods to West Africa, and has no presence in international capital markets. Navy Federal is a powerful institution for what it does. It simply does not do what JPMorgan does, and JPMorgan does not do what Navy Federal does at the community level. For African Americans, this distinction carries enormous consequence. A community with only credit unions has access to consumer financial products; mortgages, auto loans, personal savings but lacks the commercial banking infrastructure needed to finance business growth, real estate development, institutional deposits, and economic expansion. A community with only banks, and specifically only large national banks with no cultural accountability, has access to products but not necessarily to equitable underwriting, community reinvestment, or the trust that comes from shared ownership. The absence of an African American-owned bank in Ohio or Wisconsin is not just symbolic. It means no institution with a community mandate is positioned to finance the next African American developer, fund the next HBCU-adjacent business corridor, or serve as a depository for the growing institutional wealth of Black organizations in those states.

When the geography of African American banks and credit unions is examined together, a more complete — though still incomplete — picture of Black financial infrastructure emerges across the United States. The 2025 African American Owned Bank Directory covers 17 institutions across 15 states and territories. The 2025 NCUA data on African American credit unions adds 205 institutions across 29 states and territories, carrying $8.15 billion in assets and serving approximately 727,000 members. Combined, the two sectors represent over 220 institutions and more than $14.8 billion in assets operating across 31 states and territories. But geography, not just totals, is where the real story lives.

Thirteen states have both an African American-owned bank and at least one African American credit union: Alabama, the District of Columbia, Georgia, Illinois, Louisiana, Michigan, Mississippi, North Carolina, Oklahoma, Pennsylvania, South Carolina, Tennessee, and Texas. These are the states with the fullest financial ecosystem — where a community member can choose between a bank product and a credit union product from an institution with cultural roots in their community. Louisiana stands out, with one bank and 25 credit unions, the most of any state in the credit union count. Illinois follows with one bank and 23 credit unions.

Two states have African American banks but no African American credit unions in the NCUA data: Massachusetts, home to OneUnited Bank, and Utah, newly represented by Redemption Bank. These institutions serve their communities without the complementary infrastructure of a credit union network. Conversely, 16 states and territories have African American credit unions but no African American-owned bank: Arkansas, California, Connecticut, Delaware, Florida, Indiana, Maryland, Minnesota, Missouri, New Jersey, New York, Ohio, Virginia, the U.S. Virgin Islands, West Virginia, and Wisconsin.

The cases of Ohio and Wisconsin, discussed at length in the bank directory analysis, illustrate the limits of credit union coverage as a substitute for bank presence. Ohio has four African American credit unions with combined assets of approximately $18.3 million: Mahoning Valley in Youngstown, Mt. Zion Woodlawn in Cincinnati, Cleveland Church of Christ in Cleveland, and Toledo Urban in Toledo. Of these, Toledo Urban is the only institution of meaningful scale at $17.2 million in assets with 4,324 members. The other three are micro-institutions, each under $600,000 in assets and under 400 members. Wisconsin’s single credit union, Holy Redeemer Community of SE Wisconsin based in Milwaukee, holds just $764,689 in assets and serves 239 members. For a city where African Americans comprise roughly 39 percent of the population, that represents an institutional void that one small credit union cannot fill. Neither Ohio nor Wisconsin has an African American financial institution capable of writing a commercial real estate loan, funding a startup, or underwriting a mortgage for a first-generation homebuyer at any meaningful scale.

African American Financial Institutions by State, 2025

State

African American Banks

African American Credit Unions

Combined Institutions

Alabama

2

12

14

Arkansas

0

3

3

California

0

1

1

Connecticut

0

3

3

Delaware

0

1

1

District of Columbia

1

10

11

Florida

0

3

3

Georgia

2

9

11

Illinois

1

23

24

Indiana

0

5

5

Louisiana

1

25

26

Maryland

0

7

7

Massachusetts

1

0

1

Michigan

1

4

5

Minnesota

0

2

2

Mississippi

1

11

12

Missouri

0

4

4

New Jersey

0

9

9

New York

0

15

15

North Carolina

1

2

3

Ohio

0

4

4

Oklahoma

1

1

2

Pennsylvania

1

8

9

South Carolina

1

5

6

Tennessee

1

5

6

Texas

1

14

15

Utah

1

0

1

U.S. Virgin Islands

0

4

4

Virginia

0

13

13

West Virginia

0

1

1

Wisconsin

0

1

1

Maryland presents a striking and instructive contrast. It has no African American-owned bank, a gap noted in the 2025 directory, yet it is the single largest state for African American credit union assets, hosting seven institutions with a combined $4.47 billion in assets. That figure is driven primarily by two institutions: Andrews Federal Credit Union in Suitland with $2.47 billion in assets and 142,076 members, and Municipal Employees Credit Union of Baltimore with $1.26 billion in assets and 98,358 members. Maryland’s credit union sector is, in asset terms, larger than the entire African American bank sector nationally. This is remarkable. It is also a reminder that credit unions and banks occupy different structural roles. Andrews Federal and MECU of Baltimore are large, sophisticated institutions with product offerings that approach commercial banking but they are member cooperatives, not banks, and their ownership structure, regulatory environment, and community lending mandates differ accordingly. Maryland’s absence from the bank directory is still a gap worth addressing, even with $4.47 billion in credit union assets in the state.

Virginia and Missouri follow a similar pattern to Maryland, albeit at smaller scale. Virginia has 13 African American credit unions with $471 million in assets but no African American-owned bank. Missouri has four credit unions with $481 million in assets, anchored by St. Louis Community Credit Union at $431.5 million, and also no bank. New York has 15 credit unions with $76 million in assets and no African American bank, a particularly stark figure given the size of New York’s African American population and its status as the financial capital of the country.

The states that are entirely absent from both the bank and credit union directories deserve attention. While the combined coverage of 31 states and territories is broader than either sector alone, large portions of the country remain without any African American-owned financial institution. States like Nevada, Arizona, Colorado, Washington, Oregon, and much of the Mountain West and Pacific Northwest have no representation in either directory. As African Americans continue to migrate to new metros — Las Vegas, Phoenix, Denver, Seattle — the absence of community-controlled financial institutions in those corridors becomes a growing concern.

The combined picture is this: African American banks and credit unions together hold approximately $14.8 billion in assets, serve over 700,000 credit union members and the deposit base of 17 banks, and operate across 31 states and territories. The credit union sector, at $8.15 billion in assets across 205 institutions, is actually slightly larger than the bank sector’s $6.72 billion across 17 institutions, a reflection of the credit union model’s greater accessibility and the longer runway some of these institutions have had to grow. But the two sectors are not interchangeable. Banks can hold commercial deposits, write business loans, issue letters of credit, and serve as the financial backbone of an entrepreneurial ecosystem in ways that most credit unions cannot. Credit unions, in turn, offer member ownership, lower fees, and community accountability that publicly or privately held banks may not. The African American community needs both, in every state where its population is substantial. Right now, it has neither in too many places that matter.

