The United States, a land famed for its abundance and ambition, sits atop one of the most valuable portfolios of real estate in the world. From the towering commercial properties of Manhattan to the suburban sprawl of Phoenix and the vast, untouched stretches of prairie and desert in between, the collective valuation of U.S. real estate has breached an astonishing threshold: $100 trillion.

According to recent estimates, the total value of U.S. residential real estate hovers around $50 trillion, while commercial real estate accounts for an additional $22.5 to $26.8 trillion. Less visible but equally consequential is the nation’s unimproved land—agricultural acreage, forests, deserts, and raw parcels—with a market value estimated at $23 trillion. Together, these segments reveal a profound truth about the American economy: it is built quite literally on a foundation of land wealth that continues to define its structure, resilience, and long-term power.

The Residential Bedrock

Homeownership, long considered the American Dream, is more than a cultural aspiration—it is the foundation of household wealth and the gravitational center of the U.S. economy. Redfin estimates that American homes are now worth a cumulative $50 trillion, a figure that has surged nearly 50% since 2020, when the pandemic-era monetary policy and fiscal stimulus unleashed a flurry of homebuying and refinancing activity.

This valuation includes not only primary residences but also investment properties and vacation homes. Approximately 65% of Americans own homes, and for most, their house remains their single largest asset. According to the Federal Reserve’s Survey of Consumer Finances, real estate comprises more than 50% of household net worth among the middle class, making housing prices not just a matter of market speculation but a critical economic indicator.

But the recent surge in interest rates has cast a shadow. The Federal Reserve’s aggressive tightening campaign to combat inflation has pushed mortgage rates above 7%, slowing home sales and triggering price corrections in overheated markets. Nevertheless, inventory shortages and strong labor markets have kept residential property values elevated. Analysts believe this plateau—rather than a crash—will be the new normal, as housing markets recalibrate in a high-rate environment.

Commercial Real Estate’s Reckoning

The U.S. commercial real estate (CRE) market, estimated to be worth between $22.5 trillion and $26.8 trillion according to the Federal Reserve Bank of St. Louis, finds itself at a crossroads. Office towers, retail strips, multifamily developments, and industrial warehouses are being repriced in real time as remote work, e-commerce, and rising interest rates challenge legacy models.

Office vacancies in major cities like San Francisco, Chicago, and Washington, D.C. have climbed to record highs—some surpassing 30%—as companies consolidate physical footprints. This has sparked what some are calling a “silent crisis” for CRE. Valuations have dropped precipitously in certain metro areas, and regional banks with significant exposure to commercial mortgages have found themselves vulnerable.

But it is not all doom and gloom. Industrial and logistics properties—particularly those near ports, rail hubs, and urban fulfillment centers—continue to outperform, benefiting from the growth of e-commerce and reshoring of manufacturing. Meanwhile, multifamily housing has emerged as a relative safe haven, with demand bolstered by rising mortgage costs that have priced many out of homeownership.

Institutional investors, from pension funds to private equity giants, are rebalancing portfolios, shedding underperforming assets while doubling down on high-performing sub-sectors. The great repricing of commercial property could ultimately yield a leaner, more sustainable industry.

America’s Undervalued Treasure: Unimproved Land

Beyond the skyscrapers and suburbs lies the nation’s quietest giant—its unimproved land, whose estimated value of $23 trillion remains largely outside the public imagination. This figure, derived from the Bureau of Economic Analysis and academic research, encompasses the total value of raw, undeveloped land, including forests, deserts, wetlands, farmland, and government-owned acreage.

Unimproved land is often overlooked in discussions of wealth, yet it plays a central role in climate resilience, national food security, conservation, and future development. It is the terra firma upon which cities expand, solar farms rise, and conservation easements are negotiated. It also serves as collateral in trillions of dollars of financing across industries.

Yet unlike residential and commercial properties, unimproved land lacks a robust national marketplace or transparent pricing. It is often subject to local zoning laws, speculative investment, and environmental regulation—making it both a store of untapped value and a highly complex asset class. With climate change accelerating, land with access to water, resilience to extreme weather, and proximity to urban centers is already commanding premium valuations.

Land is also becoming a focus for sovereign wealth funds, family offices, and climate-conscious investors. “Farmland and timberland are now being seen as long-duration, inflation-resistant assets,” says Daniel Krueger, managing director of a Colorado-based land investment firm. “We’re at the early stages of a global land rush driven by food, carbon, and water scarcity.”

A National Portfolio of Strategic Assets

Taken together, the U.S. real estate sector functions as a $100 trillion national portfolio, integral not just to individuals and corporations but to the state itself. Local governments rely on property taxes for more than 70% of their operating budgets, while real estate assets underpin infrastructure financing through municipal bonds. The U.S. government also owns about 640 million acres of land—roughly 28% of the country—much of which is leased for energy, timber, and recreation, generating billions in annual revenue.

Real estate also serves as the backbone of U.S. capital markets. Mortgage-backed securities, REITs, and land-based derivatives are woven into the financial system, linking Wall Street to Main Street. In a typical year, real estate transactions account for more than 17% of GDP when including construction, financing, insurance, and brokerage services.

Yet this vast portfolio is not without its vulnerabilities. Natural disasters, rising sea levels, zoning bottlenecks, affordability crises, and infrastructure underinvestment all threaten the productivity of American land. Moreover, decades of racially discriminatory policies in housing and land access continue to cast a long shadow, leaving millions of Americans excluded from the benefits of land ownership.

The Geopolitics of Land

In a global economy defined increasingly by resources, logistics, and sovereignty, America’s real estate advantage is also geopolitical. With a vast and varied landscape, stable legal system, deep capital markets, and strong property rights, U.S. land remains an attractive destination for foreign capital. Investors from Canada, Germany, Singapore, and the Middle East have spent billions acquiring trophy assets in cities like New York, Los Angeles, and Miami, as well as farmland in the Midwest and ranches in Texas.

But the rise of China, strategic concerns around food and data security, and the politicization of foreign ownership have made real estate an arena of national interest. Several states have passed or are considering legislation restricting land purchases by foreign governments or their proxies. Meanwhile, the Committee on Foreign Investment in the United States (CFIUS) has widened its scope to include real estate transactions near sensitive military or infrastructure sites.

These developments suggest a growing recognition that land—long viewed as inert and apolitical—is in fact a strategic resource requiring oversight and planning.

The Sustainability Imperative

In the 21st century, the full value of real estate can no longer be measured in dollars alone. Sustainability, resilience, and carbon sequestration are emerging as parallel dimensions of value. Developers are increasingly required to meet environmental standards, and landowners are being incentivized to conserve forests, wetlands, and grasslands as carbon sinks.

The Inflation Reduction Act of 2022 poured billions into climate-smart land use initiatives, including tax credits for renewable energy on farmland and funding for urban tree canopies. These programs aim to make the American landscape more resilient while tying land use directly to climate goals.

Urban planning is also being reimagined. Cities like Portland, Denver, and Austin are investing in zoning reform to allow for greater density, affordability, and transit-oriented development. Meanwhile, rural communities are embracing land trusts and cooperative ownership models to prevent land loss and promote inclusive growth.

The Repricing of the American Dream

As the United States approaches a new demographic, environmental, and economic era, the notion of land as a static store of wealth is evolving. The repricing of American real estate—spurred by demographic shifts, financial innovation, and climate change—will redefine value for the next generation.

For homeowners, it means contending with climate risk disclosures and insurance volatility. For developers and institutional investors, it entails navigating rising construction costs, policy uncertainty, and ESG mandates. For policymakers, it means rethinking land taxation, infrastructure planning, and public land stewardship.

Yet the fundamental truth remains: the United States possesses one of the most valuable and versatile land portfolios in the world. With judicious management, equitable access, and forward-looking investment, that $100 trillion empire can continue to generate prosperity for decades to come.

