Reclaiming the right to dream the future, strengthening the muscle to imagine together as Black people, is a revolutionary decolonizing activity.” — adrienne maree brown

A running sitcom joke obscures one of the most instructive models in African American economic imagination. Revisiting Tommy Strawn as a deliberate investor not a layabout reveals what cooperative wealth-building looks like when it is practiced quietly, structurally, and across generations. For three decades, Martin Payne’s crew delivered the same punchline. Tommy Strawn — affable, well-dressed, perpetually present at Nipsey’s in the middle of a weekday would absorb the ritual taunt: ‘You ain’t got no job.’ The laugh track followed. So did the audience. The joke endured not because it was especially clever, but because it tapped something deeper than comedy: a cultural reflex that made unemployment a more plausible explanation for Tommy’s idleness than financial independence. That reflex, and what it costs, is worth examining seriously.

The question this article puts forward is not merely playful. What if Tommy Strawn was never unemployed? What if, by the time the show’s first season aired in 1992, Tommy had already spent a decade as treasurer of a Black investment club quietly compounding returns, attending shareholder meetings, and managing a diversified portfolio that rendered the forty-hour work week optional? The speculation is fictional in origin. Its implications are not.

Begin with the sociology of the joke itself. In the 1990s African American community, and in many circles today, the premise that a Black man could simply choose not to hold a traditional job because he had built sufficient passive income was, and remains, genuinely difficult to accept. It was not that the mechanics of investing were unknown. It was that the social imagination around Black wealth had not yet made room for this particular portrait. The more intuitive read — the one requiring no further explanation — was that Tommy must be hustling. He must be in the streets. A drug dealer felt more believable than an investor. The illegitimate path to economic autonomy was easier to accommodate than the legitimate one. Tommy, in this reading, never corrected anyone. Perhaps he understood that defending compound interest to a booth at Nipsey’s was not worth the breath. That silence, the invisibility of deliberate Black wealth-building is itself a form of cultural tax, one levied not by any external institution but by the limits of a community’s own economic imagination.

HBCU Money has argued consistently that economic literacy in Black America cannot be reduced to numeracy. It requires cultural reprogramming as a revision of the stories communities tell themselves about what wealth looks like, who holds it, and how it is built. Reimagining Tommy Strawn serves exactly that purpose. In its 2023 analysis, this publication asked what would have happened had Martin and Gina invested their $4,000 tax refund in Microsoft stock in 1995 rather than plowing it into a failed restaurant venture. The answer: a return exceeding 7,500 percent, translating to more than $300,000 by 2023. Had the couple sustained annual contributions of $4,000 into a diversified S&P 500 portfolio over the same period, their accumulated position would have exceeded $500,000 more than enough for their children’s tuition, a second property, or early retirement. These are not exotic outcomes. They are the arithmetic of patience applied to ordinary capital. Tommy, in our reimagining, knew this arithmetic by heart.