Sources: HBCU Money 2025 African American Owned Bank Directory; 2025 NCUA African American Credit Union Institutions data. Asset figures in U.S. dollars.

Disclaimer: This article was assisted by Claude (Anthropic).

“Nobody ever helps me into carriages, or over mud-puddles, or gives me any best place! And ain’t I a woman?” – Sojourner Truth

An Analysis of How White Womanhood Receives Redemption While Black Women Face Permanent Condemnation

When Julia Roberts climbed into Richard Gere’s Lotus Esprit on Hollywood Boulevard in 1990’s Pretty Woman, she embarked on a journey that would transform her from streetwalker to America’s sweetheart. The film grossed $463 million worldwide, launched Roberts into superstardom, and cemented itself as one of the most beloved romantic comedies in cinematic history. But beneath its glossy veneer of designer shopping bags and opera dates lies a troubling reality: this fairy tale was only ever written for white women.

The premise is deceptively simple. Vivian Ward, a Hollywood prostitute, is hired by wealthy businessman Edward Lewis for a week of companionship. What begins as a transactional arrangement blossoms into love, culminating in Edward rescuing Vivian from her fire escape—the knight in shining armor arriving in a white limousine. The audience cheers. America swoons. And a sex worker becomes a princess.

Now, imagine if Vivian Ward had been Black.

Pretty Woman operates on a fundamental assumption: that its protagonist deserves redemption, transformation, and ultimately, love. Vivian is presented as a victim of circumstance, a woman who “ended up” in sex work, whose intelligence and charm were simply waiting to be discovered by the right man. The film invites us to see past her profession, to recognize her inherent worth, and to celebrate her elevation into respectability. This grace, the permission to be flawed, to make mistakes, to be seen as complex and worthy despite one’s past is a privilege historically reserved for white women in American culture. It is the same grace that allows a reality television star to build a billion-dollar empire after a sex tape, while a Black woman who tells her own story about the entertainment industry becomes permanently marked.

The comparison between Kim Kardashian and Karrine Steffans (also known as Elisabeth Ovesen) illuminates this disparity with devastating clarity. Both women became famous through their connections to the entertainment industry and their sexuality. Yet their trajectories could not be more different. In 2007, a sex tape featuring Kim Kardashian and singer Ray J was leaked to the public. Rather than becoming a scarlet letter, this moment became the launchpad for one of the most successful media empires in modern history. Kardashian settled her lawsuit against the distributor for a reported $5 million, and months later, Keeping Up with the Kardashians premiered on E!.

Today, Kardashian is a billionaire businesswoman worth an estimated $1.7 billion. She has founded multiple successful companies including Skims, valued at over $4 billion. She has graced the covers of Vogue, been named to Time’s 100 Most Influential People, and received the Innovation Award at the prestigious CFDA Awards. She is pursuing a law degree and advocates for criminal justice reform, meeting with presidents and earning praise for her activism. The media narrative around Kardashian has evolved from scandal to legitimacy, from reality star to mogul. While critics occasionally invoke her sex tape, it exists largely as historical context rather than permanent condemnation. She has been granted the space to grow, to rebrand, to become something more than her past. Like Vivian Ward, Kim Kardashian has been rescued not by a wealthy man, but by a culture willing to let her write her own redemption arc.

In 2005, Karrine Steffans published Confessions of a Video Vixen, a memoir detailing her experiences in the hip-hop industry, including her work as a video vixen and her relationships with various entertainers. The book became a New York Times bestseller and sparked important conversations about the exploitation of women in the music industry, power dynamics, and female agency. But unlike Kardashian’s ascent, Steffans faced immediate and sustained backlash. She was vilified, ostracized, and permanently labeled. In a recent interview with Essence magazine commemorating the 20th anniversary edition of her book, Steffans who now using her birth name, Elisabeth Ovesen—reflected on the devastating impact: “Make no mistake about it, the way the public has treated me, the way the press has treated me, and the way that everyone has talked about me, made up lies about me, vicious lies that are still circulating in the press today, have ruined a lot of my relationships.”

Ovesen describes two decades of being “physically and emotionally beaten by the people in my life” and fighting “to stay alive.” She notes that “there’s been this cloud over me for 20 years,” affecting her ability to work, to form relationships, to simply exist without the weight of public condemnation. The contrast is stark. Kardashian parlayed a sex tape into a multi-billion dollar empire. Steffans wrote about her own experiences and became a pariah. One woman was granted grace and opportunity; the other faced professional exile and personal destruction. The difference in their treatment cannot be separated from race. American culture has long operated on a racialized system of respectability politics in which white womanhood is protected, salvageable, and worthy of redemption, while Black womanhood is disposable, permanently marked, and beyond repair.

This dynamic is rooted in historical systems of oppression. During slavery, white women were placed on pedestals as symbols of purity that needed protection, while Black women were systematically raped and denied any claim to virtue or protection. These ideologies didn’t disappear with emancipation they evolved, shaping everything from Jim Crow laws to contemporary media representations. Pretty Woman is a cinematic embodiment of these racial hierarchies. The film’s entire premise depends on the audience believing that Vivian deserves to be saved, that her circumstances don’t define her worth, that she is capable of transformation. This narrative of redemption is inherently tied to her whiteness.

A Black Vivian Ward would never have made it past the hotel lobby. The same Rodeo Drive saleswomen who snubbed Vivian for her appearance would have called security. The opera patrons who glanced at her with mild curiosity would have stared with open hostility. And Edward Lewis—wealthy, powerful, white—would never have seen her as a potential partner worthy of rescue. More likely, she would have remained a transaction, an object, a stereotype. But here’s the deeper, more painful truth: even if Edward Lewis had been Black, the fairy tale likely still wouldn’t have worked. A wealthy Black businessman might have hired a Black Vivian for the week, might have enjoyed her company, might have been attracted to her but the progression from transaction to transformation, from escort to equal partner, from sex worker to wife would have been profoundly unlikely.

This isn’t speculation it’s a pattern borne out in real-world dynamics. Successful Black men, particularly those who have achieved wealth and status in predominantly white spaces, often internalize the same white supremacist beauty standards and respectability politics that devalue Black women. They pursue white partners as status symbols, as evidence of their arrival, as markers of their distance from the “ghetto” or the “struggle.” A Black woman with a complicated past, with a history of survival sex work, with anything less than a perfect respectability résumé, is often deemed unworthy of the ring even, and sometimes especially, by Black men.

The real-life example of Kim Kardashian demonstrates this dynamic perfectly. Kanye West, a Black man from Chicago’s South Side who achieved massive success in music and fashion, married a white woman with a publicly distributed sex tape, elevated her, celebrated her, called her his muse, and gave her his children and his name. He saw past her history to her potential as a partner. Meanwhile, Karrine Steffans, a Black woman who survived childhood rape, domestic violence, and exploitation in the same entertainment industry, has been systematically rejected, abused, and deemed unworthy of commitment by the Black men in her life.