In an age of intangibles—from cloud computing to cryptocurrencies—the solidity of land and property remains unmatched. America’s $100 trillion real estate empire is not just a measure of wealth; it is a reflection of national identity, economic philosophy, and strategic foresight. How the country chooses to steward this land—who gets to own it, how it is used, and whether it serves the public good—will shape the next chapter of the American experiment.

Sidebar: By the Numbers – U.S. Real Estate Valuations

Residential Real Estate: $50 trillion (Redfin, 2024)

Commercial Real Estate: $22.5–$26.8 trillion (Federal Reserve Bank of St. Louis, 2024)

Real Estate Contribution to U.S. GDP: ~17% (including indirect industries)

In an age of intangibles—from cloud computing to cryptocurrencies—the solidity of land and property remains unmatched. America’s $100 trillion real estate empire is not just a measure of wealth; it is a reflection of national identity, economic philosophy, and strategic foresight. How the country chooses to steward this land—who gets to own it, how it is used, and whether it serves the public good—will shape the next chapter of the American experiment.

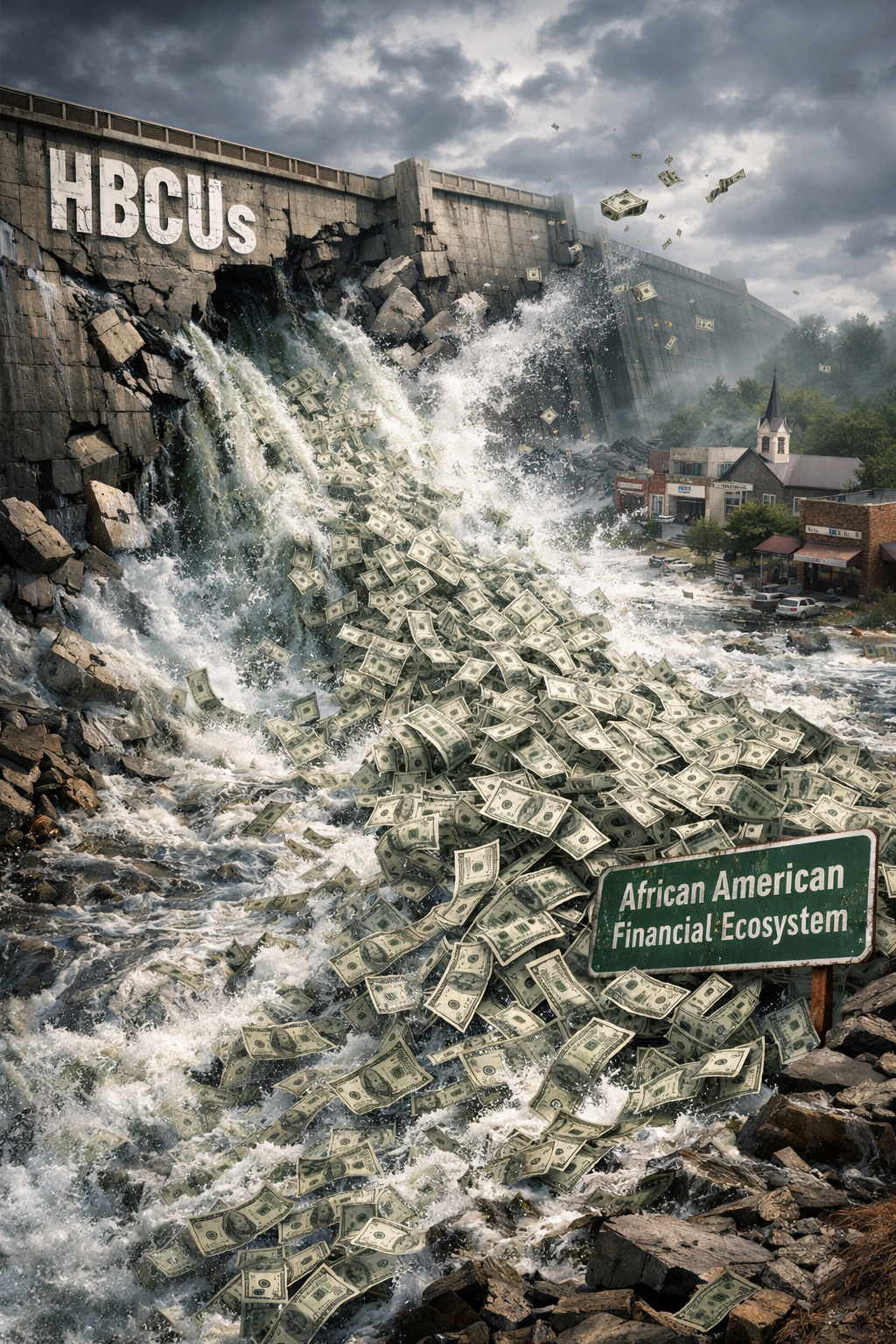

“It is disappointing that HBCUs and any African American institution for that matter have not figured out yet that the circulation of our social, economic, and political capital with each other at the institutional level is where the acute crisis of closing the wealth gap truly lies. Yet, we still chase colder ice.” – William A. Foster, IV

The percentage of PWI dollars that flow into African American owned businesses is likely limited to catering a social event. Beyond that, their dollar never even likely floats pass an African American business. However, HBCUs certainly cannot say the same. HBCU capital leaving the African American financial ecosystem looks like every dam on Earth broke at the same time.

Virginia Union University’s recent announcement of a partnership with Keller Williams Richmond West represents a familiar pattern in HBCU decision-making, one that undermines the very mission these institutions claim to champion. While VUU proudly touts this collaboration as “groundbreaking” and positions it as a pathway to “closing the racial wealth gap,” the partnership reveals a fundamental misunderstanding of how wealth gaps are actually closed. The reality is stark: you cannot close a racial wealth gap by systematically excluding institutions from your own community from the economic opportunities your institution creates.

When HBCUs partner exclusively with non-Black institutions, they create what economists call a “leaky bucket” effect. The money, talent, and social capital generated by these historically Black institutions flow outward to other communities rather than circulating within the African American ecosystem. Every dollar spent with a non-Black vendor, every partnership signed with a non-Black firm, every opportunity directed away from Black-owned businesses represents wealth that could have been building generational prosperity in Black communities—but instead enriches other groups. This is where the fundamental disconnect lies: HBCUs understand the importance of encouraging individual African Americans to support Black-owned businesses, yet these same institutions fail to apply this principle at the institutional level where the real economic power resides.

The conversation about the circulation of the African American dollar has historically focused on individual consumer behavior. We’ve heard for decades about the need for Black consumers to shop at Black-owned stores, bank with Black-owned financial institutions, and hire Black-owned service providers. Studies have shown that a dollar circulates in Asian communities for approximately thirty days, in Jewish communities for around twenty days, in white communities for seventeen days, but in Black communities for only six hours before leaving. This abysmal circulation rate is correctly identified as a critical factor in the persistent wealth gap. But what these discussions almost always miss is that individual consumer behavior, while important, pales in comparison to institutional spending power.

When Virginia Union University signs a multiyear partnership with Keller Williams, it’s not spending a few hundred or even a few thousand dollars. Institutional partnerships involve hundreds of thousands or millions of dollars in direct and indirect economic benefits—facility usage, marketing exposure, student referrals, commission opportunities, and brand association. A single institutional partnership can equal the spending power of hundreds or thousands of individual consumers. Yet HBCUs consistently fail to recognize that their institutional spending decisions have exponentially more impact on wealth circulation than any individual consumer choice their students or alumni might make.

VUU’s partnership with Keller Williams is particularly emblematic of this pattern. According to the announcement, this collaboration will create “the first Keller Williams Real Estate Hub on an HBCU campus in Virginia” and will be “designed to bridge education, entrepreneurship, and real estate into one powerful ecosystem.” The goals are admirable: career readiness, economic mobility, wealth-building opportunities through real estate education and professional pathways. The partnership is positioned as being co-led by members of Delta Sigma Theta Sorority, Incorporated, with explicit language about sisterhood, brotherhood, and service in action. But here’s the question VUU administrators apparently didn’t ask: Why not create this “powerful ecosystem” with a Black-owned real estate company?

