By William A. Foster, IV

Yesterday is a cancelled check. Today is cash on the line. Tomorrow is a promissory note. – Hank Stram

![]()

My entrepreneurship teacher in b-school was a man who grew up in the depression, was stubbornly frugal, and had LBO’d, run, and sold two companies before taking up teaching. He talked about how the depression impacted him personally (he still drove a late 80′s Acura and bought a used sailboat despite having a net worth near nine figures) and his approach to business. In class he seemed to start off every single class and every case study with the same message on the board. Cash is king. He even went so far as to say that cash was oxygen and the moment a business did not have it, that business was dead. He abhored companies (or students) who suggested that companies should pay down debt ahead of schedule unless there were obscenely excessive cash reserves. Paying ahead on debt for a company and draining its cash reserves to do so was not only foolish but dangerous. As he said you do not get any brownie points from creditors for being ahead but you do endanger your business if an emergency arose or opportunity for that matter. But what about a company that has no debt and sits on the Mount Rushmore of cash? Enter Apple.

Apple, Inc. has no debt and currently sits on $137 billion in cash and cash equivalents and they are being criticized for it. David Einhorn, an “activist” investor in Apple, who is cogently trying to convince Apple that it needs to release its mountain pile of cash back to investors. He has gone so far as to say that Apple is behaving with a depression-like mentality. Apparently, Mr. Einhorn has short-term memory loss. It was not even five years ago when companies were begging for life lines to cash. I am sure the former Lehman Brothers and Bear Stearns had wished they were sitting on a fraction of the cash Apple is currently holding. Let me not just pick on the banks as we saw Circuit City and 70 year old iconic retailer Mervyn’s go out of business in 2008. It just so happened that the only company willing to lend any cash was Warren Buffett’s Berkshire Hathaway which is not even a bank. In fact, Berkshire Hathaway lent money to two notable banks in Bank of America and Goldman “Teflon” Sachs. In return, Berkshire has received handsome returns in a current investing environment where others are better off standing on the side of the road panhandling to get returns on investments. Berkshire Hathaway’s cash pile was not only able to provide shelter to its stable of companies but Berkshire’s cash infusion into a troubled market was able to bring some level of calm to the global markets that was quickly deteriorating into pure chaos as liquidity had dried up faster than the Sahara desert on Mercury. Yes, it was that bad. Mr. Einhorn says that the money needs to be returned to shareholders because it is shareholders who can put that cash to better use.

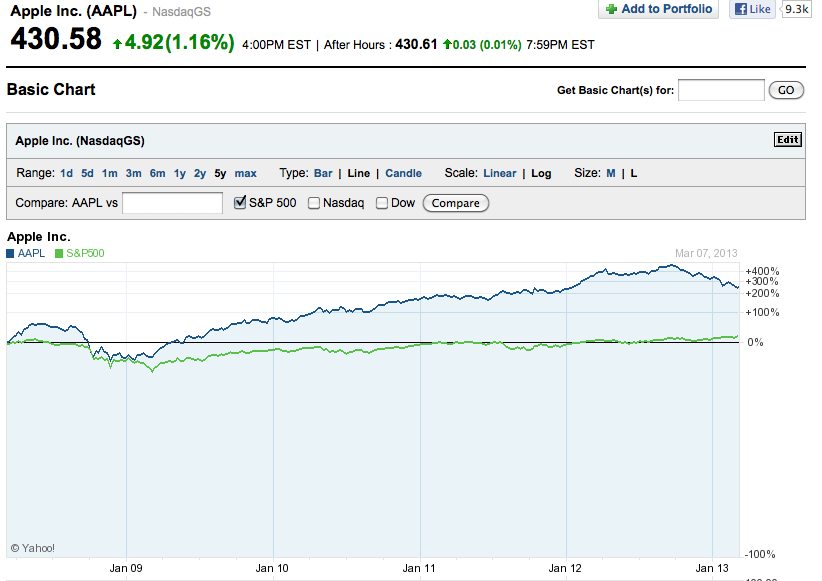

Now Mr. Einhorn, exactly where are investors going to go with this cash other than back into Apple? We are in a negative interest rate environment currently and from all impressions of Federal Reserve Chairman Bernanke posturing – not leaving it anytime soon. One has to wonder if Bernanke could find a missile to push real rates even lower he will. A look at the graph below shows just how futile it could be chasing new investments. We know fixed income is dead but over the past five years since the Great Recession the S&P 500 (even with Apple in it) overall has returned almost a 0 percent return while Apple is closing in on 300 percent over the same period. The argument that they do not need “that much” cash is almost as fun of a ponderance as asking someone “how much money is too much?” and expecting any consensus to occur in a group of more than one.

That is just the investment side of it. There is another real reality of this. Apple needs to be transforming itself into more than a company that makes the IPhone because like all things eventually it too will fade and then what? The television? The watch? This company has the ability to do something truly transformative with the cash that Mr. Einhorn so abhors. Apple can take a cue from an old rival IBM and become a technology and consulting company thereby adding and creating a diversified revenue stream to reduce the angst around so much of Apple’s revenue being based solely on one or two products. What Apple chooses to consult in should be an assessment of its managers of where the company has strengths and competitive advantages. Or it can hope the IPhone/IPad 40 will still be popular in a decade even though we know how that turned out for IBM. Yes, at one point IBM “Big Blue” made personal computers too. The company also went from one of the most profitable in the world in 1990 with $6 billion in profits to the brink of bankruptcy in 1993. Why? Because Microsoft, Dell, and others were changing the industry underneath its behemoth feet as young, energetic, and nimble companies something IBM was unable to respond to with its size, age, and bureaucracy that comes with a maturing company. It is now considered a multinational technology and consulting company and this ultimately will be the route Apple will have to take. A transition like this will take time and cash. Lots of it. There is no reason for Apple to have the same fate unless pushed by shareholders who want to join Mr. Einhorn’s short term amnesia of 2008 or forget the lessons of IBM’s near collapse taught us 20 years ago.

It appears Mr. Einhorn and much of the investment community today who are seeking yield in such an onerous investing climate have already forgotten the lessons of yesteryear. Not to mention an American political climate where Democrats and Republicans are acting as if they at best are engaged in a remnant of the Cold War and possibly moving closer to that of the Vietnam conflict as the country tries to get its financial house in order. The herd mentality that so often plagues the investment community’s inability to dare to be contrarian. Unfortunately, few managers of public companies today have the sense to not succumb to the perils of the 90 day cycle also known as quarterly earnings and instead focus on managing a company with the vision of tomorrow’s tomorrow in mind. Apple should do what it does best and what allowed it to come from the brink of irrelevance to one of the world’s most valuable company – “Think Different”. Yes, cash is king and Apple is indeed currently God – but as mythology taught us even gods can be killed.

Disclaimer: There is no ownership of any of the companies mentioned in this article by myself, my business, or my family as of this article’s publishing.