This reveals something devastating about internalized racism and misogynoir (the specific hatred of Black women). Black men who would marry white women “despite” their pasts often cannot extend that same grace to Black women. The white woman’s transgressions are forgivable, even invisible as evidence of her complexity, her journey, her humanity. The Black woman’s identical or lesser transgressions are permanent stains as evidence of her unworthiness, her damage, her fundamental unfitness for respectability.

So even in an imagined version of Pretty Woman with a Black Edward Lewis, the barriers facing a Black Vivian would remain nearly insurmountable. He might desire her, might enjoy the fantasy, might even genuinely care for her but marry her? Introduce her to his business associates? Make her the mother of his children? The social, psychological, and cultural obstacles would be formidable. She would still be fighting against centuries of messaging that Black women are sexually available but emotionally disposable, useful for pleasure but unworthy of partnership, good enough for right now but never for forever.

Perhaps nowhere is this racialized double standard more painful than in the realm of romantic relationships with Black men. Kim Kardashian has been married to and in long-term relationships with multiple Black men, most notably music producer Damon Thomas (her first husband), NFL player Reggie Bush, and the aforementioned rapper Kanye West (with whom she had four children) and none of whom held her past against her. Her sex tape, her reality television persona, her public relationships none of these factors prevented her from being pursued, married, and elevated by Black men in the entertainment industry. Kanye West collaborated with her professionally, and defended her publicly. Their 2014 wedding in Florence was described by The New York Times as “a historic blizzard of celebrity.” Despite their eventual divorce, West treated Kardashian as worthy of commitment, partnership, and the prestige of his name. Her past was irrelevant to her worthiness as a wife and mother in his eyes.

In stark contrast, Karrine Steffans has faced systematic rejection and abuse from Black men, both publicly and privately. Ovesen describes in the Essence interview spending “a lot of the last 20 years being physically and emotionally beaten by the people in my life; by the men in my life, by my former husbands, by my fiancés, by people just really treating me like garbage everywhere I go.” The message is clear: a white woman with a publicly documented sexual past can marry multiple Black men and be treated as a prize. A Black woman who speaks honestly about her experiences in the same entertainment industry becomes unmarriageable, unworthy of basic respect, deserving of violence and abandonment.

This dynamic reveals a disturbing truth about how Black men despite their own experiences with racism often participate in the devaluation of Black women while extending grace to white women that they deny their own. The same men who might celebrate Kardashian’s beauty, entrepreneurship, and motherhood have labeled Steffans as damaged goods, a cautionary tale, someone who violated the code by speaking truth to power. This individual disparity reflects broader statistical realities about marriage and relationship opportunities for white versus Black women. According to sociological research, white women are significantly more likely to be married than Black women across all education and income levels. In fact, white women who enter into relationships with Black men have higher marriage rates than Black women generally, a devastating indicator of how racial hierarchies shape intimate partnerships.

Even when controlling for comparable backgrounds and circumstances, a white woman is more likely to secure marriage and long-term commitment than a Black woman. This reality holds true whether that white woman is partnering with a white man or a Black man. The common denominator is not the race of the male partner, but the racial privilege of white womanhood itself. Kardashian’s romantic history exemplifies this phenomenon. Despite a sex tape, despite a 72-day marriage that many suspected was a publicity stunt, despite the constant media scrutiny of her relationships and body, she has never struggled to find partners willing to commit to her. She has been engaged multiple times, married three times, and has consistently attracted high-profile men who treat her past as irrelevant to her present worthiness. Meanwhile, Ovesen notes that the cloud over her reputation “has stopped me from doing certain things and caused certain people to not want to work with me, be around me, or get to know me.” The permanent scarlet letter she carries has affected every aspect of her life, including her ability to form healthy romantic relationships.

This disparity speaks to how Black women are uniquely devalued in American society. They face discrimination from white men who may fetishize them but rarely see them as worthy of commitment. They face rejection from Black men who have internalized white supremacist standards of beauty and respectability. And they face judgment from society at large that denies them the grace, forgiveness, and second chances routinely extended to white women. The differential treatment of Kardashian and Steffans reveals the impossible bind facing Black women. When Kardashian capitalized on her sexuality and media attention, she was entrepreneurial, savvy, taking control of her narrative. When Steffans wrote honestly about her experiences in an industry that commodified her body, she was a “tell-all” author, a betrayer, someone who violated unspoken codes by speaking her truth.

This reflects a broader pattern in which Black women are held to standards that are simultaneously more rigid and more dismissive than those applied to white women. Black women must be twice as good to get half as far, yet even perfection offers no protection from racism and misogyny. And when women transgress respectability politics as both Steffans and Kardashian did, albeit in different ways only one is granted the opportunity for redemption. The Eurocentric beauty standards that pervade American culture compound this injustice. Pretty Woman‘s transformation scenes emphasize Vivian’s adherence to conventional (read: white) standards of beauty—her hair, her clothes, her manner of speaking. These scenes suggest that respectability and worthiness are achieved through proximity to whiteness. Black women navigating these same spaces face additional barriers. Natural Black hair is deemed “unprofessional.” Black bodies are simultaneously hypersexualized and demonized. Black women’s anger is characterized as threatening rather than justified. The path to respectability that Vivian walks is not available to women who cannot or will not conform to white cultural norms.

Pretty Woman ultimately sells a meritocratic fantasy: that Vivian’s intelligence, charm, and inherent goodness allow her to transcend her circumstances. It suggests that worth is innate and will be recognized by those with the power to elevate it. This is the American Dream in romantic comedy form. But this dream is not equally accessible. Ovesen’s experience demonstrates that Black women can possess all the talent, intelligence, and determination in the world and still face insurmountable obstacles not because they lack merit, but because the system is designed to exclude them.

Ovesen is a bestselling author who has written multiple books, including The Vixen Manual and The Vixen Diaries. She is a literary coach helping other writers. She has been in therapy since 2006, working on her healing and growth. Yet she remains defined by decisions made decades ago, unable to escape the narrative that was written about her rather than by her. Meanwhile, Kardashian who has faced her share of criticism has been allowed to evolve. She is a businesswoman, a mother, an advocate, a law student. Her past is acknowledged but doesn’t define her present. She embodies the Pretty Woman promise: that transformation is possible, that redemption is available, that one’s history doesn’t have to determine one’s future.

The 20th anniversary edition of Confessions of a Video Vixen arrives at a moment when conversations about women’s autonomy, exploitation in entertainment, and the power of storytelling are more urgent than ever. Ovesen’s reflections on her journey offer profound insights into the costs of truth-telling for Black women. “I believe in speaking up loudly and often, I believe in saying what’s true and what is right, no matter what the consequences are,” Ovesen told Essence. This courage to speak despite knowing the price, to refuse silence even when silence might have been safer deserves recognition and respect. Ovesen’s story also challenges us to reconsider whose narratives we celebrate and whose we condemn. Pretty Woman asks us to sympathize with a white sex worker, to root for her happy ending, to believe in her worthiness of love and transformation. Yet when a Black woman shares her own experiences navigating exploitation and commodification, she faces derision rather than empathy.