The assumption underlying most HBCU partnerships with non-Black firms seems to be that suitable Black-owned alternatives don’t exist. This assumption is demonstrably false. Black-owned real estate companies operate throughout the United States, including in Virginia and the Richmond area. These firms possess the expertise, resources, and commitment to serve HBCU students and alumni. United Real Estate Richmond, which describes itself as the largest Black-owned real estate firm in the Mid-Atlantic region, operates right in VUU’s backyard. CTI Real Estate is a Black-owned, woman-owned firm serving Virginia and Maryland. Nationally, companies like Braden Real Estate Group—a Black-owned Houston-based brokerage co-founded by Prairie View A&M University graduate Nicole Braden Handy—demonstrate the success of HBCU alumni in building substantial real estate businesses. H.J. Russell & Company, founded in 1952, stands as one of the largest minority-owned real estate firms in the United States. These Black-owned firms have proven track records of success, deep community connections, and explicit missions to build wealth in African American communities. These firms could provide the same—or better—opportunities that Keller Williams offers, with the added benefit of keeping wealth circulating in the Black community.

The difference would be transformative. A partnership with a Black-owned real estate firm would actually contribute to closing the wealth gap. It would demonstrate to students what Black excellence in business looks like. It would create mentorship opportunities with professionals who understand the unique challenges and opportunities facing Black Americans in real estate. It would ensure that the commissions, fees, and other economic benefits generated by the partnership stay within the African American economic ecosystem. Most importantly, it would model the institutional behavior necessary for true wealth accumulation—showing students that circulation of Black dollars must happen at every level, not just in their personal spending habits.

But to truly understand what institutional circulation looks like, consider this scenario: An African American real estate investment firm—owned by an HBCU alumnus and employing HBCU graduates as project managers, analysts, and development specialists—decides to develop a mixed-use building in Richmond. The firm uses Braden Real Estate Group to acquire the land. They secure financing from an African American bank like OneUnited Bank or Liberty Bank, supplemented by an investment syndicate of African American investors. The construction is handled by an African American-owned construction company like H.J. Russell & Company. When the transaction closes, it’s processed through Answer Title & Escrow LLC, the Black-owned title company founded by University of the District of Columbia alumna Donna Shuler. The property management contract goes to another Black-owned firm. The legal work is handled by Black attorneys. The accounting is done by a Black-owned firm.

This is what institutional circulation actually looks like. In this single development project, wealth circulates through multiple Black-owned institutions at every stage of the transaction. The bank earns interest income that it can then lend to other Black businesses and homeowners. The title company generates revenue that allows it to hire more staff and take on larger projects. The construction company builds its portfolio and capacity to compete for even bigger developments. The real estate investment firm creates returns for its Black investors and proves the viability of Black-owned development companies. The project managers and analysts gain experience that prepares them to start their own firms. Every single point in the transaction keeps wealth circulating within the African American economic ecosystem, building institutional capacity, creating jobs, generating returns, and proving that Black-owned institutions can handle sophisticated, large-scale projects.

Now contrast that with what happens when VUU partners with Keller Williams. Students may get training and even jobs as real estate agents, but the institutional wealth flows to Keller Williams—a non-Black company. The commissions generated by VUU-affiliated agents enrich Keller Williams’ franchise system. The brand association benefits Keller Williams’ reputation. The networking opportunities primarily connect students to Keller Williams’ existing (predominantly non-Black) networks. And when these students eventually facilitate property transactions, the ancillary services—financing, title work, legal services—typically flow to whatever institutions Keller Williams recommends, which are unlikely to be Black-owned.

The VUU-Keller Williams partnership might help individual Black students enter the real estate industry, but it does absolutely nothing to build the Black-owned institutional infrastructure necessary for true wealth building. In fact, it actively undermines that infrastructure by directing institutional resources and opportunities away from Black-owned firms. VUU essentially takes Black talent, students who could be building careers with Black-owned firms, and channels them into a non-Black institution, teaching them that Black institutions aren’t capable of providing the same opportunities.

This is the critical insight that HBCUs continue to miss: institutional circulation of capital is what builds lasting economic power. When individual Black consumers support Black businesses, they create important but limited impact. One person shopping at a Black-owned grocery store or banking with a Black-owned bank makes a difference, but a small one. When Black institutions support Black businesses, they create transformative, generational impact. An HBCU that partners with Black-owned banks, construction companies, real estate firms, technology providers, and service companies doesn’t just create individual transactions it builds an entire ecosystem of mutually reinforcing institutions that grow stronger together. This institutional ecosystem then has the power to compete with non-Black institutions, create opportunities at scale, and genuinely close wealth gaps.

Think about what would happen if every HBCU made a commitment to work exclusively with Black-owned institutions whenever viable alternatives exist. Imagine if all 101 HBCUs banked with Black-owned banks, used Black-owned construction companies for campus buildings, partnered with Black-owned real estate firms for student housing and community development, contracted with Black-owned technology companies for IT services, and hired Black-owned firms for legal, accounting, and consulting work. The combined institutional spending power of HBCUs would transform the Black business landscape. Black-owned banks would have hundreds of millions in deposits, allowing them to make larger loans and compete for more business. Black-owned construction companies would have steady revenue streams that would allow them to invest in equipment, hire skilled workers, and bid on larger projects. Black-owned real estate firms would have the institutional backing to compete for major developments. Black-owned technology companies would have the resources to innovate and scale.

But beyond the immediate economic impact, this institutional circulation would create something even more valuable: proof of concept. When Alabama State University chooses a Black-owned bank to handle a $125 million transaction, it proves that Black-owned financial institutions can handle sophisticated, large-scale deals. When VUU partners with a Black-owned real estate firm to create a campus-based real estate hub, it proves that Black-owned companies can deliver the same quality and scale as non-Black competitors. When HBCUs consistently work with Black-owned construction companies, law firms, accounting firms, and consulting companies, they build a track record of success that these firms can point to when competing for other major contracts. This institutional validation is precisely what Black-owned businesses need to break through the barriers that have historically excluded them from large-scale opportunities.

VUU’s partnership is not an isolated incident, it’s part of a troubling pattern. As HBCU Money has documented, only two HBCUs are believed to bank with Black-owned banks, meaning well over 90 percent of HBCUs do not bank with African American-owned financial institutions. This mirrors the broader pattern where over 90 percent of African Americans who attend college choose non-HBCUs, and in both cases, neither Black-owned banks nor HBCUs are able to fulfill their potential without the patronage and investment of those they were built to serve. Alabama State University’s $125 million decision to partner with a non-Black financial institution exemplifies what can be called “Island Mentality”—the failure of HBCUs to connect with and support the African American private sector. When Alabama State University had the opportunity to work with Black-owned banks and financial institutions, they chose to look elsewhere. Consider the irony: Howard University, African America’s flagship HBCU, partnered with PNC Bank, a Pittsburgh-based institution with over $550 billion in assets, more than 100 times the combined assets of all remaining Black-owned banks to create a $3.4 million annual entrepreneurship center. Meanwhile, Industrial Bank, a Black-owned institution with $723 million in assets, operates right in Howard’s backyard. PNC Bank’s executive team commanded $81 million in compensation in 2022 alone, while only one Black-owned bank in America has assets exceeding $1 billion. These decisions, like VUU’s partnership with Keller Williams, send a devastating message: even historically Black institutions don’t believe Black-owned businesses are worthy of their partnership.

The impact extends beyond symbolism. Every time an HBCU chooses a non-Black partner when Black alternatives exist, it represents lost revenue for Black-owned businesses that could have grown stronger, hired HBCU graduates, and created more opportunities. It represents missed networking opportunities for students who could have built relationships with Black business leaders. It represents weakened community ties that could have been strengthened through institutional support. It represents reduced political capital for the Black business community, which needs institutional backing to compete for larger contracts. And it perpetuates stereotypes about the capability and reliability of Black-owned businesses.