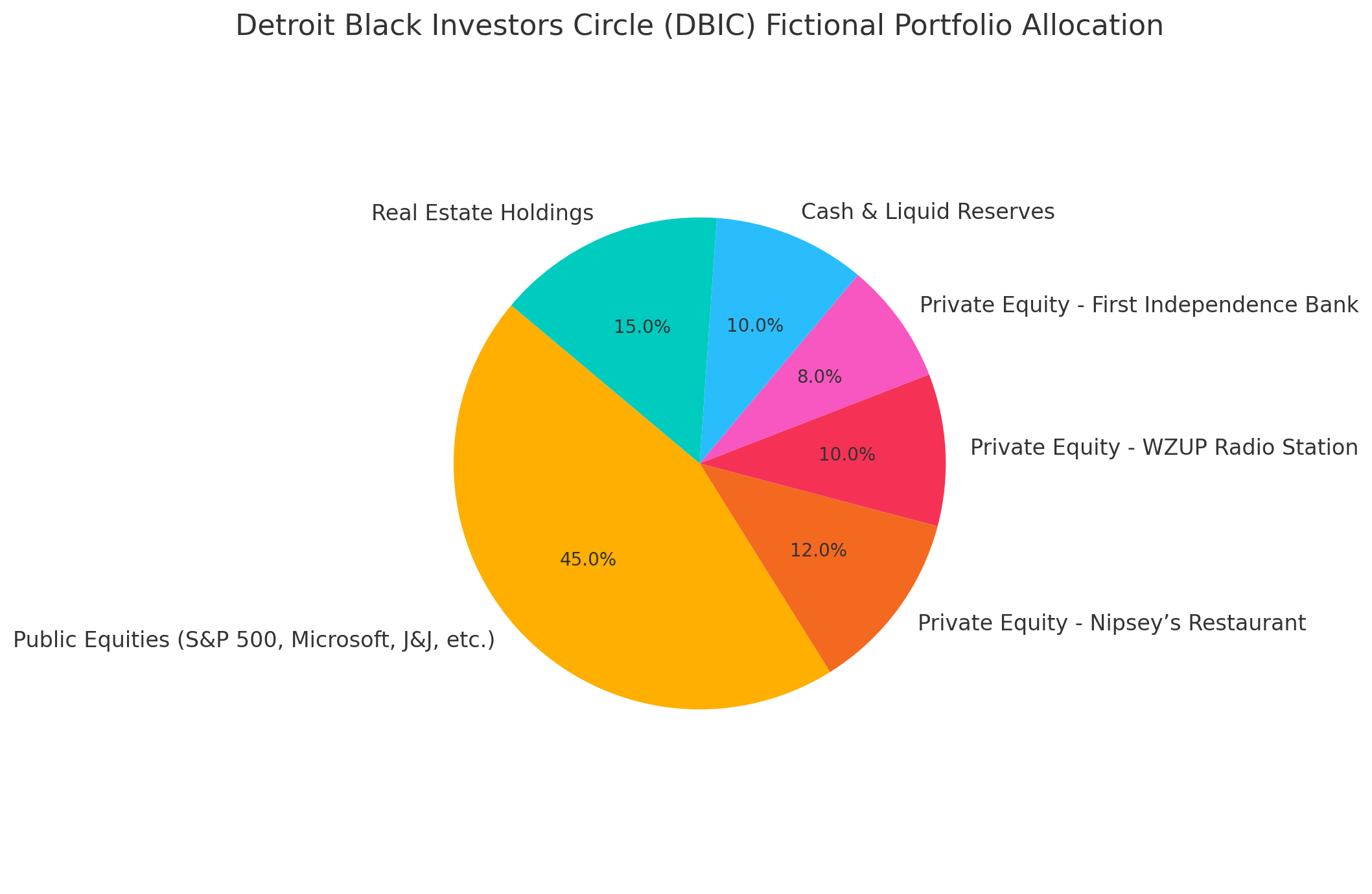

Let us construct the canon more precisely. Sometime in the early 1980s before Nipsey’s became the crew’s unofficial headquarters, before Martin’s radio career, before Cole had fully committed to being Cole — Tommy Strawn helped found the Detroit Black Investors Circle. Twelve members: working-class and middle-class Black men and women, some from his church, one a professor at Lewis College of Business, another a UPS driver with a subscription to Barron’s, another a beautician who had been tracking Coca-Cola’s dividend yield for years. They pooled contributions monthly, researched companies collectively, and invested with a long-term horizon. Their earliest positions were conservative: Johnson & Johnson in the mid-1980s, followed by Microsoft and Apple as the decade turned. Tommy, organised and methodical in ways his friends attributed to personality rather than purpose, was elected treasurer. His absence from the traditional labour market was not idleness. It was the logical outcome of a deliberate choice to treat intellectual capital and financial stewardship as his primary vocation.

The question of origins matters here, because the mythology of wealth-building in Black America too often presents the starting point as heroic or anomalous. It need not be either. Tommy’s seed capital, in this reconstruction, could have arrived through any number of entirely plausible channels. A financial aid refund from his time at Clark Atlanta or Southern University — the residual after Pell Grants and scholarships covered his tuition — deposited into a brokerage account rather than spent on spring break. A grandmother’s savings bonds and rolled currency discovered in an old armoire, pressed on Tommy because he was the responsible one, and treated not as a windfall but as seed capital. A church scholarship of $1,500 from an AME congregation, technically earmarked for tuition but freed up by other financial aid and redirected into three shares of Johnson & Johnson after a student-union speaker explained compound interest. A single tax refund of $1,200 — the same refund Martin and Gina would later squander — invested rather than consumed. None of these origins are dramatic. All of them are real. That is precisely the point.

What DBIC built over two decades was not merely a stock portfolio. It was a theory of institutional ownership, applied systematically to the infrastructure of Black Detroit. The club understood what too many investors of any background do not: that the most durable returns are not always the most legible ones, and that communities which fail to own the institutions embedded in their daily life are perpetually renting their own cultural and economic existence from someone else.

Nipsey’s was the first move. The bar-and-grill where Martin and the crew spent their evenings was also the informal civic centre of their block being part town square, part think tank, part après-work debrief. When its owner signalled, in the late 1990s, that he was considering selling to outsiders, DBIC moved with the precision of investors who had spent years watching their community’s assets change hands. They did not attempt to purchase the business outright. They structured a minority equity stake — thirty percent in exchange for capital improvements, point-of-sale infrastructure, and a customer loyalty programme. The back room became their biweekly boardroom. The arrangement was not charity. It was the conversion of social capital into ownership.