This double standard extends beyond individual women to shape cultural narratives about who deserves grace, who can be redeemed, and whose humanity is recognized. It reflects deeper structural inequalities in which Blackness and particularly Black womanhood is constructed as incompatible with innocence, worthiness, or complexity. Pretty Woman ends with Edward climbing Vivian’s fire escape, conquering his fear of heights to rescue the woman he loves. “She rescues him right back,” Vivian tells him, suggesting a partnership of equals. It’s a romantic conclusion that has captivated audiences for more than three decades. But this ending was never written for Black women. There is no knight coming to rescue Black women from systemic oppression, from racialized misogyny, from the impossible standards that demand perfection while denying opportunity. There is no fairy godmother to transform them, no shopping montage to signal their worthiness, no opera scene to demonstrate their hidden sophistication.

Instead, Black women like Ovesen must rescue themselves. They must heal in a world that continues to wound them. They must build lives and careers despite clouds that follow them for decades. They must center themselves, as Ovesen describes doing during the pandemic, because no one else will. “I spent a lot of the last 20 years being physically and emotionally beaten by the people in my life,” Ovesen shared. “I’ve just been fighting to stay alive, and it wasn’t until the pandemic that I was able to hyperfocus on my healing.” Her survival is its own form of triumph, even if it looks nothing like Hollywood’s version.

Thirty-five years after Pretty Woman premiered, we must reckon with the stories we tell and whose experiences they center. We must examine the grace we extend to some women while withholding it from others. We must acknowledge that race fundamentally shapes whose humanity is recognized, whose past can be overcome, and whose future holds possibility. Kim Kardashian’s success is not illegitimate (but even that is worthy of discussion) she has demonstrated business acumen, resilience, and strategic thinking. But her trajectory has been facilitated by structural advantages unavailable to Black women in similar circumstances. Her story is a Pretty Woman narrative because she had access to the grace economy, the benefit of the doubt, the cultural permission to evolve beyond her past.

Karrine Steffans deserves that same grace. So do countless other Black women who have been denied the opportunity to grow, to change, to be seen as more than their worst moments or their most difficult circumstances. Their stories matter. Their humanity matters. And the systems that determine whose redemption is possible and whose is permanently out of reach must be challenged and dismantled. The fairy tale ending of Pretty Woman was never meant for everyone. But perhaps it’s time to stop accepting that inequality as inevitable and start demanding that grace, opportunity, and redemption become truly universal. Because every woman regardless of race deserves the chance to rescue herself and be rescued in return.

Disclaimer: This article was assisted by ClaudeAI.

In 2024, Apple quietly killed its electric vehicle project. After nearly a decade of speculation, leaked prototypes, and engineering talent poached from Detroit and Stuttgart, the announcement arrived with a shrug. Markets barely moved. What looked like a retreat was, on closer inspection, something more interesting — a door left open to a far more consequential ambition.

Apple was never going to win by building another car. The automotive market is brutally competitive, capital-intensive, and increasingly commoditised at the electric end. Tesla, BYD, and Rivian are fighting that war. The smarter bet — and the one Apple is uniquely positioned to make — is building the platform that makes car ownership less necessary in the first place.

This is not a utopian argument. It is a business one.

The global infrastructure gap is estimated at $94 trillion by 2040, according to the World Bank. American water systems lose roughly 6 billion gallons of treated water daily through deteriorating pipes. The U.S. electrical grid, designed for a centralised fossil fuel economy, is structurally ill-suited for the distributed renewable future that both climate policy and energy economics now demand. Passenger rail — a basic connective tissue across Europe and Asia — remains an afterthought across vast stretches of the United States. Traffic congestion drains an estimated $179 billion from the American economy annually in lost time and fuel. Vehicle emissions contribute to more than 60,000 premature deaths each year in the U.S. alone.

These are not niche concerns. They are the failing arteries of modern life. And very few companies on earth are better positioned than Apple to redesign them.

Apple already integrates hardware, software, and services with a precision that no competitor has matched at scale. Its chip design produces some of the most energy-efficient processors ever built. Its cloud infrastructure, sensor technology, and payment systems span billions of devices across every continent. Its supply chain discipline and design sensibility are, by any measure, world-class. The question is not whether Apple has the capability to enter the infrastructure space. The question is whether it has the strategic imagination to try.

Consider transit. Apple would not need to lay track, operate buses, or run a single vehicle. What it could build is the operating layer — AI-optimised routing drawing on Apple Maps data, seamless ticketing through Apple Wallet, personalised journey planning through Siri, real-time crowd flow management at interchange hubs, and demand-responsive electric shuttles for lower-density districts. The iPhone would become, in effect, a passport to a life less dependent on car ownership — and all the financial and environmental costs that car ownership imposes.

The economics of this argument are well established, even if they remain politically underappreciated. Every dollar invested in public transit generates roughly five dollars in broader economic returns, according to the American Public Transportation Association. Transit-oriented development raises property values, expands tax bases, and improves labour market access for workers priced out of car ownership. Cities that invest in dense, multimodal systems reduce emissions, reclaim public space, and generate measurable public health gains. The infrastructure of movement is not a social expenditure. It is a productive one.

The opportunity extends beyond transit. Apple’s energy-efficient chip architecture translates naturally to smart grid management, where modular, predictive systems are precisely what is needed to integrate distributed solar, battery storage, and dynamic demand response. Apple sensors and cloud infrastructure already exist at the scale required to monitor water systems in real time — detecting pipe failures, tracking quality, and optimising pressure through smart valves. Apple Pay processes billions of transactions. The components for an Apple Water platform or an Apple Grid service layer are, in many respects, already assembled. What is missing is the strategic decision to point them at a larger problem.

The water case is particularly stark. The U.S. Environmental Protection Agency estimates that $472 billion in maintenance investment is required over the next twenty years simply to sustain existing water infrastructure — before a single mile of new pipe is laid. Globally, nearly one in three people lacks reliable access to safe drinking water. The market for intelligent water management — leak detection, quality monitoring, pressure optimisation — is enormous and structurally underserved. Apple’s skill in miniaturising technology, combining sensors with privacy-grade cloud processing, and delivering consumer-grade interfaces for complex data makes it an unusually credible entrant.

For Apple, the strategic logic is also a defensive one. iPhone sales have plateaued. Its Services division faces antitrust scrutiny across multiple jurisdictions. Its cash reserves — exceeding $160 billion — are an asset in search of a return that consumer electronics can no longer reliably provide. Infrastructure, by contrast, offers recurring revenue through service agreements and municipal contracts, structural diversification away from device cycles, and long-term relevance at a civilisational rather than product level. The infrastructure market is not glamorous. But it is enormous, it is durable, and it is ripe for the kind of systemic redesign that Apple has historically done better than anyone.