Let’s be clear about what “closing the wealth gap” actually requires. According to the Federal Reserve’s Survey of Consumer Finances, the median wealth of white families is approximately ten times greater than that of Black families. This gap didn’t emerge overnight, and it won’t close through symbolic gestures or partnerships that funnel Black talent and capital into non-Black institutions. Closing the wealth gap requires wealth creation within the Black community through business ownership and entrepreneurship. It requires wealth circulation that keeps dollars moving through Black-owned businesses before leaving the community. It requires wealth accumulation through strategic investments in Black-owned assets. And it requires wealth transfer across generations through education, mentorship, and institutional support.

When VUU partners with Keller Williams instead of a Black-owned real estate company, it fails on every single one of these requirements. The wealth created by student success in real estate will flow to Keller Williams and its predominantly non-Black agents. The circulation of capital will happen outside the Black community. The accumulation will benefit non-Black wealth holders. And the transfer of knowledge and opportunity will lack the cultural competency and community commitment that comes from working with Black-owned institutions. Most critically, VUU misses the opportunity to demonstrate to its students how institutional circulation of capital works, teaching them instead that even Black institutions should look outside their community for partnerships when it matters most.

The example of what institutional circulation could look like in real estate development isn’t theoretical it’s entirely possible right now with existing Black-owned institutions. When Donna Shuler founded Answer Title & Escrow LLC as a University of the District of Columbia alumna, she created exactly the kind of institutional capacity that makes the full-circle Black real estate ecosystem viable. As she explained in her interview with HBCU Money, title companies play a crucial role in every real estate transaction—they ensure clear ownership, coordinate closings, prepare legal documents, collect funds, and issue title insurance. Having a Black-owned title company means that millions of dollars in fees and service charges stay within the Black community rather than flowing out. Combined with Black-owned banks providing financing, Black-owned real estate firms handling acquisitions, Black-owned construction companies building the projects, and Black-owned development firms managing the entire process, you create a complete ecosystem where institutional wealth circulates multiple times before leaving the community.

This is what VUU could have created with its real estate initiative but chose not to. Instead of building an ecosystem where Black institutions strengthen each other, VUU created a pipeline that extracts Black talent and channels it into a non-Black institution. Students will learn real estate from Keller Williams, make connections through Keller Williams networks, and likely facilitate transactions that benefit Keller Williams and its associated service providers. The institutional wealth created by VUU’s endorsement and student pipeline flows entirely out of the Black community.

HBCUs often justify these partnerships by arguing that non-Black firms offer broader networks, more resources, or greater reach. This argument is both self-fulfilling and self-defeating. It’s self-fulfilling because when HBCUs consistently choose non-Black partners, they ensure that Black-owned businesses never gain the institutional backing needed to compete at scale. How can Black-owned real estate companies build the same networks as Keller Williams when HBCUs, the institutions that should be their natural partners, consistently choose their competitors? It’s self-defeating because it undermines the very purpose of HBCUs. These institutions were created because the existing educational ecosystem excluded Black Americans. They thrived by building their own networks, creating their own opportunities, and supporting each other. The suggestion that HBCUs now need to partner with non-Black institutions to succeed represents a fundamental abandonment of the HBCU mission and the institutional circulation principle that should guide their operations.

Imagine if VUU had instead announced a partnership with a coalition of Black-owned real estate companies. The announcement might have read: “Virginia Union University is proud to announce a groundbreaking partnership with Black-owned real estate firms across Virginia marking the creation of the first Black Real Estate Hub on an HBCU campus. This collaboration goes beyond sponsorship to create career readiness, economic mobility, and wealth-building opportunities for VUU students, alumni, and the Richmond community through real estate education, entrepreneurship, and professional pathways led by successful Black business owners including HBCU alumni. Students will learn not just how to sell houses, but how to build generational wealth through development, investment, and institutional deal-making within the Black business ecosystem. They will receive training from firms like United Real Estate Richmond, Braden Real Estate Group, and other Black-owned companies, with pathways to internships and employment that keep talent and capital circulating within the African American community. The initiative will explicitly connect students with Black-owned banks for financing education, Black-owned title companies for transaction processing, and Black-owned development firms for career opportunities in the full spectrum of real estate activities.”

Such a partnership would demonstrate commitment to the Black business community, create mentorship pipelines between Black students and Black business leaders, build economic power by concentrating resources in Black-owned institutions, establish replicable models for other HBCUs to follow, and generate authentic wealth-building that actually closes gaps rather than widening them. It would teach students the most important lesson about wealth building: that institutional circulation of capital within your community is what creates lasting prosperity, not individual success stories that extract value from the community.

Beyond economics, these partnership decisions carry enormous social and political implications. When HBCUs choose non-Black partners, they signal to their students, alumni, and communities that Black-owned businesses are insufficient, unreliable, or less capable. This message has devastating ripple effects. Students at HBCUs should graduate believing they can build successful businesses that serve their communities and compete at the highest levels. They should see their institutions modeling the behavior they’re encouraged to adopt. Instead, they witness their own universities choosing non-Black partners, learning an implicit lesson about the supposed superiority of non-Black institutions. They learn that while individual Black consumers should support Black businesses, institutions don’t have to follow the same principle. This creates a fundamental contradiction that undermines the economic empowerment message entirely.

Consider the message VUU sends with its Keller Williams partnership: “We’ll teach you to be real estate professionals, but we don’t believe Black-owned real estate companies are good enough to partner with us.” What are students supposed to take from that? That they should aspire to work for Black-owned firms, or that they should aim for the “real” opportunities at non-Black companies? That Black businesses can compete at the highest levels, or that even Black institutions don’t really believe that? The implicit message is devastating, and it’s reinforced every time an HBCU makes a major partnership announcement with a non-Black firm when Black alternatives exist.

This dynamic also weakens the political capital of the Black business community. When even HBCUs won’t support Black-owned businesses, it becomes nearly impossible for these firms to argue they deserve a seat at the table for major contracts, government partnerships, or policy decisions. If historically Black institutions don’t believe Black businesses are capable of handling significant partnerships, why would predominantly white institutions, corporations, or government agencies think differently? HBCUs, by failing to partner with Black-owned institutions, actively undermine the credibility and viability of the very businesses that could drive wealth creation in African American communities.

The solution isn’t complicated, though it requires courage and commitment. HBCUs must conduct systematic audits of all major partnerships and vendor relationships to identify where Black-owned alternatives exist. They must establish procurement policies that prioritize Black-owned businesses when quality and capability are equivalent. They should create development programs to help emerging Black-owned businesses build the capacity to serve as HBCU partners. They need to build collaborative networks connecting HBCUs with Black-owned banks, real estate firms, construction companies, technology providers, and other businesses. They must measure and report on the percentage of institutional spending directed to Black-owned businesses, creating transparency and accountability. And they need to educate all stakeholders—boards, administrators, faculty, students, and alumni—about why these partnerships matter for wealth gap closure and why institutional circulation of capital is the key to building lasting economic power.

Some will argue this approach is discriminatory or inefficient. This objection ignores history and reality. HBCUs exist because discrimination created the need for separate Black institutions. Having addressed educational exclusion by building their own colleges, it’s logical and necessary to address economic exclusion by building supportive business ecosystems. The focus on institutional circulation isn’t about excluding others; it’s about finally including Black-owned institutions in the economic opportunities that Black institutions create. It’s about recognizing that the same principle we apply to individual consumer behavior of circulate dollars in your community applies with exponentially greater impact at the institutional level.

The choice facing HBCUs is stark: continue operating as isolated islands that happen to serve Black students, or become integral parts of a thriving African American institutional ecosystem that builds collective power and prosperity. Virginia Union University’s partnership with Keller Williams, like Alabama State University’s financial decisions before it, represents the island mentality. These institutions take Black talent, Black energy, and Black resources, then channel them into non-Black institutions that have no structural commitment to Black community wealth-building. They preach to students about supporting Black businesses while their own institutional dollars flow to non-Black partners.

