“Even in death, we must ensure our community can continue to fight.” – William A. Foster, IV

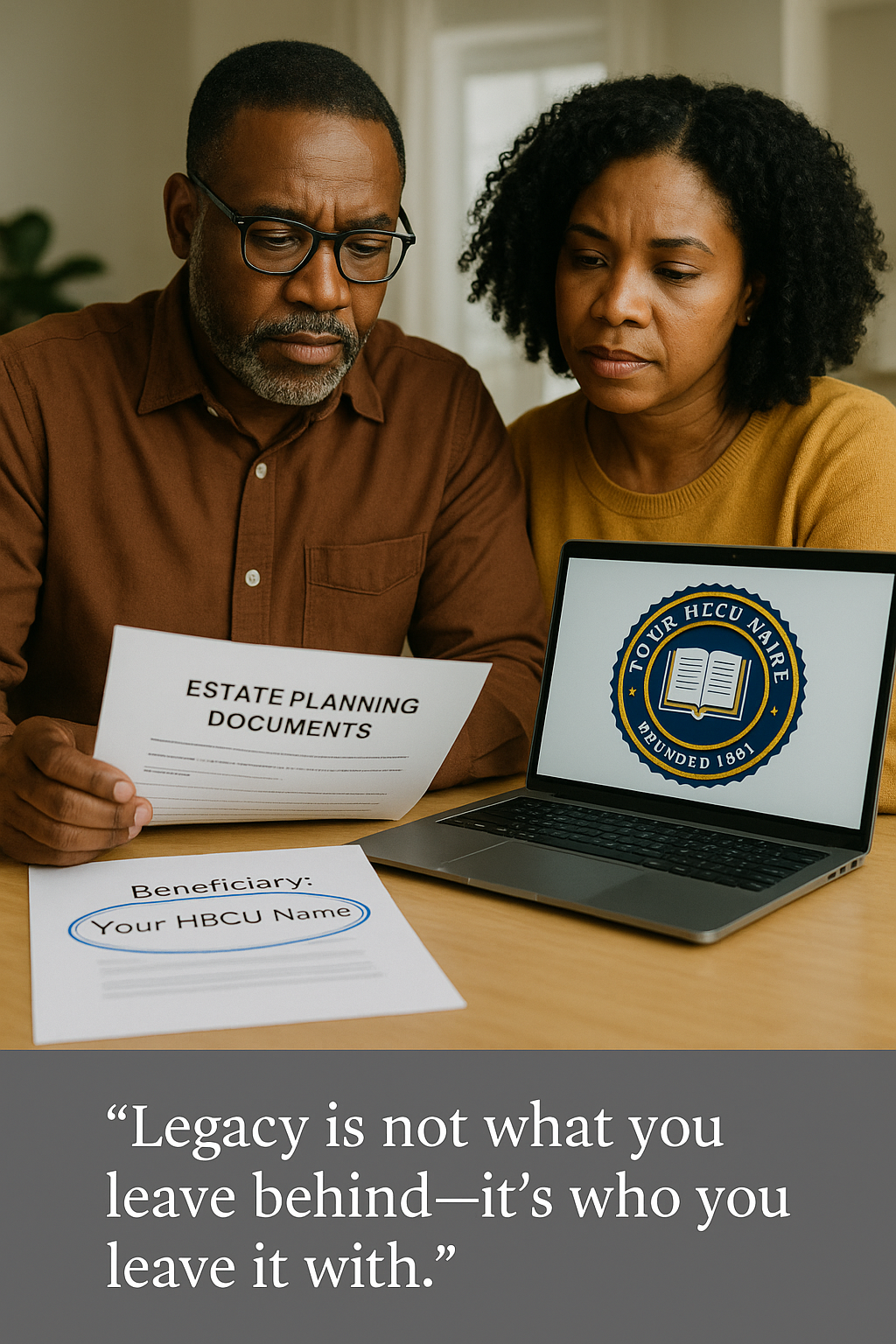

There is a sobering truth that rarely makes its way into alumni banquets or homecoming speeches: many Historically Black Colleges and Universities (HBCUs) are one generation away from crisis. Endowments remain modest, the donor base is limited, and institutional wealth gaps widen with each passing decade. Meanwhile, African American household wealth though fragile has produced a generation of professionals who, through homeownership, pensions, and insurance, collectively hold trillions in private assets. The question that must now be asked with urgency is not how much we love our HBCUs, but whether that love has been institutionalized. In simpler terms: Is your HBCU one of your beneficiaries? It should be.