The risks are genuine and should not be minimised. Apple is famously secretive, consumer-oriented, and averse to the slow-moving regulatory complexity that infrastructure demands. City contracts are messier than product launches. Margins are narrower. Failures are public and politically costly. But Apple has navigated hostile regulatory environments before — in financial services, in healthcare, in China. Its high public trust and strong ESG record are genuine assets in a domain where government partnerships require demonstrated credibility over time. And crucially, Apple would not need to own pipes, track, or transmission lines. It would build the intelligent systems layered atop them — and license those systems to governments, utilities, and citizens at scale.

The model already exists in adjacent industries. Schneider Electric and Siemens have built large, profitable businesses selling digital operating layers to physical infrastructure owners. Veolia manages water and energy systems for municipalities across the developed and developing world. These are not Apple-scale companies in terms of design capability or brand trust. Apple entering this space would not be a departure from what it does. It would be an extension of it — at a higher level of ambition.

What would this look like in practice? In dense cities, an Apple Transit platform could reduce car usage, lower emissions, and return public space to pedestrians and parks. In smaller cities and rural regions — places too dispersed for high-frequency bus networks but underserved by the on-demand platforms that have flourished in major metros — demand-responsive electric shuttles dynamically routed through Apple Maps could reconnect communities that car dependence has quietly strangled. In energy markets, an Apple Grid service could allow households to manage solar and storage through iOS, enable peer-to-peer energy trading between neighbours, and give grid operators the real-time visibility they need to prevent blackouts in a renewables-heavy system. In water, an Apple Water platform could give cities the predictive maintenance tools they currently lack, and give households transparent, real-time visibility into their consumption and the health of their local system.

None of this requires Apple to become a utility or a transport operator. It requires Apple to become what it has always been at its best: the company that builds the operating system everyone else runs on.

Steve Jobs once described the computer as a bicycle for the mind — a tool that amplifies human capability far beyond what either could achieve alone. The infrastructure of the coming century needs exactly that kind of amplification. Roads that manage themselves. Grids that think. Water systems that speak before they fail. Transit that fits around people’s lives rather than demanding they organise their lives around it.

The real disruption in mobility is not a better electric vehicle. It is a better alternative to vehicles altogether — and the broader infrastructure intelligence that makes modern life function without the waste, the inequity, and the environmental cost that the 20th century model baked in.

Apple has the cash, the capability, and the moment. The question is whether it has the ambition to match.

Disclaimer: This article was assisted by ClaudeAI.

Timidity does not inspire bold acts. – Dr. Mae Jemison

The college fair model is broken — at least for HBCUs. Here’s how alumni chapters can build a pipeline that starts long before a student ever picks up a brochure. Walk into any college fair in a major American city and you’ll find the same scene: rows of tables draped in school colors, stacks of glossy brochures, and admissions representatives competing for the attention of juniors and seniors who, by that point in their academic journey, have already largely made up their minds. For predominantly white institutions with billion-dollar endowments and national name recognition, the college fair model works well enough. For Historically Black Colleges and Universities, it represents a fundamental misalignment between the urgency of the moment and the passivity of the approach.

HBCU enrollment has seen encouraging upticks in recent years, but the long-term pipeline challenge remains real. Alumni chapters, often the most energized, locally embedded advocates for their institutions are still overwhelmingly operating in reactive mode. They show up to fairs. They host the occasional scholarship gala. They cheer at homecoming. What we are not doing, with nearly enough intentionality, is going to where the students are, years before those students are old enough to apply. That has to change. And the blueprint for changing it is hiding in plain sight.

Imagine walking down a commercial corridor in Atlanta’s West End, Houston’s Third Ward, Baltimore’s Park Heights, the five buroughs in New York, or Chicago’s South Side and seeing a storefront with the colors and seal of a prominent HBCU. Inside, a welcoming space offers something radical in its simplicity: free help.

Help filling out college applications. Help navigating the FAFSA. Tutoring for high school students. Information sessions on academic programs, scholarship opportunities, and campus life. GED preparation for adult learners. GMAT and GRE prep for prospective graduate students. A community room where a kid can sit down after school and do homework, surrounded by images of Black excellence in cap and gown.

This is not a fantasy. It is a strategic infrastructure play that HBCU alumni chapters can begin building right now and the financial logic is stronger than many chapters realize.

Alumni chapters that have built up reserves, or that are willing to pool resources with neighboring chapters, should be actively exploring storefront leases in high-traffic African American neighborhoods. The cost of leasing modest commercial space in many urban corridors, while not trivial, is within reach for chapters with organized fundraising operations. More importantly, this model transforms the alumni chapter from a social organization into a community institution — and community institutions attract donors, partnerships, and long-term sustainability.

For chapters with the financial sophistication and appetite, ownership rather than leasing should be the goal. A storefront property that houses an HBCU recruitment and support center is also a real estate asset. It appreciates. It can be refinanced. It generates community goodwill that translates into alumni donations and corporate sponsorships. Forward-thinking chapters should be thinking about their real estate portfolio the same way a small nonprofit thinks about its balance sheet — as a long-term instrument of mission and sustainability.

But the case for ownership goes well beyond the chapter’s balance sheet. When an HBCU alumni chapter purchases a commercial property in a Black neighborhood, it is making a statement that is felt far beyond the four walls of the building. Vacant storefronts are one of the most visible symptoms of disinvestment in African American communities. They signal to residents, businesses, and young people that nobody believes in the block — that the neighborhood is somewhere to leave, not somewhere to build. An alumni chapter that acquires and activates one of those properties is doing something that no amount of college fair attendance can accomplish: it is demonstrating, physically and permanently, that Black institutional investment is real.

This is the chapter functioning as a community developer — not just a recruiter. The presence of a professionally staffed, well-maintained HBCU center on a commercial corridor raises the standard for the surrounding block. It attracts foot traffic. It gives neighboring businesses a reason to invest in their own storefronts. It signals to prospective residents and entrepreneurs that the community has anchors worth building around. Property values in the immediate vicinity benefit. The narrative of the neighborhood begins to shift.

Alumni chapters that think this way are not simply supporting their alma mater — they are exercising the kind of place-based economic power that Black communities have historically been denied. Every dollar that goes toward acquiring and improving a property in the community stays in the community. The chapter builds equity. The neighborhood builds stability. And the students who walk through that door every day see, in the most tangible terms possible, what organized Black investment looks like. That lesson alone is worth the price of the building.

Chapters that cannot yet afford standalone locations should explore co-location models: shared space with Black-owned businesses, community centers, or even jointly operated centers with two or three HBCU chapters that maintain separate branding but share overhead. A joint Virginia State-Morgan State-Cheyney recruitment center in a major metro is not just a cost-saving measure — it is a statement about the HBCU ecosystem as a unified force.