The real estate development scenario described earlier where an HBCU alumnus-owned development firm works with Braden Real Estate Group, Answer Title, a Black-owned bank, and a Black-owned construction company isn’t a fantasy. All of these institutions exist right now. The only thing preventing this kind of institutional circulation from becoming the norm rather than the exception is the willingness of HBCUs to make it a priority. When HBCUs choose to partner with Black-owned institutions, they don’t just create individual transactions they validate and strengthen an entire ecosystem of Black-owned businesses that can then compete for even larger opportunities.

True wealth gap closure requires HBCUs to fundamentally reimagine their role. They must see themselves not as individual institutions competing for resources and prestige, but as anchor institutions responsible for building and sustaining a broader African American economic ecosystem. This means prioritizing partnerships with Black-owned banks, real estate companies, construction firms, technology providers, and other businesses even when doing so requires more effort, more creativity, or more patience. It means recognizing that institutional circulation of capital is what transforms individual Black success stories into generational Black wealth accumulation. It means understanding that HBCUs have the power to create the very ecosystem they claim doesn’t exist by directing their substantial institutional resources to Black-owned businesses.

The question isn’t whether Black-owned alternatives exist. They do. The question is whether HBCU leaders have the vision, courage, and commitment to build an economic ecosystem that actually closes the wealth gap rather than simply talking about it. Until HBCUs make this fundamental shift, until they recognize that institutional circulation of capital is the key to wealth building and start directing their partnerships, contracts, and spending to Black-owned institutions these announcements about “groundbreaking partnerships” that close the wealth gap will remain what they are today: well-intentioned rhetoric that masks the continued extraction of Black wealth and talent for the benefit of other communities.

Individual African Americans can only do so much with their consumer dollars. The six-hour circulation rate in Black communities is a problem, but it’s a problem that individual behavior alone cannot solve. The real power lies at the institutional level. When an HBCU spends $10 million on a construction project with a Black-owned firm, that’s not the equivalent of 10,000 individual consumers each spending $1,000—it’s exponentially more powerful because institutional spending validates capacity, builds track records, creates jobs at scale, and proves viability in ways that individual transactions never can. But HBCUs, with their millions in institutional spending power, their influence over thousands of students and alumni, and their role as anchor institutions in Black communities, have the power to transform the economic landscape. They just need to recognize that the principle of dollar circulation they teach their students applies with even greater force to their own institutional behavior.

Until HBCUs start practicing institutional circulation of capital, until they recognize that every major partnership, every significant contract, and every spending decision is an opportunity to strengthen Black-owned institutions and build the ecosystem necessary for true wealth creation they will continue to be part of the problem rather than the solution to the wealth gap they claim to want to close. The infrastructure exists. The capable Black-owned businesses exist. The only thing missing is the institutional will to make Black economic ecosystem-building a priority over convenience, familiarity, or the perceived prestige of partnering with established non-Black firms. The choice is clear: HBCUs can continue channeling Black talent and capital out of the community, or they can finally commit to the institutional circulation that makes wealth gap closure actually possible.

Disclaimer: This article was assisted by ClaudeAI.

“Revolution is based on land. Land is the basis of all independence. Land is the basis of freedom, justice, and equality.” – Malcolm X

Few institutions have carried the weight of controversy in American housing like the homeowners’ association (HOA). For much of the 20th century, HOAs were weaponized as a tool of institutional racism restricting African Americans from buying into White neighborhoods through deed covenants, enforcing exclusionary zoning, and serving as gatekeepers of generational wealth accumulation. The very mechanism of neighborhood governance became one more way African America was told “you do not belong.” Yet history has a way of flipping its instruments. The very structural force once used to keep us out may be one of the few institutional levers available to keep us in. As gentrification and predatory development rapidly encroach upon historically African American communities from Houston’s Third Ward to Atlanta’s West End, from Washington D.C.’s Shaw to New Orleans’ Tremé, the need for institutional tools of land sovereignty grows urgent. Civic associations, while noble, often lack teeth. It may be time for African American neighborhoods to rethink the HOA, not as a relic of exclusion but as a shield of survival.

Most African American neighborhoods today rely on civic clubs or neighborhood associations. These bodies are typically voluntary, underfunded, and lack the legal authority to enforce community decisions. They can advocate to city councils, organize block cleanups, and serve as a cultural glue, but when it comes to confronting a developer with millions in capital and legal teams, they are simply outgunned. Civic associations cannot foreclose properties when owners ignore rules or dues, build substantial war chests because dues are voluntary and non-enforceable, or control property transfers when long-time residents sell. This means that even when a neighborhood is organized and has strong social cohesion, it remains structurally weak in the face of predatory real estate activity. Developers exploit this weakness buying distressed properties, lobbying city officials for zoning changes, and rapidly altering the fabric of communities without consent.

Unlike civic clubs, HOAs are legally binding entities. When properly designed and governed, they give communities leverage that is otherwise impossible. The ability to foreclose ensures compliance and funding. If dues are unpaid, the HOA has a mechanism to protect the community’s collective interests. Mandatory dues create a stable revenue stream. A community with 200 homes each contributing $500 annually generates $100,000. Over five years, that becomes half a million which is enough to hire lawyers, challenge city zoning, and even purchase properties outright. This institutional capital transforms neighborhoods from reactive to proactive. HOAs can also insert right-of-first-refusal clauses, allowing them to buy homes before they go to outside investors, preventing predatory acquisitions and allowing neighborhoods to decide who their neighbors will be and what developments fit the collective vision. Rules around property maintenance, density, and usage can prevent developers from converting single-family homes into high-turnover rentals or Airbnbs. These standards are not just about aesthetics they are about protecting neighborhood identity and safety.

To advocate HOAs for African American communities is not to ignore their history. For decades, HOAs were bastions of exclusion. They operated in tandem with banks, appraisers, and city planners to enforce segregation. Deed restrictions openly barred African Americans and other minorities from ownership. Even when those covenants became unenforceable after Shelley v. Kraemer (1948), HOAs found new ways to enforce segregation through indirect mechanisms. But history also shows how institutions can be repurposed. Universities once denied African Americans; now HBCUs are among our strongest institutions. Banks once denied us credit; now Black-owned banks serve as pillars of community capital. The HOA, when reimagined under African American sovereignty, can become not a wall keeping us out, but a fortress keeping us in.

Houston’s Third Ward is emblematic. A historically Black neighborhood anchored by Texas Southern University, it has been ground zero for gentrification. Developers like TPC Endeavors LLC have defied city red tags, continued illegal construction, and ignored deed restrictions designed to protect single-family character. Residents organized, called 311, attended City Council meetings but the civic tools they had were insufficient. Enforcement by the city was lax. Meanwhile, developers were renting red-tagged properties as Airbnbs. Imagine if Third Ward had a robust HOA structure. With mandatory dues, it could hire legal counsel to file injunctions. With right-of-first-refusal, it could have purchased properties neighbors wished to sell, keeping them out of speculative hands. With codified rules, it could have legally enforced single-family restrictions, protecting housing stock for families rather than transient rentals. Instead, the community is stuck fighting asymmetrical battles, people with civic will against people with institutional power. The outcome, absent intervention, is predictable: displacement.

At its core, the case for African American HOAs is about institutional economics, the accumulation of collective capital to withstand systemic pressures. The median net worth of White households is nearly eight times that of Black households. Real estate is the largest component of wealth for African American families. When neighborhoods gentrify, this wealth is not preserved; it is extracted. HOAs serve as protectors of that capital by stabilizing community land values under African American governance. They enable neighborhoods to pool financial and legal resources to resist external exploitation. They foster long-term family residence, giving children environments with consistent community standards, building social and cultural capital alongside financial wealth. HOAs also enable neighborhoods to act like firms: they can engage developers on their own terms, negotiate concessions, or even partner in development deals that align with community interests.