The acquisition of a stake in WZUP, the radio station operated by the chronically overstretched Stan Winters, was more consequential and more instructive about how Black institutional assets are lost. Stan had built something real: a Black-owned frequency with genuine audience loyalty and genuine cultural significance. What nearly destroyed it was not programming failure or audience attrition but an IRS liability of $20,000. Without intervention, WZUP would be sold to whoever came in with the highest bid. History, unrevised, confirms that fear: the station eventually became WEHA, a country and western outlet with no memory of what it had been.

In our revision, DBIC moved before that could happen. The conversation did not occur in a boardroom. It occurred at Nipsey’s, over cards, when Stan too proud to ask directly but too desperate not to signal let slip that the walls were closing in. Tommy listened. He returned to DBIC with a proposal whose logic was institutional rather than sentimental: this is not a struggling radio station, it is a platform, a frequency, a piece of Detroit’s Black cultural infrastructure that cannot be permitted to become country music (although do not be mistaken, African America listens to and perform that as well). The group structured a convertible note of $300,000: enough to retire the IRS debt, cover operational arrears, and fund a capital improvement plan. Stan retained full operational and creative control. DBIC received two advisory board seats and co-development rights on new revenue lines. If the note was repaid within five years, the arrangement dissolved cleanly. If it was not, it would convert to a forty percent equity stake.

What Stan did with that lifeline is where the story becomes genuinely instructive. WZUP expanded into online streaming at a moment when most Black-owned radio stations were treating the internet as a secondary concern. A Virginia State University engineering professor and Detroit native within the DBIC’s membership recruited to the club in 1997 pressed the case for early digital infrastructure with the same conviction the group applied to its equity selections. By the early 2000s, WZUP was streaming to Black Detroiters in Atlanta, Chicago, and Houston: people who had left the city but never stopped needing to hear home.

The second expansion was a Youth Podcast Incubator, constructed in deliberate partnership with HBCU communications and business programmes across the Midwest. The DBIC’s vision was regional from the start. Lewis College of Business, Detroit’s own HBCU, founded in 1928 by Violet T. Lewis and the only historically Black college in Michigan, served as the anchor institution. Chicago State University brought the Chicago market’s media energy into the pipeline. Central State University and Wilberforce University in Ohio, separated by fewer than ten miles in Greene County and together representing one of the most concentrated pockets of Black academic tradition in the country, completed a four-school corridor that no single institution could have anchored alone. Students from these campuses received studio time, mentorship from working journalists and broadcasters, and a direct pipeline to on-air opportunities. The strongest podcast properties would be co-owned between student creators and the WZUP multimedia umbrella, with DBIC and their respective HBCU’s endowment holding a minority stake in each new venture. This was talent development with equity implications, a structure that treated young Black media professionals not as beneficiaries but as future owners.

The third move was television. DBIC acquired a minority ownership stake in a UHF licence, partnered with a local public-access station for shared production facilities, and launched a local evening newscast staffed by journalists trained through the WZUP pipeline. It was underfunded by network standards and precisely right for what it was: a Black-owned, community-rooted media operation accountable to one zip code. When the convertible note period expired, Stan chose not to repay it. He wanted DBIC as permanent partners. The conversion happened on good terms. What had begun as a rescue had become something neither party had fully anticipated: a Black-owned multimedia company with a radio station at its core, a streaming footprint, a podcast network seeded by HBCU talent, and a local television operation — all of it rooted in one community and answerable to it.

The DBIC’s relationship with First Independence Bank, founded in Detroit in 1970 and one of only a handful of African American-owned banks in the country, followed a similar logic, applied to the most fundamental layer of capital infrastructure. As early as 1998, the group moved its operating accounts and investment reserves to First Independence, removing their dollars from institutions that had historically redlined the neighbourhoods DBIC members called home. In 2003, they went further. Using pooled capital from years of dividends and real estate returns, DBIC participated in a private placement offering from the bank — purchasing a tranche of equity not available on the open stock market. They were not simply depositors or well-wishers. They were owners, with a seat at the table where lending priorities, community reinvestment strategies, and product development were decided. That influence translated into a small-dollar business loan product specifically designed for African American entrepreneurs under thirty — the kind of accessible, low-barrier capital that national banks had never built for Black Detroit. Nipsey’s, fittingly, became the first business funded under the initiative. The loop closed precisely.