African American baby boomers and Generation Xers are now entering the largest wealth transfer in U.S. history. Estimates from the Federal Reserve suggest that over the next 25 years, more than $70 trillion will be passed down across American households. African Americans represent a fraction of that figure, but even 2–3 percent of that total, between $1.4 trillion and $2.1 trillion is transformative if directed strategically. The reality is that most HBCUs will not receive a fraction of that wealth because too few alumni name their alma mater as beneficiaries in wills, trusts, or life insurance policies. For all of the love expressed through donations at homecoming, few alumni are ensuring that their HBCU benefits when they transition from life to legacy.

HBCUs collectively have endowments worth approximately $4 billion, compared to Harvard’s $51 billion or Stanford’s $40 billion. Even if just 10% of HBCU alumni left 5% of their estates to their alma mater, the resulting transfer of wealth could exceed $25 billion in one generation. That is not a pipe dream it is a matter of estate planning.

When most people think of beneficiaries, they think of family such as their children, spouses, grandchildren. This instinct is natural, but legacy is larger than lineage. It is institutional. Wealth without institutional roots evaporates within a generation. We see this across African America, where success stories emerge and vanish with each economic downturn because too few families and individuals tie their personal legacies to lasting institutions. In the European American tradition, universities, hospitals, museums, and foundations regularly appear in wills and trusts. These bequests sometimes modest, sometimes monumental form the lifeblood of institutional continuity. At elite private universities, as much as 40% of annual donations come from estate gifts. For most HBCUs, that figure hovers in the low single digits. That gap is not simply a reflection of wealth; it is a reflection of institutional habits. Too many African American professionals treat giving as an emotional act rather than a structural one. They give to help a student pay tuition, fund a scholarship, or support a campus event. These are vital acts of generosity. But they are also temporary. What our institutions need are permanent capital streams from assets that generate income long after we are gone.

According to a 2022 study by Caring.com, nearly 68% of African American adults do not have a will or estate plan. Among those who do, few include charitable or institutional beneficiaries. The absence of estate planning means that wealth is lost to legal battles, taxes, and disorganization. For HBCUs, it means that the most reliable source of long-term capital—planned giving—remains underdeveloped. The reasons are historical and psychological. Distrust of financial institutions, the trauma of asset seizure and land theft, and the lack of intergenerational financial literacy have all played a role. Many African Americans are the first in their families to accumulate significant assets and remain unsure how to manage or pass them on. HBCUs, too, have not always invested in the infrastructure to cultivate these conversations. Some institutions, such as Howard University and Spelman College, have begun to strengthen their planned giving offices, hiring estate planning specialists and partnering with financial advisors. Yet across the HBCU ecosystem, the field remains thin. Planned giving should not be treated as an auxiliary fundraising effort; it should be embedded in the financial literacy curriculum of every alumni association and business school.

Naming an HBCU as a beneficiary does not require immense wealth. It requires intention. A $10,000 life insurance policy that lists your alma mater as a secondary beneficiary could one day help fund a scholarship. A $25,000 bequest could seed an endowed fund that supports future students in perpetuity. Larger estates could create endowed chairs, faculty development funds, or campus infrastructure projects. For example, consider an alumnus with a $500,000 estate. If 5%—just $25,000 were left to their HBCU, and the school invested it with a conservative 7% annual return, the endowment could grow to nearly $50,000 within a decade. Now multiply that by 10,000 alumni. The cumulative impact becomes transformative: $250 million in new endowment capital. The beauty of estate gifts is that they align individual legacy with institutional longevity. They ensure that the values that shaped one’s life: education, perseverance, and community continue to bear fruit for generations.