The single biggest reason community-based recruitment initiatives fail is that they are built on volunteerism alone. Volunteers are essential — but they cannot open the doors at 9 a.m. on a Tuesday, maintain records, follow up with prospective students, or manage institutional partnerships. A storefront that is going to deliver consistent, professional service to the community needs a full-time core team. It does not need to be large. It needs to be right.

The foundation of the storefront operation is the Executive Director / Center Director, a full-time salaried role that carries the weight of the entire operation. This person manages the relationship with the alumni chapter board and the parent institution, oversees staff, builds and maintains community and school district partnerships, and is ultimately responsible for the center’s recruitment numbers and programming outcomes. This is not an entry-level position. The ideal candidate has a background in higher education administration, community organizing, nonprofit management, or some combination of the three — and they are a proud, vocal HBCU product. Salary range: $70,000–$80,000 depending on market and chapter resources.

Supporting the director is a Recruitment and Admissions Counselor, a full-time role dedicated entirely to student-facing work. This person guides prospective students through the entire application process — from first contact to submitted application to financial aid completion. They manage the center’s student database, track pipeline metrics, and are the primary point of contact for high school counselors and community college advisors in the region. A background in college admissions or student affairs is ideal, and again, HBCU alumni status is a meaningful qualification. Salary range: $60,000–$68,000.

The third full-time position is a Financial Aid and Resource Navigator. The financial aid process is where more students fall out of the pipeline than anywhere else — not because they cannot afford college, but because the system is confusing, intimidating, and unforgiving of missed deadlines. This staff member specializes in FAFSA completion, scholarship identification, financial literacy education, and connecting adult learners with workforce funding and employer tuition benefits. They serve every lifecycle stage the center touches. A background in financial aid administration, social work, or community financial services is the right profile. Salary range: $60,000–$68,000.

These three full-time positions form the operational spine of the storefront. Beyond them, part-time staff and alumni volunteers extend the center’s capacity without extending its payroll. A part-time academic tutor or tutoring coordinator — ideally a current graduate student or recently graduated HBCU alumna — can run afternoon and evening tutoring sessions. Alumni volunteers with professional backgrounds in law, medicine, business, and education rotate through the center for workshops, panel discussions, and one-on-one advising sessions. A volunteer coordinator role, which can be managed by the Executive Director in the early stages, ensures that the volunteer corps is organized, scheduled, and recognized for their contributions.

The total full-time annual personnel cost for the storefront, including modest benefits, runs approximately $190,000–$220,000. That is a real number, and chapters should treat it as such when approaching their institution, corporate partners, and grant funders. It is also the number that separates a serious operation from a well-intentioned hobby.

For communities and schools that cannot easily access a storefront location, the chapter must come to them. This is where the concept of the HBCU mobile recruitment unit becomes a game-changer.

Alumni chapters should be looking seriously at purchasing used charter or transit buses and retrofitting them as mobile engagement vehicles. The cost of a used bus is often in the range of $30,000 to $80,000 depending on age and condition, with retrofitting adding additional investment. But the return in community presence, recruitment reach, and alumni chapter identity is enormous.

A properly outfitted mobile unit becomes a rolling admissions office. Equipped with laptops, tablets, printed materials, and onboard programming capability, the bus can park outside middle schools during dismissal, set up at community festivals and church parking lots on weekends, and roll through neighborhoods that college admissions representatives have never set foot in. It can run FAFSA completion workshops at community centers, host financial literacy sessions for parents, and bring the campus — virtually, through screens and presentations directly to families who may have never considered that a college education is within their reach.

A bus without a dedicated crew is a very expensive parking lot ornament. The mobile unit, to function as a true outreach vehicle rather than an occasional showpiece, requires its own committed staffing structure — lean but professional.

The non-negotiable full-time role is the Mobile Outreach Coordinator, who is simultaneously the unit’s program lead and its logistical engine. This person owns the deployment schedule, manages school district and community partner relationships, leads or facilitates on-site programming when the bus is in the field, and tracks every student interaction for follow-up and pipeline reporting. Critically, they serve as the bridge between the bus and the storefront — ensuring that students engaged in the field are handed off cleanly into the center’s formal services. This role requires someone who is equally comfortable presenting to a room of eighth graders, negotiating access with a school principal, and updating a CRM database. Salary range: $55,000–$65,000.

The second essential role is the full-time Commercial Driver / Logistics Coordinator. This is not simply a bus driver. The right person for this role holds a commercial driver’s license (CDL) and also takes ownership of vehicle maintenance scheduling, equipment inventory, and supply logistics for the unit. On deployment days, they are a visible, welcoming presence — often the first face a student or parent sees when approaching the bus. Many alumni chapters will find this person within their own membership: a retired transit worker, a logistics professional, or a veteran with transportation experience who is deeply invested in the mission. Salary range: $45,000–$55,000.

These two full-time positions are the core of the mobile unit. On high-volume deployment days — school visit days, large community events, or multi-stop weekends — part-time Recruitment Ambassadors supplement the crew. These are ideally current HBCU students or recent graduates who can speak authentically to the college experience, assist with application and FAFSA walkthroughs on the bus’s onboard stations, and engage peers in a way that no administrator can replicate. They are paid hourly and scheduled based on the deployment calendar.

The storefront’s Recruitment and Admissions Counselor and Financial Aid Navigator should also rotate onto the bus for targeted events — particularly FAFSA completion drives and high school senior nights — ensuring that students who need deeper guidance get it in the field, not just at a fixed location.

The full-time annual personnel cost for the mobile unit runs approximately $100,000–$140,000, excluding the bus acquisition and retrofit. Chapters that operate both a storefront and a mobile unit under one organizational roof — sharing the Executive Director’s oversight and administrative infrastructure — realize meaningful efficiencies. The combined full-time staff across both operations totals five to six people, with a total annual personnel investment in the range of $300,000–$400,000. That is a community development organization of real consequence, and it should be funded and governed as one.

The most important shift in mindset this article is calling for is one of timeline. HBCU alumni chapters cannot afford to think of recruitment as something that begins in 11th grade. The pipeline has to start much earlier — and it has to serve learners at every stage of life.

Head Start (Ages 0–5): Before a child ever sets foot in a kindergarten classroom, their relationship with learning and with the adults who shepherd it is already being shaped. This is why HBCU alumni chapters must engage Head Start programs, and why that engagement represents one of the highest-leverage opportunities in the entire pipeline.

Head Start is the federal early childhood program serving primarily low-income children ages birth to five, and Black children are among its most significant constituencies. According to the most recent federal program data, 29 percent of Head Start enrollment is Black or African American, non-Hispanic making it one of the largest organized points of contact with Black families in America at the earliest stage of a child’s development. Yet the program is dramatically under-serving the eligible population it is meant to reach: nationally, only 54 percent of eligible Black children are served by Head Start preschool, a gap driven in part by residential segregation and the uneven geographic distribution of Head Start centers.