Of course, HOAs are not a panacea. Poorly run HOAs can become abusive or corrupt, mirroring the very forces they are meant to resist. Mandatory payments can strain low-income residents, though creative structures such as sliding scales, subsidies, or partnerships with HBCUs and community foundations can mitigate this. Forming an HOA requires legal expertise and state recognition, which many African American communities lack immediate access to, though partnerships with HBCU law schools could be a solution. Neighborhoods may resist HOAs due to historical mistrust or fear of bureaucracy. Education campaigns and transparent governance are crucial.

The HBCU ecosystem has a unique role to play. Many HBCUs are surrounded by historically Black neighborhoods now under siege from gentrification. These institutions could provide the technical, legal, and financial scaffolding for community HOAs. Law schools could draft HOA charters and litigate against predatory developers. Business schools could train HOA boards in financial management. Architecture and urban planning programs could design neighborhood development standards. University endowments could provide seed capital to help HOAs acquire distressed properties. If HBCUs become the backbone of HOA development, they transform from being passive neighbors to active protectors of Black land sovereignty.

Imagine a network of African American HOAs across the country, each tied to local HBCUs, each building collective war chests, each controlling neighborhood development. Together, they form a patchwork of institutional sovereignty one block at a time, one neighborhood at a time. This is not just about resisting gentrification. It is about reclaiming agency over land, the foundational asset of all wealth and power. Without land sovereignty, African American communities will forever be tenants in someone else’s design. With HOAs, we have the chance to rewrite that story.

While HOAs have been historically tainted by their role in exclusion, African America must confront a hard truth: institutional problems require institutional solutions. Civic will, without institutional teeth, cannot withstand predatory capital. HOAs, properly structured and governed, give our neighborhoods enforcement power, financial capacity, and development control. Land sovereignty is not optional; it is existential. Gentrification is not just about higher rents or new coffee shops, it is about the slow erasure of African American communities from the map. If we are to remain, to build intergenerational wealth, and to strengthen our institutional power, then we must be willing to use every tool available. The HOA may have once been a weapon against us. It can now be the fortress that protects us.

Model HOA Framework for African American Communities

1. Charter Outline

A. Name and Purpose

Name: [Neighborhood Name] Community Land Trust HOA

Mission: To preserve and protect African American homeownership, stabilize property values, and foster community-driven development.

Objectives:

Protect neighborhood land from predatory acquisition and gentrification.

Maintain architectural and cultural integrity of the neighborhood.

Build collective financial resources for legal, development, and maintenance initiatives.

Empower residents with decision-making authority over neighborhood development.

B. Membership

All property owners within the HOA boundary are automatically members.

Membership is determined by the community.

Voting rights are proportional to ownership, with one vote per property.

C. Governance Structure

Board of Directors: 5–9 elected members serving staggered three-year terms.

Committees:

Finance & Investment Committee

Architectural & Community Standards Committee

Legal & Advocacy Committee

Outreach & Education Committee

Decision-making: Major decisions (property acquisition, legal action, development approvals) require a 2/3 majority vote of the board and approval by 50%+1 of voting members.

D. Covenants and Bylaws

Rules governing property use, maintenance, and modifications.

Right-of-first-refusal on property sales to maintain African American ownership and prevent predatory acquisitions.

Restrictions on commercial rental operations (e.g., short-term rentals like Airbnb) unless approved by the board.

Enforcement of community standards through fines, liens, and, if necessary, foreclosure.

2. Funding Structure

A. Mandatory Dues

Base dues calculated per household (example: $500–$1,000/year depending on neighborhood size and needs).

Sliding scale or hardship exemptions for low-income homeowners, with supplemental funding from foundations or HBCUs.

B. Special Assessments

Imposed for extraordinary needs such as legal battles, property acquisition, or infrastructure repairs.

Must be approved by majority vote of HOA members.

C. Reserve Fund / War Chest

25–30% of annual dues set aside into a reserve fund for long-term projects or emergency legal needs.

Goal: Maintain liquidity to purchase at-risk properties and fund legal actions without delay.

D. Partnerships & Grants

Collaborate with HBCUs, local Black-owned banks, and philanthropic foundations for technical and financial support.

Seek grants specifically for community land trusts, anti-gentrification initiatives, or neighborhood revitalization.

E. The HOA Investment Fund

Neighborhood Endowment: A portion of dues is invested to build a long-term community fund. This endowment can invest in local African American businesses, the stock market, or other vetted opportunities. Returns are used to subsidize senior citizens and low-income residents, provide relief during emergencies, and strengthen the HOA’s financial independence.

Emergency Fund: A dedicated reserve for disasters, legal challenges, or community emergencies.

Special Assessments: Levied for large projects (legal defense, infrastructure, property acquisition).

3. Enforcement Mechanisms

A. Fines and Liens

Fines for non-compliance with HOA rules (maintenance, property use, etc.).

Unpaid fines converted into liens that attach to the property.

B. Legal Authority

Covenants provide authority to take legal action against violators, including:

Enforcing property use restrictions

Preventing unauthorized sales or rentals

Challenging predatory development through court injunctions

C. Foreclosure

In extreme cases of non-payment or serious violations, the HOA has the right to foreclose on the property to protect collective community interests.

Requires board approval and due process, with transparency to all members.

D. Right-of-First-Refusal

The HOA can purchase homes before they are sold to external buyers.

Maintains neighborhood ownership continuity and allows control over development aligned with community goals.

4. Community Engagement and Education

Regular town halls and workshops on:

Financial literacy and collective wealth building

Understanding HOA powers and responsibilities

Recognizing predatory developers and speculative practices

Partnerships with local HBCUs to provide pro bono legal clinics, urban planning advice, and leadership development for HOA board members.

Volunteer committees for property upkeep, neighborhood beautification, and cultural preservation.

5. Oversight and Accountability

Annual audits of finances by independent accountants.

Mandatory annual reporting to members detailing:

Income and expenses

Property acquisitions

Enforcement actions taken

Development approvals or denials

Board elections conducted transparently with all members notified in advance.

6. Strategic Objectives for Anti-Gentrification

Property Acquisition Strategy

Identify at-risk properties before they are sold to outside investors.

Use reserve funds or special assessments to purchase and hold properties for resale to qualified African American buyers.

Legal Defense Fund

Maintain a portion of the war chest specifically for litigation against predatory developers and enforcement of zoning codes.

Cultural and Architectural Preservation

Set clear standards for renovations and new construction that reflect neighborhood heritage.

Ensure that new development aligns with the neighborhood’s long-term vision and identity.

Economic Empowerment

Encourage local entrepreneurship and small business ownership within the HOA’s commercial spaces.

Partner with HBCUs and Black-owned banks to provide financing, mentorship, and business support.

“I had crossed the line. I was free; but there was no one to welcome me to the land of freedom. I was a stranger in a strange land.” – Harriet Tubman

Race riots or rural reckoning? The answer lies beneath the surface—and often beneath the soil itself.

In the blistering summer of 1919, the United States erupted in racial violence unlike anything the country had witnessed since Reconstruction. From Washington, D.C. to Chicago, from Norfolk to Omaha, from Knoxville to the cotton fields of Arkansas, more than three dozen cities and rural towns became sites of bloodshed as white mobs attacked African American communities with a ferocity that was, in many instances, organized, deliberate, and unrelenting. Historians dubbed it the Red Summer, invoking both the color of blood and the communist anxieties of the era. For more than a century, the dominant explanation has centered on racial tensions stoked by the Great Migration, post-war competition for jobs, and white anxiety over African American assertiveness. But a deeper, more unsettling question lingers beneath those textbook explanations: was Red Summer not merely about urban unrest or racial animosity, but about land?

That question has returned with renewed urgency in recent years, amid a widening reexamination of Black land ownership and its deliberate erosion over the past century. As calls for reparations grow louder and more specific, so too does the need to reassess the forces that helped decimate Black wealth and autonomy in America. And when Red Summer is placed in that context, it begins to look less like a spontaneous explosion of racial rage and more like the bloodiest chapter in a longer, quieter war — a war fought not only over race but over soil.