Of course, the responsibility is not solely on alumni. HBCUs must meet their graduates halfway. Too often, the institutional conversation around giving begins and ends with short-term fundraising. Planned giving requires education, trust, and infrastructure. Alumni must understand not only how to give but also how their gifts will be managed. Transparency is critical. Each HBCU should maintain a planned giving office or partnership that offers free estate planning workshops for alumni and local communities, works with African American financial planners and attorneys to guide donors through the process, publishes an annual planned giving report showing bequests received and fund performance, and honors those who make such commitments through a “Legacy Society.” Planned giving is not a matter of charity; it is strategic finance. It represents patient capital the kind of long-term, compounding wealth that strengthens an institution’s ability to act with independence.

If an HBCU receives $1 million in bequests each year and invests it with an average annual return of 8%, while spending only 4% annually, the compounding effect over 30 years would result in an endowment of nearly $113 million. That is the quiet power of compound interest combined with institutional stewardship. The more predictable the inflow of legacy gifts, the more financial security an institution has to weather economic downturns, invest in research, and attract top faculty and students. This model has powered Ivy League universities for over a century. Harvard, Yale, and Princeton have each built massive endowments not solely through tuition or annual campaigns but through a continuous pipeline of planned gifts from alumni. The difference between those institutions and HBCUs is not love—it is legacy management.

Too many African American alumni equate love for their alma mater with nostalgia like football games, step shows, and reunions. But love that dies with you is sentiment; love that survives you is strategy. The graduates of HBCUs are living proof of what collective investment can produce. For every dollar given by alumni of the 1940s, 50s, and 60s, generations of students were educated. Yet, the torch cannot be passed if the flame is not fueled. It is time to evolve from a culture of giving back to one of building forward. Planned giving is not about death it is about continuity. It is a declaration that your life’s work and your alma mater’s mission are intertwined.

Every alumnus, regardless of income, can take simple steps today: create or update a will; name their HBCU as a beneficiary of an estate, policy, or specific asset; inform the institution of their intentions; encourage their peers to do the same; and hold their alma mater accountable for transparency. These steps are not just financial they are cultural. They shift African American giving from reactionary to generational.

Imagine if each graduating class pledged that 25% of its members would make their HBCU a beneficiary within ten years. Imagine alumni chapters hosting estate planning events as commonly as they host networking mixers. Imagine faculty and administrators participating themselves, modeling the behavior they encourage. Such a culture would redefine the financial destiny of HBCUs. Each homecoming would represent not just a reunion but an affirmation of generational continuity. Wealth, after all, is not built by what a people earn it is built by what they keep and institutionalize.

Estate giving is not simply a personal act it is a political and economic one. It is a means of resisting the structural forces that have kept African American institutions undercapitalized. It asserts that African America will no longer rely on external philanthropy to sustain its centers of knowledge and leadership. When an alumnus names their HBCU as a beneficiary, they are engaging in quiet revolution. They are transferring not just money, but sovereignty and the ability for African American institutions to define their futures without financial dependence.

HBCUs taught generations of African Americans how to think critically, build careers, and navigate a world that often excluded them. The final lesson those same institutions now teach is about reciprocity and permanence. To include your HBCU in your estate plan is to declare that the education you received was not just for you it was for those yet to come. It is to make your life an endowment for your people’s progress. As W.E.B. Du Bois once wrote, “Education must not simply teach work it must teach life.” The same can be said of giving. Philanthropy must not simply ease today it must ensure tomorrow.

So the next time you review your financial affairs, ask yourself one question: Is your HBCU one of your beneficiaries? If not, then perhaps it is time to make sure the love you feel for your alma mater doesn’t die when you do.

A Framework for Action

Every alumnus, regardless of income, can take the following steps today:

- Create or update your will. Even if your estate is modest, formalize it. This prevents unnecessary legal complications and ensures your intentions are respected.

- Name your HBCU as a beneficiary. This can be for a percentage of your estate, a specific asset, or a life insurance policy.

- Inform your institution. Let them know of your plans so that they can record and steward your legacy appropriately.

- Encourage your peers. Alumni networks should normalize estate planning as part of professional and family life.

- Hold your HBCU accountable. Ensure transparency in how planned gifts are invested and reported.

These steps are not just financial they are cultural. They shift African American giving from reactionary to generational.

Disclaimer: This article was assisted by ChatGPT.