That gap is itself an opportunity for HBCU alumni chapters. A storefront-based center located in a Black community can serve as a trusted navigator helping families find, apply for, and access Head Start services while simultaneously introducing those same families to the HBCU pipeline that begins long before a child can read.

The engagement strategy at this stage is not academic. It is relational. Head Start programs already operate with a strong family engagement model — approximately 378,000 adults volunteered in their local Head Start programs in a recent program year, of whom 295,000 were parents of Head Start children. Alumni chapters should be plugging into that existing network of engaged parents, not waiting for those parents to find them. Partnering with local Head Start centers to host family nights, read-aloud events, and college aspiration programming for parents creates touchpoints that are warm, community-rooted, and years ahead of any college fair.

The parents of Head Start children are also, frequently, prospective students themselves. Many are in their twenties or early thirties, may have some college credit, and are navigating the competing demands of parenthood and economic insecurity. An HBCU alumni chapter that shows up at a Head Start family event with information about degree completion programs, flexible scheduling, financial aid for adult learners, and the life-changing potential of an HBCU education is not just planting seeds for the next generation — it is recruiting for this one. The storefront’s Financial Aid and Resource Navigator is a natural liaison here, building relationships with Head Start family service coordinators who are already helping parents navigate social services and can add educational pathways to that conversation.

Alumni chapter members who are educators, social workers, pediatricians, or child development professionals should be the face of this engagement. Reading to children at a Head Start center, facilitating a workshop for parents on school readiness and early literacy, or simply being a visible, joyful presence in the community establishes the HBCU brand as one that cares about Black children from the very beginning not just when they are old enough to fill out an application.

Elementary School (K–5): The goal at this stage is not recruitment it is aspiration. But there is a deeper and more urgent reason why HBCU alumni chapters must show up here: elementary school is where the majority of Black boys are lost academically, and the window to intervene is narrow.

The data is unambiguous and devastating. According to the National Assessment of Educational Progress, only about 17 percent of Black fourth-grade students are reading at or above grade-level proficiency. For Black boys specifically, the numbers are worse. Only 13 percent of fourth-grade Black boys scored proficient in reading on the NAEP, compared to 40 percent of fourth-grade White boys. Research from the Annie E. Casey Foundation shows that children who are not reading proficiently by third grade are four times more likely to drop out of high school. And the cliff is steep: schools stop teaching children how to read after third grade and expect them to read to learn — for Black boys who missed early reading milestones, the system rarely slows down to help them catch up.

The academic struggle is compounded by the discipline crisis that runs parallel to it. Black boys represent just 8 percent of total K–12 enrollment but account for 15 percent of students receiving in-school suspensions and 18 percent of those receiving out-of-school suspensions. It starts before kindergarten: Black boys account for 9 percent of preschool enrollment but represent 23 percent of preschool children who received one or more out-of-school suspensions. Every day a Black boy spends outside the classroom is a day the reading gap widens. Black boys lost 132 days of instruction per 100 students enrolled due to out-of-school suspensions — a staggering accumulation of lost learning that trails these students for years. The research also shows that Black boys are markedly less likely to be subjected to exclusionary discipline when taught by Black teachers — a finding that speaks directly to the power of representation, and to what an HBCU alumnus standing in a classroom or community center can mean to a young Black boy who has rarely seen himself reflected in a position of educational authority.

This is why HBCU alumni chapters must be present in elementary schools — not with brochures, but with people. Reading programs, mentorship initiatives, and “college visit days” that introduce young children to the very concept of higher education are not extracurricular niceties; they are interventions. Seeing an HBCU alumnus or alumna in a professional role, wearing their school colors, and speaking with pride about their college experience plants a seed that can survive years of discouragement and doubt and provides a counter-narrative to a system that, by fourth grade, has already written too many Black boys off. Chapters should be cultivating relationships with school principals and PTA organizations to create recurring, sustained programming access. The presence has to be consistent, not occasional. A single visit does not change a trajectory. A relationship does.

Middle School (6th–8th Grade): By middle school, academic identity is forming and peer influence is at its peak. This is the moment to introduce students to HBCU culture, legacy, and opportunity in a way that makes it feel aspirational and cool. Alumni chapters should be running summer enrichment programs, college campus tours, and after-school STEM or arts programming tied to their institution’s academic strengths. Students who visit an HBCU campus at age 13 are far more likely to apply at 17.

High School (9th–12th Grade): This is the traditional recruitment window, but even here the storefront and mobile unit models change the game. Rather than waiting for students to find them at a fair, chapters are already embedded in these students’ communities. The work at this stage is conversion: helping students who are already HBCU-curious move through the application process, understand their financial aid options, and see themselves as belonging on campus. Chapters should have alumni assigned as informal advisors to high school college counselors — a presence that keeps HBCUs top of mind when counselors are guiding students toward school lists.

Adult Learners and Working Professionals: The traditional 18-to-22 pipeline is not the only one that matters. Millions of Black adults in American cities have some college credit but no degree. Alumni chapters that operate storefronts can become hubs for adult learner recruitment — connecting prospective students with their institution’s degree completion programs, online offerings, and evening or weekend formats. The FAFSA is available to adult learners. Institutional scholarships often target this population. Alumni chapters are uniquely positioned to be the trusted intermediary that convinces a 32-year-old with two kids and a job that finishing their degree is still possible.

Transfer Students: Community colleges in major metros serve enormous numbers of Black students who are academically capable of completing a four-year degree. Alumni chapters should have formal relationships with the counseling offices of every community college in their region, providing materials, hosting information sessions, and facilitating articulation agreement information that helps students understand how their credits will transfer to an HBCU.

Prospective Graduate Students: HBCUs are increasingly building out competitive graduate and professional programs. Alumni chapters can serve this market by hosting networking events that connect Black professionals with information about MBA, law, public health, and social work programs at their institution. The storefront model works exceptionally well here: an evening panel of HBCU-credentialed professionals discussing the value of their graduate degree, hosted at a community location, is both a recruitment event and an alumni engagement opportunity.

None of this is free, and alumni chapters should be honest with themselves about the resource requirements. A combined storefront and mobile operation with a full-time staff of five to six people, housed in leased or owned commercial space, represents a total annual operating budget — personnel, facilities, programming, and vehicle costs — likely in the range of $400,000 to $550,000 depending on market. That is a real community development organization, and it needs to be funded like one.

The good news is that the funding landscape is more favorable than many chapters realize — particularly for chapters willing to do the work of building a formal organizational structure, a board of directors, and a documented impact model.

Corporate partners, particularly those with HBCU engagement programs, represent another significant funding channel. Black-owned businesses in the communities where storefronts would operate should be natural co-investors: they benefit from a more educated local workforce and a more vibrant community anchor institution. Faith communities, which often have both facilities and congregational fundraising capacity, are underutilized partners for HBCU alumni chapters in nearly every city.