Lewis College of Business occupied a different register in the DBIC’s portfolio, one that illuminates the distinction between institutional philanthropy and institutional investment. Founded by Violet T. Lewis in 1928, the school had spent decades doing what chronically underfunded Black institutions always do: surviving on mission, loyalty, and insufficient material support. By the time DBIC had accumulated enough capital to think at an institutional scale, Lewis College was showing the accumulated strain of that equation. Enrollment was fragile. Its endowment was thin. The city it had served for generations had not reciprocated with anything resembling adequate financial commitment.

Tommy brought it to the DBIC not as a cause but as a calculation. Michigan’s only HBCU sat in their city, trained their people, and occupied a position in Detroit’s intellectual and professional life that could not be replaced once lost. The group directed a portion of its annual dividend income into an endowed scholarship fund for Lewis College business and communications students many of whom would eventually feed into the WZUP incubator. DBIC members attended board meetings, brokered introductions between Lewis alumni and the professional networks the club had built over two decades, and applied the same long-horizon discipline to the school that they applied to their stock selections. Not what does Lewis College need this year, but what does it need to still be standing in thirty years.

In this revision, that sustained commitment meant Lewis College never reached the financial crisis that in actual history cost it its accreditation. It did not close. It did not require rescue or rebranding to survive. Backed by DBIC capital and by the talent pipeline flowing through the Midwest HBCU corridor, it evolved on its own terms expanding into design and entrepreneurship, deepening its ties with Detroit’s creative and manufacturing industries, eventually becoming the institution now known as Pensole Lewis College of Business and Design. Not as a comeback story. As a continuum. The difference between an institution that transforms by choice and one that transforms by necessity is the difference between legacy and luck. DBIC gave Lewis College the conditions to choose.

The data against which this fiction is calibrated is not encouraging. According to HBCU Money’s 2025 analysis, only seven percent of Black households report receiving passive income of any kind from rental properties, interest, dividends, or business ownership compared to twenty-four percent of white households. Where such income exists in Black families, the median annual amount barely reaches $2,000, against nearly $5,000 for white households. This disparity is not incidental. It reflects generations of deliberate exclusion: redlined mortgage markets, brokerage firms that declined to serve Black neighbourhoods, financial institutions that systematically underfinanced Black-owned businesses and over-regulated them when they did. The passive income gap is, in this sense, the most accurate single measure of American wealth inequality, because it captures not just what people earn but how money multiplies or, for most Black households, how it does not.

The African American investment club tradition was never as invisible as mainstream culture suggested. By the late 1990s, the National Association of Investors Corporation estimated that nearly twenty percent of the nation’s investment clubs were predominantly African American groups meeting in church basements, barbershops, and community centres, pooling monthly contributions, researching blue-chip dividend payers, and building wealth in the precise manner that Tommy Strawn practiced in our reconstruction. These clubs rarely received national press coverage. Martin Payne certainly never depicted one. The cultural assumption that Tommy must be a hustler, not an investor, was partly the product of that invisibility — a vacuum in representation that the show’s writers, like most of their audience, had absorbed without question.

The institutional implication is straightforward. What DBIC practised informally can be formalised and scaled. An HBCU Investment Club Federation drawing alumni networks from Wiley, Spelman, Tuskegee, Livingstone, and the Midwest corridor institutions that anchored WZUP’s incubator could pool capital across institutions, invest jointly, and provide undergraduates in finance and business programmes with direct market exposure and mentorship. The strongest student-run clubs could evolve into intergenerational family investment vehicles or neighbourhood financial cooperatives. Black churches, fraternities and sororities, and civic organisations can serve as the social infrastructure around which these cooperatives are organised and sustained. Local and state governments can incentivise the model through tax credits or matched-savings programmes. Black-owned community development financial institutions — CDFIs — are just one of the natural custodians of the institutional capital these cooperatives accumulate.

African American buying power is projected to reach $2.1 trillion by 2026. The operative question is not how much Black America earns. It is how much it retains, multiplies, and institutionalises. Tommy Strawn’s silence at Nipsey’s was not passivity. It was the patience of someone who had made a different calculation and who understood that defending compound interest to people who couldn’t yet see it was less valuable than quietly demonstrating its results. The task now is to make that calculation visible, replicable, and structural. To build federations where DBIC built a single club. To establish HBCU incubators where WZUP built a single pipeline. To treat Black-owned banks not as gestures of solidarity but as instruments of capital allocation. To fund Lewis Colleges before they reach the edge, not after.

The next time somebody says ‘you ain’t got no job,’ the correct response may simply be a quarterly dividend statement. The Tommy Doctrine is not lore. It is a blueprint. The work is to make it logistics.

Disclaimer: This article was assisted by ClaudeAI.