By William A. Foster, IV

Most everyone wants to do what’s fair, right, and good, but knowing what that is is often the tough part. – Malcolm Forbes

Recently, I was accused of being in support of slavery by the AFL-CIO’s chief economist in an exchange on Twitter for not supporting the minimum wage hike. Our discussion stemmed from my article on how a higher minimum wage would hurt African American small business growth capability. While other groups have many times our resources and wealth and since labor cost are the highest expense for any business I was simply pointing out that as a group having limited resources and higher expenses would make it harder for us to start businesses. This compounds a problem of wealth creation through business ownership and favorable taxes for ownership with employment, since businesses tend to hire within their own community, especially small businesses. By the end of the exchange he resorted to telling me I was only concerned about racism and not slavery. Oddly, I thought we were having a conversation about the minimum wage, not about racism or slavery. I sympathize with his position, but let us not throw the baby out with the bath water.

In a more macro example of why I think a blanket minimum wage hike is a problem is based on business size. Home Depot has a market cap of $110 billion, annual revenues of almost $80 billion, profits of $5 billion, and 300 000 employees of which the vast majority are paid minimum wage or close to it. In comparison, around two-thirds of small businesses, the SBA defines a small business as 500 or less employees, generate less than 100 000 annually in revenue and 88 percent of small businesses have 20 employees or less. Are we to treat these small businesses with the same stick as Home Depot and other national retailers? To bump the minimum wage up on a business with a 20 hour a week worker adds almost $2 800 annually to the cost per worker, which is no small bump to businesses making only 100 000 or less annually in revenue. However, make no mistake the SBA’s definition of a small business does propose a bit of a problem.

Enter asset and capital firms. Hedge funds, private equity, and other asset and capital firms are notoriously small. Appaloosa Management, David Tepper’s firm, reportedly only has 32 employees. Obviously, this qualifies them as a “small” business according to the SBA’s definition. The problem as it were, David Tepper himself made $2.2 billion in earnings through his hedge fund in 2012. A firm which had $25 billion in assets under management in 2012. Why is this problem? Because someone is cleaning Appaloosa’s offices. More than likely the work is contracted out and more than likely that person doing the cleaning is being paid minimum wage to do so – if that. So as you see just defining a business as “small” by its employees can leave a number of loopholes. If you have not been able to tell by the conundrums around the Affordable Care Act, businesses definitely will look for the loopholes to save money.

A better solution to the minimum wage is a progressive wage in the same way the United States has a progressive tax rate. As companies grow revenues, then so should their minimum wage requirement. Even this though is no small cost, even to big companies. If all of Home Depot’s 300 000 employees, of course not all are minimum wage earners, received a $2.85 bump in pay for every 20 hours per week they worked it would equate to an $820 million dollar increase in labor expense or 16 percent of the companies net income. This increase would be passed along to customers which is usually the case when business expenses rise anyway. I would not dare call for a lowering of the minimum wage at small businesses with smaller revenues, but it could be justified if burden were evenly spread out across a simple revenue and net income calculation. This would still raise the overall minimum wage without harming those small businesses at the very bottom trying to grow. It would also require the aforementioned firms like capital firms to ensure any contracted work they pay meets a minimum wage. For instance, if a hedge fund is contracting out its janitorial work and the employer is paying $7.25 a hour to the janitor, then the hedge fund would be responsible for the other $2.85 or whatever range that particular firm falls in based on the progressive minimum wage. This ensures the actual small business based on revenue is not bearing the burden of the higher labor cost.

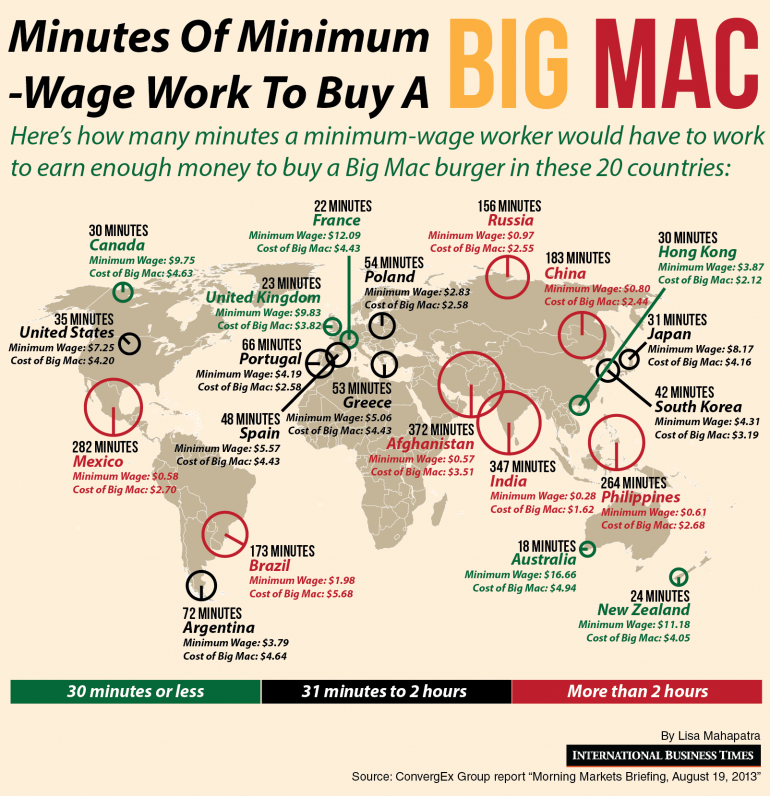

The populous argument would say 16 percent is no big deal, but most populous arguments have rarely been business owners or investors. They do not take into account capital flight and other things that potentially could cause capital to flee from these companies. This is a problem if your 401(K) happens to have investments in one of these companies, which most often they do. There goes retirement, but at least I can buy that Big Mac today (see below). The high cost of labor is what set auto companies in the United States back as they struggled to compete against foreign manufacturers who could produce the same quality car for a much cheaper price. Save for a government bailout, all of those jobs would be gone today in a true capitalist system or free market economy. Again, be careful what you wish for.

However, one of the things that could be done to offset income disparity is to give companies who are active in managing the ratio between their lowest earning full-time worker and total CEO compensation based on a five year rolling average could receive special tax breaks. The latter is important for those companies who love to give obscene golden parachutes to outgoing CEOs, which often leaves investors just as frustrated as employees. I am by no means in favor of capping anyone’s compensation, but I do believe that maintaining a proper balance between maximum-minimum is important to the overall health of businesses, labor, and the economy. Currently, the ratio between CEO compensation and the average worker of a S&P 500 company is 354:1 according to a recent report by the AFL-CIO. In 1981, the ratio was closer to 40:1 (see below).

Unfortunately we exist in a social, economic, and political climate in America currently that everything exist in extremes. The answer in the middle could restore balance, but it would take the belief that there is an actual win-win scenario for both parties also known as compromise. If we do not tax someone who makes millions the same as someone who makes thousands, then why can not the same logic be applied to businesses? Hopefully, we can find moderation because we knows what happens to a boat that leans too much to one side. Now, where did I put my life preserver?