State and federal workforce development funding including Workforce Innovation and Opportunity Act dollars can support adult learner programming and the Financial Aid Navigator role at storefront locations. Chapters with 501(c)(3) status or fiscal sponsorship arrangements can access this funding stream, as well as philanthropic grants from foundations focused on educational equity, Black wealth building, and community development. The mobile unit may also qualify for transportation equity and community access grants available through state education agencies and private foundations.

Here is the harder conversation that most alumni chapters are not having: grants run out, corporate partners change priorities, and institutional support is subject to the whims of university budget cycles. Any operational model built entirely on external funding is one budget cut away from collapse. The chapters that will sustain these operations for decades not just launch them with fanfare are the ones that build their own financial engine.

This means HBCU alumni chapters need to stop thinking of themselves purely as fundraising organizations and start thinking of themselves as investors. The distinction is critical. Fundraising asks others to fund your mission. Investing builds assets that fund your mission in perpetuity.

The first and most immediate step is the establishment of a formal chapter endowment. An endowment is not a reserve fund or a savings account, it is a permanently invested pool of capital whose principal is kept intact while the annual investment income is distributed for operations and programs. Most endowments are designed to keep the principal corpus intact so it can grow over time, while allowing the nonprofit to use the annual investment income for programs and operations. A chapter endowment seeded with $500,000 and professionally managed at a conservative annual return of 5 percent generates $25,000 per year in perpetuity — money that never has to be raised again. Scaled to $2 million, that is $100,000 annually without a single grant application. The endowment is built through major gifts from alumni, planned giving and bequest programs, proceeds from chapter events reinvested rather than consumed, and targeted endowment campaigns run every three to five years.

Beyond the endowment, chapters with the organizational maturity to do so should be seriously exploring the creation of a dedicated investment arm, a separate but affiliated entity structured as a 501(c)(3) foundation or a for-profit LLC depending on the chapter’s strategic goals, whose mandate is to build and manage a diversified portfolio of assets that generates income to fund chapter operations and community programs. Most endowments are set up as separate entities from the nonprofit they support, paying formal grants to the nonprofit, with a structure that requires a separate board of directors, officers, mission statement, and internal policies. This structure gives the investment arm its own governance, its own fiduciary standards, and its own identity while keeping the mission connection to the chapter clear and documented.

What does the portfolio of an HBCU alumni chapter investment arm look like in practice? Good old stocks and bonds to begin with to get the asset train rolling. Real estate comes next as a natural mission-aligned asset class as discussed. The storefront properties this article has already discussed are the starting point but the vision should not stop there. A chapter that owns its storefront, then acquires a second commercial property that it leases to a Black-owned business, then participates as a co-investor in a mixed-use affordable housing development in its target community, is building a real estate portfolio that generates rental income, appreciates in value, and reinforces the chapter’s identity as a community developer. Every property the chapter owns is a statement that Black institutional capital is permanent in this neighborhood.

Beyond real estate, chapter investment arms should be exploring mission-aligned equity investments in Black-owned businesses, HBCU-affiliated startups, and community development financial institutions. Alumni Ventures, a model pioneered in the broader higher education alumni space, has demonstrated that alumni funds can blend community focus with rigorous portfolio construction, leveraging deal flow to ensure quality and diversification. An HBCU alumni chapter investment fund that pools capital from members with minimum investment thresholds accessible to working professionals, not just the wealthy — democratizes wealth-building while directing capital toward enterprises that reflect the community’s values.

The chapters that will build these operations are the ones that stop thinking of themselves as social clubs with a community service component and start thinking of themselves as the community development and wealth-building arm of one of America’s most important institutional legacies. The storefront and the mobile unit are the mission. The endowment and the investment portfolio are what keep the mission alive when the grants run out and the corporate partners move on. Both are necessary. Neither is optional.

Every year that HBCU alumni chapters spend waiting at tables at college fairs is a year that students who could have found their way to a transformative HBCU education do not. The competition for Black students is fierce, well-funded, and increasingly present in the very communities where HBCUs have historically drawn their greatest strength.

The answer is not to compete on those terms. The answer is to go deeper, go earlier, and go to where the community lives. Storefronts and mobile units are not just recruitment tactics they are acts of institutional love and community investment. They say, loudly and visibly, that this HBCU is not waiting for students to find it. It is coming for them in the best possible way.

Alumni chapters have the people, the passion, and increasingly the resources to make this happen. What they need now is the will to think bigger than a folding table and a stack of brochures.

HBCU Money is the leading personal finance and business news platform focused on the HBCU community. To learn more about HBCU financial strategies, alumni engagement, and institutional development, visit hbcumoney.com.

Ideas that extend the physical infrastructure already proposed:

1. HBCU Alumni Chapter Media Studio — A small podcast/video production corner inside the storefront that creates original content: student success stories, “day in the life” campus videos, financial aid explainers, and alumni career spotlights. Content goes directly to YouTube, TikTok, and Instagram and keeps the chapter’s brand alive in the community 24/7 — long after the doors close. It serves as a recruitment tool that never sleeps and costs relatively little to set up.

2. Career and Internship Pipeline Desk — A formalized partnership structure between the storefront and local employers, specifically focused on creating internship and first-job pathways for HBCU students and graduates. The storefront becomes a local talent pipeline desk — something corporate partners can co-fund in exchange for access to HBCU talent. This also keeps alumni coming back after graduation and turns the center into a lifelong resource, not just an admissions office.

3. HBCU Health and Wellness Partnership — Several HBCU alumni alliances already do this. Given that health disparities in Black communities are severe, the storefront can host free health screenings, mental health workshops, and wellness programming co-sponsored by HBCU nursing and public health programs. This embeds the storefront even deeper in community trust and brings in foot traffic from people who may not initially be thinking about college at all — but who are now in the building.

Ideas that use the alumni chapter’s organizational capacity:

4. Returning Citizens / Reentry Pipeline — Formerly incarcerated individuals represent one of the most underserved and educationally motivated populations in Black communities. HBCUs that accept returning citizens and the Pell Grant restoration (reinstated in 2023) make this timely. The storefront is a natural hub for partnering with reentry organizations to connect this population with HBCU degree programs, adult learning pathways, and financial aid navigation.

5. HBCU Alumni Chapter Financial Cooperative — Rather than each chapter independently funding operations, HBCU chapters in a metro area or region could form a financial cooperative or CDFI (Community Development Financial Institution) to pool capital for real estate acquisition, bus purchases, and storefront buildouts. This turns the funding challenge from a per-chapter burden into a shared institutional strategy.

6. “HBCU House” Cultural Programming — Modeled loosely on cultural centers that exist in cities, the storefront runs regular cultural programming — film screenings, lectures, art exhibitions, Juneteenth and Black History Month events — that make it a destination even for community members with no immediate college interest. The goal is sustained foot traffic and community ownership of the space. The people who come for the film screening become the people who bring their kids back for tutoring.

Disclaimer: This article was assisted by ClaudeAI.