The idea that African Americans were only victims of economic exclusion in early 20th-century America is a distortion that history has been slow to correct. By 1910, African Americans owned more than 15 million acres of land, largely concentrated in the South. Black farmers — most of them formerly enslaved or their direct descendants — had managed to accumulate land against crushing odds, frequently purchasing it collectively, through church cooperatives, fraternal organizations, or from white landowners seeking to offload marginal plots. These holdings were not merely symbolic achievements. They were strategic infrastructure.

Land ownership among Black Americans was more than a pathway to individual wealth; it was a bulwark against white supremacy. Land meant food security, political leverage, and a degree of independence in a nation otherwise constructed around Black dependency and racial domination. In some areas of the South, land ownership translated into Black-majority townships and counties, Black-controlled local economies, and the fragile but real possibility of a parallel civic sovereignty. Black landowners could vote with greater difficulty for whites to suppress. They could withhold labor. They could resist eviction. They could educate their children. They were, in a word, ungovernable in ways that landless sharecroppers were not.

African Americans were not simply asking for equality; in some places, they were building it. And that may have been the greatest threat of all.

Virginia-born coachman Thomas A. Dillon and his wife, Margaret, a domestic servant and native of Newton, Massachusetts, pose in the parlor of their home at 4 Dewey Street with children Thomas, Margaret, and Mary in 1904.

Nowhere is the link between land and lethal violence more clearly illustrated than in the massacre at Elaine, Arkansas — one of the deadliest and least discussed events of the entire Red Summer. On the night of September 30, 1919, African American sharecroppers gathered in a church in Phillips County to organize a union, the Progressive Farmers and Household Union of America. Their goals were modest by any democratic standard: they wanted transparent accounting from the plantation owners who controlled the cotton market, an end to the rigged ledger systems that kept sharecroppers in perpetual debt, and the ability to sell their crops independently on the open market. It was a meeting about fair contracts, not rebellion. What descended upon them was a massacre.

White mobs, augmented by federal troops dispatched from Little Rock, swept through the area for days. An estimated 100 to 200 Black men, women, and children were killed, though the official tallies — sanitized for public consumption — counted only a handful of white deaths and labeled the episode a Black insurrection. The real insurrection was economic. The plantation economy of the Delta had been built on the enforced ignorance and powerlessness of its Black labor force. If Black sharecroppers could collectively organize, access fair markets, and demand accurate accounting, some of them might eventually become landowners themselves. That possibility — not armed revolt — was what the white establishment could not tolerate.

The Elaine massacre exposed a hidden economic architecture underlying Southern racial terror. Violence was not just an expression of hatred; it was a tool of market control. When the ledger failed to keep Black workers in debt, the mob stepped in. When the law was too slow, the rifle arrived first.

Though most of the events of Red Summer are framed through an urban lens — riots in Chicago, Washington, and Knoxville dominating the historical imagination — the violence cannot be disentangled from broader efforts to contain and reverse Black economic advancement. Indeed, many of the African Americans who had migrated to Northern cities were themselves displaced farmers or sharecroppers whose rural land ownership efforts had been stymied, swindled, or literally burned to the ground. The Great Migration was not only a story of aspiration; it was also a story of flight.

In Chicago, where violence erupted in late July after a Black teenager named Eugene Williams drowned after being struck by stones thrown by white men when he accidentally drifted past an informal racial boundary in Lake Michigan, the precipitating incident masked deeper structural conflicts. African Americans had begun purchasing homes and moving into previously all-white neighborhoods. Black entrepreneurs were opening businesses. The color line in Chicago was not just social — it was economic, and it was being crossed. What followed Williams’s death was a week of brutal violence that left 38 people dead and more than 500 injured. The riot was sparked by a beach dispute, but what it expressed was white terror at the prospect of Black economic mobility in the urban North.

Property rights were at the center of the Chicago conflict in ways that have only grown clearer with time. Redlining would not be formalized by the federal government until the 1930s, but the ideology animating it — that Black habitation diminished property values, that Black ownership was a form of invasion — was already operating through mob violence in 1919. White homeowners’ associations, some of which had explicitly bombed Black homes in the years leading up to the riot, continued their campaigns of intimidation with renewed license after the summer’s bloodshed. The message was consistent whether it came from the Delta or the Midwest: African Americans had no rightful claim to the land, whether in field or neighborhood.

What made Red Summer different from previous episodes of racial terror, and what made it so culturally resonant, was that it came at a moment when African American self-determination was not just a dream but a demonstrable reality. The years surrounding World War I had seen an extraordinary flowering of Black institutional life: newspapers like the Chicago Defender and the NAACP’s Crisis magazine reached hundreds of thousands of readers; the Universal Negro Improvement Association under Marcus Garvey was drawing mass followings with its message of African sovereignty; and Black veterans returning from the battlefields of France, having fought for democracy abroad, were unwilling to accept its absence at home. Many of these veterans would become central figures in the armed resistance that communities mounted against white mobs in 1919. They met violence with violence, and the White establishment found the combination of Black assertiveness, Black organization, and Black land deeply alarming.

The economic threat extended well beyond individual plots of farmland. In Tulsa, Oklahoma — whose 1921 Greenwood massacre falls just outside the official boundaries of Red Summer but belongs to the same continuum of violence — an entire district of Black economic life was leveled. Greenwood, known as Black Wall Street, was home to hundreds of Black-owned businesses, banks, law offices, and hotels. It was the product of deliberate community investment and collective self-determination. When white mobs descended in May 1921, aided by the Tulsa Police Department and private aircraft that reportedly dropped incendiary materials on the district, they did not merely kill people. They destroyed an economic ecosystem that had taken a generation to build. The land was seized. The insurance claims were denied. The neighborhood was never fully restored.

The pattern repeated itself, with local variations, across decades. What Red Summer initiated, the legal and bureaucratic infrastructure of mid-20th century America codified. Heirs’ property laws — in which land passed down without a formal will became jointly owned by all descendants — rendered Black landholdings acutely vulnerable to partition sales. A developer or speculator who purchased a single heir’s fractional share could force the sale of the entire property, often at below-market prices, with no recourse for the remaining family members. These laws, ostensibly race-neutral, operated with devastating specificity against Black families whose distrust of white legal institutions, forged over generations of documented fraud and violence, led them to avoid formal probate processes.

The federal government was often a direct participant in dispossession. The United States Department of Agriculture systematically denied Black farmers access to loans and subsidies that were extended routinely to their white counterparts. From the New Deal agricultural programs of the 1930s through the farm credit crisis of the 1980s, Black farmers were excluded, underfunded, and allowed to fail at rates far exceeding their white peers. In 1999, the Pigford v. Glickman class action settlement acknowledged decades of discriminatory lending by the USDA and resulted in payouts to tens of thousands of Black farmers — but by then, most of the land was already gone.

Numbers are beyond staggering in their finality. African Americans owned approximately 15 to 19 million acres of land at the peak of Black land ownership around 1910. By 1997, that figure had collapsed to fewer than 2 million acres — a loss of nearly 90 percent over the course of a single century. The USDA itself acknowledged that this loss was not driven solely by economic forces. Discrimination, fraud, violence, and legal manipulation played decisive roles in transferring land from Black families to white institutions and individuals.

The state of Black land ownership in America today reflects the accumulated weight of that century of dispossession. African Americans currently own less than 1 percent of rural land in the United States, despite constituting approximately 14 percent of the national population. In the South, where Black land ownership once represented a genuine counter-economy, the erasure is especially pronounced. In Mississippi, Alabama, and Georgia — states where Black farmers built substantial holdings after Emancipation — Black land ownership has been reduced to a thin remnant. Entire family lineages have been severed from the soil their ancestors purchased with freedom wages, war bonuses, and borrowed hope.

