“It was a wild year in many respects, but the stock market turned in a solid performance in 2021. Except for a few brief sell-offs, the S&P 500 gained 26.9% for the year. The Dow Jones Industrial Average (DJIA) gained 18.7% in 2021, while the Nasdaq Composite gained 21.4%.” – Forbes

Ariel Capital’s 2021 Black Investor Survey* continues to be a mixed bag of optimism and pessimism. Despite the increased engagement of investing among 401K plans, African Americans now only trail their European American counterparts by 20 basis points which is the closest it has ever been there is still significant struggle in the amount of capital invested. “For Black Americans, disparities grow every month; while they save $393 overall per month, whites are saving 76 percent more, at $693 per month. Even Black Americans who earn more than $100,000 a year consistently save or invest considerably less than their white counterparts at the same income level.” There are a number of factors at play, none more pronounced that with a community so impoverished that the likelihood that African Americans have to pull back on how much they invest even when their income is equal to their European American counterparts is typically attributable to how much African Americans are likely to have to help friends and family financially.

KEY HIGHLIGHTS:

- More than twice as many Black 401(k) plan participants (12% vs. 5%) borrowed money from their retirement accounts.

- Almost twice as many Black Americans (18% vs. 10%) dipped into an emergency fund.

- And 9% of Black Americans (vs. 4% of white Americans) say they asked their family or friends for financial support in 2020, while 18% of Black Americans and 13% of white Americans acknowledged giving financial support to family and friends last year.

- White 401(k) plan participants invest 26 percent more per month toward their retirement accounts than Black 401(k) plan participants ($291 vs. $231).

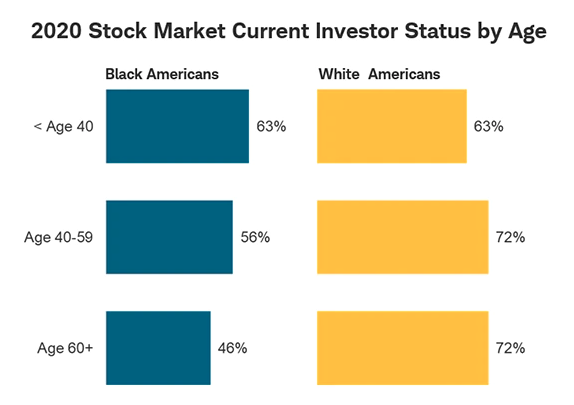

The conundrum that faces a great deal of African America is age. While the number of African Americans under 40 (see below) are participating on par with their European American counterparts, the hidden complexity there is older African Americans are not. This means that inheritances by the older demographics will continue to bolster younger European Americans and burden younger African Americans as the latter is more likely again to be burdened by immediate and extended financial issues even as they age. Carrie Schwab-Pomerantz, President of Charles Schwab Foundation, “notes that while 51% of white Americans say they have inherited wealth, just 23% of Black Americans have.” Once again, HBCUs have a critical role to play.

Getting African Americans to engage investing as early as possible in the 18-22 range is vital. This is because a primary way that younger African Americans as they age can buffer against the family burden is to have more money sooner and that is most easily accomplished through teenage/young adult investing. An added hedge to that is in IRAs where they can serve as an insurance policy of sorts given an investor is not supposed to access them until 59 1/2. Although we know we are more likely to due to our and our families’ financial situations. The problem of course is that we are not participating in IRAs (see below) anywhere near at the clip our counterparts are.

HBCUs and their alumni could be helping students open up Roth IRAs in particular. A 22-year old HBCU graduate with $6,000 in their IRA by graduation that never adds another penny and gets normal market returns would have almost $225,000 by age 60. This can be achieved by ensuring that any student participating in on-campus work study would automatically have a Roth IRA account opened for them, alumni could offer matching funds or just supporting funds into their accounts, etc. Again, the earlier they are invested the better. Should they achieve that $6,000 mark by age 20 and add nothing else it bolsters that $225,000 up to $271,000. This is the profound impact of earlier is more when it comes to compound investing.

For the full survey and analysis click here.

*About the survey

The online survey was conducted in December 2020 by Helical Research among 2,104 Americans age 18 and older with $50,000 or more household income in 2019. The margin of error for the total survey sample is two percentage points.