Consequences extend far beyond sentiment. Land is the primary vehicle through which intergenerational wealth is transferred in the United States. Home equity and real property account for the majority of household net worth for most American families. The racial wealth gap — the persistent, yawning disparity between Black and white household wealth, which current estimates place at a ratio of roughly 1 to 8 — cannot be understood without accounting for the systematic denial of land and property rights to African Americans. Every generation of a Black family that was driven from its land, or swindled out of it, or watched it seized through partition sale or eminent domain, is a generation that could not pass on the compounding advantages of ownership. The wealth gap is not an accident of markets. It is the arithmetic of dispossession.

Contemporary efforts to address this reality operate at the margins of what is needed. Organizations like the Federation of Southern Cooperatives, founded in 1967, have worked for decades to help Black farmers retain land through legal assistance and cooperative economics. The Land Loss Prevention Project in North Carolina has challenged fraudulent partition sales and helped heirs navigate probate processes designed for a legal culture that was never built with them in mind. The Black Farmers Fund and similar initiatives provide capital and technical assistance to a dwindling population of Black agriculturalists. In 2021, Congress included provisions in the American Rescue Plan Act to provide debt relief to socially disadvantaged farmers — provisions that were subsequently challenged in federal court by white farmers who argued that race-conscious relief violated the Equal Protection Clause, a stunning inversion of the history that made such relief necessary.ve increasingly focused on this disparity. But to properly assess the scale of restitution, history must be rewritten to acknowledge not just the loss of life, but the loss of land. If Red Summer is reframed as a land war not only a race war, then it demands a different response.

Programs such as the Black Farmers Fund, the Federation of Southern Cooperatives, and the work of legal nonprofits like the Land Loss Prevention Project have begun to claw back some ground. Yet without a federal reckoning one that links racial violence to economic theft the narrative remains incomplete.

Reparations proposals have increasingly focused on land as the foundational unit of redress. Scholars like Thomas Mitchell, who pioneered the Uniform Partition of Heirs Property Act — now adopted in more than a dozen states — have worked to close the legal loopholes that enabled generations of Black land theft. Others have proposed direct federal land grants or land trusts as a more durable form of repair than cash payments alone. The argument is both pragmatic and historical: if land was what was taken, land is what must be restored.

But to make that argument with the force it deserves requires an honest reckoning with Red Summer as something more than a riot. It requires understanding 1919 not as an aberration but as an acceleration — the moment when informal systems of racial violence were enlisted on a national scale to reverse Black economic progress. The targets were not random. They were selected. Churches where sharecroppers organized were burned. Prosperous Black neighborhoods were razed. Landowners were murdered and their deeds contested in their absence. The land did not transfer by accident. It was taken by design, and the taking was protected, in county courthouses and federal offices alike, for decades afterward.

Malcolm X once observed that land is the basis of all independence. He was not speaking metaphorically. He was speaking from a tradition of Black political thought that understood, from Reconstruction onward, that the promises of American citizenship were hollow without the material foundation that land provides. The freedpeople who demanded forty acres understood this. The sharecroppers of Elaine who organized for fair prices understood it. The Greenwood entrepreneurs who built Black Wall Street understood it. And the white mobs, the plantation owners, the local sheriffs, the federal troops, and the discriminatory bureaucracies that systematically dismantled what Black Americans built — they understood it too.

Red Summer was not simply a spasm of postwar bigotry, nor an understandable if deplorable expression of racial anxiety. It was a calculated and coordinated assertion of dominance over a people who were, against every structural obstacle, building something that looked like sovereignty. The violence of 1919 did not emerge from nowhere, and it did not end with the cooling of summer temperatures. It opened a door that the legal and economic machinery of the 20th century walked through for decades, quietly completing the dispossession that the mobs had begun.

In the end, Red Summer may be remembered not only for its flames but for the fertile ground those flames sought permanently to char. It was not only a summer of blood. It was a war over soil — and the aftershocks of that war continue to shape the contours of American inequality today, in the wealth gaps, the landlessness, the severed inheritances, and the unanswered demands for repair that echo across every serious conversation about racial justice in this country.

📅 Visual Timeline: The Red Summer of 1919

April 13, 1919 – Jenkins County, Georgia

A violent confrontation erupts in Millen, Georgia, resulting in the deaths of six individuals and the destruction of African American churches and lodges.

May 10, 1919 – Charleston, South Carolina

White sailors initiate a riot, leading to the deaths of three African Americans and injuries to numerous others. Martial law is declared in response.

July 19–24, 1919 – Washington, D.C.

Racial violence breaks out as white mobs attack Black neighborhoods. African American residents organize self-defense efforts.

July 27–August 3, 1919 – Chicago, Illinois

The Chicago Race Riot begins after a Black teenager is killed for swimming in a “whites-only” area. The violence results in 38 deaths and over 500 injuries.

September 30–October 1, 1919 – Elaine, Arkansas

African American sharecroppers meeting to discuss fair compensation are attacked, leading to a massacre where estimates of Black fatalities range from 100 to 800.

October 4, 1919 – Gary, Indiana

Racial tensions escalate amid a steel strike, resulting in clashes between Black and white workers.

November 2, 1919 – Macon, Georgia

A Black man is lynched, highlighting the ongoing racial terror during this period.

Disclaimer: This article was assisted by ClaudeAI.

“We don’t need to break ground to build power. Sometimes we just need to reclaim it.” – HBCU Money

In the 1990s and early 2000s, no suburban corner in America seemed complete without a modest retail strip: a nail salon, dry cleaner, small grocer, and maybe a local pizza joint. These seemingly unremarkable centers were the backbone of everyday commerce. Then came e-commerce, big box expansions, and shifting consumer behavior. The strip center fell out of fashion until now.

Today, those vintage retail strip centers are experiencing a renaissance. Commercial real estate investors, faced with skyrocketing construction costs and restrictive lending environments, are rediscovering the power and profitability of renovating existing assets. For HBCU alumni investors looking to blend stable returns with community impact, this moment presents a rare convergence of opportunity, efficiency, and cultural relevancy.

The Math Behind the Momentum

Construction costs for new retail buildings are ballooning. Estimates now range from $250 to $300 per square foot for ground-up construction sometimes higher in urban markets. At those prices, generating attractive returns is difficult unless you’re building luxury, destination retail with national anchor tenants. That’s not where the market is heading.

Instead, investors are realizing they can acquire and renovate vintage strip centers typically 20 to 40 years old for far less than the cost of new construction. Many are structurally sound but aesthetically dated or functionally obsolete. These properties often sit on prime real estate near transportation corridors, residential growth areas, or college campuses including HBCUs.

When repositioned with the right tenants, lighting, signage, and facades, vintage centers can achieve competitive rents without incurring the deep capital exposure of new construction. They offer a rent-to-cost ratio that works, especially in secondary and tertiary markets where demand for accessible neighborhood retail remains strong.

A Platform for Black Wealth Creation

For HBCU alumni who have traditionally been boxed out of Class A urban development deals, vintage strip centers represent an asset class that is:

Financially accessible

Culturally significant

Commercially viable

Most importantly, these assets can serve as anchors for Black-owned businesses, co-ops, and cultural hubs. While institutional investors often chase high-profile multifamily or office deals, retail strip centers in historically Black communities or near HBCUs are often overlooked providing a wedge for local or regional investors to step in.

A well-structured renovation project led by an HBCU graduate could transform a decaying strip into a vibrant ecosystem of barbershops, cafés, health providers, financial institutions, and coworking spaces all backed by the community, for the community.

Deferred Maintenance as Opportunity, Not Obstacle

Critics of strip centers often cite “deferred maintenance” as a red flag. And it’s true—many of these assets come with leaky roofs, outdated HVAC systems, and non-compliant ADA access. But that doesn’t make them unviable. It makes them undervalued.

Roof replacements, ADA compliance upgrades, lighting retrofits, parking lot resurfacing—these are all predictable costs that can be priced and phased. Investors willing to do their homework (or partner with experienced contractors) can use these improvements to negotiate purchase price reductions while still bringing total project costs well below new-build levels.